Biodiversity risks scoring: a quantitative approach

October 2024

9 min read

Authors:

Marije Wiersma, Sjoerd Blijlevens, Miguel Manzanares

Share:

Explore how Zanders’ scoring methodology quantifies biodiversity risks, enabling financial institutions to safeguard portfolios from environmental and transition impacts.

Addressing biodiversity (loss) is not only relevant from an impact perspective; it is also quickly becoming a necessity for financial institutions to safeguard their portfolios against financial risks stemming from habitat destruction, deforestation, invasive species and/or diseases.

In a previous article, published in November 2023, Zanders introduced the concept of biodiversity risks, explained how it can pose a risk for financial institutions, and discussed the expectations from regulators.1 In addition, we touched upon our initial ideas to introduce biodiversity risks in the risk management framework. One of the suggestions was for financial institutions to start assessing the materiality of biodiversity risk, for example by classifying exposures based on sector or location. In this article, we describe Zanders’ approach for classifying biodiversity risks in more detail. More specifically, we explore the concepts behind the assessment of biodiversity risks, and we present key insights into methodologies for classifying the impact of biodiversity risks; including a use case.

Understanding biodiversity risks

Biodiversity risks can be related to physical risk and/or transition risk events. Biodiversity physical risks results from environmental decay, either event-driven or resulting from longer-term patterns. Biodiversity transition risks results from developments aimed at preventing or restoring damage to nature. These risks are driven by impacts and dependencies that an undertaking has on natural resources and ecosystem services. The definition of impacts and dependencies and its relation to physical and transitional risks is explained below:

Companies impact natural assets through their business operations and output. For example, the production process of an oil company in a biodiversity sensitive area could lead to biodiversity loss. Impacts are mainly related to transition risk as sectors and economic activities that have a strong negative impact on environmental factors are likely to be the first affected by a change in policies, legal charges, or market changes related to preventing or restoring damage to nature.

On the other hand, companies are dependent on certain ecosystem services. For example, agricultural companies are dependent on ecosystem services such as water and pollination. Dependencies are mainly related to physical risk as companies with a high dependency will take the biggest hit from a disruption or decay of the ecosystem service caused by e.g. an oil spill or pests.

For banks, the impacts and dependencies of their own operations and of their counterparties can impact traditional financial (credit, liquidity, and market) and non-financial (operational and business) risks. In our biodiversity classification methodology, we assess both impacts and dependencies as indicators for physical and transition risk. This is further described in the next section.

Zanders’ biodiversity classification methodology

An important starting point for climate-related and environmental (C&E) risk management is the risk identification and materiality assessment. For C&E risks, and biodiversity in particular, obtaining data is a challenge. A quantitative assessment of materiality is therefore difficult to achieve. To address this, Zanders has developed a data driven classification methodology. By classifying the biodiversity impact and dependencies of exposures based on the sector and location of the counterparty, scores that quantify the portfolio’s physical and transition risks related to biodiversity are calculated. These scores are based on the databases of Exploring Natural Capital Opportunities, Risks and Exposure (ENCORE) and the World Wide Fund for Nature (WWF).

Sector classification

The sector classification methodology is developed based on the ENCORE database. ENCORE is a public database that is recognized by global initiatives such as Taskforce on Nature-related Financial Disclosures (TNFD) and Partnership for Biodiversity Accounting Financials (PBAF). ENCORE is a key tool for the “Evaluate” phase of the TNFD LEAP approach (Locate, Evaluate, Assess and Prepare).

ENCORE was developed specifically for financial institutions with the goal to assist them in performing a high-level but data-driven scan of their exposures’ impacts and dependencies. The scanning is made across multiple dimensions of the ecosystem, including biodiversity-related environmental drivers. ENCORE evaluates the potential reliance on ecosystem services2 and the changes of impacts drivers3 on natural capital assets4. It does so by assigning scores to different levels of a sector classification (sector, subindustry and production process). These scores are assigned for 11 impact drivers and 21 ecosystem services. ENCORE provides a score ranging from Very Low to Very High for a broad range of production processes, sub-sectors and sectors.

To compute the sector scores, ENCORE does not offer a methodology for aggregating scores for impacts drivers and ecosystem services. Therefore, ENCORE does not provide an overall dependency and impact per sector, sub-industry, or production process. However, Zanders has created a methodology to calculate a final aggregated impact and dependency score. The result of this aggregation is a single impact and a single dependency score for each ENCORE sector, sub-industry or production process. In addition, an overall impacts and dependencies scores are computed for the portfolio, based on its sector distribution. In both cases, scores range from 0 (no impact/dependency) to 5 (very high impact or dependency).

Location classification

The location scoring methodology is developed based on the WWF Biodiversity Risk Filter (hereafter called WWF BRF).5 The WWF BRF is a public tool that supports a location-specific analysis of physical- and transition-related biodiversity risks.

The WWF BRF consists of a set of 33 biodiversity indicators: 20 related to physical risks and 13 related to reputational risks, which are provided at country, but also on a more granular regional level. These indicators are aggregated by the tool itself, which ultimately provides one single scape physical risk and scape reputational risk per location.

To compute overall location scores, the WWF BRF does not offer a methodology for aggregating scores for countries and determine the overall transition risk (based on the scape reputational risk scores) and physical risk (based on the scape physical risk scores). However, Zanders has created a methodology to calculate a final aggregated transition and physical risk score for the portfolio, based on its geographical distribution. The result of this aggregation is a single transition and physical risk score for the portfolio, ranging from 0 (no risk) to 5 (very high risk).

Use case: RI&MA for biodiversity risks in a bank portfolio

In this section, we present a use case of classifying biodiversity risks for the portfolio of a fictional financial institution, using the sector and location scoring methodologies developed by Zanders.

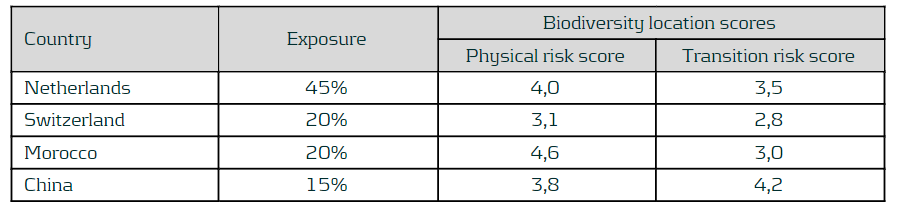

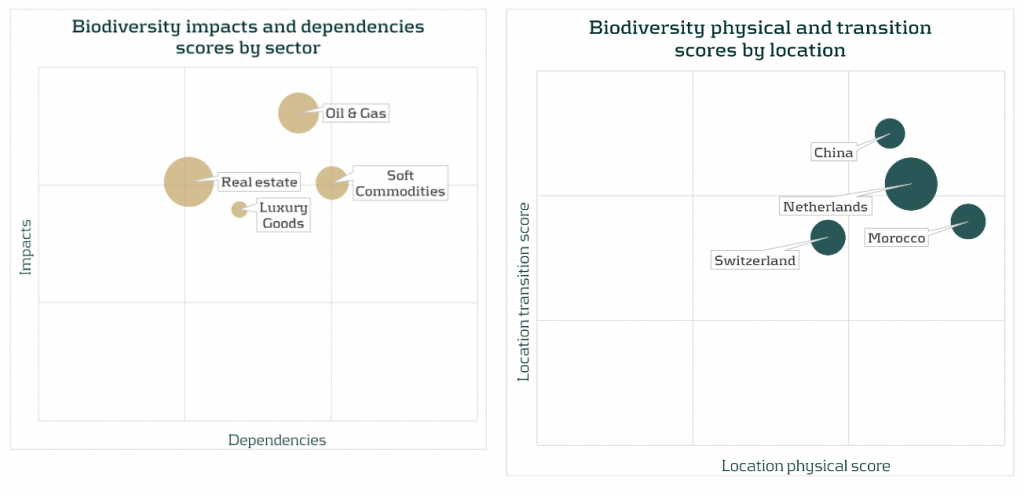

The exposures of this financial institution are concentrated in four sectors: Real estate, Oil & Gas, Soft commodities and Luxury goods. Moreover, the operations of these sectors are located across four different countries: the Netherlands, Switzerland, Morocco and China. The following matrix shows the percentage of exposures of the financial institution for each combination of sector and country:

ENCORE provides scores for 11 ecosystem services and 21 impacts drivers. Those related to biodiversity risks are transformed to a range from 0 to 5. After that, biodiversity ecosystem services and biodiversity impacts drivers are aggregated into an overall biodiversity impacts and dependencies scores, respectively. The following table shows the mapping between the sectors in the portfolio and the corresponding sub-industry in the ENCORE database, including the aggregated biodiversity impacts and dependencies scores computed for those sub-industries. The mapping is done at sub-industry level, since it is the level of granularity of the ENCORE sector classification that better fits the sectors defined in the fictional portfolio. In addition, the overall impacts and dependencies scores are computed, by taking the weighted average sized by the sector distribution of the portfolio. This leads to scores of 3.8 and 2.4 for the impacts and dependencies scores, respectively.

The WWF BRF provides biodiversity indicators at country level. It already provides an aggregated score for physical risk (namely, scape physical score) and for transition risk (namely, scape reputational risk score), so no further aggregation is needed. Therefore, the corresponding scores for the four countries within the bank portfolio are selected. As the last step, the location scores are transformed to a range similar to the sector scores, i.e., from 0 (no physical/transition risk) to 5 (very high physical/transition risk). The results are shown in the following table. In addition, the overall impacts and dependencies scores are computed, by taking the weighted average sized by the geographical distribution of the portfolio. This leads to scores of 3.9 and 3.3 for the physical and transition risk scores, respectively.

Results of the sector and location scores can be displayed for a better understanding and to enable comparison between sectors and countries. Bubble charts, such as the ones show below, present the sectors and location scores together with the size of the exposures in the portfolio (by the size of each bubble).

Combined with the size of the exposures, the results suggest that biodiversity-related physical and transition risks could result in financial risks for Soft commodities and Oil & Gas. This is due to high impacts and dependencies and their relevant size in the portfolio. Moreover, despite a low dependencies score, biodiversity risks could also impact the Real estate sector due to a combination of its high impact score and the high sector concentration (45% of the portfolio). From a location perspective, exposures located in China could face high biodiversity transition risks, while exposures located in Morocco are the most vulnerable to biodiversity physical risks. In addition, relatively high scores for both physical and transition risk scores for Netherlands, combined with the large size of these exposures in the portfolio, could also lead to additional financial risk.’

These results, combined with other information such as loan maturities, identified transmission channels, or expert inputs, can be used to inform the materiality of biodiversity risks.

Conclusion

Assessing the materiality of biodiversity risks is crucial for financial institutions in order to understand the risks and opportunities in their loan portfolios. In this article, Zanders has presented its approach for an initial quantification of biodiversity risks. Curious to learn how Zanders can support your financial institutions with the identification and quantification of biodiversity risks and the integration into the risk frameworks? Please reach out to Marije Wiersma, Iryna Fedenko or Miguel Manzanares.

In accordance with ENCORE, ecosystem services are the links between nature and business. Each of these services represent a benefit that nature provides to enable or facilitate business production processes. ↩︎

In accordance with ENCORE AND Natural Capital Protocol (2016), an impacts driver is a measurable quantity of a natural resource that is used as an input to production or a measurable non-product output of business activity. ↩︎

In accordance with ENCORE, natural capital assets are specific elements within nature that provide the goods and services that the economy depends on. ↩︎

The WWF also provides a similar tool, the WWF Water Risk Filter, which could be used as to assess specific water-related environmental risks. ↩︎

On Thursday 15 June 2023, Zanders hosted a roundtable on ‘Climate Scenario Design & Stress Testing’. This article discusses our view on the topic and highlights key insights from the roundtable.

On Thursday 15 June 2023, Zanders hosted a roundtable on ‘Climate Scenario Design & Stress Testing’. In our head office in Utrecht, we welcomed risk managers from several Dutch banks. This article discusses our view on the topic and highlights key insights from the roundtable.

In recent years, many banks took their first steps in the integration of climate and environmental (C&E) risks into their risk management frameworks. The initial work on climate-related risk modeling often took the form of scenario analysis and stress testing. For example, as part of the Internal Capital Adequacy Assessment Process (ICAAP) or by participating in the 2022 Climate Stress Test by the European Central Bank (ECB). To comply with the ECB’s expectations on C&E risks, banks are actively exploring methodologies and data sources for adequate climate scenario design and stress testing. The ECB requires that banks will meet their expectations on this topic by 31 December 2024.

Our view

We believe that banks should start early with climate stress testing, but in a manageable and pragmatic way. Banks can then improve their methodologies and extend their scope over time. This allows for a gradual development of knowledge, data and methodologies within all relevant Risk teams. Zanders has identified the following steps in the process of climate scenario design and stress testing:

Step 1: Scenario selection A bank has to select appropriate (climate) scenarios based on the bank’s climate risk materiality assessment. Important to consider in this phase is the purpose for which the scenarios will be used, whether the scenarios are in line with scientific pathways, and whether they account for different policy outcomes (like an early or late transition to a sustainable economy).

Step 2: Scope and variable definition An appropriate scope must then be selected and appropriate variables defined. For example, banks need to determine which portfolios to take in scope, which time horizons to include, select the granularity of the output, the right level of stress, and which climate- and macro-economic variables to consider.

Step 3: Methodology Then, the bank needs to develop methodologies to calculate the impact of the scenarios. There are no one-size-fits-all approaches and often a combination of different qualitative and quantitative methodologies is needed. We recommend that the climate stress test approach be initially simple and to focus on material exposures.

Step 4: Results It is important to use the results of the scenario analysis in the relevant risk and business processes. The results can be used for the bank’s risk appetite and strategy. The results can also help to create awareness and understanding among internal stakeholders, and support external disclosures and compliance.

Step 5: Stress testing framework Finally, banks should establish minimum standards for climate scenario design and stress testing. This framework should include, amongst others, policies and processes for data collection from different sources, how adequate knowledge and resources are ensured, and how the scenarios are kept up-to-date with the latest market developments.

Key insights

Prior to the roundtable, participants filled in a survey related to the progress, scope and challenges on climate risk stress testing. The key insights presented below are based on the results of this survey, together with the outcomes of the discussion thereafter.

The financial sector has advanced with several aspects around integrating climate risks in risk management over the past year. This was recognized by all participants, as they had all performed some form of climate risk stress testing. The scope of the stress testing, however, was relatively limited in some cases. For example, all participants considered credit risk in their climate risk scenario with many also including market risk. Only a limited number of participants took other risk types into account.

Furthermore, all participants assessed the short-term impact (up to 3 years) of the climate scenarios, whereas only around 40% and 10% assessed the impact on the medium term (3 to 10 years) and long term (>10 years), respectively. This is probably related to the fact that all participants used climate scenarios in their ICAAP, which typically covers a three-year horizon. The second most mentioned use for the climate scenarios, after the ICAAP, was the risk identification & materiality analysis. A smaller percentage of participants also used the climate scenarios for business strategy setting, ILAAP and portfolio management.

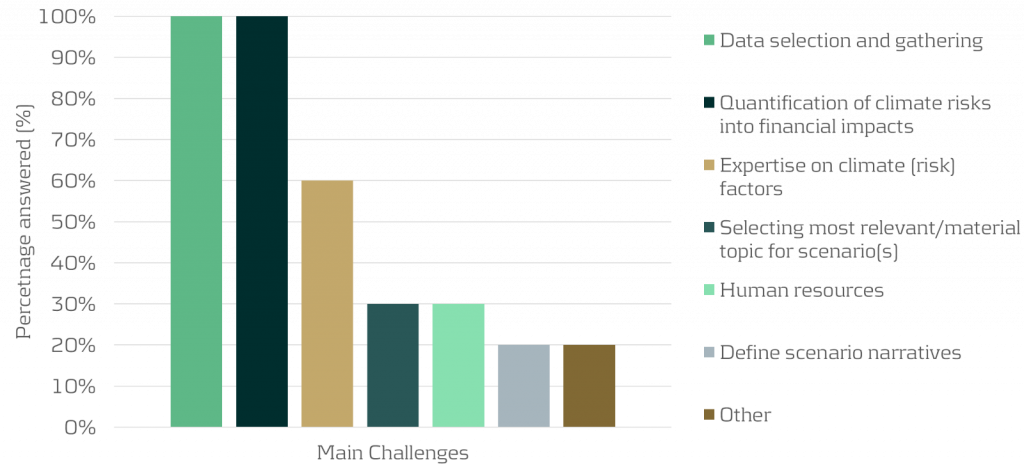

The two topics that were unanimously mentioned as the main challenges in climate risk stress testing are data selection and gathering, and the quantification of climate risks into financial impacts, as shown in the graph below:

Insight 1: Assessing impact of climate risk beyond the short-term very much increases the complexity and uncertainty of the exercise The participants indicated that climate stress testing beyond the short-term horizon (beyond 3 to 5 years) is very difficult. Beyond that horizon, the complexity of the (climate) scenarios increases materially due to uncertainties of clients’ transition plans, the bank’s own transition plan and climate strategy (e.g., related to pricing and client acceptance policies), and climate policies and actions from governments and regulators. Taking the transition plans of clients into account on a granular level is especially difficult when there is a large number of counterparties. There are no clear solutions to this. Some ideas that take longer-term effects into account were floated, such as adjusting the current valuation of various assets by translating future climate impact on assets into a net present value of impact or by taking climate impacts into account in the long-term macro-economic scenarios of IFRS9 models.

Insight 2: Whether to use a top-down or bottom-up approach depends on the circumstances It was discussed whether a bottom-up stress test for climate scenarios is preferable to a top-down stress test. The consensus was that this depends on the circumstances, for example:

Physical risks are asset- and location-specific; one street may flood but not the next. So, in that case a bottom-up assessment may be necessary for a more granular approach. On the other hand, for transition risks, less granularity might be sufficient as transition policies are defined on national or even supranational level, and trends and developments often materialize on sector-level. In those cases, a top-down type of analysis could be sufficient.

If the climate stress test is used to get a general overview of where risks are concentrated, a top-down analysis may be appropriate. However, if it is used to steer clients, a more granular, bottom-up approach may be needed.

A bottom-up approach could also be more suitable for longer-term scenarios as it allows to include counterparty-specific transition plans. For more short-term scenarios, a sector average may be sufficient, considering that there will be less transition during this period.

Insight 3: Translating the results of climate risk stress testing into concrete actions is challenging The results of the stress test can be used to further integrate climate risk into risk management processes such as materiality assessment, risk appetite, pricing, and client acceptance. Most participants, however, were still hesitant to link any binding actions to the results, such as setting risk limits (e.g., limiting exposures to a certain sector), adjusting client acceptance, or amending pricing policies. However, the ECB does require banks to consider climate impacts in these processes. The most mentioned uses of the climate risk stress testing results were risk identification & materiality assessments and risk monitoring.

Conclusion

Most banks have taken first steps in relation to climate scenario design and stress testing. However, many challenges still remain, for example around data selection and quantification methodologies. Efforts by banks, regulators and the market in general are required to overcome these challenges.

Zanders has already supported several banks with climate scenario design and stress testing. This includes the creation of a climate scenario design framework, the definition of climate scenarios, and by quantifying climate risk impacts for the ICAAP. Next to that, we have performed research on modeling approaches that can be used to quantify the impact of transition and physical risks. If you are interested to know how we can help your organization with this, please reach out to Marije Wiersma.

Are climate change risks properly captured in the prudential framework?

February 2023

3 min read

Author:

Sjoerd Blijlevens

Share:

In March 2021, the European Banking Authority (EBA) was mandated through Article 501c of the Capital Requirements Regulation (CRR) to “assess […] whether a dedicated prudential treatment of exposures related to assets or activities associated substantially with environmental and/or social objectives would be justified”.

More simply put, the EBA was asked to investigate whether the current prudential framework properly captures environmental and social risks. In response, the EBA published a Discussion Paper (DP) [1] in May 2022 to collect input from stakeholders such as academia and banking professionals.

After briefly presenting the DP, this article reviews the current Pillar 1 Capital (P1C) requirements. We limit ourselves to the P1C requirements for credit risk as this is by far the largest risk type for banks. Furthermore, we only discuss the interaction of the P1C with climate change risks (as opposed to broader environmental and/or social risk types). After establishing the extent to which the prudential framework takes climate change risks into account, possible amendments to the framework will be considered.

Key take-aways of this article:

The current prudential framework includes several mechanisms that allow the reflection of climate change risks into the P1C.

The interaction between P1C and climate change risks is limited to specific parts of the portfolio, and in those cases, it remains to be seen to what extent this is properly accounted for at the moment.

Amendments to the prudential framework can be considered, but it is important to avoid double counting issues and to take into account differences in time horizons.

The EBA is expected to publish a final report on the prudential treatment of environmental risks in the first half of this year.

Financial institutions that are using the internal ratings-based approach are advised to start with the incorporation of climate change risks into PD and LGD models.

EBA’s Discussion Paper

In the introduction of the DP, the EBA mentions the increasing environmental risks – and their interaction with the traditional risk types – as the trigger for the review of the prudential framework. One of the main concerns is whether the current framework is sufficiently capturing the impact of transition risks and the more frequent and severe physical risks expected in the coming decades. In this context, they stress the special characteristics of environmental risks: compared to the traditional risk types, environmental risks tend to have a “multidimensional, non-linear, uncertain and forward-looking nature.”

The EBA also explains that the P1C requirements are not intended to cover all risks a financial institution is exposed to. The P1C represents a baseline capital requirement that is complemented by the Pillar 2 Capital requirement, which is more reflective of a financial institution’s specific business model and risks. Still, it is warranted to assess whether environmental risks are appropriately reflected in the P1C requirements, especially if these lead to systemic risks.

Even though the DP raises more questions than it provides answers, some starting points for the discussion are introduced. One is that the EBA takes a risk-based approach. Their standpoint is that changes to the prudential framework should reflect actual risk differentials compared to other risk types and that it should not be a tool to (unjustly) incentivize the transition to a sustainable economy. The latter lies “in the remit of political authorities.”

The DP also discusses some challenges related to environmental risks. One example is the lack of high-quality, granular historical data, which is needed to support the calibration of the prudential framework. The EBA also mentions the mismatch in the time horizon for the prudential framework (i.e., a business cycle) and the time horizon over which the environmental risks will unfold (i.e., several decades). They wonder whether “the business cycle concepts and assumptions that are used in estimating risk weights and capital requirements are sufficient to capture the emergence of these risks.”

Finally, the EBA does not favor supporting and/or penalizing factors, i.e., the introduction of adjustments to the existing risk weights based on a (green) taxonomy-based classification of the exposures1. They are right to argue that there is no direct relationship between an exposure’s sustainability profile and its credit risk. In addition, there is a risk of double counting if environmental risk drivers have already been reflected in the current prudential framework. Consequently, the EBA concludes that targeted amendments to the framework may be more appropriate. An example would be to ensure that environmental risks are properly included in external credit ratings and the credit risk models of financial institutions. We explain this in more detail in the following paragraphs.

Pillar 1 Capital requirements

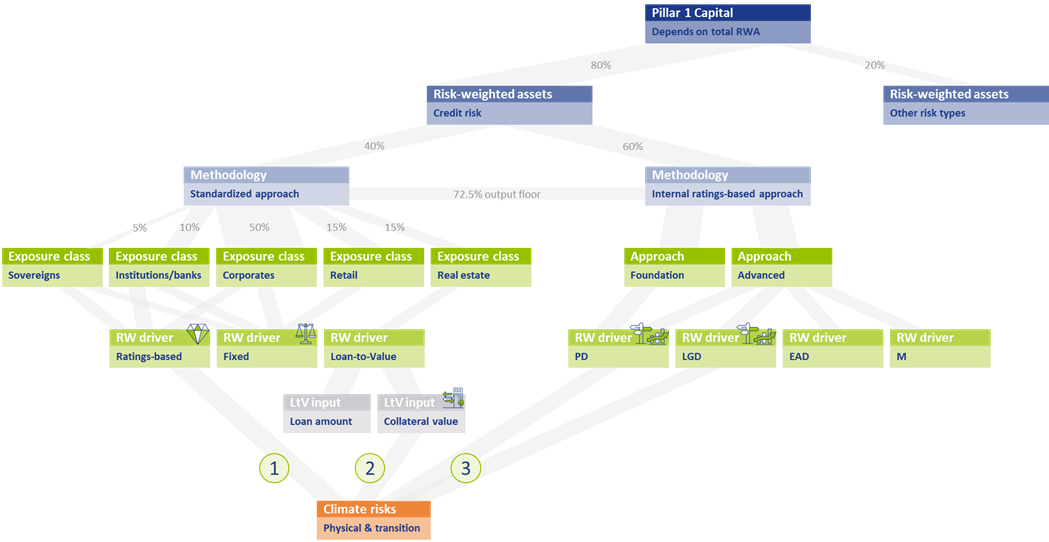

The assessment to what extent climate change risks are properly captured in the current prudential framework requires at least a high-level understanding of the framework. Figure 1 presents a schematic overview of the P1C requirements.

The P1C (at the top of Figure 1) depends on the total amount of Risk-Weighted Assets (RWAs; on the row below)2. RWAs are determined separately for each (traditional) risk type. As mentioned, we only focus on credit risk in this article. The RWAs for credit risk are approximately 80% of the average bank’s total RWAs3. Financial institutions can choose between two methodologies for determining their credit risk RWAs: the Standardized Approach (SA)4 and the internal ratings-based (IRB) approach5 . In Europe, on average 40% of the total RWAs for credit risk are based on the SA, while the rest is based on the IRB approach6 :

Figure 1 – Schematic overview of the P1C requirements and the interaction with climate change risks

Standardized Approach

In the SA, risk weights (RWs) are assigned to individual exposures, depending on their exposure class. About 50% of the RWAs for credit risk in the SA stem from the Corporates exposure class7. Generally speaking, there are three possible RW drivers: the RWAs depend on the external credit rating for the exposure, a fixed RW applies, or the RW depends on the Loan-to-Value8 (LtV) of the (real estate) exposure. The RW for an exposure to a sovereign bond for example, is either equal to 100% if no external credit rating is available (a fixed RW) or it ranges between 0% (for an AAA to AA-rated bond) and 150% (for a below B-rated bond).

Internal Ratings-Based Approach

Within the IRB approach, a distinction is made between Foundation IRB (F-IRB) and Advanced IRB (A-IRB). In both cases, a financial institution is allowed to use its internal models to determine the Probability of Default (PD) for the exposure. In the A-IRB approach, the financial institution in addition is allowed to use internal models to determine the Loss Given Default (LGD), Exposure at Default (EAD), and the Effective Maturity (M).

Interaction with climate change risks

The overview of the P1C requirements introduced in the previous section allows us to investigate the interaction between climate change risks and the P1C requirement. This is done separately for the SA and the IRB approach.

Standardized Approach

In the SA, there are two elements that allow for interaction between climate change risks and the resulting P1C. Climate change risks could be reflected in the P1C if the RW depends on an external credit rating, and this rating in turn properly accounts for climate change risks in the assessment of the counterparty’s creditworthiness (see 1 in Figure 1). The same holds if the RW depends on the LtV and in turn, the collateral valuation properly accounts for climate change risks (see 2 in Figure 1). This raises several concerns:

First, it can be questioned whether external credit ratings are properly capturing all climate change risks. In a report from the Network for Greening the Financial System (NGFS) [3], which was published at the same time as EBA’s DP, it is stated that credit rating agencies (CRAs) have so far not attempted to determine the credit impact of environmental risk factors (through back-testing for example). Also, the lack of high-quality historical data is mentioned as an explanation that statistical relationships between environmental risks and credit ratings have not been quantified. Further, a paper published by the ECB [4] concludes that, given the current level of disclosures, it is impossible for users of credit ratings to establish the magnitude of adjustments to the credit rating stemming from ESG-related risks. Nevertheless, they state that credit rating agencies “have made significant progress with their disclosures and methodologies around ESG in recent years.” The need for this is supported by academic research. An example is a study [5] from 2021 in which a correlation between credit default swap (CDS) spreads and ESG performance was demonstrated, and a study from 2020 [6] which demonstrated that high emitting companies have a shorter distance-to-default.

Secondly, the EBA has reported in the DP that less than 10% of the SA’s total RWAs is derived based on external credit ratings. This implies that a large share of the total RWAs is assigned a fixed RW. Obviously, in those cases there is no link between the P1C and the climate change risks involved in those exposures.

Finally, climate change risks only impact the P1C maintained for real estate exposures to the extent that these risks have been reflected in collateral valuations. Although climate change risks are priced in financial markets according to academic literature, many papers and institutions indicate that these risks are not (yet) fully reflected. In a survey held by Stroebel and Wurgler in 2021 [7], it is shown that a large majority of the respondents (consisting of finance academics, professionals and public sector regulators, among others) is of the opinion that climate change risks have insufficiently been priced in financial markets. A nice overview of this and related literature is presented in a publication from the Bank for International Settlements (BIS) [8]. The EBA DP itself lists some research papers in chapter 5.1 that indicate a relationship between a home’s sales price and its energy efficiency, or with the occurrence of physical risk events. It is unclear though if climate change risks are fully captured in the collateral valuations. For example, research is presented that information on flood risk is not priced into residential property prices. Recent research by ABN AMRO [9] also shows this.

Internal Ratings-Based Approach

In the IRB approach, financial institutions have more flexibility to include climate change risks in their internal models (see 3 in Figure 1). In the F-IRB approach this is limited to PD models, but in the A-IRB approach also LGD models can be adjusted.

A complicating factor is the forward-looking nature of climate change risks. In recent years, the competent authorities have pressured financial institutions to use historical data as much as possible in their model calibration and to back-test the performance of their models. As climate change risks will unfold over the next couple of decades, these are not (yet) reflected in historical data. To incorporate climate change risk, expert judgement would therefore be required. This has been discouraged over the past years (e.g., through the ECB’s Targeted Review of Internal Models (TRIM)) and it will probably trigger a discussion with the competent authorities. A possible deterioration of model performance (due to higher estimated risks compared to historically observations) is just one example that may attract attention.

Another complicating factor is that under the IRB approach, the PD of an obligor is estimated based on long-run average one-year default rates. While this may be an appropriate approach if there are no clear indications that the overall risk level will change, this does not hold if climate change risks increase in the future, and possibly increase systemic risks. By continuing to base a PD model on historical data only, especially for exposures with a time to maturity beyond a couple of years, the credit risk may be understated.

Are amendments to the prudential framework needed?

We have explained that there are several mechanisms in the prudential framework that allow environmental risks to be included in the P1C: the use of external credit ratings, the valuation of collateral, and the PD and LGD models used in the IRB approach. We have also seen, however, that it is questionable whether these mechanisms are fully effective. External credit ratings may not properly reflect all environmental risks and these risks may not be fully priced in on capital markets, leading to incorrect collateral values. Finally, a large share of the RWAs for credit risk depends on fixed RWs that are not (environmentally) risk-sensitive.

Consequently, it can be argued that amendments or enhancements to the prudential framework are needed. One must be careful, however, as the risk of double counting is just around the corner. Therefore, the following amendments or actions should be considered:

Further research should be undertaken to investigate the relationship between climate change risk and the creditworthiness of counterparties. If there is more clarity on this relationship, it should also be assessed to what extent this relationship is sufficiently reflected in external ratings. Requiring more advanced disclosures from credit rating agencies could help to understand whether these risks are sufficiently captured in the prudential framework. One should be cautious to amend the ratings-based RWs in the SA, since credit rating agencies are continuously working on the inclusion of environmental risks into their credit assessments; there would be a real risk of double counting.

The potential negative impact of climate change risks oncollateral value should be further investigated. Financial institutions are already required by the ECB9 to consider environmental risks in their collateral valuations but this is not at a sufficient level yet. It will be important to consider the possibility of sudden value changes due to transition risks like shifting consumer sentiment or awareness.

To improve the risk-sensitivity of the framework, a dependency on the carbon emissions of the counterparty could be introduced in the fixed RWs, possibly only for the most carbon-intensive sectors. It could be argued that there are other factors that have a more significant relationship with the default risk of a certain counterparty that could be included in the SA. Climate change risks, however, differ in the sense that they can lead to a systemic risk (as opposed to an idiosyncratic risk) that is currently not captured in the overall level of the RWs.

In the SA, a distinction could be introduced based on the exposure’s time to maturity. For relatively short-term exposures, the current calibrations are probably fine. For longer-term exposures, however, the risks stemming from climate change may be underestimated as these are expected to increase over time.

In the IRB approach, a reflection of climate change risk would require the regulator to allow for forward-looking expert judgment in the (re)calibration of PD and LGD models. Further guidance from the competent authorities on the potentially negative impact on model performance based on historical data would also be useful.

Conclusion

Based on the schematic overview of the P1C requirements and the (potential) interaction with climate change risks, we conclude that several mechanisms in the prudential framework allow for climate change risks to be incorporated into the P1C. At the same time, we conclude that this interaction is limited to specific parts of the portfolio, and that in those cases it remains to be seen to what extent this is properly accounted for. To remedy this, amendments to the prudential framework could be considered. It is important, however, to avoid double counting issues and to be mindful of time horizon differences.

It is expected that the EBA will publish a final report on the prudential treatment of environmental risks in the first half of this year. However, especially financial institutions that are using the IRB approach should not take a wait-and-see approach. Given the complexity of modeling climate change risks, it is prudent to start incorporating climate change risks into PD and LGD models sooner rather than later.

With Zanders’ extensive experience covering both credit risk modeling and climate change risk, we are well suited to support with this process. If you are looking for support, please reach out to us.

1 Supporting factors are currently in place for SMEs and infrastructure projects, but the EBA advocated their removal.

3 See for example the results from the EBA’s EU-wide transparency exercise. This is reflected in Figure 1 by the percentage in the grey link between P1C and RWAs for credit risk.

6 In the Netherlands, less than 20% of the total RWAs is based on the SA. See the EBA’s EU-wide transparency exercise for more information. The percentages in the grey link between ‘Risk-weighted assets’ and ‘Methodology’ in Figure 1 are based on the European average.

7 See the EBA’s Risk assessment of the European banking system [2]. The percentages in the grey link between ‘Standardized Approach’ and the ‘Exposure class’ in Figure 1 reflect the share of RWAs in the SA for each of the different exposure classes.

8 The LtV is defined as the ratio between the loan amount and the value of the property that serves as collateral.

9 See expectation 8.3 in the ECB’s Guide on climate-related and environmental risks.

References

The role of environmental risks in the prudential framework, European Banking Authority, Discussion Paper, 2 May 2022

Risk assessment of the European banking system, European Banking Authority, December 2022

Capturing risk differentials from climate-related risks, Network for Greening the Financial System, Progress Report, May 2022

Disclosure of climate change risk in credit ratings, European Central Bank, Occasional Paper Series, No. 303, September 2022

Pricing ESG risk in credit markets, Federated Hermes, March 2021

Climate change and credit risk, Capasso, Gianfrate, and Spinelli, Journal of Cleaner Production, Volume 266, September 2020

What do you think about climate finance?, Stroebel and Wurgler, Journal of Financial Economics, vol 142, no 2, November 2021

Pricing of climate risks in financial markets, Bank for International Settlements, Monetary and Economic Department, December 2022

Is flood risk already affecting house prices?, ABN AMRO, 11 February 2022

Guide on climate-related and environmental risks, European Central Bank, November 2020

BCBS Principles for the effective management of climate-related financial risks

February 2023

3 min read

Authors:

Sjoerd Blijlevens, Jill Langenberg

Share:

In March 2021, the European Banking Authority (EBA) was mandated through Article 501c of the Capital Requirements Regulation (CRR) to “assess […] whether a dedicated prudential treatment of exposures related to assets or activities associated substantially with environmental and/or social objectives would be justified”.

These risks stem from the transition towards a low carbon economy and from the physical risks of damages due to extreme weather events. To address climate-related financial risks within the banking sector, the Basel Committee on Banking Supervision (BCBS) established a high-level Task Force on Climate-related Financial Risks in 2020. It contributes to the BCBS’s mandate to strengthen the regulation, supervision and practices of banks worldwide with the purpose of enhancing financial stability.

Both the BCBS’s Core principles for effective banking supervision1 and the Supervisory Review and Evaluation Process (SREP) within the existing Basel Framework are considered sufficiently broad and flexible to accommodate additional supervisory responses to climate-related financial risks. It was felt, however, that supervisors and banks could benefit from the publication of the Principles for the effective management and supervision of climate-related financial risks2. Through this publication, the BCBS seeks to promote a principles-based approach to improving risk management and supervisory practices regarding climate-related financial risks. The document contains principles directed to banks and principles directed to supervisory authorities. In this article, we present an overview of the principles directed to banks.

The BCBS published a draft of their Principles in November 2021. During the consultation phase, which lasted until February 2022, banks and supervisors could provide feedback. The BCBS incorporated their feedback in the final version of the Principles that were published in June 2022.

Principles for the management of climate-related financial risks

In total, twelve bank-focused principles are presented and grouped in eight categories. Each of the eight categories is briefly discussed below:

Corporate governance – Principles 1 to 3

The principles related to corporate governance state that banks first need to understand and assess the potential impact of climate risks on all fields they operate in. Subsequently, appropriate policies, procedures and controls need to be implemented to ensure effective management of the identified risks. Furthermore, roles and responsibilities need to be clearly defined and assigned throughout the bank. To successfully manage climate-related risks, banks should ensure an adequate understanding of climate-related financial risks and as well as adequate resources and skills at all relevant functions and business units within the bank. Finally, the board and senior management should ensure that all climate-related strategies are consistent with the bank’s stated goals and objectives.

Internal control framework – Principle 4

The fourth principle within the internal control framework subcategory requires banks to include clear definitions and assignment of climate-related responsibilities and reporting lines across all three lines of defense. Further requirements are then presented for each line of defense.

Capital and liquidity adequacy – Principle 5

After the identification and quantification of the climate-related financial risks, these risks need to be incorporated into banks’ Internal Capital (and Liquidity) Adequacy Assessment Process (ICLAAP). Banks should provide insights in which climate-related financial risks affect their capital and liquidity position. In addition, physical and transition risks relevant to a bank’s business model assessed as material over relevant time horizons, should be incorporated into their stress testing programs in order to evaluate the bank’s financial position under severe but plausible scenarios. Furthermore, the described incorporation in the ICLAAP to handle such financial risks, should be done iteratively and progressively, as the methodologies and data used to analyze these risks continue to mature over time.

Risk management process – Principle 6

The sixth principle connects to the previous one, as it states that a bank needs to identify, monitor and manage all climate-related financial risks that could materially impair their financial condition, including their capital resources and liquidity positions. The bank’s risk management framework should be comprehensive with respect to the (material) climate-related financial risks they are exposed to. Clear definitions and thresholds should be set for materiality. These need to be monitored closely and adjusted, if necessary, as climate-related risks are evolving.

Management monitoring and reporting – Principle 7

After ensuring that the risk framework is comprehensive, banks need to implement the monitoring and reporting of climate-related financial risks in a timely manner to facilitate effective decision-making. To achieve such reporting, a good data infrastructure should be in place at the bank. This allows it to identify, collect, cleanse, and centralize the data necessary to assess material climate-related financial risks. Furthermore, banks should actively collect additional data from clients and counterparties in order to develop a better understanding of their client’s transition strategies and risk profiles.

Management of credit, market, liquidity, operational risk – Principles 8 to 11

Banks should understand the impact of climate-related risk drivers on their credit risk profiles, market positions, liquidity risk profiles and operational risks. Clearly articulated credit policies and processes to identify, measure, evaluate, monitor, report and control or mitigate the impacts of material climate-related risk drivers on banks’ credit risk exposures should be in place. From a market risk perspective, banks should consider the potential losses in their portfolios due to climate-related risks. On the business operation and strategy side of banking activities, the impact of climate-related risks also plays a large role. For example, physical risks have to be taken into account when drafting business continuity plans. After understanding the different risks and their impacts, a range of risk mitigation options to control or mitigate climate-related financial risks need to be considered.

Scenario analysis – Principle 12

The final principle states that banks need to use scenario analysis to assess the resilience of their business models and strategies to a range of plausible climate-related pathways, and to determine the impact of climate-related risk drivers on their overall risk profile. Scenario analysis should reflect the overall relevant climate-related financial risks for banks, including both physical and transition risks. This analysis should be performed for different time horizons, both short- and long-term, and should be highly dynamic.

Changes to the BCBS risk framework draft and related publications

The final Principles have not changed much compared to the November 2021 consultation document. The most important changes are that the first principle, concerning corporate governance of banks, and the fifth principle, concerning capital and liquidity adequacy, have been extended. The corporate governance principle, for example, now also includes that banks should ensure that their internal strategies and risk appetite statements are consistent with any publicly communicated climate-related strategies and commitments. The capital and liquidity adequacy principle now includes a section requiring banks to incorporate material climate-related financial risks in their stress testing programs.

These twelve bank-focused principles, providing banks guidance on effective risk management of climate-related financial risks, can also be linked to the initiatives of other regulators such as the ECB. In November 2020, for example, the ECB provided a guide that describes how it expects institutions to consider climate-related and environmental risks, when formulating and implementing their business strategy, governance and risk management frameworks (the ECB expectations). These ECB expectations are in line with the BCBS Principles (and often more elaborate).

Zanders has gained relevant experience in implementing the ECB expectations at several Dutch banks. This experience ranges from risk identification and materiality assessments to the quantification of climate-related risks, ESG data frameworks, model validations, and scenario analysis. Please reach out to us if your bank is seeking support in implementing the BCBS Principles.

References 1) Basel Committee on Banking Supervision (2012). Core Principles for Effective Banking Supervision. 2) Basel Committee on Banking Supervision (2022). Principles for the effective management and supervision of climate-related financial risks.

Regulatory timelines ESG Risk Management

January 2023

3 min read

Authors:

Sjoerd Blijlevens, Marije Wiersma

Share:

In March 2021, the European Banking Authority (EBA) was mandated through Article 501c of the Capital Requirements Regulation (CRR) to “assess […] whether a dedicated prudential treatment of exposures related to assets or activities associated substantially with environmental and/or social objectives would be justified”.

In the below overview, we present an overview of the main ESG-related publications from the European Commission (EC), the European Central Bank (ECB), and the European Banking Authority (EBA).

This is complemented by the most important timelines that are stipulated in these regulations and guidelines. Additional regulations and guidelines that are expected for the next couple of years are also highlighted.

If you want to discuss any of them, don’t hesitate to reach out to our subject matter experts.

The ESG data challenge

July 2022

6 min read

Authors:

Sjoerd Blijlevens, Marije Wiersma

Share:

Financial institutions (FIs) play an important role in the transition towards a more sustainable economy in which Environmental, Social and Governance (ESG) factors are properly addressed.

But to seize the opportunities ESG must become an integrated part of a bank’s strategy, risk management and disclosure regimes. High-quality data is instrumental to identify and measure ESG risks, but it can be lacking. FIs need to improve their internal data and use of external private and public vendors like Moody’s or the IMF, while developing a framework that plugs any data gaps.

The lack of appropriate ESG data is considered one of the main challenges for many FIs, but proxies, such as using a building’s energy rating to work out its carbon emissions, can be used.

FIs need climate change-related data that isn’t always available if you don’t know where to look. This article will give you an overview of the most relevant data vendors and provide suggestions on how to treat missing data gaps in order to get a comprehensive ESG framework for the green future where carbon measurement, assessment, reporting and trading will be vital

The data challenge

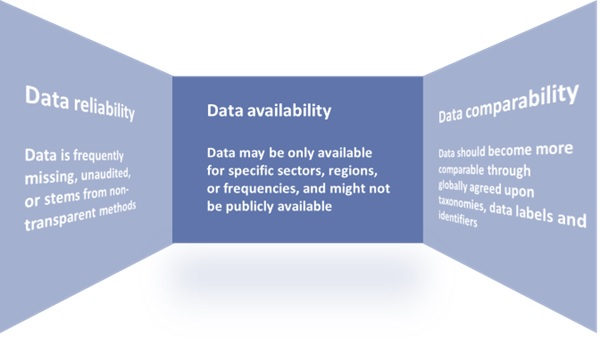

In May 2021, the Network for Greening the Financial System (NGFS) published a ‘Progress report on bridging data gaps’. In this report, the NGFS writes that meeting climate-related data needs is a challenge that can be described along the following three dimensions:

data availability,

reliability,

& comparability.

A further breakdown of the challenges related to these dimensions can be found in Figure 1.

Figure 1: The dimensions of the climate-related data challenge. Source: Graphic adapted by Zanders from a NGFS report entitled: ‘Progress report on bridging data gaps’ (2021).

Key financial metrics

The NGFS writes that a mix of policy interventions is necessary to ensure climate-related data is based on three building blocks:

Common and consistent global disclosure standards.

A minimally accepted global taxonomy.

Consistent metrics, labels, and methodological standards.

EU Taxonomy, CSRD & EBA’s 3 ESG risk disclosure standards

Several initiatives have started to ignite these needed policy interventions. For example, the EU Taxonomy, introduced by the European Commission (EC), is a classification system for environmentally sustainable activities. In addition, the recently approved Corporate Sustainability Reporting Directive (CSRD) provides ESG reporting rules for large listed and non-listed companies in the EU, including several FIs. The aim of the CSRD is to prevent greenwashing and to provide the basis for global sustainability reporting standards. Another example of a disclosure standard is the binding standards on Pillar 3 disclosures on ESG risks developed by the European Banking Authority (EBA).

Even though policy, law and regulation makers have a big part to play in the data challenge, there are also steps that individual institutions could and should take to improve their own ESG data gaps. Regulatory bodies such as the EBA and the European Central Bank (ECB) have shared their expectations and recommendations on the management of ESG data with FIs.

To illustrate, the EBA recommends FIs “[identify] the gaps they are facing in terms of data and methodologies and take remedial action” and the ECB expects institutions to “assess their data needs in order to inform their strategy-setting and risk management, to identify the gaps compared with current data and to devise a plan to overcome these gaps and tackle any insufficiencies”

Collecting data

Collecting ESG data is a challenging exercise. A distinction can be made between collecting data for large market cap companies, and small cap companies and retail clients. Although large cap companies tend to be more transparent, the data often is dispersed over multiple reports – for example, corporate sustainability reports, annual reports, emissions disclosures, company websites, and so on.

For small cap companies and retail clients, the data is more difficult to acquire. Data that is not publicly available could be gathered bilaterally from clients. For example, one European bank has developed an annual client questionnaire to collect data from its clients.

Gathering data from various reports or bilaterally from clients might not always be the best option, however, because it is time consuming or because the data is not available, reliable, or comparable. Two alternatives are:

Use tools to collect the data. For example, using open-source tooling from the Two Degrees Investing Initiative (2DII) to calculate Paris Agreement Capital Transition Assessment (PACTA) portfolio alignment.

Collect data from other external data sources, such as S&P Global.

This could be forward-looking external data on macro-economic expectations, international climate scenarios, financial market data or sectoral climate developments. Below we discuss some sources for external ESG and climate change-related data.

External data

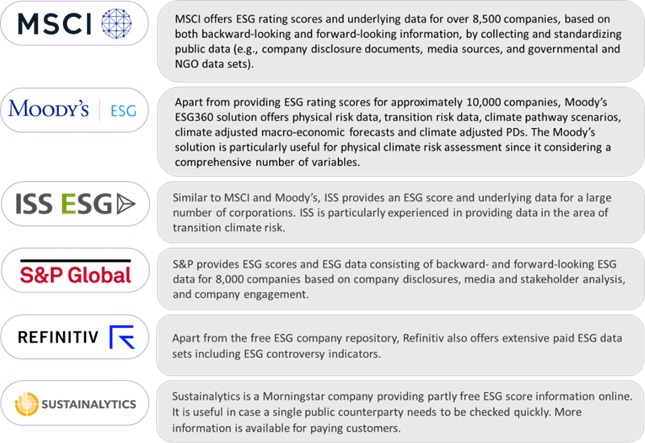

Some of Zanders’ clients resort to vendor solutions for acquiring their ESG data. The most commonly observed solutions, in random order, are:

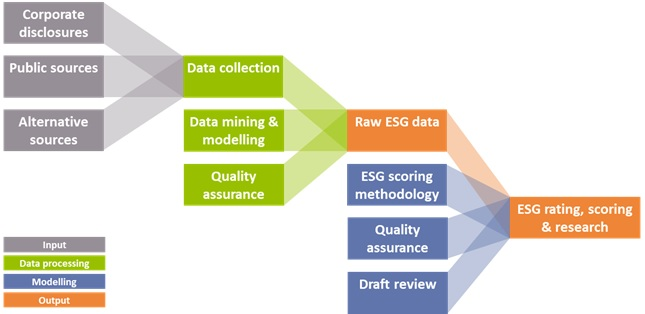

All the solutions above provide an aid to determine if climate related performance data is lacking, or can assist in reporting comparable and reliable data. They all apply a similar process of collecting the data and determining ESG scores, which is illustrated in Figure 2.

Figure 2: Data collection process for ESG data solutions (Source: Zanders).

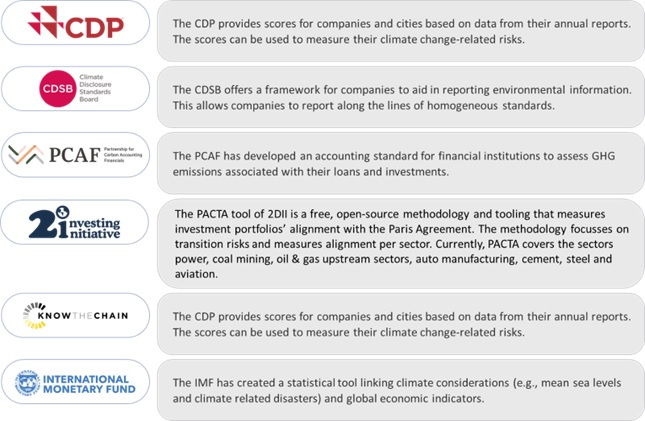

Additionally, public and non-commercial data and solution providers are available, such as:

Missing data

Given the data challenges, it is nearly impossible to create a complete data set. Until that is possible, there are several (temporary) methods to deal with missing data:

Find a comparable loan, asset, or company for which the required data is available.

Distribute sector data based on market share of individual companies. For example, assign 10% of the estimated emission of sector X to company Y based on its market share of 10%.

Find a proxy, comparable or second-best metric. For example, by taking the energy label as a proxy for CO2 emission related to properties, or by excluding scope 3 emissions and focusing on scope 1 and 2 emissions.

Change the granularity level. For example, by gathering data on sector level rather than on individual positions.

Fill in the gaps with statistical or machine learning techniques.

Conclusion

The increased attention to integrating ESG risks into existing risk frameworks has led to a need for FIs to collect and disclose meaningful data on ESG factors. However, there is still a lack of data availability, reliability, and comparability.

Several regulatory and political efforts are ongoing to tackle this data challenge, such as the EU taxonomy. More policy interventions, however, are required. Examples are additional mandatory disclosure requirements, an audit and validation framework for ESG data, and social and governance taxonomies that classify economic activities that contribute to social and governance goals.

In the meantime, FIs have to find ways to produce meaningful insights and comply with regulatory requirements related to ESG risks. Zanders has experienced that there is no one-size-fits-all solution for defining, selecting, implementing, and disclosing relevant data and metrics. It is dependent on the composition of the asset and loan portfolio, the use of the data, and the data that is (already) available. Regardless of how the lack of data is solved, it is important that FIs are transparent about their choices and methodologies, and that the related metrics and scorings are explainable and intuitive.

Financial institutions (FIs) play an important role in the transition towards a more sustainable economy in which Environmental, Social and Governance (ESG) factors are properly addressed.

The Working Group II contribution to the IPCC’s Sixth Assessment Report states that “climate change is a grave and mounting threat to our wellbeing and a healthy planet”. It is a formidable, global challenge to transition to a sustainable economy before time is running out. Banks have an important role to play in this transition. By stepping up to this role now, banks will be better prepared for the future, and reap the benefits along the way.

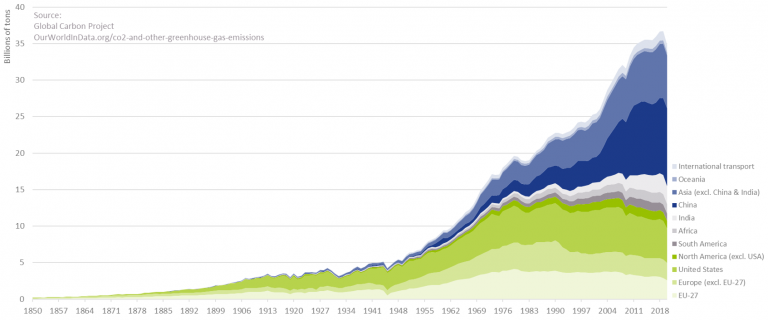

In the Paris Agreement (or COP21), adopted in December 2015, 196 parties agreed to limit global warming to well below 2.0°C, and preferably to no more than 1.5°C. To prevent irreversible impacts to our climate, the IPCC stresses that the increase in global temperature (relative to the pre-industrial era) needs to remain below 1.5°C. To achieve this target, a rapid and unprecedented decrease in the emission of greenhouse gasses (GHG) is required. With CO2 emissions still on the rise, as depicted in Figure 1, the challenge at hand has increased considerably in the past decade.

Figure 1 – Annual CO2 emissions from fossil fuels.

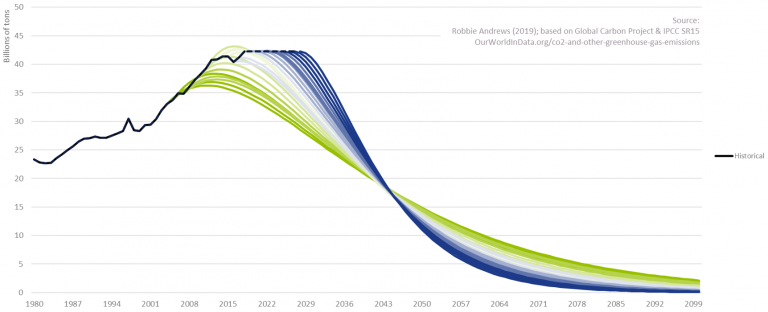

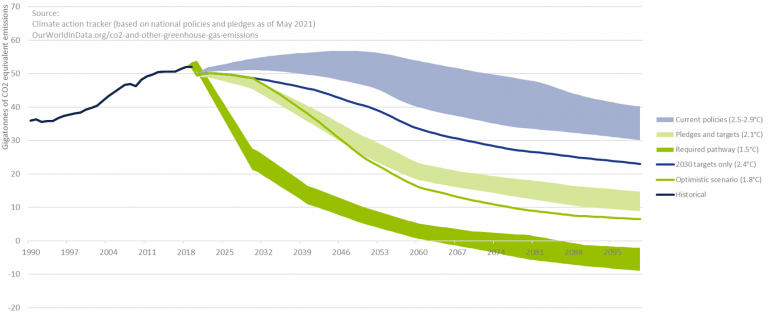

To further illustrate this, Figure 2 depicts for several starting years a possible pathway in CO2 reductions to ensure global warming does not exceed 2.0°C. Even under the assumption that CO2 emissions have already peaked, it becomes clear that the required speed of CO2 reductions is rapidly increasing with every year of inaction. We are a long way from limiting global warming to 2.0°C. This even holds under the assumption that all countries’ pledges to reduce GHG emissions will be achieved, as can be observed in Figure 3.

To quote the IPCC Working Group II co-chair Hans-Otto Pörtner: “Any further delay in concerted anticipatory global action on adaptation and mitigation will miss a brief and rapidly closing window of opportunity to secure a livable and sustainable future for all.”

Figure 2 – CO2 reduction need to limit global warming.

Figure 3 – Global GHG emissions and warming scenario’s.

The role of banks in the transition – and the opportunities it offers

Historically, banks have been instrumental to the proper functioning of the economy. In their role as financial intermediaries, they bring together savers and borrowers, support investment, and play an important role in facilitating payments and transactions. Now, banks have the opportunity to become instrumental to the proper functioning of the planet. By allocating their available capital to ‘green’ loans and investments at the expense of their ‘brown’ counterparts, banks can play a pivotal role in the transition to a sustainable economy. Banks are in the extraordinary position to make a fundamentally positive contribution to society. And even better, it comes with new opportunities.

The transition to a sustainable economy requires huge investments. It ranges from investments in climate change adaption to investments in GHG emission reductions: this covers for example investments in flood risk warning systems and financing a radical change in our energy mix from fossil-fuel based sources (like coal and natural gas) to clean energy sources (like solar and wind power). According to the Net Zero by 2050 Report from the International Energy Agency (IEA)2, the annual investments in the energy sector alone will increase from the current USD 2.3 trillion to USD 5.0 trillion by 2030. Hence, across sectors, the increase in annual investments could easily be USD 3.0 to 4.0 trillion. As much as 70% of this investment may need to be financed by the private sector (including banks and other financial institutions)3. To put this in perspective, the total outstanding credit to non-financial corporates currently stands at USD 86.3 trillion4. Assuming an average loan maturity of 5 years, this would translate to a 12-16% increase in loans and investments by banks on a global level. Hence, the transition to a sustainable economy will open up a large market for banks through direct investments and financing provided to corporates and households.

The transition to a sustainable economy is also triggering product development. The Climate Bonds Initiative (CBI) for example reports that the combined issuance of Environmental, Social, and Governance (ESG) bonds, sustainability-linked bonds and transition debt reached almost USD 500 billion in 2021H1, representing a 59% year-on-year growth rate. Other initiatives include the introduction of ‘green’ exchange-traded funds (ETFs) and sustainability-linked derivatives. The latter first appeared in 2019 and they provide an incentive for companies to achieve sustainable performance targets. If targets are met, a company is for example eligible for a more attractive interest coupon. Again, this is creating an interesting market for banks.

By embracing the transition, with all the opportunities that it offers, banks are also bracing themselves for the future. Banks that adopt climate change-resilient business models and integrate climate risk management into their risk frameworks will be much better positioned than banks that do not. They will be less exposed to climate-related risks, ranging from physical and transition risks to risks stemming from a reputational perspective or litigation, also justifying lower capital requirements. The early adaptors of today will be the leaders of tomorrow.

A roadmap supporting the transition

How should a bank approach this transition? As depicted in Figure 4, we identify four important steps: target setting, measurement and reporting, strategy and risk framework, and engaging with clients.

Figure 4 – The roadmap supporting the transition to a sustainable economy.

Target setting

The starting point for each transition is to set GHG emission targets in alignment with emission pathways that have been established by climate science. One important initiative that can support banks in setting these targets is the Science Based Targets initiative (SBTi). This organization supports companies to set targets in line with the goals of the Paris Agreement. Unlike many other companies, the majority of a bank’s GHG emissions are outside their direct control. They can influence, however, their so-called financed emissions, which are the GHG emissions coming from their lending and investment portfolios. The SBTi has developed a framework for banks that reflects this. It encourages banks to use the Absolute Contraction approach that requires a 2.5% (for a well-below 2.0°C target) or 4.2% (for a 1.5°C target) annual reduction in GHG emissions. A clear emission pathway guides banks in the subsequent steps of the transition process.

Measurement and reporting

With targets in place, the next important step for a bank is to determine their level of GHG emissions: both for scope 1 and 2 (the GHG emissions they control) and for scope 3 (the financed emissions). Important initiatives for the quantification of the financed emissions are the Paris Agreement Capital Transition Assessment (PACTA) and the Platform Carbon Accounting Financials (PCAF). PCAF is a Dutch initiative to deliver a global, standardized GHG accounting and reporting approach for financial institutions (building on the GHG Protocol). PACTA enables banks to measure the alignment of financial portfolios with climate scenarios.

By keeping track of the level of GHG emissions on an annual basis, banks can assess whether they are following their selected emission pathway. Reporting, in line with the recommendations of the Task Force on Climate-Related Financial Disclosures (TCFD), will contribute to a greater understanding of climate risks with their investors and other stakeholders.

Strategy and risk framework

Setting targets and measuring the current level of GHG emissions are necessary but not sufficient conditions to achieve a successful transition. Climate change risk needs to be fully integrated into a bank’s strategy and its risk framework. To assess the climate change-resilience of a bank’s strategy, a logical first step is to understand which climate change risks are material to the organization (e.g., by composing a materiality matrix). Subsequently, studying the transmission channels of these risks using scenario analysis and/or stress testing creates an understanding of what parts of the business model and lending portfolio are most exposed. This could lead to general changes in a bank’s positioning, but these risks should also be factored into the bank’s existing risk framework. Examples are the loan origination process, capital calculations, and risk reporting.

Engaging with clients

A fourth step in the game plan to successfully support the transition is for a bank to actively engage with its clients. A dialogue is required to align the bank’s GHG emission targets with those of its clients. This extends to discussing changes in the operations and/or business model of a client to align with a sustainable economy. This also may include timely announcing that certain economic activities will no longer be financed, and by financing client’s initiatives to mitigate or adapt to climate change: e.g., financing wind turbines for clients with energy- or carbon-intensive production processes (like cement or aluminium) or financing the move of production locations to less flood-prone areas.

Conclusion

Banks are uniquely positioned to play a pivotal role in the transition to a sustainable economy. The transition is already providing a wide range of opportunities for banks, from large financing needs to the introduction of green bonds and sustainability-linked derivatives. At the same time, it is of paramount importance for banks to adopt a climate change-resilient strategy and to integrate climate change risk into their risk frameworks. With our extensive track record in financial and non-financial risk management at financial institutions, Zanders stands ready to support you with this ambitious, yet rewarding challenge.

ESG risk management and Zanders

Zanders is currently supporting several clients with the identification, measurement, and management of ESG risks. For a start, we are supporting a large Dutch bank with the identification of ESG risk factors that have a material impact on the credit risk profile of its portfolio of corporate loans. The material risk factors are then integrated in the bank’s existing credit risk framework to ensure a proper management of this new risk type.

We are supporting other banking clients with the quantification of climate change risk. In one case, we are determining climate change risk-adjusted Probabilities of Default (PDs). Using expected future emissions and carbon prices based on the climate change scenarios of the Network for Greening the Financial System (NGFS), company specific shocks based on carbon prices and country specific shocks on GDP level are determined. These shocked levels are then used to determine the impact on the forecasted PDs. In another case, we are investigating the potential impact of floods and droughts on the collateral value of a portfolio of residential mortgage loans.

We also gained experience with the data challenges involved in the typical ESG project: e.g., we are supporting an asset manager with integrating and harmonizing ESG data from a range of vendors, which is underlying their internally developed ESG scores. We also support them with embedding these scores in the investment process.

With our extensive track record in financial and non-financial risk management at financial institutions in general, and our more recent ESG experience, Zanders stands ready to support you with the ambitious, yet rewarding challenge to adopt a climate change-resilient strategy and to integrate climate change risk in your existing risk frameworks.

In March 2021, the European Banking Authority (EBA) was mandated through Article 501c of the Capital Requirements Regulation (CRR) to “assess […] whether a dedicated prudential treatment of exposures related to assets or activities associated substantially with environmental and/or social objectives would be justified”.

Next to sustainable funding instruments, including both green and social, we also see that these KPI’s can be used for other financial instruments, such as ESG (Environmental, Social, Governance) derivatives. These derivatives are a useful tool to further drive the corporate sustainability strategy or support meeting environmental targets.

Since the first sustainability-linked derivative was executed in 2019, market participants have entered into a variety of ESG-related derivatives and products. In this article we provide you with an overview of the different ESG derivatives. We will touch upon the regulatory and valuation implications of this relatively new derivative class in a subsequent article, which will be published later this year.

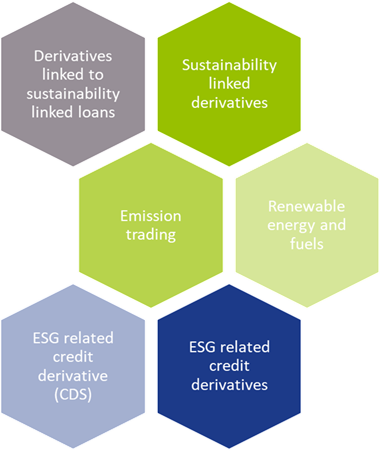

Types of ESG-related derivatives products

Driven by regulatory pressure and public scrutiny, corporates have been increasingly looking for ways to manage their sustainability footprint. As a result of a blooming ESG funding market, the role of derivatives to help meet sustainability goals has grown. ESG-related derivatives cover a broad spectrum of derivative products such as forwards, futures and swaps. Five types (see figure 1) of derivatives related to ESG can be identified; of which three are currently deemed most relevant from an ESG perspective.

The first category consists of traditional derivatives such as interest rate swaps or cross currency swaps that are linked to a sustainable funding instrument. The derivative as such does not contain a sustainability element.

Sustainability-linked derivatives

Sustainability-linked derivatives are agreements between two counterparties (let’s assume a bank and a corporate) which contain a commitment of the corporate counterparty to achieve specific sustainability performance targets. When the sustainability performance targets are met by the corporate during the lifetime of the derivative, a discount is applied by the bank to the hedging instrument. When the targets are not met, a premium is added. Usually, banks invest the premium they receive in sustainable projects or investments. Sustainability-linked derivative transactions are highly customizable and use tailor-made KPIs to determine sustainability goals. Sustainability-linked derivatives provide market participants with a financial incentive to improve their ESG performance. An example is Enel’s sustainability-linked cross currency swap, which was executed in July 2021 to hedge their USD/EUR exchange rate and interest rate exposures.

Emission trading derivatives

Other ESG-related derivatives support meeting sustainable business models and consist of trading carbon offsets, emission trading derivatives, and renewable energy and renewable fuels derivatives, amongst others. Contrary to sustainability-linked derivatives, the use of proceeds of ESG-related derivatives are allocated to specific ESG-related purposes. For example, emissions trading is a market-based approach to reduce pollution by setting a (geographical) limit on the amount of greenhouse gases that can be emitted. It consists of a limit or cap on pollution and tradable instruments that authorize holders to emit a specific quantity of the respective greenhouse gas. Market participants can trade derivatives based on emission allowances on exchanges or OTC markets as spots, forwards, futures and option contracts. The market consists of mandatory compliance schemes and voluntary emission reduction programs.

Renewable energy and fuel derivatives

Another type of ESG-related derivatives are renewable energy and renewable fuel hedging transactions, which are a valuable tool for market participants to hedge risks associated with fluctuations in renewable energy production. These ESG-related credit derivatives encourage more capital to be contributed to renewable energy projects. Examples are Power Purchase Agreements (PPAs), Renewable Energy Certificate (REC) futures, wind index futures and low carbon fuel standard futures.

ESG related credit derivatives

ESG-related CDS products can be used to manage the credit risk of a counterparty when financial results may be impacted by climate change or, more indirectly, if results are affected due to substitution of a specific product/service. An example of this could be in the airline industry where short-haul flights may be replaced by train travel. Popularity of ESG-related CDS products will probably increase with the rising perception that companies with high ESG ratings exhibit low credit risk.

Catastrophe and weather derivatives

Catastrophe and weather derivatives are insurance-like products as well. Both markets have existed for several decades and are used to hedge exposures to weather or natural disasters. Catastrophe derivatives are financial instruments that allow for transferral of natural disaster risk between market participants. These derivatives are traded on OTC markets and enable protection from enormous potential losses following from natural disasters such as earthquakes to be obtained. The World Bank has designed catastrophe swaps that support the transfer of risks related to natural disasters by emerging countries to capital markets. An example if this is the swap issued for the Philippines in 2017. Weather derivatives are financial instruments that derive their value from weather-related factors such as temperature and wind. There derivatives are used to mitigate risks associated with adverse or unexpected weather conditions and are most commonly used in the food and agriculture industry.

What’s old, what’s new and what’s next?

ESG-related credit derivatives would be best applied by organizations with credit exposures to certain industries and financial institutions. Despite the link to an environmental element, we do not consider catastrophe bonds and weather derivatives as a sustainability-linked derivative. Neither is it an innovative, new product that is applicable to corporates in various sectors.

Truly innovative products are sustainability-linked derivatives, voluntary emissions trading and renewable energy and fuel derivatives. These products strengthen a corporate’s commitment to meet sustainability targets or support investments in sustainable initiatives. A lack of sustainability regulation for derivatives raises the question to what extent these innovative products are sustainable on their own? An explicit incentive for financial institutions to execute ESG-related derivatives, such as a capital relief, is currently absent. This implies that any price advantage will be driven by supply and demand.

Corporate Treasury should ensure they consider the implications of using ESG-related derivatives that affect the cashflows of derivatives transactions. Examples of possible regulatory obligations consist of valuation requirements, dispute resolution and reporting requirements. Since ESG-related derivatives and products are here to stay, Zanders recommends that corporate treasurers closely monitor the added value of specific instruments, as well as the regulatory, tax and accounting implications. Part II of this series, later in the year, will focus on the regulatory and valuation implications of this relatively new derivative class.

For more information on ESG issues, please contact Sander van Tol.

Climate Change Risk Management for insurers.

September 2021

6 min read

Author:

Lennard Beijering

Share:

Financial institutions (FIs) play an important role in the transition towards a more sustainable economy in which Environmental, Social and Governance (ESG) factors are properly addressed.

Climate change risks are relatively newly identified risks that insurers are facing. These risks can negatively impact both assets and liabilities of insurers. Already in 2018, the European Commission requested the European Insurance and Occupational Pensions Authority (EIOPA) to investigate how climate change risk could be integrated into the Solvency II Framework.