Budget at Risk: Empowering a global non-profit client with a clearer steer on FX risk

How can a non-profit organization operating on a global stage safeguard itself from foreign currency fluctuations? Here, we share how our ‘Budget at Risk’ model helped a non-profit client more accurately quantify the currency risk in its operations.

Charities and non-profit organizations face distinct challenges when processing donations and payments across multiple countries. In this sector, the impact of currency exchange losses is not simply about the effect on an organization’s financial performance, there’s also the potential disruption to projects to consider when budgets are at risk. Zanders developed a ‘Budget at Risk’ model to help a non-profit client with worldwide operations to better forecast the potential impact of currency fluctuations on their operating budget. In this article, we explain the key features of this model and how it's helping our client to forecast the budget impact of currency fluctuations with confidence.

The client in question is a global non-profit financed primarily through individual contributions from donors all over the world. While monthly inflows and outflows are in 16 currencies, the organization’s global reserves are quantified in EUR. Consequently, their annual operating budget is highly impacted by foreign exchange rate changes. To manage this proactively demands an accurate forecasting and assessment of:

- The offsetting effect of the inflows and outflows.

- The diversification effect coming from the level of correlation between the currencies.

With the business lacking in-house expertise to quantify these risk factors, they sought Zanders’ help to develop and implement a model that would allow them to regularly monitor and assess the potential budget impact of potential FX movements.

Developing the BaR method

Having already advised the organization on several advisory and risk management projects over the past decade, Zanders was well versed in the organization’s operations and the unique nature of the FX risk it faces. The objective behind developing Budget at Risk (BaR) was to create a model that could quantify the potential risk to the organization’s operating budget posed by fluctuations in foreign exchange rates.

The BaR model uses the Monte Carlo method to simulate FX rates over a 12-month period. Simulations are based on the monthly returns on the FX rates, modelled by drawings from a multivariate normal distribution. This enables the quantification of the maximum expected negative FX impact on the company’s budget over the year period at a certain defined level of confidence (e.g., 95%). The model outcomes are presented as a EUR amount to enable direct comparison with the level of FX risk in the company’s global reserves (which provides the company’s ‘risk absorbing capacity’). When the BaR outcome falls outside the defined bandwidth of the FX risk reserve, it alerts the company to consider selective FX hedging decisions to bring the BaR back within the desired FX risk reserve level.

The nature of the model

The purpose of the BaR model isn’t to specify the maximum or guaranteed amount that will be lost. Instead, it provides an indication of the amount that could be lost in relation to the budgeted cash flows within a given period, at the specified confidence interval. To achieve this, the sensitivity of the model is calibrated by:

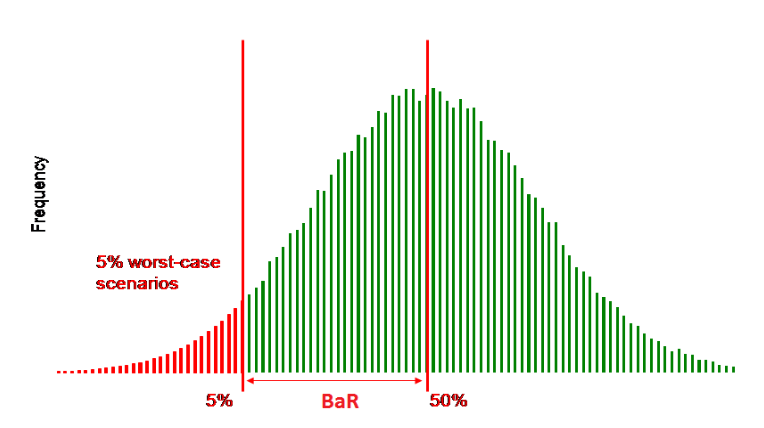

- Modifying the confidence levels. This changes the sensitivity of the model to extreme scenarios. For example, the figure below illustrates the BaR for a 95% level of confidence and provides the 5% worst-case scenario. If a 99% confidence level was applied, it would provide the 1% worst (most extreme) case scenario.

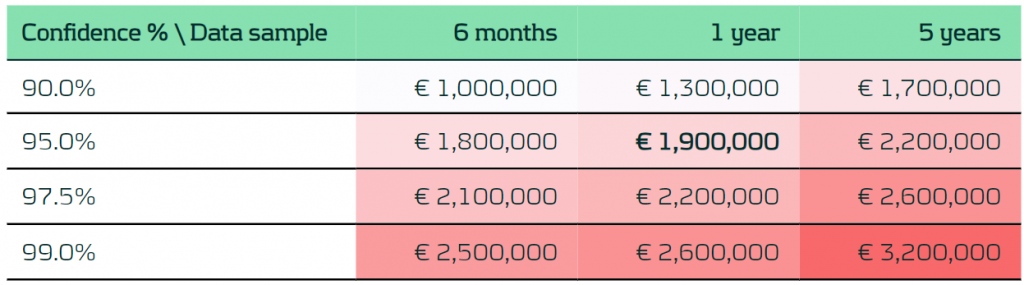

- Selecting different lengths of sample data. This allows the calculation of the correlation and volatility of currency pairs. The period length of the sample data helps to assess the sensitivity to current events that may affect the FX market. For example, a sample period of 6 months is much more sensitive to current events than a sample of 5 years.

Figure 1 – BaR for a 95% level of confidence

Adjusting these parameters makes it possible to calculate the decomposition of the BaR per currency for a specified confidence level and length of data sample. The visual outcome makes the currency that’s generating most risk quick and easy to identify. Finally, the diversification effect on the BaR is calculated to quantify the offsetting effect of inflows and outflows and the correlation between the currencies.

Table 1 – Example BaR output per confidence level and length of data sample

Pushing parameters

The challenge with the simulation and the results generated is that many parameters influence the outcomes – such as changes in cash flows, volatility, or correlation. To provide as much clarity as possible on the underlying assumptions, the impact of each parameter on the results must be considered. Zanders achieves this firstly by decomposing the impact by:

- Changing FX data to trigger a difference in the market volatility and correlation.

- Altering the cash flows between the two assessment periods.

Then, we look at each individual currency to better understand its impact on the total result. Finally, additional background checks are performed to ensure the accuracy of the results.

This multi-layered modeling technique provides base cases that generate realistic predictions of the impact of specific rate changes on the business’ operating budget for the year ahead. Armed with this knowledge, we then work with the non-profit client to develop suitable hedging strategies to protect their funding.

Leveraging Zanders’ expertise

FX scenario modeling is a complex process requiring expertise in currency movements and risk – a combination of niche skills that are uncommon in the finance teams of most non-profit businesses. But for these organizations, where there can be significant currency exposure, taking a proactive, data-driven approach to managing FX risk is critical. Zanders brings extensive experience in supporting NGO, charity and non-profit clients with modeling currency risk in a multiple currency exposure environment and quantifying potential hedge cost reduction by shifting from currency hedge to portfolio hedge.

For more information, visit our NGOs & Charities page here, or contact the authors of this case study, Pierre Wernert and Jaap Stolp.

-

Zanders Updates DLL’s Hedge Accounting With a Faster, More Integrated Model

-

Partnering with Nationaal Warmtefonds: From Niche Fund to Becoming a Key Pillar in the National Energy Transition

-

Smarter Cash Management Unlocks a Powerful Growth Lever for Savvy Games Group

-

A new IRRBB Roadmap for Knab

-

Empowering Médecins Sans Frontières (MSF)/Doctors Without Borders to Take Control of FX Uncertainty

-

Empowering UGI International with real-time cashflow visibility

-

Charting Treasury Horizons: Zanders’ Treasury Benchmark Scan Paves the Path for NGO’s Future

-

A multi-faceted refinancing for C. Steinweg

-

Transfer Pricing Compliance with Zanders Transfer Pricing Suite: Royal Philips Case Study

-

Bolt chooses treasury efficiency in scale-up of business