Zanders helped Royal FloraHolland – the largest B2B floriculture platform in the world – to secure a new debt facility of €210 million with three banks and built a compelling case for their future credit requirements.

How do you get banks on board to provide you with financing on favorable terms when your modus operandi isn’t maximizing profit? Zanders helped Royal FloraHolland find the answer, leading them to secure a new debt facility of €210 million with three banks. Royal FloraHolland is the largest B2B floriculture platform in the world. Operating as a member-owned cooperative has always been the strongest element of Royal FloraHolland’s manifesto - right from its first flower auction back in 1912. But this unique structure also proved to be a complication when it came to refinancing its credit facility. Fortunately, they had Zanders on hand to help frame a compelling case for their future credit requirements.

Harnessing cooperative strength

Royal FloraHolland was first established as a cooperative for growers and sellers more than 110 years ago and is renowned for organizing flower auctions via clock sales. Over the years, as the floriculture trade has become increasingly international and competitive, the role and remit of Royal FloraHolland has expanded beyond flower auctions. Today, it is an international B2B trading platform offering a wide variety of deal-making, logistics, and financial services to its members.

Royal FloraHolland - and as a consequence a large part of the sector - is currently in the midst of a large-scale transformation, focusing on, among other things, migrating to a more digital way of working (via the Floriday platform) and promoting more sustainable practices across the floriculture sector. The refinancing of Royal FloraHolland’s credit facility in 2024 was not only important in terms of securing financial back-up for its day-to-day operations but also to invest in ongoing strategic developments.

Putting in the groundwork

The impending maturity of Royal FloraHolland’s existing credit facility in 2024 prompted the cooperative to appoint Zanders in 2022 to maximize the success of their corporate refinancing process. A process that started with the internal team conducting a lengthy reevaluation of their capital needs in the light of their evolving strategic priorities and ambitions.

“When Royal FloraHolland first reached out to us in 2022, we had a few talks, looked into numbers and analysis, and talked about the questions that they were likely to be asked and where they stood at that point in time,” remembers Zanders' Partner, Koen Reijnders. “This revealed that the future financial projections for the refinancing were not sufficiently substantiated. At this point, there were two options. We could go to the banks straight away with a story that was not finished yet - but this would inevitably lead to questions. Or Royal FloraHolland could take some time to do more homework and go to the banks better prepared. We all agreed the second option was the route to take.”

Due to the scale of Royal FloraHolland’s transformation program, clarifying financial projections and scoping funding requirements was a lengthy process. “We needed to revisit our strategy and really have commitment internally on our strategic implementation route map and corresponding results, which we could present to the banks,” says David van Mechelen, Chief Financial Officer of Royal FloraHolland. “This required the involvement of the total management team of Royal FloraHolland, across all disciplines. It was a burden, but it was also worthwhile because it sharpened our internal planning and alignment and a year later when we came to preparing the pitch for the banks, it was very concrete and thoroughly elaborated.”

With the structure and characteristics of the new facility agreed, in the summer of 2023, the information memorandum was completed. The RFP documents were then issued to the group of banks identified as a good match. In addition to Royal FloraHolland’s existing lenders, a few other banks and the European Investment Bank (EIB) were invited to participate in the process.

Coaxing banks out of their comfort zone

Royal FloraHolland might be midway through a significant transformation strategy, but the ethos at the heart of its business model remains unchanged—connecting growers and buyers to make it easier to trade and do business together, to achieve the best possible market prices for flowers and plants and to unite members to tackle the challenges facing the future of their industry. A large driver behind the organization’s success is its structure as a cooperative. Royal FloraHolland is owned and works primarily in the interest of its members. In order for banks to understand the value of this unique approach required a pitch that was sufficiently compelling to convince banks to step outside of their comfort zone.

“We are a cooperative, and this is not a normal company and that's sometimes hard for banks to understand,” says Wilco van de Wijnboom, Corporate Finance Manager for Royal FloraHolland. “What is it? How does it work? How is our financial model designed? Why are we not making that much profit?”

In addition, unlike more conventional agricultural cooperatives, Royal FloraHolland never owns any products. Because all proceeds from sales through the platform go directly to the growers, funding is not generated through the profit made on selling products. Instead, Royal FloraHolland finances its operations primarily by charging an annual service fee to its members. By removing the cooperative’s interest in the profit derived from trade transactions, it is free to focus its role on enabling the easy exchange of floral products between grower and buyer parties for the best possible price. This is a sound strategy for Royal FloraHolland, but it is not a profit-driven enterprise that fits neatly into the banks’ standard credit rating and modeling processes.

“We have a different business model,” explains David. “Our traded volumes yield €5.5 billion. The service fees derived from the trades generate €500 million. We just raise the tariffs enough every year to breakeven. But the banks want to see profitability. Conceptually, it's very difficult for a bank.”

“Zanders gave us guidelines on how to build the case for the banks, Because many of our investments in the coming years are in sustainability, they advised us to introduce this into the framing of the refinancing and this was an interesting addition to the discussions we had with banks.”

Wilco van de Wijnboom, Corporate Finance Manager for Royal FloraHolland

Building the credit story

Without profit as a leverage for raising finance, Royal FloraHolland needed to carefully frame its refinancing pitch to appeal to the banks and satisfy their due diligence. For this reason, Zanders worked with Royal FloraHolland to demonstrate the soundness of the business, in particular emphasizing its diversification and the crucial role of the cooperative and the platform for the sector. In addition, they introduced sustainability as an extra angle for discussion.

“Zanders gave us guidelines on how to build the case for the banks,” Wilco explained. “Because many of our investments in the coming years are in sustainability, they advised us to introduce this into the framing of the refinancing and this was an interesting addition to the discussions we had with banks.”

Royal FloraHolland is committed to promoting sustainability throughout the floriculture value chain. From reducing CO2 emissions through smarter logistics and investing in more energy-efficient real estate to encouraging the use of more innovative methods to reduce the climate impact of the floriculture sector, such as LED lighting and geothermal and solar energy. The cooperative’s sustainability ambitions became an interesting lever during the refinancing negotiations and made an important contribution to the positive reaction from the banks to the refinancing.

Securing the right terms

The strength of the proposal meant ultimately the refinancing was agreed swiftly, with the agreement signed and sealed in March 2024, well ahead of their previous facility maturing. “From the beginning of the discussions with the banks until we signed the contract was seven months—we did it all in seven months,” Wilco remembers.

This armed Royal FloraHolland with a financing agreement with three banks worth €210 million, giving the group access to both the additional capital they need to invest in its growth strategy and the credit line to absorb fluctuations in liquidity due to business operations. Securing favorable terms (when at times it felt against the odds) is something they largely credit to being able to leverage Zanders’ market knowledge and experience and their handling of the negotiations with banks. This was particularly valuable when it came to addressing the large disparity in the initial quotes received from the banks.

“I realized more than ever during this process how important it is that Zanders was doing most of the negotiations - this was very important,” David adds. “The banks know that Zanders oversees the market so they also know they can't fool Zanders. Plus, it is in the interest of Zanders commercially, to remain a reliable partner and this means not bluffing too much to banks. This adds trust to the negotiation process. And we needed that, especially when working with the banks to adjust their quotes so they were in line with each other.”

The value of independence

This project underscores the value of having an independent debt advisor to navigate your company through the complexities of structuring credit facilities. From developing a compelling business case to present to banks to securing the most beneficial terms for corporate financing agreements, Zanders supports its clients throughout the entire process.

For more information on Zanders’ debt advisory and refinancing expertise, please contact Koen Reijnders.

In 2027, SAP will end its support for SAP ECC. Having spent years honing their ERP system to perfectly fit their business needs, this posed a challenge for Dutch network company Alliander – how and when to move to SAP S/4HANA.

There are risks in undertaking any big treasury transformation project, but the risks of not adjusting to the changing world around you can be far bigger. Recognizing the potential pitfalls of relying on an outdated (and soon to be unsupported) SAP ECC system, Alliander embarked on a large-scale, business-wide transition to SAP S/4HANA. Zanders advised on the Central Payments and Treasury phase of this project, which completed in May 2024.

A future-focused perspective

Network company, Alliander, is the Netherlands’ biggest decentralized grid operator, responsible for transporting energy to households and businesses, 24 hours a day, 7 days a week. As a driving force behind the energy transition, the business is committed to investing in innovation - and this extends to how they are future-proofing their business operations as well as their contribution to shaping the sustainable energy agenda.

With their SAP ECC system approaching end of life, Alliander embarked on a company-wide switch to SAP S/4HANA. However, transitioning to SAP’s newest ERP platform is not just another simple upgrade, it’s a completely new system built on top of the software company’s own in-memory database HANA. For a business of Alliander’s size and complexity, this is a huge undertaking and a lengthy process. In order to minimize the disruption and potential risks to mission-critical business systems, Alliander has started the transition early, breaking down the implementation into a series of logically ordered phases. This means individual business areas are migrated to S/4HANA as separate projects.

“In finance, this transition started about four years ago with the transition of Central Finance to S/4—that was the first stepping stone,” says Thijs Lender, Financial Controller and Alliander’s Project Owner for SAP S/4HANA in Finance. “The second major project was Central Payments and Treasury. From a business point of view, this was the first real business finance process that we implemented on S/4.”

Central Payments and Treasury was selected as a critical gateway to moving other business areas to the new target infrastructure, for example, purchasing. It was also an ideal test ground for the migration process from ECC to S/4HANA as Alliander’s cash management processes operate in relative isolation, therefore presenting a lower risk of collateral damage across other business operations when the department moved to the new system. ''Treasury and Central Payments is at end of the of the source-to-pay and order-to-cash process—it’s paying our invoices and collecting money,” explains Guido Tabor, Digital Lead Finance at Alliander. “This means it could be moved to the target architecture without impacting other areas.”

Greenfield or brownfield?

The two most common pathways to SAP S/4HANA are a greenfield approach and a brownfield approach. For a brownfield migration a company’s existing processes are converted into the new architecture. In contrast, the greenfield alternative involves abandoning all existing architecture and starting from scratch. The second is a far more extensive process, requiring a business to often make wide-ranging changes to work practices, reengineering processes in order to optimally standardize their workflows. As Alliander’s business had changed significantly over the period of running SAP ECC, they recognized the benefit of starting from a clean slate, building their new ERP system from scratch to meet their future business needs rather than trying to retro fit their existing system into a new environment.

“We really wanted to bring it back to best practices, challenging them and standardizing our processes in the new system,” adds Thijs. “In the old way, we had some ways of working that were not standard. So, there were sometimes tough discussions, and we had to make choices in order to achieve standard processes.”

A collaborative approach

While the potential benefits of greenfield migrations are substantial, untangling legacy processes and building a new S/4HANA system from scratch is a complex undertaking. Success hinges on the collaboration of various stakeholders, including experts with understanding of the inner workings of the SAP architecture.

“From the very beginning, we didn't see this as an IT project,” Guido says. “IT was involved but also the business - in this case, finance from a functional perspective, and also Zanders and the Alliander technical team. It was really a joint collaboration.”

Zanders worked alongside Alliander right from the early stages of the Central Payments and Treasury project. From helping them to strategically assess their treasury processes through to planning and implementing the transition to SAP S/4HANA. Having worked with the business previously on the ECC implementation for Central Payments and Treasury, Zanders’ knowledge of Alliander’s current environments combined with their specialist knowledge of both treasury and SAP S/4HANA meant the team were well placed to guide the team through the migration process. The strength of the partnership was particularly important when the timing of the deployment was brought forward.

“Initially we wanted to go live shortly before quarter close” Guido recalls “Then at the beginning of January, we had a discussion with our CFO about the deployment. With June 1 being very close to June 30 half year close, we decided we didn't want to take the risk of going live on this date, and he challenged us to move it back to the middle of May.”

What became really important was having a partner [Zanders] who helps you think out of the box. What's the possibility? How can you deal with it? While also being agile in supporting on fast changes and even faster solutions.

Guido Tabor, Digital Lead Finance at Alliander.

Adopting a 'Fix It' mindset

With the new deadline set, the team were encouraged by the CFO to adopt a ‘fix it’ mindset. This empowered them to take a bold, no compromises approach to implementation. For example, they were resolute in insisting on a week-long payment freeze ahead of the transition, despite pleas for leniency from some areas of the business. This confident, no exceptions approach (driven by the ‘fix it’ mentality) ensured the transition was concluded on time leading to a seamless transition of Central Payments and Treasury to the new S/4HANA system.

“This was a totally new perspective for us,” says Guido. “With go live processes or transitions like this, there will be some issues. But it didn't matter what, it didn't matter how, we just had to fix it. What became really important was having a partner [Zanders] who helps you think out of the box. What's the possibility? How can you deal with it? While also being agile in supporting on fast changes and even faster solutions.”

Central Payments and Treasury project went live on S/4HANA in May 2024, on time and with a smooth transition to the new system.

“I was really happy on the first Monday after go-live and in that early week that there weren't big issues,” Guido says. “We had some hiccups, that's normal, but it was manageable and that's what is important.”

This project represented an important milestone in Alliander’s transition to SAP S/4HANA. Successfully and smoothly shifting a core business process into the new architecture clearly progressed the company past the point of turning back. This reinforced momentum for the wider project, laying robust foundations for future phases.

To find out how Zanders could help your treasury make the transition from SAP ECC to SAP S/4HANA, contact our Director Marieke Spenkelink.

How can a non-profit organization operating on a global stage safeguard itself from foreign currency fluctuations? Here, we share how our ‘Budget at Risk’ model helped a non-profit client more accurately quantify the currency risk in its operations.

Charities and non-profit organizations face distinct challenges when processing donations and payments across multiple countries. In this sector, the impact of currency exchange losses is not simply about the effect on an organization’s financial performance, there’s also the potential disruption to projects to consider when budgets are at risk. Zanders developed a ‘Budget at Risk’ model to help a non-profit client with worldwide operations to better forecast the potential impact of currency fluctuations on their operating budget. In this article, we explain the key features of this model and how it's helping our client to forecast the budget impact of currency fluctuations with confidence.

The client in question is a global non-profit financed primarily through individual contributions from donors all over the world. While monthly inflows and outflows are in 16 currencies, the organization’s global reserves are quantified in EUR. Consequently, their annual operating budget is highly impacted by foreign exchange rate changes. To manage this proactively demands an accurate forecasting and assessment of:

- The offsetting effect of the inflows and outflows.

- The diversification effect coming from the level of correlation between the currencies.

With the business lacking in-house expertise to quantify these risk factors, they sought Zanders’ help to develop and implement a model that would allow them to regularly monitor and assess the potential budget impact of potential FX movements.

Developing the BaR method

Having already advised the organization on several advisory and risk management projects over the past decade, Zanders was well versed in the organization’s operations and the unique nature of the FX risk it faces. The objective behind developing Budget at Risk (BaR) was to create a model that could quantify the potential risk to the organization’s operating budget posed by fluctuations in foreign exchange rates.

The BaR model uses the Monte Carlo method to simulate FX rates over a 12-month period. Simulations are based on the monthly returns on the FX rates, modelled by drawings from a multivariate normal distribution. This enables the quantification of the maximum expected negative FX impact on the company’s budget over the year period at a certain defined level of confidence (e.g., 95%). The model outcomes are presented as a EUR amount to enable direct comparison with the level of FX risk in the company’s global reserves (which provides the company’s ‘risk absorbing capacity’). When the BaR outcome falls outside the defined bandwidth of the FX risk reserve, it alerts the company to consider selective FX hedging decisions to bring the BaR back within the desired FX risk reserve level.

The nature of the model

The purpose of the BaR model isn’t to specify the maximum or guaranteed amount that will be lost. Instead, it provides an indication of the amount that could be lost in relation to the budgeted cash flows within a given period, at the specified confidence interval. To achieve this, the sensitivity of the model is calibrated by:

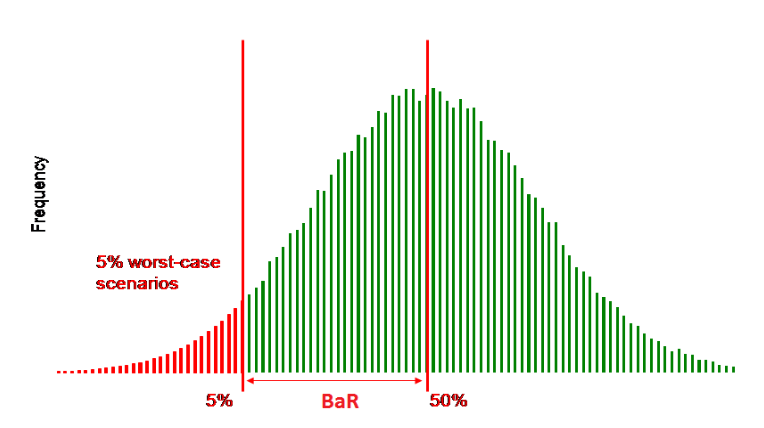

- Modifying the confidence levels. This changes the sensitivity of the model to extreme scenarios. For example, the figure below illustrates the BaR for a 95% level of confidence and provides the 5% worst-case scenario. If a 99% confidence level was applied, it would provide the 1% worst (most extreme) case scenario.

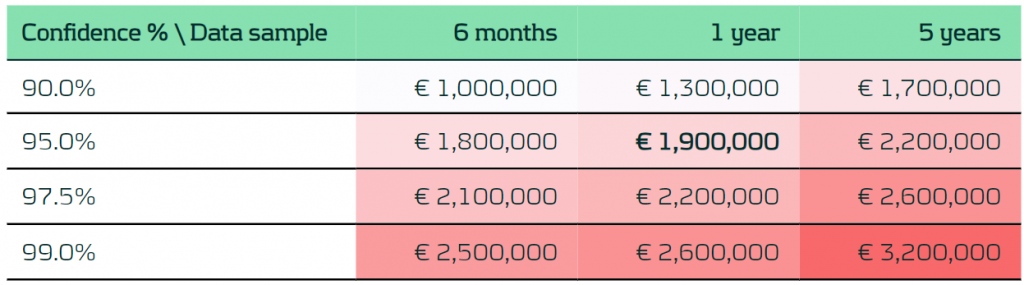

- Selecting different lengths of sample data. This allows the calculation of the correlation and volatility of currency pairs. The period length of the sample data helps to assess the sensitivity to current events that may affect the FX market. For example, a sample period of 6 months is much more sensitive to current events than a sample of 5 years.

Figure 1 – BaR for a 95% level of confidence

Adjusting these parameters makes it possible to calculate the decomposition of the BaR per currency for a specified confidence level and length of data sample. The visual outcome makes the currency that’s generating most risk quick and easy to identify. Finally, the diversification effect on the BaR is calculated to quantify the offsetting effect of inflows and outflows and the correlation between the currencies.

Table 1 – Example BaR output per confidence level and length of data sample

Pushing parameters

The challenge with the simulation and the results generated is that many parameters influence the outcomes – such as changes in cash flows, volatility, or correlation. To provide as much clarity as possible on the underlying assumptions, the impact of each parameter on the results must be considered. Zanders achieves this firstly by decomposing the impact by:

- Changing FX data to trigger a difference in the market volatility and correlation.

- Altering the cash flows between the two assessment periods.

Then, we look at each individual currency to better understand its impact on the total result. Finally, additional background checks are performed to ensure the accuracy of the results.

This multi-layered modeling technique provides base cases that generate realistic predictions of the impact of specific rate changes on the business’ operating budget for the year ahead. Armed with this knowledge, we then work with the non-profit client to develop suitable hedging strategies to protect their funding.

Leveraging Zanders’ expertise

FX scenario modeling is a complex process requiring expertise in currency movements and risk – a combination of niche skills that are uncommon in the finance teams of most non-profit businesses. But for these organizations, where there can be significant currency exposure, taking a proactive, data-driven approach to managing FX risk is critical. Zanders brings extensive experience in supporting NGO, charity and non-profit clients with modeling currency risk in a multiple currency exposure environment and quantifying potential hedge cost reduction by shifting from currency hedge to portfolio hedge.

For more information, visit our NGOs & Charities page here, or contact the authors of this case study, Pierre Wernert and Jaap Stolp.

Embarking on a transformative journey to strengthen its treasury function, an international non-governmental organization turned to Zanders for guidance to elevate its operations to the highest industry standards.

A force for change

The NGO sector today is facing a multitude of conflicting pressures. Growing humanitarian need has heightened the pressure on these organizations to change the world, but a constantly shifting landscape means they also need to radically change themselves in order to remain compliant and able to manage their financial operations effectively.

In mid-2022, a prominent NGO appointed Zanders to conduct a comprehensive review and benchmarking of its treasury function. Operating in more than 80 countries, the NGO’s treasury team of 30 dedicated professionals managed a diverse array of banking relationships and accounts. Finely tuned treasury processes and systems are critical to managing such a sprawling financial ecosystem, and the team was aware they needed a more innovative response to their sector’s ever-evolving treasury landscape.

Despite implementing a Treasury Management System (TMS) two years previously, the team was still relying on a large number of manual processes. Recognizing the imperative of automating more of its treasury operations, they asked Zanders to conduct an in-depth assessment to evaluate their performance, benchmark it against industry best practices and to identify areas for improvement.

Clarifying the current state

The primary objectives of the project were manifold: to evaluate the existing setup, identify potential financial and operational risks, define improvement opportunities, design a roadmap, and ultimately, deliver tangible value to the treasury team. Achieving these goals relied on first gaining the clarity provided by a thorough benchmarking exercise.

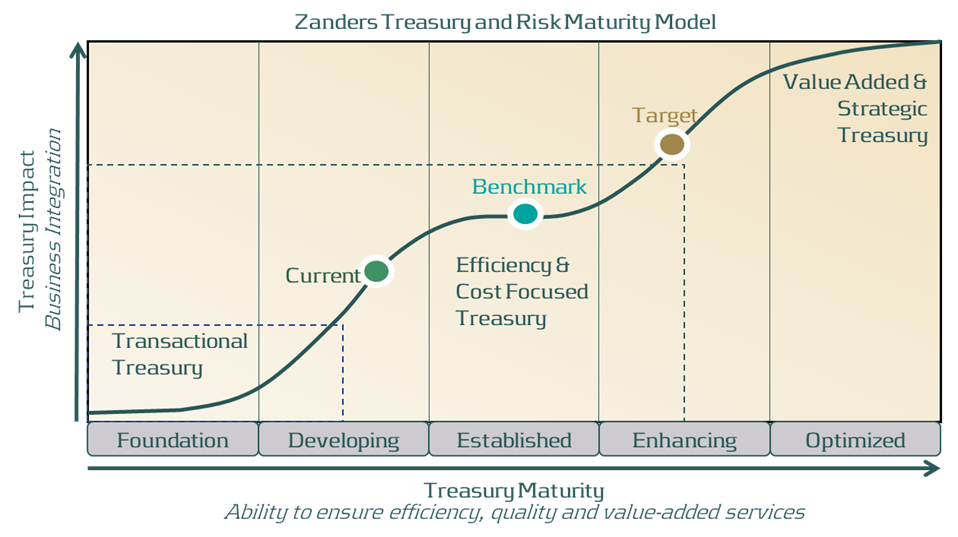

Leveraging its proprietary Treasury and Risk Maturity Model, Zanders performed a deep dive into the organization’s treasury function. By considering and scoring all treasury activities as well as the teams, controls and technologies involved in delivering them, the team modeled the ‘as-is’ situation in a highly structured and meaningful way. When measured against market best practices, this provided a sector-calibrated benchmark from which areas for improvement were identified. The outcomes of this exercise allowed Zanders to develop new targets for the NGO’s treasury function that were then used to design a framework for the future.

A new treasury roadmap

Using Zanders’ Treasury and Risk Maturity Model, the NGO's treasury function was classified as ‘Developing’. This highlighted a number of areas where there was an opportunity to make improvements that would facilitate their advancement towards an ‘Enhancing’ level of treasury maturity. Zanders then collaborated closely with the organization to devise a comprehensive roadmap. This outlined actionable steps designed to elevate performance in the key areas identified and also prescribed follow-up initiatives to provide a structure for their implementation.

This triggered the launch of a series of strategic initiatives aimed at strengthening the NGO’s treasury capabilities. For example, a thorough fit-gap analysis of the existing TMS was undertaken as well as a deep dive into the treasury function’s organizational design. This led to targeted enhancements and optimization measures designed to increase efficiency and resilience within the treasury organization. Central to this endeavor was the prioritization of automating manual processes and streamlining accounting procedures.

From functional to future-ready

By leveraging Zanders' expertise and adopting a proactive approach to treasury management, the NGO has positioned itself on a trajectory of sustained growth and operational excellence. Armed with a strategic roadmap and fortified by targeted improvements, the NGO’s treasury team is not only prepared to navigate the complexities of the global financial landscape with confidence and agility but also fully equipped to transition from a cost-focused to a value-added role. For more information, visit our NGOs & Charities page here, or contact the author of this case study, Joanne Koopman.

When the impending maturity of C. Steinweg’s group credit facility prompted the company to re-evaluate another debt facility at the same time, Zanders provided the expertise to attract a new pool of banks and secure a more flexible financing structure for the business.

C. Steinweg Group is a market-leading logistics and warehousing company with over 6,250 employees and warehouses and terminals that span more than 100 locations in 55 countries worldwide. With 175 years plus experience of storage, handling, forwarding and chartering services throughout the world, the company is a renowned and respected logistics partner for the global commodity trade.

Over its long history, Steinweg has demonstrated agility and resilience, responding to market challenges through innovating its approach to logistics and warehousing services and showing relentless commitment to customer services. Over the years, the business has also diversified into commodity financing as an added value service to its logistics and warehousing activities. At the end of 2022, the company appointed Zanders to advise them on the refinancing of two debt facilities. The aim was to provide the business with the robust and flexible access to capital they needed to continue to support, scale and grow their international operations.

The refinancing project comprised of two core requirements:

- The refinancing of Steinweg’s group credit facility.

- A new, more flexible credit facility for the commodity finance subsidiary.

Due to an overlap in the counterparties invited to participate in the two transactions, Steinweg saw the efficiency potential of taking both of the transactions to market simultaneously. But this also added complexity in terms of arranging and managing the refinancing process and procedures.

It was not a standard refinancing

Pim Van Der Heijden, C. Steinweg Group

“There was a certain complexity to this project, because the refinancings were interrelated from various perspectives,” says Pim Van Der Heijden, Steinweg’s group treasurer and global head of commodity finance. “It was not a standard refinancing. Especially the commodity financing activity, where we didn't go for just a straightforward, typical trade financing credit facility. We were putting something in place which was not only new for us but also for lenders and the legal counsels involved—we had to get them a little bit out of the comfort zone.”

Steinweg recognised early that they would need external support from a debt advisor to help get banks on board with this more innovative structure and also to optimize the value they would get from the refinancing process as well as adding capacity to the team. Zanders had previously worked with Steinweg when its group credit facility was first renewed in 2017, and this experience contributed to the appointment of Zanders to assist them with the new refinancing transactions.

“We approached a few advisors, but we selected Zanders based on track record and pricing,” Van Der Heijden adds. “We know Zanders and we had a good relationship with them, so we had confidence that they could deliver what we were looking for.”

Advice grounded in robust understanding of market practice

As well as their history and established relationship with Steinweg, it was also Zanders’ experience in the market that influenced their appointment on this project. Whereas a company will go to the market every five or seven years to refinance facilities, Zanders is continuously working with lenders on these transactions. This empowers them with current know-how on market practice regarding terms and pricing. Steinweg recognized the value this could bring to their process.

“It really helps to have a debt advisor who has insights into what's happening in the market, what is possible and what is not possible based on actual transactions—they understand how banks work and what is achievable,” Van Der Heijden says. “When Zanders came up with this alternative structure for the commodity financing facility, there was a certain amount of risk involved with going forward with it. This was however one of the reasons that we started the process early, this gave us time to sound and refine the structure. In addition, we knew that we were in good hands, and we ended up getting the results we wanted from it in terms of gaining flexibility that previously wasn't available and might not have been available with a more conventional approach.”

With the maturity of the group credit facility looming in July 2024, this transaction was mission critical and the driving force behind the timing of the combined refinancing project.

“We wanted to start early, and we set the goal to have the new group financing in place before the end of the year 2023,” says Van Der Heijden. “We started preparing by selecting Zanders as a debt advisory partner at the end of 2022, ready to start the process in early 2023, leaving time to complete the transaction by the end of that year.”

A resilient process

The process started with Zanders sitting down with Steinweg to discuss their objectives and requirements for the refinancing. Various scenarios were then modelled before finalizing the structure and characteristics of the new facilities. The RFP documents were then issued to the group of banks identified as a good match. In this case, six banks were invited to pitch—Steinweg’s existing lenders and a selection of additional lenders that matched the required criteria. Zanders’ attention then turned to collecting responses and creating term sheets for the new credit facilities, starting with the group financing.

When it comes to refinancing processes, it’s always wise to prepare for all scenarios. In this case, particularly given the progressive structure of the new facilities, it was important to be prepared for the eventuality that a lender could opt to exit the process. For this reason, more banks than strictly required were invited to participate.

“The new structure was a bit off the beaten track and while we were keen to push new boundaries, we had to be prepared for the reality that some lenders might not share our enthusiasm,” remembers Van Der Heijden. “This approach paid off when an existing lender decided not to participate. Rather than unsettling the process, instead it served to reassure us that the strategy to include more than just our existing bank in the process was good. And it all worked out.”

Due to the highly structured approach and extensive project set-up, when changes occurred there were provisions in place to ensure they caused minimal disruption to the process. This approach ultimately enabled Steinweg to secure competitive pricing and terms for their new group facility. And importantly, this was achieved comfortably ahead of the deadline set by the maturity of their previous agreement.

While the two financing processes ran in parallel, due to the impending maturity of the group facility, securing this was the primary focus initially. Once the group facility was agreed, attention shifted to the commodity financing facility. Steinweg was looking to increase their credit facility, to give them scalable access to more flexible funding to finance commodities on behalf of its clients. Previously, bilateral loan agreements were used to fund this aspect of the business leading to funding inefficiencies. “We had some goals we wanted to achieve with this new funding structure,” says Van Der Heijden. “The most critical was, of course, securing scalable financial headroom, but flexibility was almost as important.”

To deliver this more scalable and flexible access to credit, Zanders modelled a facility that allowed multiple banks to provide funding for commodity financing under the same loan. As an atypical arrangement, it required Zanders to work closely with each counterparty to gain their support for this novel structure.

“The new structure was relatively off the beaten track, but it provided what we needed, which is a lot of flexibility,” says Van Der Heijden. “And the flexibility it gives us is now paying off daily. We can now have three banks participating in a loan and other banks can also be added to the structure as well.”

Reaping the benefits

The new commodity financing facility not only provides essential access to more sources of funding, but also enables Steinweg to react quicker to opportunities and deliver faster, more seamless commodity financing solutions to its customers.

“The group facility was a lifeline, whereas the credit facility for the commodity financing activities was more of a ‘nice to have’ but now it's really adding value in terms of enabling us to pursue growth,” says Van Der Heijden. “We no longer have to talk to our lenders every time we go to market and that really pays off. Previously, if we had a new commodity financing prospect, we sometimes had to wait two weeks to get an answer from our banks to see if we can use the funding. Now, as long as we’re comfortable that it's within the pre-agreed rules, we can pretty much reply to them the same day.”

Conclusion

This project was not only strategically critical for Steinweg but also represented a bold departure from their existing financing agreements. With Zanders’ guidance, they were able to pursue this ambitious approach with confidence and conclude both of the refinancing projects before the end of 2023. This gave the team the peace of mind that their funding was agreed well ahead of their group facility maturing.

This project underscores the value of having an independent debt advisor to navigate your company through the complexities of structuring credit facilities. From ensuring essential deadlines are achieved and developing innovative structures to maintaining the momentum for the process and securing the most beneficial terms with banks. For more information on Zanders' debt advisory and refinancing expertise, contact Koen Reijnders and visit our Corporate finance page.

Transforming financial crime data management from reactive compliance to strategic insight.

We have helped a Dutch bank with over 500 billion in assets understand and realize their data ambitions regarding customer due diligence, sanctions, transaction monitoring, and fraud.

Challenge

Entering the final stages of remediation, the bank wishes to develop a best-in-class data strategy in the financial crime domain. Having spent the last few years focusing on ensuring short-term compliance, the management team requested Zanders’ help to transition into an institution capable of tackling financial crime proactively.

This project aligns with a wider trend in the financial industry, where institutions, after addressing regulatory findings, invest in augmenting and automating their financial crime systems as a stepping stone toward an integration phase with a holistic view of client risk.

Solution

Zanders proposed a three-step approach:

- Step 1: Determine the current maturity state

- Step 2: Work along with stream leads to determine ambition

- Step 3: Create and execute a roadmap to guide the bank through until 2027

In Step 1, we determined the current state of data management regarding customer due diligence (CDD), sanctions, transaction monitoring (TM), and fraud. Since data is a multifaceted and all-encompassing element of an institution’s fight against financial crime, we divided our investigation into six key themes. This structure allowed for better alignment with stream leads within the bank while also enabling comparisons with best practices across the financial industry.

During Step 2, we assisted stream leads in identifying pain points and future objectives, thereby developing ambitions for each of the six themes. These ambitions balanced the bank’s desire to foster a cutting-edge data policy while still being actionable given the available resources—technical and otherwise.

Finally, in Step 3, not only did we bring all ambitions together into a coherent roadmap defining the data strategy through 2027, but we also began executing this roadmap immediately, minimizing the time between vision and realization to maximize value creation.

Moreover, a key deliverable was a comprehensive overview of the primary dataflows between departments. Our experience shows that, in trying to ensure short-term compliance, financial institutions often inherit a legacy of tangled dataflows, where data origins are obscured and key features are redundantly recalculated.

The first step toward resolving this issue was to carefully analyze how data flows between different pillars (Transaction Monitoring, KYC, Fraud Detection, and Sanctions). Once identified, inefficiencies and vulnerabilities were addressed through improved architecture and governance.

Making the Data Transformation Visual

The broad scope of this project, combined with the large amount of data it involves, poses a risk that stakeholders may struggle to stay informed about developments and decisions.

That’s why, from the very beginning, we committed to visualizing the ongoing transformations by creating a Data Initiative Dashboard to track progress on key data initiatives. This tool enables leadership to monitor and adjust priorities throughout the execution phase and establishes a gold standard for reporting future initiatives in an informative and intuitive manner.

For more information, visit our Financial Crime Prevention page, or reach out to Johannes Lont, Senior Manager.

Cutting costs and increasing accuracy with automated periodic reviews.

Our client faced a challenge with a large volume of KYC/CDD reviews that needed to be conducted periodically, but many did not contain material CDD risks. Zanders supported the development and management of the PR automation model, which automates cases requiring limited research and allows analysts to focus on more complex, high-risk cases.

Challenge

The traditional approach to CDD case handling requires significant manual effort by analysts. However, many cases that require minimal investigation are still reviewed manually. As a result, the current approach is neither risk-based nor cost-effective.

Typically, a Client Risk Rating model classifies clients as low, medium, or high risk. These clients are then reviewed at set intervals, such as every five, three, or one year(s), respectively. During these periodic reviews, analysts spend considerable time reviewing cases with no significant changes since the last manual review. This process is inefficient, and improvements can be made to make it more risk-based.

Solution

The PR automation model identifies cases that require minimal research and processes them automatically. The process begins with analyzing the current group of clients. From this large dataset, a subset of low-risk clients is identified based on expert knowledge combined with data analysis.

Next, the model determines which additional automated checks are necessary to ensure that the case has not undergone material changes since the last manual review. With these additional checks in place, the case can be processed automatically.

Automating PRs is only possible with a strong data foundation. Zanders assisted not only in developing the PR model but also in ensuring that data quality meets the necessary standards.

Performance

The PR automation model delivers significant cost savings while improving the efficiency and effectiveness of CDD case handling. Additionally, Zanders supports clients in demonstrating to regulators that this model helps transition to a more risk-based CDD approach.

For more information, visit our Financial Crime Prevention page, or reach out to Johannes Lont, Senior Manager.

Managing over 80 intercompany loans annually and with a wide geographical scope, Royal Philips faced the challenge of complying with their Transfer Pricing obligations.

Zanders Transfer Pricing Suite is an innovative, cloud-based solution designed for companies looking to automate the Transfer Pricing compliance of financial transactions. With over five years of experience and trusted by more than 60 multinational corporations, the platform is the market-leading solution for financial transactions Transfer Pricing. On March 31, 2023, Zanders and Royal Philips jointly presented the conference "How Philips Automated Its Transfer Pricing Process for Group Financing" at the DACT (Dutch Association of Corporate Treasurers) Treasury Fair 2023.

Context

The publication of Chapter X of Financial Transactions by the OECD, as well as its incorporation into the 2022 OECD Transfer Pricing Guidelines, has led to an increased scrutiny by tax authorities. Consequently, transfer pricing for financial transactions, such as intra-group loans, guarantees, cash pools, and in-house banks, has become a critical focus for treasury and tax departments.

ZANDERS TRANSFER PRICING SOLUTION

As compliance with Transfer Pricing regulations gains greater significance, many companies find that the associated analyses consume excessive time and resources from their in-house tax and treasury departments. Several struggle to automate the end-to-end process, from initiating intercompany loans to determining the arm's length interest, recording the loans in their Treasury Management System (TMS), and storing the Transfer Pricing documentation.

Since 2018, Zanders Transfer Pricing Solution has supported multinational corporations in automating their Transfer Pricing compliance processes for financial transactions.

ROYAL PHILIPS CASE STUDY

Managing over 80 intercompany loans annually and with a wide geographical scope, Royal Philips faced the challenge of complying with their Transfer Pricing obligations. During the conference, Joris Van Mierlo, Corporate Finance Manager at Philips, detailed how Royal Philips implemented a fully integrated solution to determine and record the arm's length interest rates applicable to its intra-group loans.

Revolutionizing Bolt’s Treasury: Efficiency, Reliability, and Growth

Mid 2023, Bolt successfully implemented its new full-fledged treasury management system (TMS). With assistance of Zanders consultants, the mobility company implemented Kyriba – a necessity to support Bolt’s small treasury team. As a result, all daily processes are almost completely automated. “It's about reliability.”

Bolt is the leading European mobility platform that’s focused on more efficient, convenient and sustainable solutions for urban travelling. With more than 150 million customers in at least 45 countries, it offers a range of mobility services including ride-hailing, shared cars and scooters, food and grocery delivery. “Bolt was founded by Markus Villig, a young Estonian guy who quit his school to start this business with €5,000 that he borrowed from his parents,” says Mahmoud Iskandarani, Group Treasurer at Bolt. “He built an app and started to ask drivers on the street to download it and try it out. Now we have millions of drivers and passengers, almost 4,000 employees and several business lines. Last August, we celebrated our 10th anniversary. So, we have one of the fastest growing businesses in Europe. And our ambition is to grow even faster than so far.”

Driven by technology

Because of its fast growth, Bolt’s Treasury team decided to look for a scalable solution to cope with the further expansion of the business. Freek van den Engel, Treasury manager at Bolt: “We needed a system that could automate most of our daily processes and add value. Doing things manually is not efficient and risks are high. To help us scale up while maintaining efficiency, we needed our Treasury to be driven by technology.”

Iskandarani adds: “Meanwhile, our macro environment is changing and we had some bank events. In the past years, startups or scale-ups have seen big growth and didn't focus too much on working capital management. Interest rates were low, which made it easy to raise money from investors. Now, we need to make sure that we manage our working capital the right way so that we can access our money, mitigate risks, and that we get a decent return on our cash. That’s when it's controlled by Treasury and invested correctly.”

Choosing Kyriba

Van den Engel led a treasury system selection process three years ago for his previous employer, where he also worked together with Iskandarani. “That experience helped us to come up with a shortlist of three providers, instead of having a very long RfP process looking at a long list of vendors. We started the selection process in June 2022 and two months later we chose Kyriba because of its strong functionality. Also, it’s a solution offered as SaaS, which means we don't have to worry about upgrades – a very important reason for us. Kyriba has been working with tech companies similar to ours. Another decisive factor was their format library, called Open Format Studio. It allows us to use self-service when it comes to configuring payment formats, reducing our costs and turn-around time when expanding to new geographies.”

Implementation partner

For Bolt, Kyriba will function as in-house bank system, and support its European cash pool. During the selection process, the team had some reference calls with other Kyriba users to discuss experiences with the system and the implementation. “One piece of feedback we received was that it works very well to bring in implementation partners to complete such a project successfully. Zanders stood out, because of its proven track record and the awards it had won. Also, Mahmoud and I both had experience with Zanders during some projects at our previous employer. That’s why we asked them to be our implementation partner.”

In October 2022, the implementation process started. In July 2023, the system went live. Kyriba’s TMS solution covered all treasury core processes, including cash position reporting (including intra-day balance information), liquidity management, funding, foreign exchange with automatic integration to 360T and Finastra, investments, payment settlements and risk management.

Trained towards independency

As part of the implementation process, Zanders trained Bolt on how to use the new tool, and assisted in using the Open Format Studio. In this way, the team built the knowledge and experience needed to roll out to new countries more independently.

Van den Engel: “We aimed to be independent and do as much as possible ourselves to reduce costs and build up in-house expertise on the system. Zanders helped us figuring out what we wanted, explained and guided us, and showed what the system can do and how to align that with our needs in the best possible way. Once we were clear on the blueprint, they helped us with our static data, connectivity and initial system set-up. After the training they led, we were able to do most of it ourselves, including the actual system configuration work, for which Zanders had laid the foundation.”

Rolling out the payment hub

With assistance of Zanders consultants, Bolt also set up a framework to roll out the payment hub, for the vendor payments from its ERP system called Workday and its payroll provider, Immedis. The consultants assisted with configuration of initial payment scenarios and workflows. “We made the connections, tested them and did a pilot with Workday last summer. After training and with the experience that we've built up using Open Format Studio, we can roll out to new countries and expand it ourselves. Starting in August, we continued to roll out Kyriba’s payment hub to more countries, and to implement Payroll. With the payment hub we are now live in 16 countries and that's basically fully self-serviced. Apart from some support for specialized cases, we don’t need support anymore for the payment hub.”

Many material benefits

Having a small hands-on project team meant no need for a complex project management organization to be set-up. Naturally Bolt and Zanders started using agile project management, with refocus of priorities to different streams as necessary. The Kyriba implementation project was closed within the set budget in 9 months’ time.

Iskandarani is happy with the results. “It is clear there are benefits of this implementation when it comes to efficiency and risk management. We now have the visibility over our cash and the fact that we have a system telling us that there’s an exposure that we should get rid of, that has a lot of value. Also, we have some financial benefits that we could not have achieved without the system. Today we can pool our cash better, we can invest it better, and we can handle our foreign exchange in a better way. Before this, we have overpaid banks.”

Reliability and control

“We could have hired more people”, Van den Engel adds. “But some things are just very difficult to do without this system. It's also about reliability. Even if you have a manual process in place that works, you will see it breaking down from time to time. If someone deletes a formula, or a macro stops working, that becomes very risky. It’s also about the control environment. As a company we're looking to become more mature and implement controls that should be there – that too is very difficult to do without a proper system that can generate these reports, be properly secured with all the right standards that we need to adhere to, or do fraud detection based on machine learning in the future. It's impossible to do all that manually. Those are material benefits, but hard to quantify.”

Preventing problematic debt situations or increase access to finance after default recovery?

In countries worldwide, associations of credit information providers play a crucial role in registering consumer-related credits. They are mandated by regulation, operate under local law and their primary aim is consumer protection. The Dutch Central Credit Registration Agency, Stichting Bureau Krediet Registratie (BKR), has reviewed the validity of the credit registration period, especially with regards to the recurrence of payment problems after the completion of debt restructuring and counseling. Since 2017, Zanders and BKR are cooperating in quantitative research and modeling projects and they joined forces for this specific research.

In the current Dutch public discourse, diverse opinions regarding the retention period after finishing debt settlements exist and discussions have started to reduce the duration of such registrations. In December 2022, the four biggest municipalities in the Netherlands announced their independent initiative to prematurely remove registrations of debt restructuring and/or counseling from BKR six months after finalization. Secondly, on 21 June 2023, the Minister of Finance of the Netherlands published a proposal for a Credit Registration System Act for consultation, including a proposition to shorten the retention period in the credit register from five to three years. This proposition will also apply to credit registrations that have undergone a debt rescheduling.

The Dutch Central Credit Registration Agency, Stichting Bureau Krediet Registratie (BKR) receives and manages credit registrations and payment arrears of individuals in the Netherlands. By law, a lender in the Netherlands must verify whether an applicant already has an existing loan when applying for a new one. Additionally, lenders are obligated to report every loan granted to a credit registration agency, necessitating a connection with BKR. Besides managing credit data, BKR is dedicated to gathering information to prevent problematic debt situations, prevent fraud, and minimize financial risks associated with credit provision. As a non-profit foundation, BKR operates with a focus on keeping the Dutch credit market transparent and available for all.

BKR recognizes that the matter concerning the retention period of registrations for debt restructuring and counseling is fundamentally of societal nature. Many stakeholders are concerned with the current discussions, including municipalities, lenders and policymakers. To foster public debate on this matter, BKR is committed to conducting an objective investigation using credit registration data and literature sources and has thus engaged Zanders for this purpose. By combining expertise in financial credit risk with data analysis, Zanders offers unbiased insights into this issue. These data-driven insights are valuable for BKR, lawmakers, lenders, and municipalities concerning retention periods, payment issues, and debt settlements.

Problem Statement

The Dutch Central Credit Registration Agency, Stichting Bureau Krediet Registratie (BKR) receives and manages credit registrations and payment arrears of individuals in the Netherlands. By law, a lender in the Netherlands must verify whether an applicant already has an existing loan when applying for a new one. Additionally, lenders are obligated to report every loan granted to a credit registration agency, necessitating a connection with BKR. Besides managing credit data, BKR is dedicated to gathering information to prevent problematic debt situations, prevent fraud, and minimize financial risks associated with credit provision. As a non-profit foundation, BKR operates with a focus on keeping the Dutch credit market transparent and available for all.

The research aims to gain a deeper understanding of the recurrence of payment issues following the completion of restructuring credits (recidivism). The information gathered will aid in shaping thoughts about an appropriate retention period for the registration of finished debt settlements. The research includes both qualitative and quantitative investigations. The qualitative aspect involves a literature study, leading to an overview of benchmarking, key findings and conclusions from prior studies on this subject. The quantitative research comprises data analyses on information from BKR's credit register.

External International Qualitative Research

The literature review encompassed several Dutch and international sources that discuss debt settlements, credit registrations, and recidivism. There is limited research published on recidivism, but there are some actual cases where retention period are materially shortened or credit information is deleted to increase access to financial markets for borrowers. Removing information increases information asymmetry, meaning that borrower and lender do not have the same insights limiting lenders to make well-informed decisions during the credit application process. The cases in which the retention period was shortened or negative credit registrations were removed demonstrate significant consequences for both consumers and lenders. Such actions led to higher default rates, reduced credit availability, and increased credit costs, also for private individuals without any prior payment issues.

In the literature it is described that historical credit information serves as predictive variable for payment issues, emphasizing the added value of credit registrations in credit reports, showing that this mitigates the risk of overindebtedness for both borrowers and lenders.

Quantitative Research with Challenges and Solutions

BKR maintains a large data set with information regarding credits, payment issues, and debt settlements. For this research, data from over 2.5 million individuals spanning over 14 years were analyzed. Transforming this vast amount of data into a usable format to understand the payment and credit behavior of individuals posed a challenge.

The historical credit registration data has been assessed to (i) gain deeper insights into the relationship between the length of retention periods after debt restructuring and counseling and new payment issues and (ii) determine whether a shorter retention period after the resolution of payment issues negatively impacts the prevention of new payment issues, thus contributing to debt prevention to a lesser extent.

The premature removal of individuals from the system of BKR presented an additional challenge. Once a person’s information is removed from the system, their future payment behavior can no longer be studied. Additionally, the group subject to premature removal (e.g. six months to a year) after a debt settlement registration constitutes only a small portion of the population, making research on this group challenging. To overcome these challenges, the methodology was adapted to assess the outflow of individuals over time, such that conclusions about this group could still be made.

Conclusion

The research provided BKR with several interesting conclusions. The data supported the literature that there is difference in risk for payment issues between lenders with and without debt settlement history. Literature shows that reducing the retention period increases the access to the financial markets for those finishing a debt restructuring or counseling. It also increases the risk in the financial system due to the increased information asymmetry between lender and borrower, with several real-life occasions with

increased costs and reduced access to lending for all private individuals. The main observation of the quantitative research is that individuals who have completed a debt rescheduling or debt counseling face a higher risk of relapsing into payment issues compared to those without debt restructuring or counseling history. An outline of the research report is available on the website of BKR.

The collaboration between BKR and Zanders has fostered a synergy between BKR's knowledge, data, and commitment to research and Zanders' business experience and quantitative data analytical skills. The research provides an objective view and quantitative and qualitative insights to come to a well informed decision about the optimal registration period for the credit register. It is up to the stakeholders to discuss and decide on the way forward.