Unlocking Value in Private Equity: Treasury Optimization as the Strategic Lever in the New Era of Operational Value Creation

August 2024

6 min read

Authors:

Lou Gueroeva, Pieter Kraak

Share:

In the high-stakes world of private equity, where the pressure to deliver exceptional returns is relentless, the playbook is evolving.

In the high-stakes world of private equity, where the pressure to deliver exceptional returns is relentless, the playbook is evolving. Gone are the days when financial engineering—relying heavily on leveraged buyouts and cost-cutting—was the silver bullet for value creation. Today, the narrative is shifting toward a more sustainable, operationally driven approach, with treasury and finance optimization emerging as pivotal levers in this transformation.

In this article, we blend fictional examples, use cases and other real-world examples to vividly illustrate key concepts and drive our points home.

The Disconnect Between Promised and Delivered Operational Value

Limited Partners (LPs) are becoming more discerning in their investment decisions, increasingly demanding more than just financial returns. They expect General Partners (GPs) to deliver on promises of operational improvements that go beyond mere financial engineering. However, there is often a significant disconnect between the operational value creation promised by GPs and the reality, which frequently relies too heavily on short-term financial tactics.

A report by McKinsey highlights that while 60% of GPs claim to focus on operational improvements, only 40% of LPs feel that these efforts significantly impact portfolio performance. This gap between intention and execution underscores the need for GPs to align their value creation strategies with LP expectations. LPs are particularly focused on consistent investment strategies, strong management teams, and robust operational processes that drive sustainable growth. They view genuine operational value creation as the cornerstone of a repeatable and sustainable investment strategy, offering reassurance that future fund generations will perform consistently.

Treasury: The Unsung Hero of Value Creation

Treasury functions, once seen as mere back-office operations, are increasingly recognized as crucial drivers of value in private equity. These functions—ranging from cash management to financial risk mitigation—are the lifeblood of any portfolio company.

The evolution of treasury functions, now known as Treasury 4.x, has transformed them into pivotal drivers of value. These modernized treasury roles—encompassing advanced cash management and risk mitigation—now align financial operations with broader strategic goals, leveraging technology and data analytics to optimize performance.

Yet, many firms struggleto appreciate just how much inefficiencies in these areas can erode value. Poor liquidity management, fragmented cash operations, and outdated financial processes can strangle a company's ability to invest in growth and hamstring its potential to capitalize on market opportunities.

Consider the example of a mid-sized European manufacturing firm acquired by a private equity investor. Initially, the focus was solely on scaling revenue by entering new markets. However, it soon became apparent that fragmented treasury operations were hemorrhaging resources, particularly due to decentralized cash management systems across multiple jurisdictions.

By centralizing these operations into a single source of truth, like a treasury management system (TMS), the company was able to cut down on redundant processes, improve visibility and central control on cash, reduce external borrowing cost and cash related operational costs by 20%. This freed up capital that was then reinvested into R&D and expansion efforts, positioning the firm to seize new growth opportunities with agility.

Cash Flow Forecasting: The Financial Crystal Ball

In the realm of private equity, where every dollar counts, cash flow forecasting is not just a routine exercise—it’s a strategic imperative. Accurate cash flow forecasting provides a clear window into a company's financial future, offering transparency that is invaluable for both internal decision-makers and external stakeholders, especially Limited Partners (LPs) who demand rigorous insights into their investments.

Take, for example, a mid-market technology firm backed by private equity, poised to launch a groundbreaking product. Initially, the firm’s cash flow forecasts were rudimentary, lacking the sophistication needed to anticipate the working capital needs for the product launch phase. As a result, the company nearly ran into a liquidity crisis that could have delayed the launch.

By overhauling its cash flow forecasting processes and incorporating scenario analysis, the company was able to better anticipate cash needs, secure bridge financing, and ensure a successful product rollout, which ultimately boosted investor confidence.

Navigating Financial Risks in a Volatile World

In today’s unpredictable economic landscape, managing financial risks such as currency fluctuations and interest rate spikes is more critical than ever. As private equity firms increasingly engage in cross-border acquisitions, the exposure to foreign exchange risk has become a significant concern. Similarly, the current high-interest-rate environment complicates debt management, adding layers of complexity to financial operations.

Consider a global consumer goods company within a private equity portfolio, operating in regions with volatile currencies like Brazil or South Africa. Without a robust FX hedging strategy, the company was previously exposed to unpredictable swings in cash flows due to exchange rate fluctuations, which affected its ability to meet debt obligations denominated in foreign currencies.

By implementing a comprehensive FX hedging strategy, including the use of natural hedges, the firm was able to lock in favorable exchange rates, stabilize its cash flows, and protect its margins. This not only ensured financial stability but also allowed the company to reinvest profits into expanding its footprint in emerging markets.

Treasury in M&A: A Crucial Integration Component

Treasury management is often the linchpin in the success or failure of mergers and acquisitions (M&A). The ability to seamlessly integrate treasury operations is essential for realizing the synergies promised by a merger. Failure to do so can lead to significant financial inefficiencies, eroding the anticipated value.

A cautionary tale can be seen in General Electric’s acquisition of Alstom Power, where unforeseen integration challenges led to substantial restructuring costs. The treasury teams faced difficulties in aligning the cash management systems and integrating different financial cultures, which delayed synergies realization and led to missed financial targets.

Conversely, in another M&A scenario involving the merger of two mid-sized logistics firms, a pre-emptive focus on treasury integration—such as harmonizing cash pooling arrangements and consolidating banking relationships—enabled the new entity to achieve cost synergies ahead of schedule, saving millions in operational expenses and improving free cash flow.

Streamlined Treasury and Finance: Driving Strategic Value and Returns in Private Equity

Streamlined treasury and finance operations are crucial for maximizing value in private equity. These enhancements go beyond cost savings, improving a company's agility and resilience by ensuring financial resources are available precisely when needed. This empowers portfolio companies to seize growth opportunities while driving cost savings and better resource utilization through operational efficiency. Optimizing cash management and liquidity also enables companies to better navigate market volatility, reducing risks such as poor cash flow forecasting.

Enhanced transparency and real-time data visibility lead to more informed decision-making, aligning with long-term value creation strategies. This not only strengthens investor confidence but also prepares companies for successful exits by making them more attractive to potential buyers. Improved free cash flow directly boosts the money-on-money multiple, enhancing financial outcomes for private equity investors.

Conclusion

In today’s private equity landscape, the strategic importance of treasury and finance optimization is undeniable. The era of relying solely on financial engineering is over. A comprehensive approach that includes robust treasury management and operational efficiency is now essential for driving sustainable growth and maximizing value. By addressing treasury inefficiencies, private equity firms can unlock significant value, ensuring portfolio companies have the financial health to thrive. This approach meets the rising expectations of Limited Partners, setting the stage for long-term success and profitable exits.

If you're interested in delving deeper into the benefits of strategic treasury management for private equity firms, you can contact Job Wolters.

Transfer Pricing Compliance with Zanders Transfer Pricing Suite: Royal Philips Case Study

Managing over 80 intercompany loans annually and with a wide geographical scope, Royal Philips faced the challenge of complying with their Transfer Pricing obligations.

Zanders Transfer Pricing Suite is an innovative, cloud-based solution designed for companies looking to automate the Transfer Pricing compliance of financial transactions. With over five years of experience and trusted by more than 60 multinational corporations, the platform is the market-leading solution for financial transactions Transfer Pricing.On March 31, 2023, Zanders and Royal Philips jointly presented the conference "How Philips Automated Its Transfer Pricing Process for Group Financing" at the DACT (Dutch Association of Corporate Treasurers) Treasury Fair 2023.

Context The publication of Chapter X of Financial Transactions by the OECD, as well as its incorporation into the 2022 OECD Transfer Pricing Guidelines, has led to an increased scrutiny by tax authorities. Consequently, transfer pricing for financial transactions, such as intra-group loans, guarantees, cash pools, and in-house banks, has become a critical focus for treasury and tax departments.

ZANDERS TRANSFER PRICING SOLUTION

As compliance with Transfer Pricing regulations gains greater significance, many companies find that the associated analyses consume excessive time and resources from their in-house tax and treasury departments. Several struggle to automate the end-to-end process, from initiating intercompany loans to determining the arm's length interest, recording the loans in their Treasury Management System (TMS), and storing the Transfer Pricing documentation.

Since 2018, Zanders Transfer Pricing Solution has supported multinational corporations in automating their Transfer Pricing compliance processes for financial transactions.

ROYAL PHILIPS CASE STUDY

Managing over 80 intercompany loans annually and with a wide geographical scope, Royal Philips faced the challenge of complying with their Transfer Pricing obligations. During the conference, Joris Van Mierlo, Corporate Finance Manager at Philips, detailed how Royal Philips implemented a fully integrated solution to determine and record the arm's length interest rates applicable to its intra-group loans.

In the high-stakes world of private equity, where the pressure to deliver exceptional returns is relentless, the playbook is evolving. Gone are the days when financial engineering—relying

Zanders Transfer Pricing Suite is an innovative, cloud-based solution designed for companies looking to automate the Transfer Pricing compliance of financial transactions. With over five years

This paper offers a straightforward analysis of the Basel Committee on Banking Supervision's standards on crypto asset exposures and their adoption by 2025. It critically assesses

In recent years, consumers’ and investors’ interest in sustainability has been growing. Since 2015, assets under management in ESG funds have nearly tripled, the outstanding value of

In this report, biodiversity loss ranks as the fourth most pressing concern after climate change adaptation, mitigation failure, and natural disasters. For financial institutions (FIs), it

Carbon offset processes are currently dominated by private actors providing legitimacy for the market. The two largest of these, Verra and Gold Standard, provide auditing services, carbon

Early October, the Basel Committee on Banking Supervision (BCBS) published a report[1] on the 2023 banking turmoil that involved the failure of several US banks as well as Credit Suisse. The

The SAP Business Technology Platform (BTP) is not just a standalone product or a conventional module within SAP's suite of ERP systems; rather, it serves as a strategic platform from SAP,

Treasurers dealing with multiple jurisdictions, scattered banking landscape, and local requirements face many challenges in this regard. Japan is one of the markets where bank connectivity

Seventy banks have been considered, which is an increase of twenty banks compared to the previous exercise. The portfolios of the participating banks contain around three quarters of all EU

The CSP helps reinforce the controls protecting participants from cyberattack and ensures their effectivity and that they adhere to the current Swift security requirements.

*Swift does not

As a result of the growing importance of this transformative technology and its applications, various regulatory initiatives and frameworks have emerged, such as Markets in Crypto-Assets

Over the past decades, banks significantly increased their efforts to implement adequate frameworks for managing interest rate risk in the banking book (IRRBB). These efforts typically focus

Nationaal Warmtefonds was established in 2013 as an experimental fund backed by the Dutch government to help homeowners make their houses more energy efficient. Today, it's a key player in the

As the European Union increasingly emphasizes robust digital resilience within the financial sector as of January 17th 2025, the Digital Operational Resilience Act (DORA) has become a critical

Managing banking book risk remains a critical challenge in today’s financial markets and regulatory environment. There are many strategic decisions to be made and banks are having trouble

On July 2nd, the European Banking Authority (EBA) published a Consultation Paper proposing amendments to its 2016 Guidelines on the application of the definition of default (DoD). As part of the

Artificial intelligence (AI) is advancing rapidly, particularly with the emergence of large language models (LLMs) such as Generative Pre-trained Transformers (GPTs). Yet, in quantitative risk

The games market just keeps getting bigger. And with limits on this growth seemingly uncharted, interest from governments and private sector investors is at an all-time high. Savvy Games Group

In an industry where growth is often measured in multiples, and value creation is expected to be both scalable and repeatable, operational excellence is no longer a supporting function—it’s

With extreme weather events becoming more frequent and climate policy tightening across jurisdictions, banks are under increasing pressure to understand how climate change will impact their

With the introduction of CRR3, effective from January 1, 2025, the ‘extra’ guarantee on Dutch mortgages – known as the Dutch National Mortgage Guarantee (NHG) – will no longer be

According to the IFRS 9 standards, financial institutions are required to model probability of default (PD) using a Point-in-Time (PiT) measurement approach — a reflection of present

Inflows from open reverse repos

In May 2024 the EBA stated1 that inflows from open reverse repos cannot be recognised in LCR calculations unless the call option has already been

This article is intended for finance, risk, and compliance professionals with business and system integration knowledge of SAP, but also includes contextual guidance for broader audiences.

1.

Our team at Zanders has been at the forefront of implementing BACS AUDDIS (Automated Direct Debit Instruction Service) with SAP S/4HANA, helping clients to streamline their direct debit

Thailand's e-Withholding Tax (e-WHT) system officially launched on October 27, 2020, in collaboration with 11 banks, marking a significant digital transformation with far-reaching benefits for

In today’s rapidly evolving financial landscape, fortifying the Financial Risk Management (FRM) function remains a top priority for CFOs. Zanders has identified a growing trend among

Emergence of Artificial Intelligence and Machine Learning

The rise of ChatGPT has brought generative artificial intelligence (GenAI) into the mainstream, accelerating adoption across

Introduction

In December 2024, FINMA published a new circular on nature-related financial (NRF) risks. Our main take-aways:

NRF risks not only comprise climate-related risks,

As mid-sized corporations expand, enhancing their Treasury function becomes essential. International growth, exposure to multiple currencies, evolving regulatory requirements, and increased

Industry surveys show that FRTB may lead to a 60% increase in regulatory market risk capital requirements, placing significant pressure on banks. As regulatory market risk capital requirements

First, these regions were analyzed independently such that common trends and differences could be noted within. These results were aggregated for each region such that these regions could be

Crypto Asset Exposures: Critical Assessment of Infrastructure Risks

March 2024

8 min read

Authors:

Robert Richter, Justus Schleicher

Share:

This paper explores vital infrastructure decisions, regulatory scrutiny, and proposes a flexible risk approach for financial institutions in crypto asset navigation by 2025.

This paper offers a straightforward analysis of the Basel Committee on Banking Supervision's standards on crypto asset exposures and their adoption by 2025. It critically assesses infrastructure risks, categorizes crypto assets for regulatory purposes, and proposes a flexible approach to managing these risks based on the blockchain network's stability. Through expert interviews, key risk drivers are identified, leading to a framework for quantifying infrastructure risks. This concise overview provides essential insights for financial institutions navigating the complex regulatory and technological landscape of crypto assets.

Greenwashing in Finance: Navigating the Shades of Sustainability

February 2024

8 min read

Authors:

Martin Ruf, Elena Paniagua-Avila

Share:

This article explores the growing interest in sustainability among consumers and investors, the role of financial institutions in supporting green initiatives, and the rising concern about “greenwashing” – deceptive claims regarding environmental efforts by some financial institutions.

In recent years, consumers’ and investors’ interest in sustainability has been growing. Since 2015, assets under management in ESG funds have nearly tripled, the outstanding value of green bonds issued by residents of the euro area has surged eightfold, and emission-related derivatives have seen a more than sevenfold increase1.

The global push for sustainable and environmentally responsible practices has led to an increased focus on the role of financial institutions in supporting green initiatives. One of the ways financial institutions use to incentivise sustainable investments, is by designing new products, such as blue bonds to protect marine areas and other sustainability-linked bonds2, or by transitioning to funding sectors with positive sustainability impact.

However, amidst the growing wave of environmental consciousness, the credibility of "green" claims made by some financial institutions is a point of concern. This phenomenon, known as greenwashing, is gaining attention, not only within financial institutions, but also with regulators. Financial regulators, including the European Supervisory Authorities (ESAs) and UK’s Financial Conduct Authority (FCA) have taken action against potentially misleading green statements made by institutions. Despite these regulatory interventions, the persistent risk of greenwashing persists, primarily due to the absence of consistent standards governing sustainability claims and disclosures. The lack of uniform criteria poses an ongoing challenge to effectively combatting greenwashing practices within the financial landscape.

Defining Greenwashing

The ESAs describe greenwashing as “a practice where sustainability-related statements, declarations, actions, or communications do not clearly and fairly reflect the underlying sustainability profile of an entity, a financial product, or financial services. This practice may be misleading to consumers, investors, or other market participants” 3.

Financial institutions, as key players in the global economy, play a crucial role in fostering sustainability. However, some have been accused of using deceptive practices to push their green image without making substantial changes. This practice may be misleading to consumers, investors, and other market participants.

In practice, greenwashing can take different forms depending on the institution. For insurance companies, the European Insurance and Occupational Pensions Authority (EIOPA) found in their Advise to the European Commission on Greenwashing4 various examples where insurers misleadingly claimed to be transitioning their underwriting activities to net zero by 2050 without any credible plans to do so. Other examples include insurance companies falsely claiming to plant trees for each life insurance policy sold but failing to fulfil this promise, or products being marketed as sustainable merely because of a positive "ESG rating," despite the rating not taking into account any actual sustainability factors and focusing solely on financial risks.

Withing the banking sector, the EBA reported5 that the most common misleading claims relate to the current approach to integrating sustainability into the business strategy, claims on the sustainability results and the real-world impact, and claims on future commitments on medium and long-term plans.

Finally, for investment companies and pension funds, the European Securities and Markets Authority (ESMA) reported6 that most the common greenwashing practices result from exaggerated claims without any proven link between and ESG metric and the real-world impact.

Key Indicators of Greenwashing:

Vague and Ambiguous Language: Financial institutions engaging in greenwashing often use vague terms and ambiguous language in their marketing materials. This lack of clarity makes it challenging for consumers to discern the actual environmental impact of their investments.

Lack of Transparency: Genuine commitment to sustainability involves transparency about investment choices and the environmental impact of financial products. Institutions that are less forthcoming about their practices may be concealing less-than-green investments.

Inconsistent Policies: Greenwashing is also evident when there is a misalignment between a financial institution's sustainability claims and its actual policies and practices. Actions, or lack thereof, can speak louder than words.

The Role of Regulatory Bodies

Greenwashing poses potential reputational and financial risks for the institutions involved. Addressing greenwashing might not only improve consumer’s trust in the products and services offered by financial institutions, but also will allow customers to make informed decisions that are align with their sustainability preferences and increase the capital into products that genuinely represent a more sustainable choice and drive a positive change. Tackling greenwashing should therefore be a priority for regulatory supervisors.

The introduction of the EU’s Taxonomy Regulation and the Sustainable Finance Disclosure Regulation (SFDR) addresses the initial concerns of greenwashing within the financial sector. The Taxonomy determines which economic activities are environmentally sustainable and addresses greenwashing by enabling market participants to identify and invest in sustainable assets with more confidence. SFDR promotes openness and transparency in sustainable finance transactions and requires Financial Market Participants to share the environmental and social impact of their transactions with stakeholders. In May 2023, the ESA published their progress report on greenwashing monitoring and supervision7. The report aims to provide insights into an understanding of greenwashing and identify the specific forms it can take within banking. It also evaluates greenwashing risk within the EU banking sector and determines the extend to which it might be and issue from a regulatory perspective.

In the UK, the FCA published in November 2023 a guidance consultation on the Anti-Greenwashing Rule8. The anti-greenwashing rule is one part of a package of measures introduced through the Sustainability Disclosure Requirements (SDR). The anti-greenwashing rule requires FCA-authorised firms to ensure that any claims they make to the sustainability characteristics of their financial products and services are consistent with the actual sustainability characteristics of the product or service and are fair, clear and not misleading, and have evidence to back them up. The propose rule will come into force on 31 May 2024.

While the existing and planned regulation contributes to addressing aspects of greenwashing, several measures have not yet fully entered into application, making the impact of the frameworks not visible yet. Beyond disclosures, regulators should also focus on tightening requirements on sustainability data and ratings, and creating mandates to prevent misleading statements and unfair commercial practices.

Going forward, as regulators gain more experience to comprehensively address greenwashing, financial institutions should expect increased supervision and enforcement of sustainable finance policies aimed at preventing misleading sustainability claims.

Actions to mitigate greenwashing risk

One of the biggest challenges financial institutions faced in relation to sustainability is that scientific progress, policy development and social values are in constant evolution. What was a well-supported green initiative two years ago can potentially be considered as greenwashing today.

In the meantime that stricter regulations and guidance is in place, financial institutions should take a broad view on how to develop and communicate sustainability strategies to mitigate greenwashing risk.

Here are three ways on how to prevent greenwashing:

Promote disclosure: financial institutions should publish comprehensive sustainability reports and disclose ESG information as part of their financial reports.

Commit to transparency: claims about environmental aspects or performance of their products should be justified with science-based and verifiable methods. Financial institutions should be transparent about their ambitions, status, and be open about any shortcomings they identified.

Align business practices with purpose: financial institutions should determine which climate-related and environmental risks impact business strategy in the short, medium and long term. They should reflect climate-related and environmental risks in business strategies and its implementation. In addition, they should balance sustainability ambitions with the reality of real transformation.

Zanders’ approach to managing reputational risk

Avoiding greenwashing should always be a priority for institutions. If a risk arises in this area, reputational risk management can help to limit negative effects. Due to the interdependencies between ESG, reputational, business and liquidity risk, the supervisory authorities are also increasingly focusing on this area.

In the context of reputational risk management, we recommend a holistic approach that includes both existing and new business in the analysis. In addition to identifying critical transactions from a reputational perspective, the focus is also on active stakeholder management. This requires cross-departmental cooperation between various units within the institution. In many cases, the establishment of a reputation risk management committee is key to manage that topic properly within the institution.

Conclusion

While many financial institutions genuinely strive for sustainability, the rise of greenwashing highlights the need for increased vigilance and scrutiny. Consumers, regulators, and industry stakeholders must work together to ensure that financial institutions align their actions with their environmental claims, fostering a truly sustainable and responsible financial sector.

European Central Bank, Climate-related risks to fiancial stability, 2021. ↩︎

European Central Bank, Climate-related risks to fiancial stability, 2021. ↩︎

European Banking Authority, Progress report on greenwashing monitoring and supervision, 2023. ↩︎

European Banking Authority, Progress report on greenwashing monitoring and supervision, 2023. ↩︎

European Banking Authority, Progress report on greenwashing monitoring and supervision, 2023. ↩︎

European Securities and Markets Authority, Progress report on greenwashing, 2023. ↩︎

European Banking Authority, Progress report on greenwashing monitoring and supervision, 2023. ↩︎

Financial Conduct Authority, Guidance on the Anti-Greenwashing rule, 2023. ↩︎

Biodiversity risks and opportunities for financial institutions explained

November 2023

8 min read

Authors:

Marije Wiersma, Jaap Gerrits, Iryna Fedenko

Share:

This paper explores vital infrastructure decisions, regulatory scrutiny, and proposes a flexible risk approach for financial institutions in crypto asset navigation by 2025.

In this report, biodiversity loss ranks as the fourth most pressing concern after climate change adaptation, mitigation failure, and natural disasters. For financial institutions (FIs), it is therefore a relevant risk that should be taken into account. So, how should FIs implement biodiversity risk in their risk management framework?

Despite an increasing awareness of the importance of biodiversity, human activities continue to significantly alter the ecosystems we depend on. The present rate of species going extinct is 10 to 100 times higher than the average observed over the past 10 million years, according to Partnership for Biodiversity Accounting Financials[i]. The Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES) reports that 75% of ecosystems have been modified by human actions, with 20% of terrestrial biomass lost, 25% under threat, and a projection of 1 million species facing extinction unless immediate action is taken. Resilience theory and planetary boundaries state that once a certain critical threshold is surpassed, the rate of change enters an exponential trajectory, leading to irreversible changes, and, as noted in a report by the Nederlandsche Bank (DNB), we are already close to that threshold[ii].

We will now explain biodiversity as a concept, why it is a significant risk for financial institutions (FIs), and how to start thinking about implementing biodiversity risk in a financial institutions’ risk management framework.

What is biodiversity?

The Convention on Biological Diversity (CBD) defines biodiversity as “the variability among living organisms from all sources including, i.a., terrestrial, marine and other aquatic ecosystems and the ecological complexes of which they are part.”[iii] Humans rely on ecosystems directly and indirectly as they provide us with resources, protection and services such as cleaning our air and water.

Biodiversity both affects and is affected by climate change. For example, ecosystems such as tropical forests and peatlands consist of a diverse wildlife and act as carbon sinks that reduce the pace of climate change. At the same time, ecosystems are threatened by the accelerating change caused by human-induced global warming. The IPBES and Intergovernmental Panel on Climate Change (IPCC), in their first-ever collaboration, state that “biodiversity loss and climate change are both driven by human economic activities and mutually reinforce each other. Neither will be successfully resolved unless both are tackled together.”[iv]

Why is it relevant for financial institutions?

While financial institutions’ own operations do not materially impact biodiversity, they do have impact on biodiversity through their financing. ASN Bank, for instance, calculated that the net biodiversity impact of its financed exposure is equivalent to around 516 square kilometres of lost biodiversity – which is roughly equal to the size of the isle of Ibiza in Spain[v]. The FIs’ impact on biodiversity also leads to opportunities. The Institute Financing Nature (IFN) report estimates that the financing gap for biodiversity is close to $700 billion annually[vi]. This emphasizes the importance of directing substantial financial resources towards biodiversity-positive initiatives.

At the same time, biodiversity loss also poses risks to financial institutions.

The global economy highly depends on biodiversity as a result of the increasedglobalization and interconnectedness of the financial system. Due to these factors, the effects of biodiversity losses are magnified and exacerbated through the financial system, which can result in significant financial losses. For example, approximately USD 44 trillion of the global GDP is highly or moderately dependent on nature (World Economic Forum, 2020). Specifically for financial institutions, the DNB estimated that Dutch FIs alone have EUR 510 billionof exposure to companies that are highly or very highly dependent on one or more ecosystems services[vii]. Furthermore, in the 2010 World Economic Forum report worldwide economic damage from biodiversity loss is estimated to be around USD 2 to 4.5 trillion annually. This is remarkably high when compared to the negative global financial damage of USD 1.7 trillion per year from greenhouse gas emissions (based on 2008 data), which demonstrates that institutions should not focus their attention solely on the effects of climate change when assessing climate & environmental risks[viii].

Examples of financial impact

Similarly to climate risk, biodiversity risk is expected to materialize through the traditional risk types a financial institution faces. To illustrate how biodiversity loss can affect individual financial institutions, we provide an example of the potential impact of physical biodiversity risk on, respectively, the credit risk and market risk of an institution:

Credit risk:

Failing ecosystem services can lead to disruptions of production, reducing the profits of counterparties. As a result, there is an increase in credit risk of these counterparties. For example, these disruptions can materialize in the following ways:

A total of 75% of the global food crop rely on animals for their pollination. For the agricultural sector, deterioration or loss of pollinating species may result in significant crop yield reduction.

Marine ecosystems are a natural defence against natural hazards. Wetlands prevented USD 650 million worth of damages during the 2012 Superstorm Sandy [OECD, 2019), while the material damage of hurricane Katrina would have been USD 150 billion less if the wetlands had not been lost.

Market risk:

The market value of investments of a financial institution can suffer from the interconnectedness of the global economy and concentration of production when a climate event happens. For example:

A 2011 flood in Thailand impacted an area where most of the world's hard drives are manufactured. This led to a 20%-40% rise in global prices of the product[ix]. The impact of the local ecosystems for these type of products expose the dependency for investors as well as society as a whole.

Core part of the European Green Deal

The examples above are physical biodiversity risk examples. In addition to physical risk, biodiversity loss can also lead to transition risk – changes in the regulatory environment could imply less viable business models and an increase in costs, which will potentially affect the profitability and risk profile of financial institutions. While physical risk can be argued to materialize in a more distant future, transition risk is a more pressing concern as new measures have been released, for example by the European Commission, to transition to more sustainable and biodiversity friendly practices. These measures are included in the EU biodiversity strategy for 2030 and the EU’s Nature restoration law.

The EU’s biodiversity strategy for 2030 is a core part of European Green Deal. It is a comprehensive, ambitious, and long-term plan that focuses on protecting valuable or vulnerable ecosystems, restoring damaged ecosystems, financing transformation projects, and introducing accountability for nature-damaging activities. The strategy aims to put Europe's biodiversity on a path to recovery by 2030, and contains specific actions and commitments. The EU biodiversity strategy covers various aspects such as:

Legal protection of an additional 4% of land area (up to a total of 7%) and 19% of sea area (up to a total of 30%)

Strict protection of 9% of sea and 7% of land area (up to a total of 10% for both)

Reduction of fertilizer use by at least 20%

Setting measures for sustainable harvesting of marine resources

A major step forwards towards enforcement of the strategy is the approval of the Nature restoration law by the EU in July 2023, which will become the first continent-wide comprehensive law on biodiversity and ecosystems. The law is likely to impact the agricultural sector, as the bill allows for 30% of all former peatlands that are currently exploited for agriculture to be restored or partially shifted to other uses by 2030. By 2050, this should be at least 70%. These regulatory actions are expected to have a positive impact on biodiversity in the EU. However, a swift implementation may increase transition risk for companies that are affected by the regulation.

The ECB Guide on climate-related and environmental risks explicitly states that biodiversity loss is one of the risk drivers for financial institutions[x]. Furthermore, the ECB Guide requires financial institutions to asses both physical and transition risks stemming from biodiversity loss. In addition, the EBA Report on the Management and Supervision of ESG Risk for Credit Institutions and Investment Firms repeatedly refers to biodiversity when discussing physical and transition risks[xi].

Moreover, the topic ‘biodiversity and ecosystems’ is also covered by the Corporate Sustainability Reporting Directive (CSRD), which requires companies within its scope to disclose on several sustainability related matters using a double materiality perspective.[1] Biodiversity and ecosystems is one of five environmental sustainability matters covered by CSRD. At a minimum, financial institutions in scope of CSRD must perform a materiality assessment of impacts, risks and opportunities stemming from biodiversity and ecosystems. Furthermore, when biodiversity is assessed to be material, either from financial or impact materiality perspective, the institution is subject to granular biodiversity-related disclosure requirements covering, among others, topics such as business strategy, policies, actions, targets, and metrics.

Where to start?

In line with regulatory requirements, financial institutions should already be integrating biodiversity into their risk management practices. Zanders recognizes the challenges associated with biodiversity-related risk management, such as data availability and multidimensionality. Therefore, Zanders suggests to initiate this process by starting with the following two steps. The complexity of the methodologies can increase over time as the institution’s, the regulator’s and the market’s knowledge on biodiversity-related risks becomes more mature.

Perform materiality assessment using the double materiality concept. This means that financial institutions should measure and analyze biodiversity-related financial materiality through the identification of risks and opportunities. Institutions should also assess their impacts on biodiversity, for example, through calculation of their biodiversity footprint. This can start with classifying exposures’ impact and dependency on biodiversity based on a sector-level analysis.

Integrate biodiversity-related risks considerations into their business strategy and risk management frameworks. From a business perspective, if material, financial institutions are expected to integrate biodiversity in their business strategy, and set policies and targets to manage the risks. Such actions could be engagement with clients to promote their sustainability practices, allocation of financing to ‘biodiversity-friendly’ projects, and/or development of biodiversity specific products. Moreover, institutions are expected to adjust their risk appetites to account for biodiversity-related risks and opportunities, establish KRIs along with limits and thresholds. Embedding material ESG risks in the risk appetite frameworks should include a description on how risk indicators and limits are allocated within the banking group, business lines and branches.

Considering the potential impact of biodiversity loss on financial institutions, it is crucial for them to extend their focus beyond climate change and also start assessing and managing biodiversity risks. Zanders can support financial institutions in measuring biodiversity-related risks and taking first steps in integrating these risks into risk frameworks. Curious to hear more on this? Please reach out to Marije Wiersma, Iryna Fedenko, or Jaap Gerrits.

[1] CSRD applies to large EU companies, including banks and insurance firms. The first companies subject to CSRD must disclose according to the requirements in the European Sustainability Reporting Standards (ESRS) from 2025 (over financial year 2024), and by the reporting year 2029, the majority of European companies will be subject to publishing the CSRD reports. The sustainability report should be a publicly available statement with information on the sustainability-matters that the company considers material. This statement needs to be audited with limited assurance.

[ii] De Nederlandche Bank. (2020). Indepted to nature - Exploring biodiversity risks for the Dutch Financial Sector.

[iii] CBD. (2005). Handbook of the convention on biological diversity

[iv] IPBES. (2021). Tackling Biodiversity & Climate Crises Together & Their Combined Social Impacts

[v] ASN Bank (2022). ASN Bank Biodiversity Footprint

[vi] Paulson Institute. (2021). Financing nature: Closing the Global Biodiversity

[vii] De Nederlandche Bank. (2020). Indepted to nature - Exploring biodiversity risks for the Dutch Financial Sector

[viii] PwC for World Economic Forum. (2010). Biodiversity and business risk

[ix] All the examples related to credit and market risk are presented in the report by De Nederlandsche Bank. (2020). Biodiversity Opportunities and Risks for the Financial Sector

[x] ECB. (2020). Guide on climate-related and environmental risks.

[xi] EBA. (2021). EBA Report on Management and Supervision of ESG Risk for Credit Institutions and Investment Firms

Blockchain-based Tokenization for decentralized Issuance and Exchange of Carbon Offsets

November 2023

8 min read

Authors:

Robert Richter, Justus Schleicher

Share:

This paper explores vital infrastructure decisions, regulatory scrutiny, and proposes a flexible risk approach for financial institutions in crypto asset navigation by 2025.

Carbon offset processes are currently dominated by private actors providing legitimacy for the market. The two largest of these, Verra and Gold Standard, provide auditing services, carbon registries and a marketplace to sell carbon offsets, making them ubiquitous in the whole process. Due to this opacity and centralisation, the business models of the existing companies was criticised regarding its validity and the actual benefit for climate action. By buying an offset in the traditional manner, the buyer must place trust in these players and their business models. Alternative solutions that would enhance the transparency of the process as well as provide decentralised marketplaces are thus called for.

The conventional process

Carbon offsets are certificates or credits that represent a reduction or removal of greenhouse gas emissions from the atmosphere. Offset markets work by having companies and organizations voluntarily pay for carbon offsetting projects. Reasons for partaking in voluntary carbon markets vary from increased awareness of corporate responsibility to a belief that emissions legislation is inevitable, and it is thus better to partake earlier.

Some industries also suffer prohibitively expensive barriers for lowering their emissions, or simply can’t reduce them because of the nature of their business. These industries can instead benefit from carbon offsets, as they manage to lower overall carbon emissions while still staying in business. Environmental organisations run climate-friendly projects and offer certificate-based investments for companies or individuals who therefore can reduce their own carbon footprint. By purchasing such certificates, they invest in these projects and their actual or future reduction of emissions. However, on a global scale, it is not enough to simply lower our carbon footprint to negate the effects of climate change. Emissions would in practice have to be negative, so that even a target of 1,5-degree Celsius warming could be met. This is also remedied by carbon credits, as they offer us a chance of removing carbon from the atmosphere. In the current process, companies looking to take part in the offsetting market will at some point run into the aforementioned behemoths and therefore an opaque form of purchasing carbon offsets.

The blockchain approach

A blockchain is a secure and decentralised database or ledger which is shared among the nodes of a computer network. Therefore, this technology can offer a valid contribution addressing the opacity and centralisation of the traditional procedure. The intention of the first blockchain approaches were the distribution of digital information in a shared ledger that is agreed on jointly and updated in a transparent manner. The information is recorded in blocks and added to the chain irreversibly, thus preventing the alteration, deletion and irregular inclusion of data.

In the recent years, tokenization of (physical) assets and the creation of a digital version that is stored on the blockchain gained more interest. By utilizing blockchain technology, asset ownership can be tokenized, which enables fractional ownership, reduces intermediaries, and provides a secure and transparent ledger. This not only increases liquidity but also expands access to previously illiquid assets (like carbon offsets). The blockchain ledger allows for real-time settlement of transactions, increasing efficiency and reducing the risk of fraud. Additionally, tokens can be programmed to include certain rules and restrictions, such as limiting the number of tokens that can be issued or specifying how they can be traded, which can provide greater transparency and control over the asset.

Blockchain-based carbon offset process

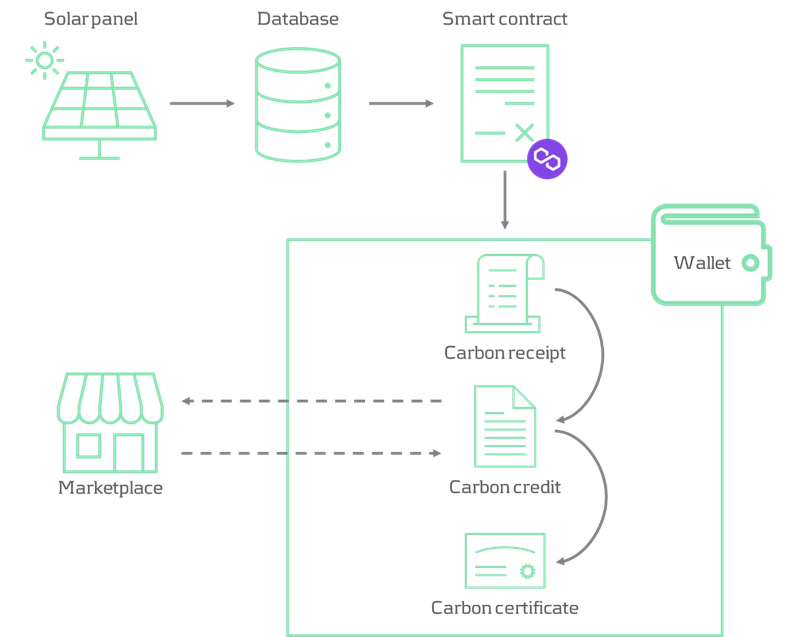

The tokenisation process for carbon credits begins with the identification of a project that either captures or helps to avoid carbon creation. In this example, the focus is on carbon avoidance through solar panels. The generation of solar electricity is considered an offset, as alternative energy use would emit carbon dioxide, whereas solar power does not.

The solar panels provide information regarding their electricity generation, from which a figure is derived that represents the amount of carbon avoided and fed into a smart contract. A smart contract is a self-executing application that exist on the blockchain and performs actions based on its underlying code. In the blockchain-based carbon offset process, smart contracts convert the different tokens and send them to the owner’s wallet. The tokens used within the process are compliant with the ERC-721 Non-Fungible Token (NFT) standard, which represents a unique token that is distinguishable from others and cannot be exchanged for other units of the same asset. A practical example is a work of art that, even if replicated, is always slightly different.

In the first stage of the process, the owner claims a carbon receipt, based on the amount of carbon avoided by the solar panel. Thereby the aggregated amount of carbon avoided (also stored in a database just for replication purposes) is sent to the smart contract, which issues a carbon receipt of the corresponding figure to the owner. Carbon receipts can further be exchanged for a uniform amount of carbon credits (e.g. 5 kg, 10 kg, 15 kg) by interacting with the second smart contract. Carbon credits are designed to be traded on the decentralised marketplace, where the price is determined by the supply and demand of its participants. Ultimately, carbon credits can be exchanged for carbon certificates indicating the certificate owner and the amount of carbon offset. Comparable with a university diploma, carbon certificates are tied to the address of the owner that initiated the exchange and are therefore non-tradable. Figure 1 illustrates the process of the described blockchain-based carbon offset solution:

Figure 1: Process flow of a blockchain-based carbon offset solution

Conclusion

The outlined blockchain-based carbon offset process was developed by Zanders’ blockchain team in a proof of concept. It was designed as an approach to reduce dependence on central players and a transparent method of issuing carbon credits. The smart contracts that the platform interacts with are implemented on the Mumbai test network of the public Polygon blockchain, which allows for fast transaction processing and minimal fees. The PoC is up and running, tokenizing the carbon savings generated by one of our colleagues photovoltaic system, and can be showcased in a demo. However, there are some clear optimisations to the process that should be considered for a larger scale (commercial) setup.

If you're interested in exploring the concept and benefits of a blockchain-based carbon offset process involving decentralised issuance and exchange of digital assets, or if you would like to see a demo, you can contact Robert Richter or Justus Schleicher.

The 2023 Banking Turmoil

November 2023

8 min read

Author:

Pieter Klaassen

Share:

This paper explores vital infrastructure decisions, regulatory scrutiny, and proposes a flexible risk approach for financial institutions in crypto asset navigation by 2025.

Early October, the Basel Committee on Banking Supervision (BCBS) published a report[1] on the 2023 banking turmoil that involved the failure of several US banks as well as Credit Suisse. The report draws lessons for banking regulation and supervision which may ultimately lead to changes in banking regulation as well as supervisory practices. In this article we summarize the main findings of the report[2]. Based on the report’s assessment, the most material consequences for banks, in our view, could be in the following areas:

Reparameterization of the LCR calculation and/or introduction of additional liquidity metrics

Inclusion of assets accounted for at amortized cost at their fair value in the determination of regulatory capital

Implementation of extended disclosure requirements for a bank's interest rate exposure and liquidity position

More intensive supervision of smaller banks, especially those experiencing fast growth and concentration in specific client segments

Application of the full Basel III Accord and the Basel IRRBB framework to a larger group of banks

Bank failures and underlying causes

The BCBS report first describes in some detail the events that led to the failure of each of the following banks in the spring of 2023:

Silicon Valley Bank (SVB)

Signature Bank of New York (SBNY)

First Republic Bank (FRB)

Credit Suisse (CS)

While each failure involved various bank-specific factors, the BCBS report highlights common features (with the relevant banks indicated in brackets).

Long-term unsustainable business models (all), in part due to remuneration incentives for short-term profits

Governance and risk management did not keep up with fast growth in recent years (SVB, SBNY, FRC)

Ineffective oversight of risks by the board and management (all)

Overreliance on uninsured customer deposits, which are more likely to be withdrawn in a stress situation (SVB, SBNY, FRC)

Unprecedented speed of deposit withdrawals through online banking (all)

Investment of short-term deposits in long-term assets without adequate interest-rate hedges (SVB, FRC)

Failure to assess whether designated assets qualified as eligible collateral for borrowing at the central bank (SVB, SBNY)

Client concentration risk in specific sectors and on both asset and liability side of the balance sheet (SVB, SBNY, FRC)

Too much leniency by supervisors to address supervisory findings (SVB, SBNY, CS)

Incomplete implementation of the Basel Framework: SVB, SBNY and FRB were not subject to the liquidity coverage ratio (LCR) of the Basel III Accord and the BCBS standard on interest rate risk in the banking book (IRRBB)

Of the four failed banks, only Credit Suisse was subject to the LCR requirements of the Basel III Accord, in relation to which the BCBS report includes the following observations:

A substantial part of the available high quality liquid assets (HQLA) at CS was needed for purposes other than covering deposit outflows under stress, in contrast to the assumptions made in the LCR calculation

The bank hesitated to make use of the LCR buffer and to access emergency liquidity so as to avoid negative signalling to the market

Although not part of the BCBS report, these observations could lead to modifications to the LCR regulation in the future.

Lessons for supervision

With respect to supervisory practices, the BCBS report identifies various lessons learned and raises a few questions, divided into four main areas:

1. Bank’s business models

Importance of forward-looking assessment of a bank’s capital and liquidity adequacy because accounting measures (on which regulatory capital and liquidity measures are based) mostly are not forward-looking in nature

A focus on a bank’s risk-adjusted profitability

Proactive engagement with ‘outlier banks’, e.g., banks that experienced fast growth and have concentrated funding sources or exposures

Consideration of the impact of changes in the external environment, such as market conditions (including interest rates) and regulatory changes (including implementation of Basel III)

2. Bank’s governance and risk management

Board composition, relevant experience and independent challenge of management

Independence and empowerment of risk management and internal audit functions

Establishment of an enterprise-wide risk culture and its embedding in corporate and business processes.

Senior management remuneration incentives

3.Liquidity supervision

Do the existing metrics (LCR, NSFR) and supervisory review suffice to identify start of material liquidity outflows?

Should the monitoring frequency of metrics be increased (e.g., weekly for business as usual and daily or even intra-day in times of stress)?

Monitoring of concentration risks (clients as well as funding sources)

Are sources of liquidity transferable within the legal entity structure and freely available in times of stress?

Testing of contingency funding plans

4. Supervisory judgment

Supplement rules-based regulation with supervisory judgment in order to intervene pro-actively when identifying risks that could threaten the bank’s safety and soundness. However, the report acknowledges that a supervisor may not be able to enforce (pre-emptive) action as long as an institution satisfies all minimum requirements. This will also depend on local legislative and regulatory frameworks

Lessons for regulation

In addition, the BCBS report identifies various potential enhancement to the design and implementation of bank regulation in four main areas:

1. Liquidity standards

Consideration of daily operational and intra-day liquidity requirements in the LCR, based on the observation that a material part of the HQLA of CS was used for this purpose but this is not taken into account in the determination of the LCR

Recalibration of deposit outflows in the calculation of LCR and NSFR, based on the observation that actual outflow rates at the failed banks significantly exceeded assumed outflows in the LCR and NSFR calculations

Introduction of additional liquidity metrics such as a 5-day forward liquidity position, survival period and/or non-risk based liquidity metrics that do not rely on run-off assumptions (similar to the role of the leverage ratio in the capital framework)

2. IRRBB

Implementation of the Basel standard on IRRBB, which did not apply to the US banks, could have made the interest rate risk exposures transparent and initiated timely action by management or regulatory intervention.

More granular disclosure, covering for example positions with and without hedging, contractual maturities of banking book positions and modelling assumptions

3. Definition of regulatory capital

Reflect unrealised gains and losses on assets that are accounted for at amortised cost (AC) in regulatory capital, analogous to the treatment of assets that are classified as available-for-sale (AFS). This is supported by the observation that unrealised losses on fixed-income assets held at amortised cost, resulting from to the sharp rise in interest rates, was an important driver of the failure of several US banks when these assets were sold to create liquidity and unrealised losses turned into realised losses. The BCBS report includes the following considerations in this respect:

If AC assets can be repo-ed to create liquidity instead of being sold, then there is no negative impact on the financial statement

Treating unrealised gains and losses on AC assets in the same way as AFS assets will create additional volatility in earnings and capital

The determination of HQLA in the LCR regulation requires that assets are measured at no more than market value. However, this does not prevent the negative capital impact described above

Reconsideration of the role, definition and transparency of additional Tier-1 (AT1) instruments, considering the discussion following the write-off of AT1 instruments as part of the take-over of CS by UBS

4. Application of the Basel framework

Broadening the application of the full Basel III framework beyond internationally active banks and/or developing complementary approaches to identify risks at domestic banks that could pose a threat to cross-border financial stability. The events in the spring of this year have demonstrated that distress at relatively small banks that are not subject to the (full) Basel III regulation can trigger broader and cross-border systemic concerns and contagion effects.

Prudent application of the ‘proportionality’ principle to domestic banks, based on the observation that financial distress at such banks can have cross-border financial stability effects

Harmonization of approaches that aim to ensure that sufficient capital and liquidity is available at individual legal entity level within banking groups

Conclusion

The BCBS report identifies common shortcomings in bank risk management practices and governance at the four banks that failed during the 2023 banking turmoil and summarizes key take-aways for bank supervision and regulation.

The identified shortcomings in bank risk management include gaps in the management of traditional banking risks (interest rate, liquidity and concentration risks), failure to appreciate the interrelation between individual risks, unsustainable business models driven by short-term incentives at the expense of appropriate risk management, poor risk culture, ineffective senior management and board oversight as well as a failure to adequately respond to supervisory feedback and recommendations.

Key take-aways for effective supervision include enforcing prompt action by banks in response to supervisory findings, actively monitoring and assessing potential implications of structural changes to the banking system, and maintaining effective cross-border supervisory cooperation.

Key lessons for regulatory standards include the importance of full and consistent implementation of Basel standards as well as potential enhancements of the Basel III liquidity standards, the regulatory treatment of interest rate risk in the banking book, the treatment of assets that are accounted for at amortised cost within regulatory capital and the role of additional Tier-1 capital instruments.

The BCBS report is intended as a starting point for discussion among banking regulators and supervisors about possible changes to banking regulation and supervisory practices. For those interested in engaging in discussions related to the insights and recommendations in the BCBS report, please feel free to contact Pieter Klaassen.

[2] Although recognized as relevant in relation to the banking turmoil, the BCBS report explicitly excludes from its consideration the role and design of deposit guarantee schemes, the effectiveness of resolution arrangements, the use and design of central bank lending facilities and FX swap lines, and public support measures in banking crises.

Driving Treasury Innovation: A Closer Look at SAP BTP

October 2023

8 min read

Author:

Ian Haegemans

Share:

This paper explores vital infrastructure decisions, regulatory scrutiny, and proposes a flexible risk approach for financial institutions in crypto asset navigation by 2025.

The SAP Business Technology Platform (BTP) is not just a standalone product or a conventional module within SAP's suite of ERP systems; rather, it serves as a strategic platform from SAP, serving as the foundational underpinning for all company-wide innovations. In this article, we will delve deeper into some of the key offerings of SAP BTP for treasury and explore how it can contribute to driving innovation within treasury.

The platform is designed to offer a versatile array of tools and services, aiming to enhance, extend, and seamlessly integrate with your existing SAP systems and other applications. Ultimately enabling a more efficient realization of your business objectives, delivering enhanced operational efficacy and flexibility.

Analytics and AI

One of the standout features of SAP BTP for treasury is its analytics and planning solution, SAP Analytics Cloud (SAC). This feature seamlessly connects with different data sources and other SAP applications. It supports Extended Planning & Analysis and Predictive Planning using machine learning models.

At the core of SAC, various planning areas – like finance, supply chain, and workforce – are combined into a cloud-based interconnected plan. This plan is based on a single version of the truth, bringing planning content together. Enhanced by predictive AI and ML models, the plan achieves more accurate forecasting and supports near-real-time planning. Users can also compare different scenarios and perform what-if analysis to evaluate the impact of changes on the plan equipping organizations to prepare for uncertainties effectively.

Application Development and Integration

An organization's treasury architecture landscape often involves numerous systems, custom applications, and enhancements. However, this complexity can result in challenges related to maintenance, technical debt, and operational efficiency.

Addressing these challenges, SAP BTP offers a solution known as the SAP Build apps tool. The tool enables users to adapt standard functionalities and create custom business applications through intuitive no-code/low-code tools. This allows that all custom development takes place outside your SAP ERP system, thereby preserving a ‘clean core’ of your SAP system. This will allow for a simpler, more streamlined maintenance process and a reduced risk of compatibility issues when upgrading to newer versions of SAP.

In addition, SAP BTP facilitates seamless connectivity through a range of connectors and APIs integrated within the SAP Integration Suite. Enabling a harmonious integration of data and processes across diverse systems and applications, whether they are on-premise or cloud-based.

Process Automation and Workflow Management

Efficient process automation and workflow management play a pivotal role in enhancing treasury operations. SAP BTP offers an efficient solution named SAP Build Process Automation which enables users to design and oversee business processes using either low-code or no-code methods. It combines workflow management, robotic process automation, decision management, process visibility, and AI capabilities, all consolidated within a user-friendly interface.

A significant advantage of SAP BTP's workflow approach over conventional SAP workflows is the unification of workflows across diverse systems, including non-SAP systems and increased flexibility, enabling smoother interaction between processes and systems.

The integration of SAP BTP for workflow with different SAP modules such as TRM, IHC, BAM is facilitated through the SAP Workflow Management APIs within your SAP S/4 HANA system.

In the context of treasury functions, SAP Build Process Automation proves invaluable for automating and refining diverse processes such as cash management, risk management, liquidity planning, payment processing, and reporting. For instance, users can leverage the integrated AI functionalities for tasks like collecting bank statements/account balance information from different systems, consolidating information, saving and/or distributing the cash position information to the appropriate people and systems. Furthermore, the automation recorder can be employed to mechanize the extraction and input of data from diverse systems. Finally, the SAP Build Process Automation can also be utilized to create workflows for complex payment approval scenarios, including exceptions and escalations.

Extensions to the Treasury Ecosystem

SAP BTP extends the treasury ecosystem with multiple treasury-specific developed solutions, seamlessly enhancing your treasury SAP S/4 HANA system functionality. These extensions include: Multi-Bank Connectivity for simplified and secure banking interactions, SAP Digital Payment Add-On for efficiently connecting to payment service providers. Trading Platform Integration for streamlined financial instrument trading, SAP Cloud for Credit Integration to assess business partner credit risk, SAP Taulia for Working Capital Management, Cash Application for automatic bank statement processing and cash application, and lastly, SAP Market Rates Management for the reliable retrieving of market data.

Empowering organizations with extensive treasury needs by enabling them to selectively adopt these value-added capabilities and solutions offered by SAP.

Alternatives to SAP BTP

The primary driving factor to consider integrating SAP BTP as an addon to your SAP ERP is when there is an integrated company-wide approach towards adopting BTP. Furthermore, if the standard SAP functionalities fall short of meeting the specific demands of the treasury department, or if the need for seamless integration with other systems arises.

It's important to prioritize the optimization of complex processes whenever feasible first, avoiding the pitfall of optimizing inherently flawed processes using advanced technologies such as SAP BTP. It is worth noting that the standard SAP functionality, which is already substantial, could very well suffice. Consequently, we recommend conducting an analysis of your processes first, utilizing the Zanders best practices process taxonomy, before deciding on possible technology solutions.

Ultimately, while considering technology options, it's wise to explore offerings from best-of-breed treasury solution providers as well – keeping in mind the potential need for integration with SAP.

Getting Started

The above highlights just a glimpse of SAP BTP's capabilities. SAP offers a free trial that allows users to explore its services. Instead of starting from scratch, you can leverage predefined business content such as intelligent RPA bots, workflow packages, predefined decision and business rules and over 170 open connectors with third-party products to get inspired. Some examples relevant for treasury include integration with Trading Brokers, S4HANA SAP Analytics Cloud, workflows designed for managing free-form payments and credit memos, as well as connectors linking to various accounting systems such as Netsuite Finance, Microsoft Dynamics, and Sage.

Conclusion

SAP BTP for Treasury is a powerful platform that can significantly enhance treasury. Its advanced analytics, app development and integration, and process automation capabilities enable organizations to gain valuable insights, automate tasks, and improve overall efficiency. If you are looking to revolutionize your treasury operations, SAP BTP is a compelling option to consider.

How to connect with local banks in Japan?

September 2023

5 min read

Author:

Michal Zelazko

Share:

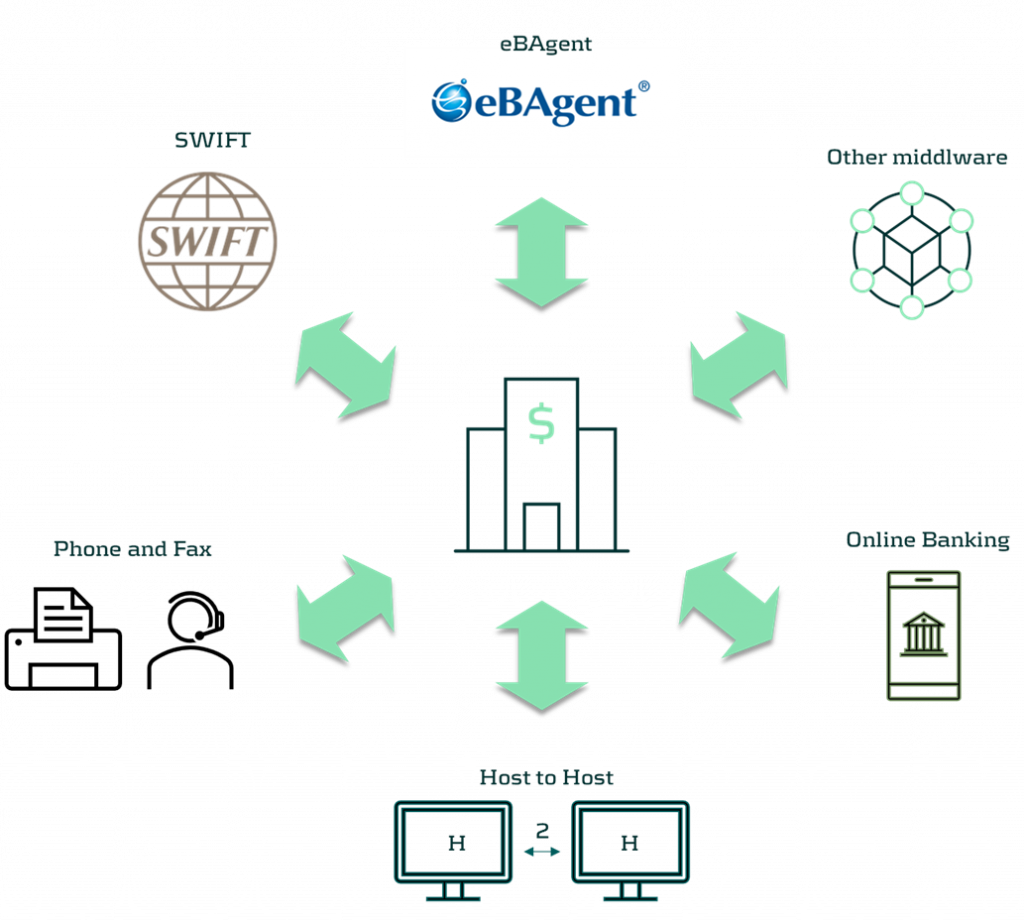

Seamless and automated connectivity between a Treasury Management System (TMS) and banks has always been an arduous task to accomplish.

Treasurers dealing with multiple jurisdictions, scattered banking landscape, and local requirements face many challenges in this regard. Japan is one of the markets where bank connectivity is indeed a challenge, especially when it comes to connecting with local banks.

Traditional options

The initial reaction from treasurers not familiar with local market conventions might be to seek connection through the SWIFT network. However, in Japan only a handful of banks offer SWIFT connectivity. Second natural choice is the Host-to-Host connection (H2H). This is the classic File Transfer Protocol (FTP), or preferably the secured version (sFTP) setup. Some will say old fashioned, rather than classic, since it is as old as the internet. Nonetheless, it is still popular, and frankly quite often the best fit for the purpose. However, if there are dozens of local banks to connect to, it can be difficult to be expected to connect to each of them with a direct H2H. While this could be technically feasible, it would be nothing short of a nightmare to maintain, with the initial setup being time-consuming in the first place.

Other solutions

There is an answer, or should we rather say ANSER, to this question. ANSER, an abbreviation of ‘Automatic answer Network System for Electrical Request’, is a data transfer system provided by NTT Data Corporation since 1981, which links banks with firms.[1] ANSER then is a way to connect a corporate client to the bank. The system has been around for a while, and together with Cash Management Service (CMS) centers it is a part of the so-called Firm Banking solution in Japan. Since its inception, ANSER offered a wider range of services, through which corporates could access their banking information. Among the offered channels are telephone, fax, firm banking terminal, and personal computer. With the ever-increasing need for speedy and accurate information exchange, the more traditional ways, such as telephone and fax, gave way to the more sophisticated and automated solution, namely eBAgent.

eBAgent making use of API

The said eBAgent is a proprietary middleware platform offered by NTT Data. The solution establishes an automated connection with banks through the above-mentioned ANSER network. In short, eBAgent offers a gateway to multiple local banking partners in Japan utilizing the ANSER network. The remaining part for the corporate is then to establish a connection between the TMS and eBAgent, and secure appropriate contracts with the eBAgent provider, NTT Data, as well as the banks.

As for the connection protocol, the choice is between the classic sFTP, or Application Programming Interface (API). The latter has the real-time advantage, with less lag between the pick-and-drop sFTP connection. API seems to be a choice for an increasing number of corporates these days in this area. What is also interesting, apart from the API connection, are the supported formats for transfers and bank statements. In addition to the local Japanese ZENGIN, the protocol also offers data transmission in a proprietary XML format. This XML format is actually quite simple, with a very limited amount of tags. In addition to this, unlike the ISO 20022 standard, it contains only one level of tags, without the nesting function. Depending on the exact ERP/TMS infrastructure, eBAgent can also provide conversion services from and to the IS 20022 standard. As for the connection to eBAgent, the whole setup seems easier said than done. However, some TMS providers, in response to the demand from the market, started offering off-the-shelf solutions for a plug-and-play connection to eBAgent. Kyriba and Reval already offer it, with SAP set to roll out its solution on the S/4HANA and Multi Bank Connectivity (MBC) platform in early 2024.

Various ways to connect TMS / ERP with banks in Japan

How to connect with local banks in Japan?

It all depends on the exact landscape of banks and systems. It may just as well turn out that a hybrid solution would be best suited. There is no one-size fits all, as each corporate is unique, thus careful consideration and design will be paramount for a stable and reliable connection with banks. One thing is certain, solutions that involve obtaining bank statement information and enact payments by telephone or fax are simply no longer sufficient. In this day and age, when much sensitive information is exchanged between corporates and banks, having a reliable, automated solution is indispensable.

If you would like to know more, do not hesitate to get in touch with Michal Zelazko via [email protected] or via + 81 (0) 8 3255 9966

This paper explores vital infrastructure decisions, regulatory scrutiny, and proposes a flexible risk approach for financial institutions in crypto asset navigation by 2025.

Seventy banks have been considered, which is an increase of twenty banks compared to the previous exercise. The portfolios of the participating banks contain around three quarters of all EU banking assets (Euro and non-Euro).

Interested in how the four Dutch banks participating in this EBA stress test exercise performed? In this short note we compare them with the EU average as represented in the results published [1].

General comments

The general conclusion from the EU wide stress test results is that EU banks seem sufficiently capitalized. We quote the main 5 points as highlighted in the EBA press release [1]:

The results of the 2023 EU-wide stress test show that European banks remain resilient under an adverse scenario which combines a severe EU and global recession, increasing interest rates and higher credit spreads.

This resilience of EU banks partly reflects a solid capital position at the start of the exercise, with an average fully-loaded CET1 ratio of 15% which allows banks to withstand the capital depletion under the adverse scenario.

The capital depletion under the adverse stress test scenario is 459 bps, resulting in a fully loaded CET1 ratio at the end of the scenario of 10.4%. Higher earnings and better asset quality at the beginning of the 2023 both help moderate capital depletion under the adverse scenario.

Despite combined losses of EUR 496bn, EU banks remain sufficiently apitalized to continue to support the economy also in times of severe stress.

The high current level of macroeconomic uncertainty shows however the importance of remaining vigilant and that both supervisors and banks should be prepared for a possible worsening of economic conditions.

For further details we refer to the full EBA report [1].

Dutch banks

Making the case for transparency across the banking sector, the EBA has released a detailed breakdown of relevant figures for each individual bank. We use some of this data to gain further insight into the performance of the main Dutch banks versus the EU average.

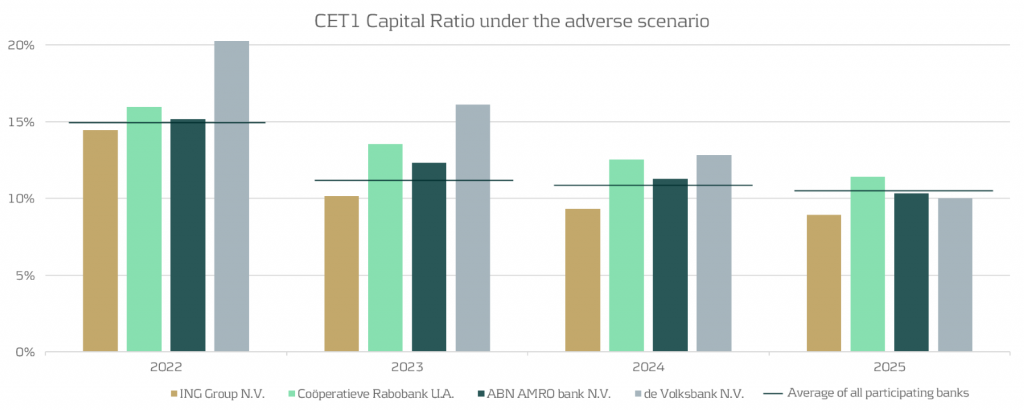

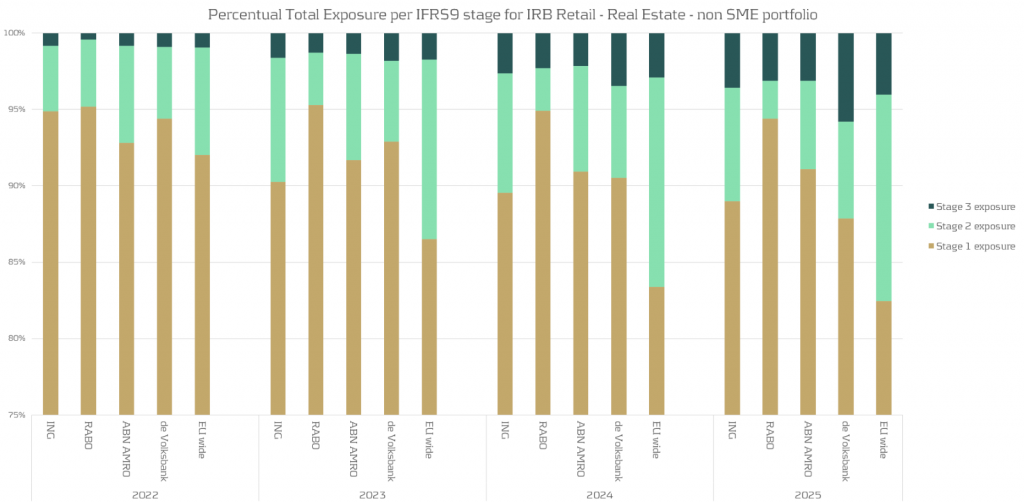

CET1 ratios

Using the data presented by EBA [2], we display the evolution of the fully loaded CET1 ratio for the four banks versus the average over all EU banks in the figure below. The four Dutch banks are: ING, Rabobank, ABN AMRO and de Volksbank, ordered by size.

From the figure, we observe the following:

Compared to the average EU-wide CET1 ratio (indicated by the horizontal lines in the graph above), it can be observed that three out of four of the banks are very close to the EU average.

For the average EU wide CET1 ratio we observe a significant drop from year 1 to year 2, while for the Dutch banks the impact of the stress is more spread out over the full scenario horizon.

The impact after year 4 of the stress horizon is more severe than the EU average for three out of four of the Dutch banks.

Evolution of retail mortgages during adverse scenario

The most important product the four Dutch banks have in common are the retail mortgages. We look at the evolution of the retail mortgage portfolios of the Dutch banks compared to the EU average. Using EBA data provided [2], we summarize this in the following chart:

Based on the analysis above , we observe: