Transfer Pricing Compliance with Zanders Transfer Pricing Suite: Royal Philips Case Study

Managing over 80 intercompany loans annually and with a wide geographical scope, Royal Philips faced the challenge of complying with their Transfer Pricing obligations.

Zanders Transfer Pricing Suite is an innovative, cloud-based solution designed for companies looking to automate the Transfer Pricing compliance of financial transactions. With over five years of experience and trusted by more than 60 multinational corporations, the platform is the market-leading solution for financial transactions Transfer Pricing.On March 31, 2023, Zanders and Royal Philips jointly presented the conference "How Philips Automated Its Transfer Pricing Process for Group Financing" at the DACT (Dutch Association of Corporate Treasurers) Treasury Fair 2023.

Context The publication of Chapter X of Financial Transactions by the OECD, as well as its incorporation into the 2022 OECD Transfer Pricing Guidelines, has led to an increased scrutiny by tax authorities. Consequently, transfer pricing for financial transactions, such as intra-group loans, guarantees, cash pools, and in-house banks, has become a critical focus for treasury and tax departments.

ZANDERS TRANSFER PRICING SOLUTION

As compliance with Transfer Pricing regulations gains greater significance, many companies find that the associated analyses consume excessive time and resources from their in-house tax and treasury departments. Several struggle to automate the end-to-end process, from initiating intercompany loans to determining the arm's length interest, recording the loans in their Treasury Management System (TMS), and storing the Transfer Pricing documentation.

Since 2018, Zanders Transfer Pricing Solution has supported multinational corporations in automating their Transfer Pricing compliance processes for financial transactions.

ROYAL PHILIPS CASE STUDY

Managing over 80 intercompany loans annually and with a wide geographical scope, Royal Philips faced the challenge of complying with their Transfer Pricing obligations. During the conference, Joris Van Mierlo, Corporate Finance Manager at Philips, detailed how Royal Philips implemented a fully integrated solution to determine and record the arm's length interest rates applicable to its intra-group loans.

In the high-stakes world of private equity, where the pressure to deliver exceptional returns is relentless, the playbook is evolving. Gone are the days when financial engineering—relying

Zanders Transfer Pricing Suite is an innovative, cloud-based solution designed for companies looking to automate the Transfer Pricing compliance of financial transactions. With over five years

This paper offers a straightforward analysis of the Basel Committee on Banking Supervision's standards on crypto asset exposures and their adoption by 2025. It critically assesses

In recent years, consumers’ and investors’ interest in sustainability has been growing. Since 2015, assets under management in ESG funds have nearly tripled, the outstanding value of

In this report, biodiversity loss ranks as the fourth most pressing concern after climate change adaptation, mitigation failure, and natural disasters. For financial institutions (FIs), it

Carbon offset processes are currently dominated by private actors providing legitimacy for the market. The two largest of these, Verra and Gold Standard, provide auditing services, carbon

Early October, the Basel Committee on Banking Supervision (BCBS) published a report[1] on the 2023 banking turmoil that involved the failure of several US banks as well as Credit Suisse. The

The SAP Business Technology Platform (BTP) is not just a standalone product or a conventional module within SAP's suite of ERP systems; rather, it serves as a strategic platform from SAP,

Treasurers dealing with multiple jurisdictions, scattered banking landscape, and local requirements face many challenges in this regard. Japan is one of the markets where bank connectivity

Seventy banks have been considered, which is an increase of twenty banks compared to the previous exercise. The portfolios of the participating banks contain around three quarters of all EU

The CSP helps reinforce the controls protecting participants from cyberattack and ensures their effectivity and that they adhere to the current Swift security requirements.

*Swift does not

As a result of the growing importance of this transformative technology and its applications, various regulatory initiatives and frameworks have emerged, such as Markets in Crypto-Assets

Over the past decades, banks significantly increased their efforts to implement adequate frameworks for managing interest rate risk in the banking book (IRRBB). These efforts typically focus

According to the IFRS 9 standards, financial institutions are required to model probability of default (PD) using a Point-in-Time (PiT) measurement approach — a reflection of present

Inflows from open reverse repos

In May 2024 the EBA stated1 that inflows from open reverse repos cannot be recognised in LCR calculations unless the call option has already been

This article is intended for finance, risk, and compliance professionals with business and system integration knowledge of SAP, but also includes contextual guidance for broader audiences.

1.

Our team at Zanders has been at the forefront of implementing BACS AUDDIS (Automated Direct Debit Instruction Service) with SAP S/4HANA, helping clients to streamline their direct debit

Thailand's e-Withholding Tax (e-WHT) system officially launched on October 27, 2020, in collaboration with 11 banks, marking a significant digital transformation with far-reaching benefits for

In today’s rapidly evolving financial landscape, fortifying the Financial Risk Management (FRM) function remains a top priority for CFOs. Zanders has identified a growing trend among

Emergence of Artificial Intelligence and Machine Learning

The rise of ChatGPT has brought generative artificial intelligence (GenAI) into the mainstream, accelerating adoption across

Introduction

In December 2024, FINMA published a new circular on nature-related financial (NRF) risks. Our main take-aways:

NRF risks not only comprise climate-related risks,

As mid-sized corporations expand, enhancing their Treasury function becomes essential. International growth, exposure to multiple currencies, evolving regulatory requirements, and increased

Industry surveys show that FRTB may lead to a 60% increase in regulatory market risk capital requirements, placing significant pressure on banks. As regulatory market risk capital requirements

First, these regions were analyzed independently such that common trends and differences could be noted within. These results were aggregated for each region such that these regions could be

The EU instant payments regulation1 comes into force on the 5th October this year. Importantly from a corporate perspective, it includes a VoP (verification of payee) regulation that requires

Human activities such as deforestation, pollution, and resource over-extraction have caused a dramatic decline in biodiversity, with approximately 1 million species at risk of extinction,

We have developed a machine learning model for a leading Dutch bank with over EUR 300 billion in assets to detect potential money laundering activities within its high-net-worth client

The evolution of the payments industry over the past 20 years has been significant, both in terms of the number of available settlement methods and how transactions can now be made. At a

In the ongoing efforts to enhance tax transparency for multinational corporations, tax authorities have progressively increased scrutiny on intercompany financial transactions. While the

With recent volatility in financial markets, firms need increasingly faster pre-trade and risk calculations to react swiftly to changing markets. Traditional computing methods for these

After a prolonged period of stable low (and at points even negative) interest rates, 2022 saw the return of rising rates, prompting Dutch digital bank, Knab, to appoint Zanders to

The implementation update covers observations, recommendations and supervisory tools to enhance the assessment of IRRBB risks for institutions and supervisors.1 Main topics include

Over the past year, the interest rates on intercompany financial transactions have come under closer examination by tax authorities. This intensified scrutiny stems from a mix of

Insurance Treasury is evolving into Treasury 4.x, a forward-thinking paradigm integrating advanced technology and strategic foresight to enhance efficiency and resilience in the digital era.

The productivity and performance of the treasury function within insurance companies have undergone a transformative evolution, driven by the emergence of what is now termed Treasury 4.x. In this digital era, characterized by rapid technological advancements, Insurance Treasury is transitioning towards a more dynamic and strategic role. Treasury 4.x is distinguished by its capacity to envision and operate within various financial scenarios, reflecting a forward-thinking approach. The contemporary Insurance Treasury aligns itself with the principles of "Fit-for-purpose" – emphasizing a centralized organizational structure embedded seamlessly within the financial supply chain. Highly automated processes, often referred to as "exception-based management," are integral to this paradigm shift, enabling treasuries to focus resources on critical issues and exceptions, thereby enhancing efficiency and minimizing manual intervention. This evolution underscores the imperative for insurance treasuries to leverage cutting-edge technologies and embrace a proactive, scenario-driven mindset, ensuring adaptability and resilience in the face of dynamic market conditions.

Innovation of Payment Landscape

In the ever-evolving landscape of payment innovation within the treasury functions of insurance companies, a pivotal focus has been placed on migrating to the ISO 20022 XML messaging standard and moving away from FIN MT messages. This migration, driven by SWIFT, is not just a strategic choice but an industry-wide mandate, compelling all financial institutions, including insurance companies, to transition to the ISO standard by November 2025. This migration is a cornerstone in revolutionizing payment processes, offering a standardized and enriched data format that not only enhances interoperability but also facilitates more robust and information-rich communication. As insurance companies navigate this time-sensitive transition, a review of address logic within payment files becomes even more critical. The insurance companies are mandated to review and refine address logic within payment files by November 2026. Ensuring that the company is compliant with evolving financial messaging standards will not only improve the overall efficiency, speed and compliance of payments, but it will also provide the opportunity to redefine the best-in-class cash management operating model.

In additional to the industry migration to a new messaging standard, the introduction of Central Bank Digital Currency (CBDC) could impact the traditional roles of treasuries by offering new means of payment, settlement, and potentially altering liquidity management strategies. CBDCs could enhance efficiency in cross-border transactions, simplify reconciliation processes, and influence investment strategies. Insurance treasuries might need to adapt their systems and processes to incorporate CBDCs effectively, ensuring compliance with regulatory requirements and taking advantage of potential benefits associated with this digital form of currency. We are also witnessing an increase in momentum around the use of distributed ledger technology within the wholesale banking domain. In December, JP Morgan announced it was live on Partior, the Singapore-based interbank payment network that uses blockchain and is designed as a multi-bank, multi-currency system for wholesale use, with each bank controlling its own node. This is clear evidence we are starting to gain real traction around potential solutions using both blockchain and CBDC’s that will further increase the number of payment rails available to support the payments ecosystem.

Finally, the payment landscape of insurance companies sees further innovation with Faster Claims Payment (FCP). This solution streamlines the disbursement of claims, decoupling it from traditional monthly processes. FCP integrates seamlessly with the Vitesse payment platform, ensuring direct access to insurer funds and significantly reducing delays in payments. This paradigm shift promotes efficiency and enhances customer satisfaction through its accelerated claims payment system. The innovative payment landscape, however, could highlight a potential impact for processes of insurance treasuries. Increased application of faster and real-time payments requires insurance treasuries to have sufficient liquidity readily available to meet the immediate financial obligations. This demands careful planning of cash reserves to ensure uninterrupted claim processing while maintaining financial stability and stresses the importance of effective cash management for navigating any potential downside impact of FCP.

Changing Macroeconomic Environment

The insurance treasury is profoundly influenced by macroeconomic events, and the convergence of several geopolitical challenges has introduced heightened uncertainty and downside risks. Elevated geopolitical tensions, particularly the intensified strategic rivalry between the United States and China, the Russia-Ukraine war, and the recent Middle East conflict, pose significant threats to the insurance industry's stability. These events bring the potential for energy price shocks, amplifying concerns about increased insurance industry losses stemming from geopolitical and economic upheavals. Furthermore, the scheduled elections in 76 countries, with pivotal ones in the United States, Taiwan, and India, add an additional layer of uncertainty. Political transitions can introduce policy shifts, impacting regulatory environments and potentially altering economic landscapes, further complicating risk assessment for insurance treasuries. As the global geopolitical landscape remains dynamic, insurance treasuries must navigate these challenges prudently, emphasizing resilience and adaptability in their financial strategies to mitigate potential adverse impacts.

Interest rate changes command a substantial impact on the treasury functions of insurance companies, and the recent shifts in central bank policies have introduced a dynamic landscape. The conclusion of the central banks' rate tightening cycle, coupled with the Federal Reserve's announcement of rate cuts for 2024 and beyond, signals a pivotal change. While these rate cuts are aimed at supporting economic recovery, they pose challenges for insurance treasuries that traditionally benefit from higher interest rates. The insurance industry faces the paradox of modest GDP growth across advanced economies, with the downside risk of a potential rebound in inflation and further geopolitical shocks. The relatively elevated interest rates, however, offer a silver lining for (re)insurers, providing a boost to future recurring income. As maturing assets are reinvested at higher rates, this strategic advantage could help mitigate some of the challenges posed by the shifting interest rate environment, fostering resilience and adaptability in the treasury functions of insurance companies.

Taking into account the aforementioned macroeconomic changes, insurance treasuries must ensure they possess local treasury experts capable of supporting multiple regions with adapting to shifting business dynamics.

Changing Market Rates

The impact of changing market rates on the asset management activities of insurers is profound, extending to collateral management practices. Market rate fluctuations exert direct influence on the valuation and performance of their investment portfolios, notably affecting the required Variation Margin (VR) and Uncleared Margin Rules (UMR) on derivatives holdings. As rates oscillate, the value of derivative positions can vary significantly, necessitating adjustments in margin requirements to effectively manage risk exposures and collateral obligations.

Additionally, these changes in market rates affect the liquidity position of insurers, prompting the need for more dynamic models to optimize liquidity management. Given the importance of maintaining sufficient cash and liquid assets, insurers must adapt their strategies to ensure they can meet obligations promptly, especially considering the impact of FX fluctuations on assets denominated in non-base currencies. This entails employing more dynamic models to gauge liquidity needs accurately and employing strategies such as RePo agreements to enhance flexibility in accessing cash when required. Thus, navigating the complexities of changing market rates requires insurers to employ a comprehensive approach that integrates risk management, liquidity optimization, and currency hedging strategies.

Data Analytics and Predictive Modelling

The integration of artificial intelligence (AI) and predictive analytics has revolutionized the treasury function within insurance companies, particularly in the realm of cash flow forecasting. These advanced technologies enable insurance treasuries to analyze vast datasets, identify patterns, and make more accurate predictions regarding future cash flows. AI algorithms can process information rapidly, taking into account a multitude of variables, such as market trends, policyholder behavior, and economic indicators. This enhanced predictive capability is instrumental in optimizing liquidity management, allowing insurance companies to proactively anticipate cash needs and allocate resources efficiently. The importance of AI and predictive analytics in cash flow forecasting cannot be overstated, as it empowers treasuries to make informed decisions, mitigate financial risks, and navigate the complexities of the insurance landscape with greater precision and agility.

Regulatory Compliance

Regulatory compliance is pivotal for insurance company treasuries, significantly influencing financial strategies and operations. The complex regulatory landscape, including directives like the Insurance Recovery and Resolution Directive, Solvency II, and EMIR Refit, aims at ensuring financial stability, consumer protection, and market integrity. These requirements, from solvency standards to reporting obligations, impact how treasuries manage assets, liabilities, and capital. Non-compliance can lead to severe consequences, prompting insurance treasuries to invest in sophisticated systems for continuous monitoring. Striking a balance between compliance and strategic financial goals is crucial for navigating the regulatory environment and ensuring long-term organizational sustainability.

Additionally, insurance companies operating across different jurisdictions face fragmented compliance regulations, consisting of local laws and regulations. This has become a prominent challenge experienced by insurance company treasuries and visible in various treasury processes, from payments to liquidity management. Establishing robust processes and conducting regular compliance reviews could help insurance companies to address the fragmented compliance framework. By proactively addressing compliance challenges and embracing innovative solutions, insurance companies could achieve robust global operations and success in an increasingly interconnected world.

For more information about Treasury 4.x, download our latest whitepaper: Treasury 4.x - The age of productivity, performance and steering.

Bolt chooses treasury efficiency in scale-up of business

Managing over 80 intercompany loans annually and with a wide geographical scope, Royal Philips faced the challenge of complying with their Transfer Pricing obligations.

Mid 2023, Bolt successfully implemented its new full-fledged treasury management system (TMS). With assistance of Zanders consultants, the mobility company implemented Kyriba – a necessity to support Bolt’s small treasury team. As a result, all daily processes are almost completely automated. “It's about reliability.”

Bolt is the leading European mobility platform that’s focused on more efficient, convenient and sustainable solutions for urban travelling. With more than 150 million customers in at least 45 countries, it offers a range of mobility services including ride-hailing, shared cars and scooters, food and grocery delivery. “Bolt was founded by Markus Villig, a young Estonian guy who quit his school to start this business with €5,000 that he borrowed from his parents,” says Mahmoud Iskandarani, Group Treasurer at Bolt. “He built an app and started to ask drivers on the street to download it and try it out. Now we have millions of drivers and passengers, almost 4,000 employees and several business lines. Last August, we celebrated our 10th anniversary. So, we have one of the fastest growing businesses in Europe. And our ambition is to grow even faster than so far.”

Driven by technology

Because of its fast growth, Bolt’s Treasury team decided to look for a scalable solution to cope with the further expansion of the business. Freek van den Engel, Treasury manager at Bolt: “We needed a system that could automate most of our daily processes and add value. Doing things manually is not efficient and risks are high. To help us scale up while maintaining efficiency, we needed our Treasury to be driven by technology.”

Iskandarani adds: “Meanwhile, our macro environment is changing and we had some bank events. In the past years, startups or scale-ups have seen big growth and didn't focus too much on working capital management. Interest rates were low, which made it easy to raise money from investors. Now, we need to make sure that we manage our working capital the right way so that we can access our money, mitigate risks, and that we get a decent return on our cash. That’s when it's controlled by Treasury and invested correctly.”

Choosing Kyriba

Van den Engel led a treasury system selection process three years ago for his previous employer, where he also worked together with Iskandarani. “That experience helped us to come up with a shortlist of three providers, instead of having a very long RfP process looking at a long list of vendors. We started the selection process in June 2022 and two months later we chose Kyriba because of its strong functionality. Also, it’s a solution offered as SaaS, which means we don't have to worry about upgrades – a very important reason for us. Kyriba has been working with tech companies similar to ours. Another decisive factor was their format library, called Open Format Studio. It allows us to use self-service when it comes to configuring payment formats, reducing our costs and turn-around time when expanding to new geographies.”

Implementation partner

For Bolt, Kyriba will function as in-house bank system, and support its European cash pool. During the selection process, the team had some reference calls with other Kyriba users to discuss experiences with the system and the implementation. “One piece of feedback we received was that it works very well to bring in implementation partners to complete such a project successfully. Zanders stood out, because of its proven track record and the awards it had won. Also, Mahmoud and I both had experience with Zanders during some projects at our previous employer. That’s why we asked them to be our implementation partner.”

In October 2022, the implementation process started. In July 2023, the system went live. Kyriba’s TMS solution covered all treasury core processes, including cash position reporting (including intra-day balance information), liquidity management, funding, foreign exchange with automatic integration to 360T and Finastra, investments, payment settlements and risk management.

Trained towards independency

As part of the implementation process, Zanders trained Bolt on how to use the new tool, and assisted in using the Open Format Studio. In this way, the team built the knowledge and experience needed to roll out to new countries more independently.

Van den Engel: “We aimed to be independent and do as much as possible ourselves to reduce costs and build up in-house expertise on the system. Zanders helped us figuring out what we wanted, explained and guided us, and showed what the system can do and how to align that with our needs in the best possible way. Once we were clear on the blueprint, they helped us with our static data, connectivity and initial system set-up. After the training they led, we were able to do most of it ourselves, including the actual system configuration work, for which Zanders had laid the foundation.”

Rolling out the payment hub

With assistance of Zanders consultants, Bolt also set up a framework to roll out the payment hub, for the vendor payments from its ERP system called Workday and its payroll provider, Immedis. The consultants assisted with configuration of initial payment scenarios and workflows. “We made the connections, tested them and did a pilot with Workday last summer. After training and with the experience that we've built up using Open Format Studio, we can roll out to new countries and expand it ourselves. Starting in August, we continued to roll out Kyriba’s payment hub to more countries, and to implement Payroll. With the payment hub we are now live in 16 countries and that's basically fully self-serviced. Apart from some support for specialized cases, we don’t need support anymore for the payment hub.”

Many material benefits

Having a small hands-on project team meant no need for a complex project management organization to be set-up. Naturally Bolt and Zanders started using agile project management, with refocus of priorities to different streams as necessary. The Kyriba implementation project was closed within the set budget in 9 months’ time.

Iskandarani is happy with the results. “It is clear there are benefits of this implementation when it comes to efficiency and risk management. We now have the visibility over our cash and the fact that we have a system telling us that there’s an exposure that we should get rid of, that has a lot of value. Also, we have some financial benefits that we could not have achieved without the system. Today we can pool our cash better, we can invest it better, and we can handle our foreign exchange in a better way. Before this, we have overpaid banks.”

Reliability and control

“We could have hired more people”, Van den Engel adds. “But some things are just very difficult to do without this system. It's also about reliability. Even if you have a manual process in place that works, you will see it breaking down from time to time. If someone deletes a formula, or a macro stops working, that becomes very risky. It’s also about the control environment. As a company we're looking to become more mature and implement controls that should be there – that too is very difficult to do without a proper system that can generate these reports, be properly secured with all the right standards that we need to adhere to, or do fraud detection based on machine learning in the future. It's impossible to do all that manually. Those are material benefits, but hard to quantify.”

In the high-stakes world of private equity, where the pressure to deliver exceptional returns is relentless, the playbook is evolving. Gone are the days when financial engineering—relying

Zanders Transfer Pricing Suite is an innovative, cloud-based solution designed for companies looking to automate the Transfer Pricing compliance of financial transactions. With over five years

This paper offers a straightforward analysis of the Basel Committee on Banking Supervision's standards on crypto asset exposures and their adoption by 2025. It critically assesses

In recent years, consumers’ and investors’ interest in sustainability has been growing. Since 2015, assets under management in ESG funds have nearly tripled, the outstanding value of

In this report, biodiversity loss ranks as the fourth most pressing concern after climate change adaptation, mitigation failure, and natural disasters. For financial institutions (FIs), it

Carbon offset processes are currently dominated by private actors providing legitimacy for the market. The two largest of these, Verra and Gold Standard, provide auditing services, carbon

Early October, the Basel Committee on Banking Supervision (BCBS) published a report[1] on the 2023 banking turmoil that involved the failure of several US banks as well as Credit Suisse. The

The SAP Business Technology Platform (BTP) is not just a standalone product or a conventional module within SAP's suite of ERP systems; rather, it serves as a strategic platform from SAP,

Treasurers dealing with multiple jurisdictions, scattered banking landscape, and local requirements face many challenges in this regard. Japan is one of the markets where bank connectivity

Seventy banks have been considered, which is an increase of twenty banks compared to the previous exercise. The portfolios of the participating banks contain around three quarters of all EU

The CSP helps reinforce the controls protecting participants from cyberattack and ensures their effectivity and that they adhere to the current Swift security requirements.

*Swift does not

As a result of the growing importance of this transformative technology and its applications, various regulatory initiatives and frameworks have emerged, such as Markets in Crypto-Assets

Over the past decades, banks significantly increased their efforts to implement adequate frameworks for managing interest rate risk in the banking book (IRRBB). These efforts typically focus

According to the IFRS 9 standards, financial institutions are required to model probability of default (PD) using a Point-in-Time (PiT) measurement approach — a reflection of present

Inflows from open reverse repos

In May 2024 the EBA stated1 that inflows from open reverse repos cannot be recognised in LCR calculations unless the call option has already been

This article is intended for finance, risk, and compliance professionals with business and system integration knowledge of SAP, but also includes contextual guidance for broader audiences.

1.

Our team at Zanders has been at the forefront of implementing BACS AUDDIS (Automated Direct Debit Instruction Service) with SAP S/4HANA, helping clients to streamline their direct debit

Thailand's e-Withholding Tax (e-WHT) system officially launched on October 27, 2020, in collaboration with 11 banks, marking a significant digital transformation with far-reaching benefits for

In today’s rapidly evolving financial landscape, fortifying the Financial Risk Management (FRM) function remains a top priority for CFOs. Zanders has identified a growing trend among

Emergence of Artificial Intelligence and Machine Learning

The rise of ChatGPT has brought generative artificial intelligence (GenAI) into the mainstream, accelerating adoption across

Introduction

In December 2024, FINMA published a new circular on nature-related financial (NRF) risks. Our main take-aways:

NRF risks not only comprise climate-related risks,

As mid-sized corporations expand, enhancing their Treasury function becomes essential. International growth, exposure to multiple currencies, evolving regulatory requirements, and increased

Industry surveys show that FRTB may lead to a 60% increase in regulatory market risk capital requirements, placing significant pressure on banks. As regulatory market risk capital requirements

First, these regions were analyzed independently such that common trends and differences could be noted within. These results were aggregated for each region such that these regions could be

The EU instant payments regulation1 comes into force on the 5th October this year. Importantly from a corporate perspective, it includes a VoP (verification of payee) regulation that requires

Human activities such as deforestation, pollution, and resource over-extraction have caused a dramatic decline in biodiversity, with approximately 1 million species at risk of extinction,

We have developed a machine learning model for a leading Dutch bank with over EUR 300 billion in assets to detect potential money laundering activities within its high-net-worth client

The evolution of the payments industry over the past 20 years has been significant, both in terms of the number of available settlement methods and how transactions can now be made. At a

In the ongoing efforts to enhance tax transparency for multinational corporations, tax authorities have progressively increased scrutiny on intercompany financial transactions. While the

With recent volatility in financial markets, firms need increasingly faster pre-trade and risk calculations to react swiftly to changing markets. Traditional computing methods for these

After a prolonged period of stable low (and at points even negative) interest rates, 2022 saw the return of rising rates, prompting Dutch digital bank, Knab, to appoint Zanders to

The implementation update covers observations, recommendations and supervisory tools to enhance the assessment of IRRBB risks for institutions and supervisors.1 Main topics include

Over the past year, the interest rates on intercompany financial transactions have come under closer examination by tax authorities. This intensified scrutiny stems from a mix of

After taking a long hard look at its treasury function, Accell Group took the plunge by investing in a treasury management system (TMS) and improving bank connectivity with a payment hub solution.

So how exactly did the European market leader in bicycles achieve these goals? Accell Group is the European market leader in the mid- and upper-segments for high-quality bicycles and associated parts and accessories (XLC). Employing over 3,000 people across 18 countries, Accell Group manages a strong portfolio of national and international (sports) brands, each with its own distinctive positioning.

In 2018 the company sold 1.1 million bicycles, realizing a turnover of €1.1 billion and a net profit of €20.3 million. The bicycle brands in the Accell Group stable include Haibike, Winora, Ghost, Lapierre, Babboe, Batavus, Sparta, Koga, Diamondback and Raleigh. They are manufactured in several locations in the Netherlands, Hungary, Turkey and China.

Bicycles, and particularly e-bikes, are increasingly being seen as a key contributor in addressing issues such as urban congestion, hazardous city traffic, rising CO₂ emissions and our desire to live healthier lifestyles. For this reason, the bicycle market represents excellent potential for further worldwide growth.

“Given that we focus on new, clean and safe mobility solutions, we are certainly in the right business in terms of market potential,” agrees Jonas Fehlhaber, Treasurer at Accell Group, “Furthermore, there is a growing trend for large cities to adapt their infrastructures to offer cyclists more space and make them safer.”

Given that we focus on new, clean and safe mobility solutions, we are certainly in the right business in terms of market potential.

Jonas Fehlhaber, Treasurer at Accell Group

Omnichannel approach

Initially, Accell Group was a small holding company with decentralized management. Fehlhaber joined the Group in 2013 as its first treasurer, but his responsibilities soon expanded to encompass cash management, currency risk management and credit insurance. At the same time, the structure of the company changed. Based on a new strategy defined in 2016, the most important change was that the company wanted to shift from a manufacturing-driven approach to a consumer-centric one. In other words, everything must revolve around the consumer.

“In the past our sales channel was mainly defined by the dealers but now, thanks to experience centers and the use of e-commerce, this is changing into an omnichannel approach,” says Fehlhaber. “The dealers still play the most important role, but with more and more functions being provided centrally, the size of the holding has grown substantially. For the past two-and-a-half years we have had a strong supply chain organization, and our finance team, just like the Treasury, has expanded.”

Challenge

Treasury roadmap

After centralizing several components and rationalizing the bank portfolio, Accell asked Zanders to carry out a quick scan of the Treasury department. In the context of this scan, the treasury function was examined and several potential risks and possible improvement areas were identified.

“To further professionalize the Treasury, we worked with Zanders to start a project in 2017 to establish a treasury roadmap,” adds Fehlhaber. “In this project our strategic goals, along with what we wanted to achieve with them, were laid out. All in all it was an intensive undertaking in which all the respective processes were documented.”

The outcome was reconciled into three pillars: organization, systems and treasury policy. To limit the organizational vulnerability of what would otherwise have been a single-person department, Accell used Zanders’ Treasury Continuity Service (TCS) and appointed an additional treasury employee. An element of the Treasury Continuity Service is a TMS, Integrity, with which processes can be automated and standardized, while risks are simultaneously minimized.

“The Treasury Continuity Service allowed us to implement the system quickly, without the need to go through an RfP [Request for Proposal] process,” says Fehlhaber. “Zanders had already made advance agreements with the supplier, FIS, giving us a partially pre-configured system that could be quickly implemented. Moreover, the support days that we are allocated can be used for advice, for example, or if there is temporary understaffing. We acted on the advice to start up our new payment hub, from the RfP to the actual selection and, if necessary, the implementation too.”

The final improvement was to set up a comprehensive treasury policy, which has injected more structure and transparency into the daily treasury activities.

Solution

More Complete and more interactive

The new TMS and the extra support have meant that Accell’s treasury department is now less vulnerable. “While Excel allows you to work flexibly, sharing information is more difficult because it is much more personal,” continues Fehlhaber. “The owner of the Excel file will be aware of all the details, but issues can quickly arise during transfer. A complicating factor is that there is no audit trail in Excel, making it generally more risky to work with. A TMS, on the other hand, is more complete and interactive, and the transfer is much easier. It has more functionalities and provides daily bank updates, so you always have a good overview of your latest cash positions. What’s more, it records all transactions, such as FX instruments and bank- and inter-company loans, with settlements being done from within Integrity. Above all, though, the TMS offers the option of creating bespoke reports, which in itself saves a lot of time.”

Payments via TIS

A key requirement of Accell was for the payment landscape to be organized more efficiently and controlled more centrally. What we tend to see is that corporates have masses of bank cards, for everyone involved in the authorization of payments. Not only is this very inefficient, it also makes it difficult to effectively manage these processes centrally. This is why Accell decided to implement a payment hub solution [TIS; Treasury Intelligence Solutions]. The payment hub serves as an interface, to replace the banking applications. A further advantage is that TIS offers the option of single sign-on, greatly improving the on-and off-boarding process for users.

Rolling out a TIS project takes between 18 and 24 months. It is a separate system to FIS Integrity, but they are connected in terms of infrastructure. “Bank statements arrive through the payment hub and then interface software distributes them to the systems that need the information, such as the ERP system and Integrity,” explains Fehlhaber. “Furthermore, all systems are fed current market data from our terminal, while payment files, for example, are sent from Integrity via TIS to the bank.”

The once-humble bicycle has evolved into a true lifestyle product.

Tjitze Auke Rijpkema, Treasury Team

Performance

The road to the future

The increasing need to reduce exhaust emissions in major urban areas is fuelling further growth potential for the bicycle market. “The market is still growing,” agrees Fehlhaber, “especially when it comes to e-bikes. We are focusing on the mid- and upper-market segments and doing particularly well with the so-called e-performance bikes, the power-assisted mountain bikes catered for by brands such as Haibike, Ghost and Lapierre.”

In 2018, Accell acquired Velosophy, a fast-growing innovative player in e-cargo biking solutions that serves both consumer and business markets. The Velosophy stable includes Babboe, the market leader in Europe for family cargo bikes, CarQon, the new premium cargo bike brand, and Centaur Cargo. The latter of these three is a specialist in B2B cargo bikes for the so-called ‘last-mile deliveries‘. These are typically to locations that are either impossible or very difficult to reach by car, such as city centers, for example. The acquisition of Velosophy has enabled Accell Group to accelerate its innovation strategy, which is focused, among other things, on the development of urban mobility solutions.

Bicycles are becoming increasingly bespoke products, reveals Fehlhaber. Mobility as a service (offering a service concept rather than just a bicycle), lease options or special, self-selected elements are all maintaining the current momentum in the bicycle market.

“The once-humble bicycle has evolved into a true lifestyle product,” insists Tjitze Auke Rijpkema, who joined the treasury team in 2018. “Smart internet technology and handy connectivity apps are further enriching the cycling experience and making bicycles better and safer in all kinds of ways. Just like treasury, the bicycle is constantly moving with the times.”

In the high-stakes world of private equity, where the pressure to deliver exceptional returns is relentless, the playbook is evolving. Gone are the days when financial engineering—relying

Zanders Transfer Pricing Suite is an innovative, cloud-based solution designed for companies looking to automate the Transfer Pricing compliance of financial transactions. With over five years

This paper offers a straightforward analysis of the Basel Committee on Banking Supervision's standards on crypto asset exposures and their adoption by 2025. It critically assesses

In recent years, consumers’ and investors’ interest in sustainability has been growing. Since 2015, assets under management in ESG funds have nearly tripled, the outstanding value of

In this report, biodiversity loss ranks as the fourth most pressing concern after climate change adaptation, mitigation failure, and natural disasters. For financial institutions (FIs), it

Carbon offset processes are currently dominated by private actors providing legitimacy for the market. The two largest of these, Verra and Gold Standard, provide auditing services, carbon

Early October, the Basel Committee on Banking Supervision (BCBS) published a report[1] on the 2023 banking turmoil that involved the failure of several US banks as well as Credit Suisse. The

The SAP Business Technology Platform (BTP) is not just a standalone product or a conventional module within SAP's suite of ERP systems; rather, it serves as a strategic platform from SAP,

Treasurers dealing with multiple jurisdictions, scattered banking landscape, and local requirements face many challenges in this regard. Japan is one of the markets where bank connectivity

Seventy banks have been considered, which is an increase of twenty banks compared to the previous exercise. The portfolios of the participating banks contain around three quarters of all EU

The CSP helps reinforce the controls protecting participants from cyberattack and ensures their effectivity and that they adhere to the current Swift security requirements.

*Swift does not

As a result of the growing importance of this transformative technology and its applications, various regulatory initiatives and frameworks have emerged, such as Markets in Crypto-Assets

Over the past decades, banks significantly increased their efforts to implement adequate frameworks for managing interest rate risk in the banking book (IRRBB). These efforts typically focus

According to the IFRS 9 standards, financial institutions are required to model probability of default (PD) using a Point-in-Time (PiT) measurement approach — a reflection of present

Inflows from open reverse repos

In May 2024 the EBA stated1 that inflows from open reverse repos cannot be recognised in LCR calculations unless the call option has already been

This article is intended for finance, risk, and compliance professionals with business and system integration knowledge of SAP, but also includes contextual guidance for broader audiences.

1.

Our team at Zanders has been at the forefront of implementing BACS AUDDIS (Automated Direct Debit Instruction Service) with SAP S/4HANA, helping clients to streamline their direct debit

Thailand's e-Withholding Tax (e-WHT) system officially launched on October 27, 2020, in collaboration with 11 banks, marking a significant digital transformation with far-reaching benefits for

In today’s rapidly evolving financial landscape, fortifying the Financial Risk Management (FRM) function remains a top priority for CFOs. Zanders has identified a growing trend among

Emergence of Artificial Intelligence and Machine Learning

The rise of ChatGPT has brought generative artificial intelligence (GenAI) into the mainstream, accelerating adoption across

Introduction

In December 2024, FINMA published a new circular on nature-related financial (NRF) risks. Our main take-aways:

NRF risks not only comprise climate-related risks,

As mid-sized corporations expand, enhancing their Treasury function becomes essential. International growth, exposure to multiple currencies, evolving regulatory requirements, and increased

Industry surveys show that FRTB may lead to a 60% increase in regulatory market risk capital requirements, placing significant pressure on banks. As regulatory market risk capital requirements

First, these regions were analyzed independently such that common trends and differences could be noted within. These results were aggregated for each region such that these regions could be

The EU instant payments regulation1 comes into force on the 5th October this year. Importantly from a corporate perspective, it includes a VoP (verification of payee) regulation that requires

Human activities such as deforestation, pollution, and resource over-extraction have caused a dramatic decline in biodiversity, with approximately 1 million species at risk of extinction,

We have developed a machine learning model for a leading Dutch bank with over EUR 300 billion in assets to detect potential money laundering activities within its high-net-worth client

The evolution of the payments industry over the past 20 years has been significant, both in terms of the number of available settlement methods and how transactions can now be made. At a

In the ongoing efforts to enhance tax transparency for multinational corporations, tax authorities have progressively increased scrutiny on intercompany financial transactions. While the

With recent volatility in financial markets, firms need increasingly faster pre-trade and risk calculations to react swiftly to changing markets. Traditional computing methods for these

After a prolonged period of stable low (and at points even negative) interest rates, 2022 saw the return of rising rates, prompting Dutch digital bank, Knab, to appoint Zanders to

The implementation update covers observations, recommendations and supervisory tools to enhance the assessment of IRRBB risks for institutions and supervisors.1 Main topics include

Over the past year, the interest rates on intercompany financial transactions have come under closer examination by tax authorities. This intensified scrutiny stems from a mix of

Digital transformation through a corporate treasury lens

May 2022

7 min read

Author:

Mark Sutton

Share:

The corporate landscape is being redefined by a plethora of factors, from new business models and changing regulations to increased competition from digital natives and the acceleration of the consumer digital-first mindset.

The new landscape is all about a digital real-time experience which is creating the need for change in order to stay relevant and ideally thrive. If we reflect on the various messages from the numerous industry surveys, it’s becoming crystal clear that a digital transformation is now an imperative.

We are seeing an increasing trend that recognizes technological progress will fundamentally change an organization and this pressure to move faster is now becoming unrelenting. However, to some corporates, there is still a lack of clarity on what a digital transformation actually means. In this article we aim to demystify both the terminology and relevance to corporate treasury as well as considering the latest trends including what’s on the horizon.

What is digital transformation? There is no one-size-fits-all view of a digital transformation because each corporate is different and therefore each digital transformation will look slightly different. However, a simple definition is the adoption of the new and emerging technologies into the business which deliver operational and financial efficiencies, elevate the overall customer experience and increase shareholder value.

Whilst these benefits are attractive, to achieve them it’s important to recognize that a digital transformation is not a destination – it’s a journey that extends beyond the pure adoption of technology. Whilst technology is the enabler, in order to achieve the full benefits of this digital transformation journey, a more holistic view is required.

Figure 1 provides a more holistic view of a digital transformation, which embraces the importance of cultural change like the adoption of the ‘fail fast’ philosophy that is based on extensive testing and incremental development to determine whether an idea has value.

In terms of the drivers, we see four core pillars providing the motivation:

Elevate the customer experience

Operational agility and resilience

Data driven real time vision

Workforce enablement

Figure 1: Digital Transformation View

What is the relevance to corporate treasury? Considering the digital transformation journey, it’s important to understand the relevance of the technologies available.

Whilst figure 2 highlights the foundational technologies, it’s important to note that these technologies are all at a different stage of evolution and maturity. However, they all offer the opportunity to re-define what is possible, helping to digitize and accelerate existing processes and elevate overall treasury performance.

Figure 2: Core Digital Transformation Technologies

To help polarize the potential application and value of these technologies, we need to look through two lenses.

Firstly, what are some of today’s mainstream challenges that currently impact the performance of the treasury function, and secondly, how these technologies provide the opportunity to both optimize and elevate the treasury function.

The challenges and opportunities to optimize Considering some of the major challenges that still exist within corporate treasury, the new and emerging technologies will provide the foundation for the digital transformation within corporate treasury as they will deliver the core capabilities to elevate overall performance. Figure 3 below provides some insights into why these technologies are more than just ‘buzzwords’, providing a clear opportunity to elevate current performance.

Figure 3: Common challenges within corporate treasury

Cognitive cash flow forecasting systems can learn and adapt from the source data, enabling automatic and continuous improvements in the accuracy and timeliness of the forecasts. Additionally, scenario analysis accelerates the informed decision-making process. Focusing on currency risk, the cognitive technology is on a continuous learning loop and therefore continues to update its decision-making process which helps improve future predictions.

Moving onto working capital, these new cognitive technologies combined with advanced optical character recognition/intelligent character recognition can automate and accelerate key processes within both the accounts payables (A/P) and account receivables (A/R) functions to contribute to overall working capital management. On the A/R side, these technologies can read PDF and email remittance information as well as screen scrape data from customer portals. This data helps automate and accelerate the cash application process with levels exceeding 95% straight through reconciliation now being achieved. Applying cash one day earlier has a direct positive impact on days sales outstanding (DSO) and working capital. On the A/P side, the technology enables greater compliance, visibility and control providing the opportunity for ‘autonomous A/P’. With invoice approval times now down to just 10.4 business hours*, it provides a clear opportunity to maximize early payment discounts (EPDs).

Whilst artificial intelligence/machine learning technologies will play a significant role within the corporate treasury digital transformation, the increased focus on real-time treasury also points to the power of financial application program interfaces (APIs). API technology will play an integral part of an overall blended solution architecture. Whilst API technology is not new, the relevance to finance really started with Europe’s PSD2 (Payment Services Directive 2) Open Banking initiative, with API technology underpinning this. There are already several use cases for both Treasury and the SSC (shared service center) to help both digitize and importantly accelerate existing processes where friction currently exists. This includes real time balances, credit notifications and payments.

The latest trends Whilst a number of these new and emerging technologies are expected to have a profound impact on corporate treasury, when we consider the broader enterprise-wide adoption of these technologies, we are generally seeing corporate treasury below these levels. However, in terms of general market trends we see the following:

Artificial intelligence/machine learning is being recognized as a key enabler of strategic priorities, with the potential to deliver both predictive and prescriptive analytics. This technology will be a real game-changer for corporate treasury not only addressing a number of existing and longstanding pain-points but also redefining what is possible.

Whilst robotic process automation (RPA) is becoming mainstream in other business areas, this technology is generally viewed as less relevant to corporate treasury due to more complex and skilled activities. That said, Treasury does have a number of typically manually intensive activities, like manual cash pooling, financial closings and data consolidations. So, broader adoption could be down to relative priorities.

Adoption of API technology now appears to be building momentum, given the increased focus around real time treasury. This technology will provide the opportunity to automate and accelerate processes, but a lack of industry standardization across financial messaging, combined with the relatively slow adoption and limited API banking service proposition across the global banking community, will continue to provide a drag on adoption levels.

What is on the horizon? Over the past decade, we have seen a tsunami of new technologies that will play an integral part in the digital transformation journey within corporate treasury. Given that, it has taken approximately ten years for cloud technology to become mainstream from the initial ‘what is cloud?’ to the current thinking ‘why not cloud?’ We are currently seeing the early adoption of some of these foundational transformational technologies, with more corporates embarking on a digital first strategy. This is effectively re-defining the partnership between man and machine, and treasury now has the opportunity to transform its technology, approach and people which will push the boundaries on what is possible to create a more integrated, informed and importantly real-time strategic function.

However, whilst these technologies will be supporting critical tasks, assisting with real-time decision-making process and reducing risk, to truly harness the power of technology a data strategy will also be foundational. Data is the fuel that powers AI, however most organizations remain heavily siloed, from a system, data, and process perspective. Probably the biggest challenge to delivering on the AI promise is access to the right data and format at the right time.

So, over the next 5-10 years, we expect the solutions underpinned by these new foundational technologies to evolve, leveraging better quality structured data to deliver real time data visualization which embraces both predictive and prescriptive analytics. What is very clear is that this ecosystem of modern technologies will effectively redefine what is possible within corporate treasury.

*) Coupa 2021 Business Spend Management Benchmark Report

Providing possible technical solutions for CLS in SAP Treasury

March 2022

7 min read

Author:

Aleksei Abakumov

Share:

The corporate landscape is being redefined by a plethora of factors, from new business models and changing regulations to increased competition from digital natives and the acceleration of the consumer digital-first mindset.

The CLS system was established back in 2002 and since then, the FX market has grown significantly. Therefore, there is a high demand from corporates to leverage CLS to improve corporate treasury efficiency.

In this article we shed some light on the possible technical solutions in SAP Treasury to implement CLS in the corporate treasury operations. This includes CLS deal capture, limit utilization implications in Credit risk analyzer, and changes in the correspondence framework of SAP TRM.

Technical solution in SAP Treasury There is no SAP standard solution for CLS as such. However, SAP standard functionality can be used to cover major parts of the CLS solution. The solution may vary depending on the existing functionality for hedge management/accounting and limit management as well as the technical landscape accounting for SAP version and SWIFT connectivity.

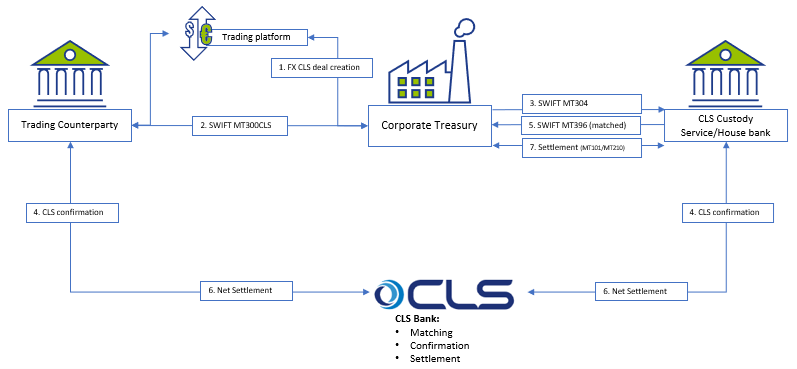

Below is a simplified workflow of CLS deal processing:

The proposed solution may be applicable for a corporate using SAP TRM (ECC to S/4HANA), having Credit risk analyzer activated and using SWIFT connection for connectivity with the banks.

Capturing CLS FX deals There are a few options on how to register the FX deal as a CLS deal, with two described below:

Option 1: CLS Business partner – a replica of your usual business partner (BP) which would have CLS BIC code and complete settlement instructions. Option 2: CLS FX product type/transaction type – a replica of normal FX SPOT, FX FORWARD or FX SWAP product type/transaction type.

Each option has pros and cons and may be applied as per a client technical specific.

FX deals trading and capturing may be executed via SAP Trade Platform Integration (TPI), which would improve the processing efficiency, but development may still be required depending on characteristics of the scope of FX dealing. In particular, the currency, product type, counterparty scope and volume of transactions would drive whether additional development is required, or whether standard mapping logic can be used to isolate CLS deals.

For the scenarios where a custom solution is required to convert standard FX deals into CLS FX deals during its creation, a custom program could be created that includes an additional mapping table to help SAP determine CLS eligible deals. The bespoke mapping table could help identify CLS eligibility based on the below characteristics:

Counterparty

Currency Pair

Product Type (Spot, Forward, SWAP)

Correspondence framework Once CLS deal is captured in SAP TRM, it needs to be counter-confirmed with the trading counterparty and with CLS Bank. Three new types of correspondence need to be configured:

MT300 with CLS specifics to be used to communicate with the trading counterparty;

MT304 to communicate with CLS Custody service;

SWIFT MT396 to get the matching status from CLS bank.

Credit Risk Analyzer (CRA) FX CLS deals do not bring settlement exposure, thus CLS deals need to be exempt from the settlement risk utilization. Configuration of the limit characteristics must include either business partner number (for CLS Business Partner) or transaction type (for CLS transaction type). This will help determine the limits without FX CLS deals.

No automatic limits creation should be allowed for the respective limit type; this will disable a settlement limit creation based on CLS deal capture in SAP. CLS Business partner setting must be done with ‘parent <-> subsidiary’ relationship with the regular business partner. This is required to keep a single credit limit utilization and having FX deals being done with two business partners.

Deal execution Accounting for CLS FX deals is normally the same as for regular FX deals, though it depends on the corporate requirements. We do not see any need for a separate FX unrealized result treatment for CLS deals.

However, settlement of CLS deals is different and standard settlement instructions of CLS deals vary from normal FX deals.

Either the bank’s virtual accounts or separate house bank accounts are opened to settle CLS FX deals.

Since CLS partner performs the net settlement on-behalf of a corporate there is no need to generate payment request for every CLS deal separately. Posting to the bank’s CLS clearing account with cash flow postings (TBB1) is sufficient at this level.

The following day the bank statement will clear the postings on the CLS settlement account on a net basis based on the total amount and posting date.

Cash Management A liquidity manager needs to know the net result of the CLS deals in advance to replenish the CLS bank account in case the net settlement amount for CLS deal is negative. In addition, the funds would need to be transmitted between the house bank accounts either manually or automatically, with cash concentration requiring transparency on the projected cash position.

The solution may require extra settings in the cash management module with CLS bank accounts to be added to specific groupings.

Conclusion Designing a CLS solution in SAP requires deep understanding of a client’s treasury operations, bank account structure and SAP TMS specifics. Together with a client and based on the unique business landscape, we review the pros and cons of possible solutions and help choosing the best one. Eventually we can design and implement a solution that makes treasury operations more efficient and transparent.

Our corporate clients are requesting our support with design and implementation of Continuous Linked Settlement (CLS) solutions for FX settlements in their SAP Treasury system. If you are interested, please do not hesitate to contact us.

Top priorities driving your Treasury agenda in 2022

December 2021

7 min read

Author:

Bianca Maskova

Share:

The corporate landscape is being redefined by a plethora of factors, from new business models and changing regulations to increased competition from digital natives and the acceleration of the consumer digital-first mindset.

Now that we have passed and are still in an uncertain period, it is time to discover opportunities to reposition and prepare for new challenges and developments. How should you, as a treasurer, prepare for another unpredictable year? What can your company, and the treasury organization specifically, do to add value by recognizing the trends? How can Treasury contribute to dealing with current challenges in global supply chains?

While much about what 2022 will hold is uncertain, there are a few trends that will definitely play an important role. In this article we explore three main topics to navigate through the new environment and which are crucial to guide your treasury plan for the coming year.

Foresee the accelerating winds of change within the payments landscape Innovation within the payments industry is closely linked to the continued digitization of commercial and consumer transactions. There are three topics worth mentioning when discussing the main points of attention for corporate treasury within the global payment landscape, being: (1) integration of e-commerce, (2) rise of alternative payment instruments, and (3) further payment standardization.

Integration of e-commerce into corporate treasury is an important topic for many treasurers. Consumers are driving the significant rise in the usage of alternative payments methods, like digital wallets (e-wallets), mobile payments, and ‘buy now, pay later’ solutions. Chinese consumers are leading the way with digital wallets which now account for over 72% of e-commerce purchases . Additionally, 56 countries are now providing real-time payment rails and the rising use of APIs promises to deliver a frictionless experience for more consumer payments. As a result, one of the important actions for Treasury in 2022, is to ensure that Treasury is linked into the different e-commerce platforms in the group in a similar fashion to how Treasury is responsible for managing traditional payments and bank relationships. Treasury should be the guardian of a safe payments infrastructure (including e-commerce payments) performed by reliable counterparties that are compliant with international regulation.

In terms of the rise of alternative instruments, we see the introduction of new digital coins, aimed at reducing volatility compared to the ‘traditional’ cryptos. This includes governments looking at the possibility of launching their own central bank digital currencies (CBDCs) which leverages the underlying distributed ledger technology as well as the introduction of so-called stablecoins, which are pegged to the value of an underlying asset. While the Bahamas was the world’s first CBDC with the launch of the Sand Dollar in October 2020, China is currently taking the lead with around 70 million digital Yuan transactions reported since the start of its pilot, which initially covered 4 cities. According to Atlantic Council, there are now 81 countries considering CBDCs, including the Federal Reserve, the European Central bank, the Bank of Japan and the Bank of England. While the future remains uncertain, these developments could lead to more mainstream use cases for digital currencies. This would have a potential impact on the payment formats we use, timing of payments and the role of traditional (network) banks. While use cases are limited at this moment, treasurers should be aware of the potential material impact on the payments landscape.

When it comes to payments standardization, API adoption is starting to accelerate, which will have a profound impact on both corporate treasury and financial shared service centers through the acceleration of information and processes. However, the lack of standardization within the industry appears to be causing the primary drag on adoption. This will become a foundational technology for real-time treasury, as real time balance and transactional information will provide immediate visibility and enable faster, more informed decisions to be made. The final payments innovations on the horizon are a combination of global messaging and infrastructure projects. First, there is the planned SWIFT adoption of a selection of the ISO20022 XML messages included in the 2019 annual standards release. While this will initially be adopted within the banking community as part of the publicized MT-MX migration, the expectation is that banks will look for corporates to migrate at some point to take advantage of the more structured data opportunities and, if the CGI-MP is successful, greater alignment around the implementation within the banking sector. Moving onto the country level infrastructure, the UK is progressing its RTGS renewal program which will be underpinned by the adoption of ISO 20022 XML messaging. In addition, Hong Kong and Singapore are also building new RTGS payment rails underpinned by ISO 20022. Within the Nordics, there is P27, which aims to establish the first integrated region for domestic and cross-border payments in multiple currencies.

Stay ahead of new global tax regimes The BEPS initiative impacted Treasury structures and the pricing of financial transactions in recent years. For example, thin capitalization rules, limitations to interest deductions and transfer pricing guidance have initiated multinationals to rethink their intercompany finance practices.

More specifically, the final OECD transfer pricing guidelines for financial transactions had a major impact on the internal corporate finance function of corporate treasuries. Numerous corporates revisited their pricing framework for intercompany loans, financial guarantees, cash pools and in-house banks in order to prevent issues during tax audits and possible transfer pricing adjustments.

We observe that more scrutiny is placed on the ‘at arm’s length’ pricing of treasury transactions and expects this to continue in 2022. It is thus advisable for treasurers to ensure that their intercompany lending framework is consistent, transparent and compliant with the latest transfer pricing guidelines. Especially since the simplified practice of using one group credit spread for all in-house bank participants is not compliant with the OECD guidelines. Therefore, as the burden of compliance increases, corporates are being pushed to look for solutions which can support them in automating this onerous process whilst still be fully compliant.

Lastly, treasurers should be aware of the latest development in international taxation: the global minimum tax. The G20 and all OECD member countries agreed on 8 October 2021 that multinationals will have to pay a minimum global tax of 15%. As the scope and the details of the tax reform are not clear yet, treasurers are advised to be aware of the topic and align with the internal tax team in order to identify the potential business impact. Treasury and tax can collaboratively serve as a strategic advisor towards their organization.

Seize the strategic opportunity in ESG When talking about sustainability within treasury, many treasurers’ first port of call is to investigate a sustainable financing framework, either via green or social financing. ESG (environmental, social and governance) considerations play an important role in the external financing and the internal capital allocation process. In the long run, companies that have not implemented an ESG strategy may be deprived from fresh capital. This particular case is becoming more apparent within certain industries, like polluting industries or the so-called sin stocks (gambling, alcohol, tobacco, and weapons industry), where the transition from Greenium to a Brown money penalty may be more present than in other industries. However, there is more than just green or social financing. The topic around ESG is currently gaining momentum. ESG considerations are essential for long-term success; it is no longer just a necessity, but also a strategic opportunity. So how should Treasury drive the ESG agenda? There are numerous innovative ways for Treasury to incorporate ESG into its strategy. For example, in addition to including ESG factors in the financing documentation or SCF programs, Treasury may incorporate ESG elements in the internal capital allocation process too. This can be done by adding ESG-related risk factors to the weighted average cost of capital (WACC) or internal hurdle investment rates for its capital allocation decisions. By having an ESG-adjusted WACC, one can evaluate projects by considering the ESG impact of an investment. By adjusting the WACC to, for example, the level of CO2 that is emitted by a project, the capital allocation process favors projects with low CO2 emissions. Another example of how Treasury can contribute to the company’s ESG goals is to encourage new and existing partners (e.g. banks or vendors) to take sustainable measures, by embedding ESG requirements into selections processes.

A corporate reaps the most benefits from its ESG policy when initiatives are mapped to the right KPIs to track the sustainable performance over time. KPI’s should be SMART, forward looking and focus on material themes. For Treasury, an example of such a metric is the percentage of suppliers rewarded with preferred supply chain finance (SCF) terms because of their ESG performance. To enlarge the impact of an ESG policy even more, and increase market transparency, KPIs should be benchmarked against industry standards.

Another way to increase market transparency is to maintain a corporate’s records by getting an external verification of its sustainable performance. This is enabled by the EU taxonomy model to avoid greenwashing.

Are you ready for your treasury journey? 2022 promises to be another exiting year with many opportunities to drive the Treasury function forward. The three main topics described in this article highlight the longer-term trend of Treasury moving closer to the business. The changing role of Treasury towards a comprehensive value-added center towards the business often requires a transformation in the Treasury organization. Zanders looks forward to discussing these and other trends with you and to support you on your treasury journey in 2022!

References 1) 2021 Global Payments Report by Worldpay from FIS 2) Common Global Implementation – Market Practice Group (formed October 2009)

A Treasury Technology Roadmap to S/4HANA

September 2021

7 min read

Author:

Greg Williams

Share:

The corporate landscape is being redefined by a plethora of factors, from new business models and changing regulations to increased competition from digital natives and the acceleration of the consumer digital-first mindset.

This is particularly relevant for large complex organizations that are running SAP. The SAP S/4HANA move is complex and presents great opportunities and challenges. For the treasury within these large complex organizations it does not make sense to wait for the enterprise to formulate a roadmap as then the likelihood of the treasury requirements not being properly prioritized are high.

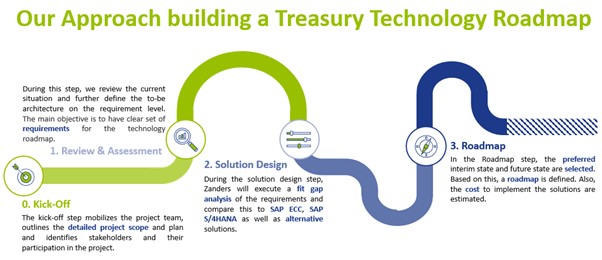

It is in this context that Zanders provides the option to help your organization formulate a treasury technology roadmap. Driven by 27 years of experience we have built a best practice framework for treasury transformation projects. The approach we have formulated for the treasury technology roadmap ensures that we start by focusing efforts on establishing a clear set of requirements for the treasury organization and processes. Here too we have built up a sound catalogue of strategic treasury requirements which are mapped to a solid treasury business process framework, and it is against this foundation that we engage with the treasury organization to ensure we emerge with an accurate view of the specific treasury requirements. In the process we ensure these requirements are categorized according to priority and evaluated relative to current available functionality.

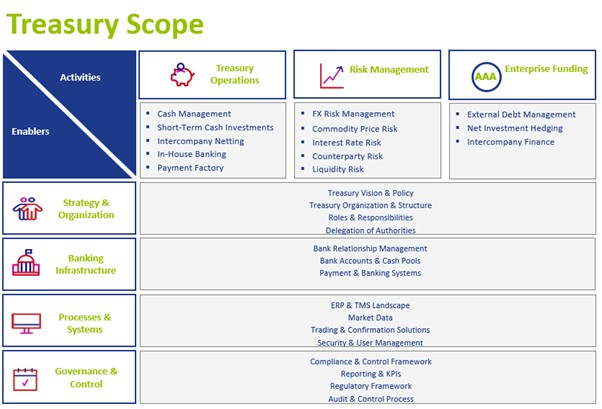

Enablers for core treasury activities We also establish a clear scope for the roadmap based on the activities to be covered which in effect defines the processes in scope. The Zanders framework uses three core treasury activities being Treasury Operations, Risk Management and Enterprise Funding with the associated 15 underlying sub-processes that support these.

The Zanders framework then has four enablers that support these core treasury activities. These are:

Strategy and organization

Banking Infrastructure

Processes and systems

Governance and controls

Typically for a treasury technology roadmap engagement, the focus is on the processes and systems enabler, but we will also take into the strategy and organization in formulating the scope of the assessment here the geographic and organizational scope is established and confirmed. For banking infrastructure, the banks, bank accounts and payment type scope is established.

Figure 1: Treasury Roadmap; Driven by 27 years of experience we have built a best practice framework for Treasury Transformation projects. Based on this framework and considering what has been requested by clients, we propose the following approach to build a well-defined Treasury Technology Roadmap.

Figure 2 – Treasury scope; The starting point for kicking off the roadmap is defining the functional scope in line with the three core Treasury activities (Treasury Operations, Risk Management, Enterprise Funding) and the relevant underlying 15 sub-activities.

Fit-gap analysis of requirement The next step in the process is solution design where we perform a fit-gap analysis of requirement and compare this to the existing and proposed treasury technology platforms. This analysis can be tailored to exclusively focus on SAP treasury solutions or include suitable alternative technology platforms. In addition, with the increase in available add-on solutions in the market this analysis can also be expanded to explore and expose the relevant technology solutions that fit the unique treasury requirements based on the prioritization established.