The International Organization for Migration (IOM) is the principal intergovernmental agency in the field of migration. Due to increasing migratory flows over the past decade, which have escalated in recent months, the organization realized that its treasury needed a transformation in order to continue supporting the organization and its cause.

The IOM is committed to the principle that humane and orderly migration benefits both migrants and society. The organization was established in 1951, then known as the Provisional Intergovernmental Committee for the Movement of Migrants from Europe (PICMME), which helped people resettle in Western Europe following the chaos and displacement of the Second World War.

In subsequent years, the organization underwent a succession of name changes to the Intergovernmental Committee for European Migration (ICEM) in 1952, the Intergovernmental Committee for Migration (ICM) in 1980, and the International Organization for Migration (IOM) in 1989. These name changes reflect the organization’s transition from a logistics operation to a migration agency. The IOM’s members currently include 157 states and 10 observer states. It has offices in more than 150 countries and at any one time has more than 2,500 active projects ongoing.

It works to help ensure the orderly and humane management of migration, to promote international cooperation on migration issues, to assist in the search for practical solutions to migration problems, and to provide humanitarian assistance to migrants in need, including refugees, displaced persons, or other uprooted people. The organization works closely with several partners in four broad areas of migration management: migration and development, facilitating migration, regulating migration, and addressing forced migration. The IOM assists in meeting the growing operational challenges of migration management. It aims to advance the understanding of migration issues and encourages social and economic development through migration, while upholding the human dignity and well-being of migrants.

Differing paces

In 2008 and 2009, the organization went through a major transformation. “As recently as 10 years ago, the organization was still executing payments manually at its headquarters – payment by payment,” says Malcolm Grant, head of treasury at the IOM. With a new enterprise resource planning (ERP) system, the IOM took its first step towards improving its treasury. But more change was needed. While migration activities were growing – leading to increases in staff, projects, and donation allocation – treasury didn’t grow at the same pace as the rest of the organization. On top of that, in the years thereafter, the financial crisis resulted in a sharp increase of compliance requirements. “Due to all these developments, our treasury was way behind where it should have been.

The impact of the organization’s growth in an outdated system environment was that people looked for solutions by firefighting; they built up several different systems and various ways of working. For example, new bank accounts were added, instead of using existing bank accounts and relationships. We found ourselves with more than 700 accounts and over 150 bank relationships. We needed to bring treasury back to the heart of the organization – a huge challenge, because we needed more people, more up-to-date technology and improved governance.”

Due to the tight funding in the years following 2009, it was a slow process, says Grant: “From a treasury point of view, we look like a corporate; we get money in, we pay it out and invest it. A corporate has a profit motive, a different set of values and different stakeholders. So there are cultural differences and due to political issues some things don’t happen as quickly.”

A treasury blueprint for the future

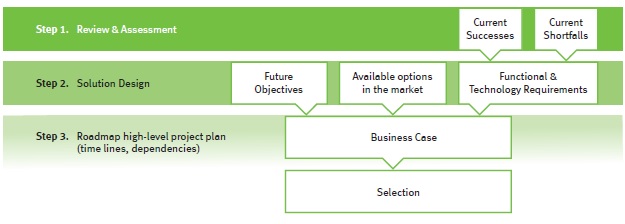

Eventually, the organization’s management was persuaded to review its treasury. Grant explains: “So in 2012, we initiated the ‘treasury review’ project. We wanted a comprehensive wide-reaching review that tackled just about all key areas of treasury. Therefore, we asked some consultant firms for treasury advice and after some meetings we hired Zanders to reinforce and challenge our assumptions. And it turned out to be a great step; they added deep knowledge of treasury, markets, and best practices, and together we built a very strong business case showing what needed to be done in our strategic planning to overhaul our treasury.”

Based on the organization’s strategy, Zanders helped IOM in writing a blueprint for the future, based on a number of areas such as treasury management, financial risk management, and treasury governance. “And a few months later we started our ‘global treasury design’ project, aimed at scaling up our treasury operations. But then the question was how to get there. So, how could all issues be improved?”

Treasury risk committee & governance

But before IOM’s treasury realized these three objectives on the technical side, it had already looked at some of the ‘no-cost’ recommendations. Grant says: “In terms of structure, we were very keen to make sure we had a written treasury policy – we now have one. We also lacked an annual treasury plan, which we have now introduced. And one of the most important aspects was setting up a treasury risk committee, which brings together some senior managers in finance and one from operations. They have now been meeting quarterly for two years and it has added enormously to treasury transparency. Moreover, it’s a two-way channel; it has also been a very effective channel for feedback into senior management – to show what treasury is doing and what we want to achieve in the near future. As a result of the review, some serious and valuable changes have been made.”

Grant’s treasury department worked hard to realize the targets as described in the roadmap. He needed some assistance in finding the organization’s banking partners for its cash management, to solve the problem of a too widely dispersed bank portfolio and bank account structure.

“We need to see what money is where,” says Grant. “We don’t see certain key collections in our accounts. Different field offices have different cultures; some are very proactive and engaged in centralized cash management, yet others aren’t. Therefore visibility is very important and a big challenge.”

Simplifying bank relationships

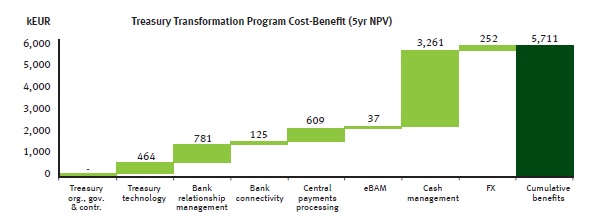

So, last year, IOM asked Zanders to conduct a European Cash Management RFP. Grant notes: “The number of bank relationships was over 150 across our organization. When we did the European RFP, we had 39 countries in scope with 38 different banking parties in those countries. Depending on the region, you could begin to centralize payments. We don’t need to have bank accounts all over Europe, for example. So instead of having 38 bank partners, in the future we may only have five or six.”

Based on IOM’s requirements, five banks were shortlisted for its cash management bank selection project with a pan-European scope. Zanders helped to write the RFP document, was part of the bank selection, managed the evaluation process, and supported the recommendation to senior management. IOM now has just two banking partners and has started the implementation with both banks. “And it’s going very well. We have good support from our internal IT team, which is extremely important. We did a lot of homework and research in Europe, mission by mission, to establish all treasury requirements and banking needs in detail.”

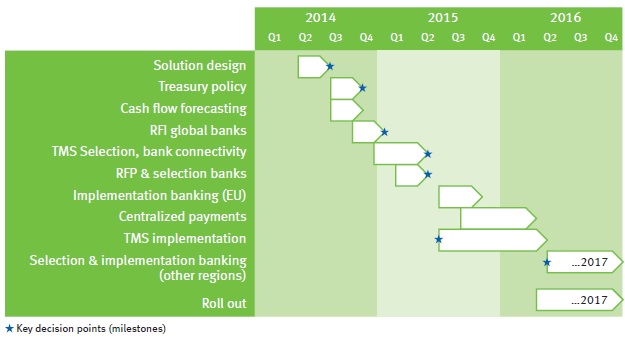

The strategic recommendations that Zanders gave were gathered in a roadmap for IOM’s treasury, with a prioritization of projects and focus areas. Grant adds: “We started by looking at three key achievable short-term objectives – things we could do within one year. The first was to bring on board the foreign exchange trading platform, 360T. The second was to bring on board a treasury management system (TMS). Third was to conduct a cash management RFP (request for proposal) in Europe for banking services. These objectives have been met; the systems are now live and working. There is still some additional TMS functionality to bring on board, but the initial level of functionality related to reporting and basic payment processing is available.”

The end of the beginning

“Our department is now about a third of the way to where we want to be. Centralizing payments and having payment factories, for example, is still years away for IOM; that demands a phased approach. In terms of payments, reconciliation, pooling, and technical architecture, we are improving our basic structures; we are looking at in-house banking (IHB) and payment factories. You need to walk before you can run. To illustrate it in an appropriate quote from Winston Churchill: ‘This is not the end, it may not even be the beginning of the end but it is the end of the beginning.’ I think that’s where we are now.”

Despite the many tough challenges for IOM’s treasury department, working for an organization in the field of migration gives Grant both energy and satisfaction. “Treasury is a humble servant of the dedicated workers doing the tough job in the field. We are just here to take a potential set of problems away from them. By, for example, ensuring that they have enough liquidity so they can do what they need to do, ensuring they do not get into trouble with local compliance, get best value in buying local currency, and ensuring they have proper banking partners and accounts. Our advice and expertise is a key area of support to the local missions, thereby ensuring that the mission activities in the field are not held up due to treasury issues.”

IOM’s key strategic focus areas:

- Migration management; helping migrants in any way possible regarding security.

- Operations and emergencies: ready to react rapidly to emergency events such as earthquakes or military actions. IOM is not a refugee agency – that work is done by the UN – however it works closely together with UNHCR.

- International cooperation and partnerships: including relationships with donors. IOM is very active in the development of international migration law. It has a team of lawyers and a department working on clarifying, establishing, and modifying international law, as far as it relates to migrants.