Fast-growing technological developments are accelerating the pace of change for treasury. Zanders and Citi have produced a whitepaper that reflects perspectives on the future of corporate treasury. Ron Chakravarti, Citi’s global head of treasury advisory, and Zanders partner Laurens Tijdhof discuss some of the key themes.

What are the main changes influencing treasury’s added value within corporates?

Laurens Tijdhof (LT): “Business models are changing. In the decades since the introduction of the internet, ‘digital natives’ - new multinational companies such as Uber and Google - have emerged to disrupt all industry sectors. These companies have less legacy than traditional multinationals. Treasury plays an important role in that digital native environment, for example with payment innovation in ecommerce. Traditional multinationals are typically dealing with a lot of legacy because of mergers and acquisitions throughout their history. For them, the change is more transformational in nature, as they are doing something different than they have done in the past decades or even in the past century. This is one of the elements where treasury can add significant value; to understand from a financial point of view where the business is in the current cycle and to see what things need to be changed, updated or optimized to add value.”

Ron Chakravarti (RC): “Firstly, the pace of change in commerce has picked up, driven by new technologies and new ways of doing business. These are shifting the timing, value, and volume of cash flows and, of course, that impacts treasury. Secondly, while treasury always has to manage regulations and the cash flow impact of changes in global taxation, the pace of change in these have also picked up. Finally, geopolitical uncertainty has created additional considerations at this point in time. Corporate treasurers, therefore, need to ensure their teams are increasingly nimble to deal with all of these issues. The good news is that the availability of new technologies, data and artificial intelligence have the potential to change how treasury works and to create added value.”

At which point are companies ready for new technology?

LT: “Before a company can enter the next stage of treasury maturity, it first needs to get the basics right. This means having a focus on centralization, standardization and automation, typically using traditional technology like a TMS or an ERP system. And if you have these systems in place, be sure you’re using and benefiting them optimally from that environment first. Once you have the basics right, you can go to the next stage of a smart treasury, using the new digital or exponential technologies. Then you can benefit from the good basis and use more of the data in analytical ways, with algorithms or newer technologies like robotic process automation (RPA) or artificial intelligence (AI).”

RC: “I completely agree that getting the basics right, by completing the journey to an efficient treasury comes first. Treasury is on an evolution path of becoming first efficient, then smart, and finally integrated. Getting to efficient means that you must standardize, centralize, and automate. Even among multinational companies, not all have mature, centralized treasury models. Getting to a best in class model is key. In most industries that includes a functionally centralized regionally distributed treasury model, with operational treasury on a common infrastructure and processes. Once you are substantially there, you can work on the next step change, in making the move to a smart treasury. And ultimately to an integrated treasury.”

How should a treasurer deal with the continuous change driven by these exponential technologies?

RC: “Well, an issue is that – as The Future of Treasury whitepaper indicates - only 14 percent of corporates have a digital strategy at the treasury level. Why is this so low? One reason is the availability of the right resources. While treasurers have previously adapted to technology change, this change is all happening a lot faster now - for treasury and the broader business. Ultimately, treasury is all about information. Today, more than ever, the treasury function needs to include people who are technologically savvy. People who are able to comprehend what is changing and how to best deploy technology. That will become increasingly important to create value for the business. Treasury teams recognize that they need to have a digital strategy, but many of them are not fully equipped to define one. They are looking for help from industry leaders with a treasury framework to define their digital treasury strategy. That is one of the reasons for this collaboration between Citi and Zanders; in many cases we recognize that we can better do it together, creating added value for our mutual clients.”

LT: “If you compare the current situation to ten years ago, a treasurer would only buy new technology if there was a real requirement. Today, there’s new technology that many treasurers do not fully understand – in terms of what problems it could potentially solve for the company. What you often see now is that treasurers start with small projects, proofs of concepts, to test some innovative ideas. You can compare it with the iPhone; when Steve Jobs invented it, it took some time before people really understood what to do with it, what value it would add in their life. First you need to see what it is, what it can do for you, whether it can solve a real problem. That’s the exiting stage in which we are now. Some treasurers are trail blazers, others are more followers that first want to learn from others about how it has brought them forward.”

Where can these latest technologies really improve treasury? Are there any issues they cannot solve?

LT: “Treasury is all about information and data. There’s a lot of information available in a treasury environment and you sometimes need new technologies and standardized processes to unlock the value out of these data. Treasury covers a large amount of structured data in all kinds of systems. If you want to translate that data insight into valuable conclusions, then technology is probably the right enabler to help; with data analytics and visualization, for example. But, if you don’t have your data centrally available in a data warehouse or data lake, then that’s the first part you should work on; you first need to have your data centrally available to be able to do something with it. Unfortunately, many large multinational companies are still in that stage, they still have data that’s very fragmented and decentralized. For those companies, you could say that the newest technologies have come too early.”

RC: “What will improve treasury? We should first consider what treasurers are seeking to do. Today, we are seeing an increasing appetite from corporate treasurers for integrated decision support tools going beyond what treasury management systems can provide. To that end, we at Citi are running a number of experiments, collaborating with our clients and fintechs, and enabling our clients’ journey towards smart treasury. This is about moving beyond descriptive analytics to decision support and decision automation, and offering opportunity to realize the full automation of operational treasury. What won’t be solved? Well, we won’t get there in 2020 but we will certainly soon start seeing the foundational steps in this transition to a fully automated operational treasury and that’s what is so exciting.”

MuniFin is one of Finland’s largest financial institutions, specialized in financing local government and state-subsidized social housing production.

As MuniFin has been growing fast in recent years, the bank is now under the supervision of the European Central Bank (ECB). This means complying with the corresponding regulations, particularly in the field of asset and liability management (ALM). How does the organization deal with the new ALM challenges?

MuniFin, the shortened name for Municipality Finance Plc, aims to promote welfare in Finland through the financing of municipal projects related to basic infrastructure, healthcare, education and the environment. Therefore, a significant portion of its lending is used for socially responsible projects such as building hospitals, healthcare centers, schools, day care centers and homes for the elderly. Finland’s local government sector is characterized by a high degree of autonomy over financial matters and strong credit quality, which is reflected in the high quality of MuniFin’s loan portfolio.

We do 200 to 300 transactions in the funding market, in almost 20 different currencies. This results in quite a bit of complexity.

Pyry Happonen, head of ALM at MuniFin

International player

MuniFin operates domestically, but is an international player, says Pyry Happonen, head of ALM at MuniFin: “We do all of our lending in Finland, but we fund our operations through international capital markets. Traditionally we have been very flexible in terms of funding. Each year we do 200 to 300 transactions in the funding market, in almost 20 different currencies. This results in quite a bit of complexity.”

In the meantime, MuniFin’s balance sheet has grown significantly in the last few years, to approximately EUR 35 billion. Simultaneously, the number of people working at MuniFin has increased to 149. As a result, the bank moved from domestic supervision to European supervision. Together with many developments in the financial markets, this has brought new challenges for MuniFin. European supervision raises the bar continuously regarding risk management.

“We therefore need to stay on top of things”, says Pasi Heikkilä, head of Treasury at MuniFin. “Not just by checking the boxes and fulfilling the requirements. To maintain our profitability and reduce risks, we need to improve the way we work too.”

External requirements and internal goals

According to Heikkilä, the changes bring both challenges and opportunities. “We’ve been directly regulated by the ECB since 2016 and our focus has been very much on complying with all ratios and liquidity requirements. We also want to put more focus on the long-term profitability side. The external requirements and our internal goals can strengthen one another. Both encourage us to look at ALM in different ways and to manage our balance sheet more efficiently.”

In terms of interest rate risk management, MuniFin is compliant. “We can manage our economic value of equity (EVE) and our net interest income (NII),” Happonen explains. “But we also wanted to dive a bit deeper than ticking the boxes and to find an optimal way to manage this risk. We wanted to enhance the capabilities and at the same time, we were looking for a third party to share and discuss our thoughts on our interest rate risk strategy. We therefore engaged with Zanders; to review the strategy and to ensure that we are optimally managing our profitability with regards to interest rate risk. Furthermore, we want to ensure we are fully leveraging the increased data and modeling capabilities.”

Iterative process

Ensuring compliance and simultaneously striving for improved internal risk management has influenced MuniFin’s strategy, says Heikkilä: “It’s an iterative process, a constant development which happens in cycles. For a relatively small company like ours, additional support is welcome. We continuously have active dialogues with our peers. But not all information is open; market participants cannot always share all information. So, in some cases we consult experts like Zanders, to help us with gap analyses so that we can figure out what to further improve on.”

Better quality data

In the current regulatory environment, managing a balance sheet efficiently is not a trivial task, Heikkilä explains. “Balance sheet profitability and risk need to be managed and optimized while considering multiple metrics, like the liquidity coverage ratio (LCR), the net stable funding ratio (NSFR) and the leverage ratio. To ensure liquidity is priced correctly and to have a sustainable profit margin, a robust funds transfer pricing (FTP) framework is required. At the same time, this needs to be done in a cost-efficient manner and with good data and systems.”

To meet these requirements, MuniFin is significantly improving its data and modeling capabilities too, to provide the company with reliable information on a daily basis.

“To ensure liquidity is priced correctly and to have a sustainable profit margin, a robust funds transfer pricing (FTP) framework is required”

Pasi Heikkilä, head of Treasury at MuniFin

“Latency is decreasing”, says Happonen. “We can do analyses and calculations more frequently. In Finland the big banks are investing hundreds of millions in their IT and systems. They are getting rid of legacy systems and bringing in new software, in order to improve quality of data and modeling capabilities to enable good decision-making. This is key in going forward in ALM; subpar data and Excel files no longer cut it. We are also proactive on this front, investing in our data collection and modeling capabilities for better analyses on a more frequent basis, with up-to-date data. And of course, technology helps us to make better strategic choices too, concerning managing interest rate risk, net interest income and so on.”

Green finance

In terms of the future strategy, green finance is a very important topic in MuniFin’s plans. The bank offers green financing, funded by green bonds, for projects that promote the transition to low-carbon and climate resilient growth. Sustainability initiatives and climate change ambitions are increasingly key in financing, according to Happonen.

“On the global bond market many investors are craving for green bonds”

Pyry Happonen, head of ALM at MuniFin

“Green finance is a very big thing for us. We are lending to a lot of domestic green projects, like public transportation. And we report the impact of the green financing we’ve done. On the global bond market many investors are craving for green bonds. The better our ALM strategy, the more optimal our profitability and risk return profile are and the more we can contribute to sustainability too. It means that we need to be sustainable in all senses, so both financially and environmentally.”

Sustainable balance sheet management: Running a sustainable business model requires maintaining a sustainable balance sheet. A stable profit margin and a risk profile that is in line with the risk appetite is essential. Finding the balance between risk and profitability can be a challenging task that requires continuous monitoring and steering. On the one hand, long lending with short funding results in high margins and therefore great profitability, in the short run. However, such a position yields significant risks in the longer run. As interest rates increase, more expensive funding is required, potentially resulting in a negative margin. Only by making the right trade-off between risk and profitability, and therefore between the short-term view and the long-term view, can a sustainable balance sheet be maintained.

Separating AkzoNobel’s sprawling operations into two distinct businesses required aligning complex financial systems and bank relations efficiently.

Dutch company AkzoNobel is known worldwide for its coatings and specialty chemicals for both industry and consumers. As part of a new strategy to accelerate growth and value creation, the multinational decided to spin off its chemicals division. The challenge was to do this in just eight months. How did AkzoNobel’s treasury manage to split its activities into two?

With activities in more than 80 countries and 46,000 employees, AkzoNobel has a turnover of around EUR 14 billion. In April 2017, the company decided to change its strategy and transform itself into two high-performing businesses focused on coatings and specialty chemicals. “We needed to embark on a new strategy to build two strong independent companies”, says Gerrit Willem Gramser, head of treasury at AkzoNobel. “This plan had been on our mind some for some time, but was accelerated by market forces.”

Apart from timelines, the challenge in this project was to set up the new environment technically, with the right master data.

Laura Koekkoek, Partner Treasury Advisory Group

Rules of engagement

The announcement to split up the company went out on April 1st, 2017. “We almost immediately started having discussions for treasury on how to digest this”, says Gramser. “In Q1 of 2018 we wanted the company to be completely separated. So, as treasury, we started to do our math backwards. And we realized, given the timelines, it was probably something we couldn’t fully execute ourselves. When you realize that, all other decisions fall into place.”

AkzoNobel’s treasury department had already gone through a bank rationalization and had a fit-for-purpose treasury management system (TMS), in the form of SAP Treasury. “The system was complex, but it fit our needs very well”, says Joshua Watts, treasury infrastructure and project manager during the internal spin-off activities. “With the tight timelines, the first thing we decided as a treasury team, was to determine our so-called ‘rules of engagement’. We needed full focus on replication, duplication, cleansing – and not transformation. The treasury management structure we had was a strong solution. We’re going to continue working as one team and apply strict strategic discipline to meet our deadlines. That was our starting point.”

Treasury setting the scene

To achieve its aims, AkzoNobel required more resources than were available internally. “We were cautious about the deadlines”, says Watts. “The infrastructure we had was built, to a large extent, with the continued support of Zanders. We already had a long-running partnership, so we said: this is where we want to go – can you support us? By the end of June we had started and according to the planning, which was aligned between AkzoNobel and Zanders, we should have the system up and running by the first of January 2018.”

AkzoNobel also built up a cross-business project management office (PMO) to manage the separation from a group level, for all functions. The governance for the project consisted of the central PMO and expert-separation teams for treasury, tax, HR, commercial, accounting and other functions. “Beneath that we had local separation teams to deal with the local issues”, says Gramser. “We aligned ourselves as treasury in that expert-separation team in which the separation of our cash management and treasury technology were our primary deliverables. It was a layer of projects with a portfolio management on top of it. In the end, that structure worked very well. We started very early, so instead of watching how the rest of the company would approach the separation, we immediately formulated a plan. Quite deliberately we made choices in the beginning of the process – from a timeline and resources perspective – and that was crucial.”

From a systems point of view, the SAP Treasury system was cloned and the set-up was adjusted to fit the new bank account landscape. Watts says: “The system was already built for purpose and, as such, we had a good starting point for both companies.”

Integrated complexity

During the project, the main challenge was to align the cash management stream and technology stream. The idea to clone the system and not to build a new environment and cash management structure was therefore an important decision, says Zanders consultant Laura Koekkoek. “Apart from timelines, the challenge in this project was to set up the new environment technically, with the right master data.”

Decisions needed to be made regarding which entities belong to the coatings business and which to the chemicals business. Some entities needed to be split and it took time to arrange these new legal entities. For the integration at the end and to test the new solution, the bank accounts also needed to be ready, as well as the banking infrastructure. Koekkoek adds: “But at the end, all bank accounts were open, with all legal documentation in place.”

That was an achievement, according to Watts. “Everything is so integrated; you can’t start on one area without knowing the status of the other. The complexity is that – apart from all of the individual legal entity or bank account issues – there are so many interdependencies. You can’t approach the TMS separately from your global cash management activities. At a certain point we put a lot of energy into the so-called long tail of the separation. Small entities or small branches, that have a small impact on the overall figures, were consuming a significant amount of project resource time. So at a certain stage we changed the priorities to the bigger impact issues.”

We needed full focus on replication, duplication, cleansing – and not transformation

Joshua Watts, AkzoNobel

Team effort

Across AkzoNobel, the vast majority of the teams were already allocated to the specific business units, so fully separated. Both parts are and remain active in the current global markets. Gramser notes: “The two separated businesses are both good businesses, but they have different futures. And that will be the same for the treasury environment. But starting from now, the businesses can run very well on what we’ve given them.”

In March 2018, AkzoNobel announced the sale of its specialty chemicals part to The Carlyle Group and GIC. “Irrespective of the new owner’s system, our function was to be ready, no matter what scenario. That has been successful, with treasury being an early mover, having a clear plan and sticking to these rules of engagement. We’ve been quite brutal in protecting our own boundaries and guidance. The ‘as-is principle’ was leading: this is what you get. Treasury is an integrated, global operational function.”

According to Watts, the project’s success was a real team effort: “The interaction was great, on all levels. Compared to the more generic technology consultants, Zanders is much more strategic in its advice. We understand each other’s language and our teams were quite impressed by the efficiency of the work. There was good integration, good communication. It was on time, on budget – we’re very pleased.”

Endemol Shine Group transformed its decentralized treasury by centralizing operations and unlocking trapped cash, leading to award-winning innovations and enhanced financial efficiency amid a growing demand for scripted productions.

Endemol Shine Group (ESG), a private equity-owned, Dutch-based media company with global operations, is the world’s largest independent producer and traveler of formats. The company has grown mainly through acquisitions, resulting in a treasury organization that was largely decentralized. In 2017, the new treasury team opted for a full treasury transformation project, to unlock the available potential and to support the business’s growth ambitions.

With activities in more than 80 countries and 46,000 employees, AkzoNobel has a turnover of around EUR 14 billion. In April 2017, the company decided to change its strategy and transform itself into two high-performing businesses focused on coatings and specialty chemicals. “We needed to embark on a new strategy to build two strong independent companies”, says Gerrit Willem Gramser, head of treasury at AkzoNobel. “This plan had been on our mind some for some time, but was accelerated by market forces.”

Moving to more scripted productions has led to significantly longer cash conversion cycles, which increased working capital needs

Albert Hollema, Treasury Director at Endemol Shine Group

In 2017, Endemol Shine Group created over 800 productions in 78 territories, airing on more than 275 channels around the world. The group’s turnover is around 2 billion euros. Global hits include many non-scripted formats such as MasterChef, Big Brother, Your Face Sounds Familiar, Fear Factor and Hunted. The company's scripted business focuses on scripts for films and television series with a longer life cycle, such as the drama blockbusters Black Mirror, Humans, Peaky Blinders and Broadchurch. These series were each sold in at least a hundred regions. Another example is Sweden’s critically acclaimed hit Bron/The Bridge, which has been successfully adapted for different local regions.

As the group has mainly been growing through small acquisitions and the merger of the Endemol and Shine business, the decentralized treasury organization lacked full visibility at a central level. Consequently, treasury head office wasn't aware on a daily basis of the cash movements and other activities of thousands of bank accounts at more than 40 banks, resulting in high amounts of trapped cash. Besides, the company is highly leveraged with limited additional borrowing opportunities. Although a treasury management system was in place, it was mainly used to maintain intercompany accounts only.

Time for change

In early 2017, the treasury team underwent some changes and was slightly expanded. In the meanwhile, the demand for scripted business started to grow quickly. “For these scripted productions we need to invest more, and the broadcaster pays ESG later due to the longer production time”, Albert Hollema, treasury director at Endemol Shine Group, explains. “So, due to the longer life cycle of these productions, our opcos (operational companies) were increasingly demanding more working capital. For us there is no real credit risk – we always have signed contracts before we start to produce, so we know that the client is going to pay – but we need to bridge the gap between producing and getting paid. The cash conversion cycle is important for us. Moving to more scripted productions has led to significantly longer cash conversion cycles, which increased working capital needs. The non-scripted productions, like The Wall and Deal Or No Deal, have shorter cash conversion cycles and are therefore important for financing our business.”

Hollema explains: “We are a highly leveraged company and have a credit rating of CCC+, so for additional financing we can’t simply go to a bank to invest in working capital. Also, our two shareholders – Apollo and Fox – were not really looking to put more money into the business.” The increase in working capital thus had to come from the company’s existing resources. Hollema says: “There was a lot of cash in the organization, spread over all different bank accounts and in different entities on different locations. If we could unlock that amount of trapped cash, we would find our source of finance. That’s why we started a treasury transformation project: to make our treasury activities more efficient and to use the cash within our company to finance our growth. Because by developing the business, we generate higher profits and a higher cash flow which will help to reduce our debts and get out of the highly-leveraged situation.”

To a better category

The group’s treasury transformation included improved use of a treasury management system (TMS), bank connectivity and new treasury processes. Hollema adds: “We needed our TMS supplier to be a business partner, providing us with a solution that would really help us in today’s markets. We reached out to several providers and at the same time we had contact with Zanders, who was already supporting us on some treasury matters. They told us about their new offering, the Treasury Continuity Service, consisting of a certain number of consultancy days per month on which they support treasury, with provision of a high-end TMS and including access to their knowledge database. The service looked very helpful and was a good fit for our needs. We are a relatively small business and had just experienced a lack of interest from system providers, but due to the support of Zanders we moved to a better category on the system vendors’ lists. So, we got a state-of-the-art system that we normally wouldn’t have bought. Another important thing for us was that it offered us a software as a service (SAAS) solution, which basically needs no internal IT support. Updates are done on a regular basis and keeps our system up to date all the time. Overall, the combination of supporting elements was attractive for us.”

During the EuroFinance conference, the audience was impressed by what we had achieved in such a short time frame

Albert Hollema, Treasury Director at Endemol Shine Group

The award winning show

According to Dave van der Zwan, deputy treasurer at Endemol Shine, the implementation process went quick and smoothly: “As a team we worked closely together and within four months we were live on FIS Integrity SaaS.” At the same time, the company decided to set up new bank connectivity via Swift to receive the bank statements and access liquidity through the TMS in an efficient way. “We have a lot of opcos and learned that as a group we held over 1,000 bank accounts – and the information on these accounts was previously only available by the end of the month and a subsequent week for major opcos after the cash flow forecasting was submitted. With the managed bank connectivity solution from FIS’s Swift Service Bureau, we managed to get connected to all our banks directly to pick up all balances from all the opcos on a daily basis. Now we can see exactly how much money an individual opco holds and how much money can be extracted from it. That’s very helpful. During the implementation we opted for active pulling of balances as well – giving ourselves authority to move funds in and out of the opco accounts.”

The innovative system solution won two awards. Global Finance awarded the group for the ‘Best Treasury Management Systems Program’ and Treasury Today gave an Adam Smith Award in the ‘Highly Commended – One to Watch’ category. Hollema notes: “During the EuroFinance conference in October 2017, we presented our case and the audience was impressed by what we had achieved in such a short time frame; the solution, approach, and project management together with the scrum approach, cutting the process into small pieces.”

Bridging the gap

So what exactly made this project so successful? Van der Zwan says: “Our aim was to unlock funds for our investments in working capital. By freeing up that liquidity we were able to keep funding the business according to plan and without any need to postpone certain productions. The business case was easily made from a treasury perspective, it pays for itself quickly, but it also unlocks the liquidity we need in order to be able to grow the business. During the process, there was a snowball effect by which we’re moving from one improvement to the next. Also, the opcos realized what we were trying to achieve and proposed their own initiatives, which fitted perfectly in our overall strategy. A lot of elements came together and were unlocked in this transformation process by a small and high-quality team of Endemol Shine and Zanders people.”

Hollema adds: “From the investment point of view the treasury transformation project was a real success. By unlocking trapped cash for the company, the whole business case is basically paid out of the savings achieved in the first six months. Remember our financing costs are high given our CCC+ rating. We started to build in mid-2017 and by the end of the year the investment in the transformation was repaid, from that perspective.”

To be continued

It was the first time that the company’s head office was centralizing some activities. Van der Zwan says: “If we had taken a ‘big bang’ bank rationalization approach and required opcos to change their invoicing details, electronic banking, etc., we would have seen strong resistance. But instead we said: you can stay with your bank, things will remain as they are, we only want visibility and access. We wanted the transformation to disrupt as little as possible but on the other hand we knew exactly what our end goal was. Step-by-step, with support from the opcos, we will move to that end goal. Once you take the first step, the next step is obvious, and that response was exactly what we saw from our opcos. The support we received from both management and opcos was a big help during implementation.” Zanders consultant Adela Kozelova adds: “Endemol Shine’s treasury acted quickly, while doing things step-by-step, to get as many people on board as possible – a good example for many companies.”

With greater visibility of the company’s cash, the treasury team will be able to better evaluate which businesses are performing well and where to allocate capital. Hollema concludes: “We now pick up information via the bank statements, which doesn't require additional reporting from the opcos, but is very useful for us as a group and can even be seen as an early warning indicator on how our businesses are performing. The next steps involve the creation of cash P&Ls and cash flow overviews from this info, eliminating more manual processes by integrating the local ERPs with the FIS Integrity Solution to help improve real-time cash forecasting. Better control over FX and simplification of the IC settlement process by optimizing the in-house bank (IHB) module are also high on the priority list. The banks and bank accounts will need to be further rationalized to help the opcos. They do a lot of things that can better be centralized so they can focus on doing business. We are a business partner to our opcos, we take care of the whole financial logistics. Zanders and FIS are our sparring partners and we use them to discuss what to do in the next phase.”

In the summer of 2015, Johnson Controls International (JCI) announced that it would divest its Automotive Division via a spin-off in a new publicly listed company: Adient. Shortly thereafter, JCI announced a merger with Tyco, a fire protection & security company. What was the impact of these strategic transactions on the treasury activities of the company?

JCI is the global leader and largest manufacturer of automotive batteries, powering nearly every type of passenger vehicle, heavy-duty and light commercial trucks, motorcycles, golf cars, lawn and garden tractors, and marine applications, and a leading provider of building technology, products, and solutions (building automation & controls, HVAC, refrigeration, fire, security, and integrated solutions). The multinational has USD 30 billion in sales and employs 120,000 employees spread over 2,000 locations on six continents. Building automation & controls, HVAC, refrigeration, fire, security, and integrated solutions are part of the Building Technologies & Security (BT&S) division and represent the majority of sales: USD 23 billion. The Power Solutions division has sales of USD 7 billion. One in three cars around the world is powered by a Johnson Controls battery. There are over one billion cars in circulation globally, and with a production of 150 million batteries a year, JCI is a world leader in this field.

Increasingly less automotive

Three years ago, JCI had a very different company profile. Its activities were divided into four divisions, including a very large Automotive division mainly focused on the interior of the vehicle. This division consisted of two parts: Automotive Seating, which manufactured car seats, and Automotive Interiors for the production of dashboards, floor and overhead consoles, and door panels. A fourth division, called Global Workplace Solutions, provided facility management services for third-party buildings. “We first divested Global Workplace Solutions by selling it to CB Richard Ellis. We subsequently contributed our Automotive Interiors division into a joint venture with Yanfeng, one of the largest automotive suppliers in China. Then the company decided to dispose of the entire Automotive division – including the stake in the Yanfeng joint venture – in a spin-off,” says Jean-Philippe De Waele, VP & Treasurer EMEA, responsible for the treasury activities in the EMEA region. “This division eventually became an autonomous publicly listed company called Adient.” But prior to completing the spin-off, JCI merged with Tyco, where JCI’s building automation & controls, HVAC, and refrigeration activities were combined with Tyco’s fire and security activities.

Automotive represented more than half of JCI’s revenue when the spin-off of Adient was announced in July 2015. The operational spin-off had to be realized in a very short time frame, with Adient becoming a fully independent unit under the JCI umbrella by July 1, 2016. All the teething problems had to be identified in a dry run period of several months in order to properly and efficiently execute the legal spin-off on October 31, 2016. After all, the entire Automotive division had to be completely disconnected in terms of processes, systems, and employees.

Systems and people

In a very short period of eight months, a brand new treasury department had to be set up from scratch to support Adient, a global organization with revenue of USD 17.5 billion. In the fall of 2015, JCI was looking for external consultants to assist with the treasury spin-off project. Jean-Philippe De Waele explains: “Because we knew we could never accomplish this without external help, I visited EuroFinance in Copenhagen looking to secure the right consultants. A large part of the treasury spin-off consisted of implementing a treasury management system for Adient. Given the time constraints, we therefore decided to copy JCI’s current treasury systems and processes to Adient. As Zanders successfully assisted JCI in 2010 with the initial implementation of our treasury management system, Quantum, it was a logical choice to reach out to Zanders for this part of the spin-off work as they were already familiar with the system, processes, and people.”

JCI first upgraded its current system from version 4.6 to 6.2 and then cloned it for Adient. Jean-Philippe De Waele: “It was a very intense project as we had to go live on July 1. As part of our global liquidity management and inter-company netting processes, we use a cross-currency notional cash pool at Bank Mendes Gans (BMG). A similar structure was set up for Adient, and Zanders assisted with its implementation.”

Zanders helped us to audit, streamline, and improve the back-office processes.

Jean-Philippe De Waele, VP & Treasurer EMEA

Merger

In January 2016, employees learned that JCI – for the part that did not continue as Adient – was going to merge with Tyco, a company that provides fire and security systems. The merger with Tyco took place on September 1, 2016 – two months before the spin-off of Adient came into effect. As a consequence of the merger, JCI had a new footprint of treasury centers around the world. Jean-Philippe De Waele explains: “The US treasury center of Tyco was located in Princeton, New Jersey, while we were based in Milwaukee, Wisconsin. In Asia, they were in Singapore, and we had offices in Hong Kong and Shanghai. In Europe, they were in Switzerland, while we had an establishment in Brussels. And while we were in Brazil, Tyco did not have an active presence in Latin America. It was clear that there had to be a rationalization in treasury centers. In the US, the office in Princeton was closed; in Asia, everything was concentrated in Shanghai, and in Europe, it was decided to keep Tyco’s treasury center operating as a satellite of Brussels.”

With the merger of the treasury centers in Brussels and Zürich, it was necessary to determine which processes would be conducted where. “Because Tyco had an established and operating back office in Zürich and our back office in Brussels operated post spin-off with temporary workers and Zanders consultants, we decided to centralize our back-office activities in Zürich. Zanders helped us to audit, streamline, and improve the back-office processes, and then we transferred those operations from Brussels to Zürich.”

Trade finance

When the transfer of the back-office activities and other treasury integration work were successfully completed, a new internal project started at JCI: the implementation of a new trade finance system. This project was also a result of the merger with Tyco. Jean-Philippe De Waele: “We have a fairly extensive portfolio of bank guarantees and letters of credit. We have about 8,000 bank guarantees outstanding, amounting to approximately USD 1.2 billion. We also have a large portfolio of parent guarantees. At JCI, we did not have a system in place while an old trade finance system existed at Tyco. The integration activities triggered us to think about what should be done in this area. Move from no system to the Tyco system? Or would it be better to switch to a brand new system? Zanders analyzed the Tyco system and compared it with the current needs of JCI, where Swift connectivity is extremely important. The conclusion of this audit was that the cost of upgrading Tyco’s legacy system would be about as high as the implementation of a brand new system. That is why we decided to implement a new system, GTC (Global Trade Corporation), in which all communications with banks occur via Swift. Zanders is assisting with the implementation and the onboarding of the various banks on GTC and Swift.” The project started in mid-September, and the first bank will go live in February 2018.

Decommissioning

With the merger, whereby Ireland-based Tyco International Plc acquired the US-based Johnson Controls, Inc., the new parent company (Johnson Controls International Plc) was incorporated in Ireland. “As all our derivatives trading is done in the name of the parent company, a lot of work was done in transferring our hedging activities – FX and commodities – from the old (Johnson Controls, Inc.) to the new (Johnson Controls International Plc) dealing entity, and Zanders supported us with this transfer,” says Jean-Philippe De Waele. “Tyco operated a very large in-house bank which we decommissioned. In addition, we dismantled Tyco’s notional cash pool and integrated it into our BMG cash pool structure. We transferred all Tyco’s hedging activities from its treasury management system (IT2) to Quantum, and all Tyco banks were on boarded on our AvantGard Trax system (Global Payment Factory) and Swift.”

Awards

The list of projects gives an indication of the extensiveness of the treasury operations at both companies. After the spin-off of Adient, Johnson Controls was a company with USD 20 billion in sales. Tyco was a company with sales of USD 10 billion, bringing total group sales to approximately USD 30 billion. As Jean-Philippe De Waele notes, “During the merger of two such large companies, there are significant integration efforts at all levels, including the treasury level.”

Looking back at the projects, Jean-Philippe De Waele is very satisfied. “The work accomplished for the Adient treasury spin-off was impressive,” he says. “This is also recognized outside of JCI. We obtained two awards for the work that we have done in this regard. One from CFO Magazine as ‘Best finance team - best treasury practices’, and one from Treasury Management International Magazine, for ‘Best Treasury Transformation’. In addition, we received several requests to share our experiences concerning this project - including ATEB, the Belgian Association of Corporate Treasurers and at the EuroFinance conference. Our practices have become a showcase for many people on how to best handle a spin-off and carve-out of a business division.

Future

Under Jean-Philippe De Waele’s stewardship, there are still a number of ongoing integration activities relating to banking and cash management that will continue over the next 12 months. “Zanders will remain onboard until an initial group of countries have become active on the new trade-finance platform. Meanwhile, we have completed the recruitment of our additional analysts, who will be managing our BMG cash pools.” We are never sure what the future will bring, notes Jean-Philippe De Waele. “The company has been very active in M&A and divestments over the past three years and publicly stated that it is focused on creating long-term shareholder value in the remix of its business portfolio. For example, as we were integrating Tyco, the company decided to sell part of its business (Scott Safety) to 3M, a US company. So who knows…”

Gasunie has managed the Dutch gas network since 1963, when natural gas was first produced at Slochteren. In recent years the energy mix has changed, with the focus now more on sustainable energy sources. But Gasunie has maintained its involvement, capitalizing on the key role that gas plays in the current energy transition. The changing strategy of this gas distributor has also had a bearing on the activities of its treasury department.

Gasunie, which is wholly owned by the Dutch government, transports natural gas through more than 15,500km of pipelines in the Netherlands and Germany. In addition to these pipeline systems, Gasunie’s assets comprise hundreds of installations, including one for liquefied natural gas (LNG), an LNG import terminal and facilities for underground gas storage. Every year, the company transports approximately 125 billion cubic meters of natural gas, equal to about a quarter of Europe’s total gas consumption. As a bona fide gas country, the Netherlands has become ‘Europe’s gas hub’, the central trading place for gas.

Terrific challenge

One of the government’s key objectives is to make the Netherlands one of the most sustainable countries in Europe by 2020. To limit climate change, the country is currently working on an energy transition: a switch to a CO2 free energy supply. This means that fossil fuels will increasingly be replaced by fully renewable energy sources, such as solar, wind and geothermal energy, and biogas. Due to this, natural gas, which is undisputedly the least polluting fossil fuel, has now been cast in a somewhat less-than-positive light. “You just have to mention energy transition and the level of uncertainty is very obvious,” says Janneke Hermes, manager of corporate finance & risk advisory at Gasunie. “And there are plenty of givens. But many people don’t have the right information – about the reliability of energy sources, their costs and what they can be used for. Solar panels on roofs have become symbolic of renewable energy, but even if they covered all the roofs in the Netherlands, they could only generate a limited percentage of the country’s energy requirements. So much more needs to be done. The role played by gas is, and will remain, crucial in the energy transition. This will increasingly be renewable forms of gas, such as gas from biomass, or hydrogen that can be obtained from wind energy. But natural gas also has a role to play, because it can reduce CO2 emissions significantly using it instead of coal in power stations. The big challenges we face are how to connect all the energy lines in the near future and how it should all be organized. It’ll take a lot of time and money and it constitutes a very substantial challenge for the Netherlands and the rest of Europe.

Hydrogen

Gasunie is already involved in a number of innovative projects. “Many impressive projects are already being carried out, by players big and small,” explains Hermes. “TenneT, for example, wants to harvest offshore wind energy on the North Sea, on a large scale, and our contribution can be to convert the excess electricity into hydrogen and transport it via existing gas pipelines to land, where it can be used as renewable fuel.” Adding CO2 to hydrogen produces methane, which can be introduced to the gas network as a gas. A further advantage of doing this is that hydrogen, or the gas that it helps to produce, can be stored as a buffer for subsequent energy generation or use. Many industries already use hydrogen in their production processes, continues Hermes. “Naturally, we are exploring how, with the existing infrastructure in our country, we can optimally exploit and facilitate this fact.”

Into Europe

In addition to its network in the Netherlands, Gasunie also has one in Germany, which also plays a key role in the security of supply of natural gas to the Netherlands. “Our number one strategic pillar is to remain the reliable, safe player in the Netherlands when it comes to gas infrastructure,” assures Hermes. “To this end our focus is very much on the storage of energy, during both the summer and winter and on a daily basis too. In other words, monitoring peaks during the day and deciding how to cope with them. Our second pillar is the facilitation of the gas markets elsewhere in Europe.”

While in the Netherlands gas has fallen out of favor – as a result of the earthquakes in Groningen, for example, and because it’s a fossil fuel – the opposite is true in the rest of Europe. Gasunie’s strategy looks beyond the Netherlands, Belgium and Germany. “We are looking further afield – the gas market is developing very strongly outside the North European area. The further you venture into Europe the more popular gas seems to be, to the extent that in some regions it’s akin to an emerging commodity. Thanks to our knowledge and expertise we can help, facilitate and invest in those markets. For example in the construction of new pipelines and networks, and new LNG terminals. I’m talking about countries in which we want to accumulate experience step-by-step, starting off by providing advice and service. Later this can be expanded into participation in a consortium in proportional stakes. We want to build up our presence incrementally.” According to Hermes, the third strategic pillar focuses on the afore-mentioned energy transition. “We are increasingly and emphatically demonstrating just how important a role we can play in all this. By supporting solar and wind energy, offering gas as a back-up, and making our own products more sustainable, or green. Green gas, by the way, is the same quality as natural gas. We are working on innovations that should lead to an increase in scale in the supply of green – so sustainable – natural gas.

Diversified supply

Alongside the transport of gas, Gasunie is also focusing on heating networks based on geothermal energy or residual heat. “Together with Eneco, the Port of Rotterdam Authority and Warmtebedrijf Zuid-Holland, the so-called Heat Alliance, we are trying to make optimum use of residual heat produced by the Port of Rotterdam for heating in the immediate region.

We are striving for open access in that market, with all customers and suppliers enjoying access to the infrastructure. Independence has always been a key aspect of what we do; we have no interest in the commodity. We make it possible for the various players – such as producers, customers, traders – to find one another. Our range of activities is currently very broad, from doing the right things today to exploring what’s possible in terms of tomorrow’s services and facilities and how we can contribute to their realization.”

The energy supply in the Netherlands is strongly dependent on gas. In 2016, a third of all energy in the Netherlands was supplied by natural gas. And due to the reduction of production from the Groningen field as a result of earthquakes in the province, its dependence on countries like Russia and Norway seems to have increased. This is why Gasunie wants the supply of gas to be as diversified as possible, says Hermes. “Customers find it important to have options; it prevents unilateral dependence. In this respect, southern Europe is gaining in importance because that’s where gas from the Middle East comes in. As a supplier of gas, Russia is still a very important partner for all of Europe, but this only strengthens the argument that LNG could be an excellent way of realizing the desired diversity.”

New Role

But just what do all these developments mean for the activities of Gasunie’s treasury? “Having made the necessary investments in the Netherlands’ existing gas infrastructure, we can now generate the kind of cash flow we expected,” insists Hermes. “Consequently, this will reduce the amount of debt we’ll need to take on. We have a reasonably diverse long-term loan portfolio and once that’s matured we’ll no longer need to refinance the full amount, which translates to a moderation of our financing needs. For our international activities, however, it’s not yet clear how much funding we’ll need. The same is true when it comes to green gas and supercritical water gasification projects. Relative to our assets, these all represent modest investments, but we don’t yet know how big they will become in future. Once their success has been proven, we’ll scale up projects like these. In terms of financing requirements, ours are indeed very diverse.”

That diversity has not escaped the attention of Gasunie’s treasury, while Hermes’ own role has also changed and become more diverse. “Suppose we’re talking about a benchmark loan of €500 million, it won’t be a problem because we’ve done something similar in the past. But if the discussion is about a new biogas hub with several farmers from Twente, for example, the dynamics become very different. We don’t yet have a contingency plan for something like that so we’ll need to be extremely flexible.” When financing these new, different types of projects, the sums involved are a lot lower, but the same cannot be said about the time the treasury has to invest. “That can sometimes be inversely proportional,” concedes Hermes. “But the contacts are also very different and this calls for a completely different skillset to what was needed before.” It also means that advice is asked more frequently from within the organization, she acknowledges. “Whereas we initially provided corporate financing, we now also extend loans to the business units themselves. This too calls for a different dynamic.”

Sustainable Cooperation

The first advisory role played by Zanders in Gasunie’s treasury activities dates all the way back to 2002, says Hermes. “So for me I’ve only known collaboration with Zanders. Back then it included SAP implementation, in which all kinds of instruments had to be configured. Since then we’ve been in constant contact; whenever the treasury needed support, we contacted Zanders. In May 2016, Lisette Overmars even took on the role of interim treasurer for several months. Our most recent collaboration was the adaptation of our treasury statute, which was necessary because we wanted our treasury policy to be aligned with our new objectives. In a broader context, Zanders has always proved an excellent sparring partner, one that asks us the right questions and provides the necessary structure for tackling the challenges our treasury faces. It’s what I’d define as an excellent and sustainable collaboration.”

If you would like to know more about treasury solutions in the energy sector, please contact our Partner Laura Koekkoek.

Treasury transformation refers to the definition and implementation of the future state of a treasury department. This includes treasury organization & strategy, the banking landscape, system infrastructure and treasury workflows & processes.

Treasury transformation refers to the definition and implementation of the future state of a treasury department. This includes treasury organization & strategy, the banking landscape, system infrastructure and treasury workflows & processes.

Introduction

Zanders has witnessed first-hand a treasury transformation trend sweeping global corporate treasuries in recent years and has seen an elite group of multinationals pursue increased efficiency, enhanced visibility and reduced cost on a grand scale in their respective finance and treasury organizations.

Triggers for treasury transformations

Why does a treasury need to transform? There comes a point in an organization’s life when it is necessary to take stock of where it is coming from, how it has grown and especially where it wants to be in the future.

Corporates grow in various ways: through the launch of new products, by entering new markets, through acquisitions or by developing strong pipelines. However, to sustain further growth they need to reinforce their foundations and transform themselves into stronger, leaner, better organizations.

What triggers a treasury organization to transform? Before defining the treasury transformation process, it is interesting to look at the drivers behind a treasury transformation. Zanders has identified five main triggers:

1. Organic growth of the organization Growth can lead to new requirements.

As a result of successive growth the as-is treasury infrastructure might simply not suffice anymore, requiring changes in policies, systems and controls.

2. Desire to be innovative and best-in-class

A common driver behind treasury transformation projects is the basic human desire to be best-in-class and continuously improve treasury processes. This is especially the case with the development of new technology and/or treasury concepts.

3. Event-driven

Examples of corporate events triggering the need for a redesign of the treasury organization include mergers, acquisitions, spin-off s and restructurings. For example, in the case of a divestiture, a new treasury organization may need to be established. After a merger, two completely different treasury units, each with their own systems, processes and people, will need to find a new shape as a combined entity.

4. External factors

The changing regulatory environment and increased volatility in financial markets have been major drivers behind treasury transformation in recent years. Corporate treasurers need to have a tighter grasp on enterprise risks and quicker access to information.

5. The changing role of corporate treasury

Finally the changing role of corporate treasury itself is a driver of transformation projects. The scope of the treasury organization is expanding into the fi nancial supply chain and as a result the relationship between the CFO and the corporate treasurer is growing stronger. This raises new expectations and demands of treasury technology and organization.

Treasury transformation – strategic opportunities for simplification

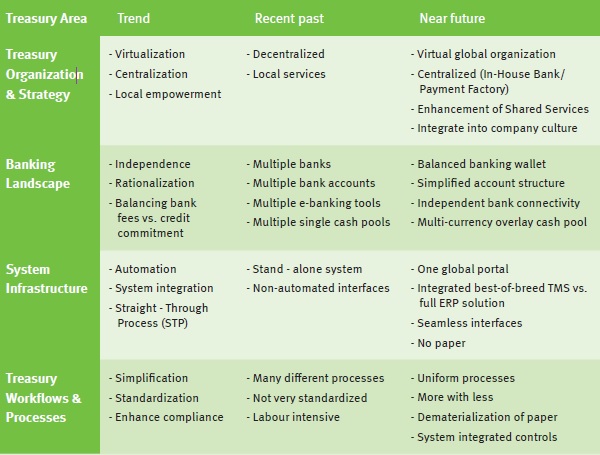

A typical treasury transformation program focuses on treasury organization, the banking landscape, system infrastructure and treasury workflows & processes. The table below highlights typical trends seen by Zanders as our clients strive for simplified and effective treasury organizations. From these trends we can see many state of the art treasuries strive to:

- be centralized

- outsource routine tasks and activities to a financial shared service centre (FSSC)

- have a clear bank relationship management strategy and have a balanced banking wallet

- maintain simple and transparent bank account structures with automatic cash concentration mechanisms

- be bank agnostic as regards bank connectivity and formats

- operate a fully integrated system landscape

Figure 1: Strategic opportunities for simplification

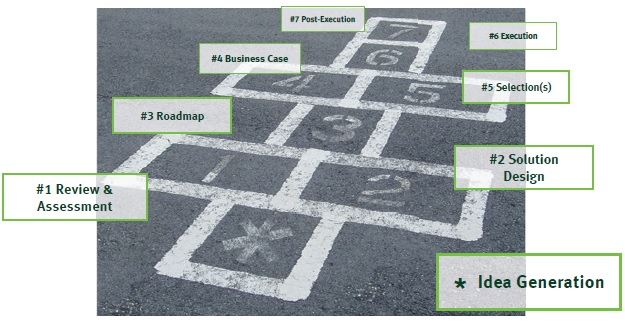

The seven steps

Zanders has developed a structured seven-step approach towards treasury transformation programs. These seven steps are shown in Figure 2 below

Figure 2: Zanders seven steps to treasury transformation projects

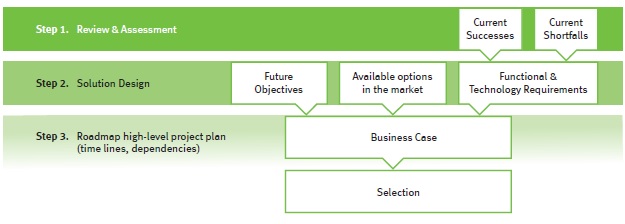

Step 1: Review & Assessment

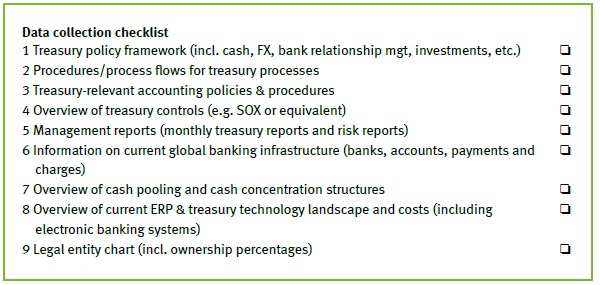

Review & assessment, as in any business transformation exercise, provides an in-depth understanding of a treasury’s current state. It is important for the company to understand their existing processes, identify disconnects and potential process improvements.

The review & assessment phase focusses on the key treasury activities of treasury management, risk management and corporate finance. The first objective is to gain an in-depth understanding of the following areas:

- organizational structure

- governance and strategy policies

- banking infrastructure and cash management

- financial risk management

- treasury systems infrastructure

- treasury workflows and processes

Figure 3: Example of data collection checklist for review & assessment

Based on the review and assessment, existing short-falls can be identified as well as where the treasury organization wants to go in the future, both operationally and strategically.

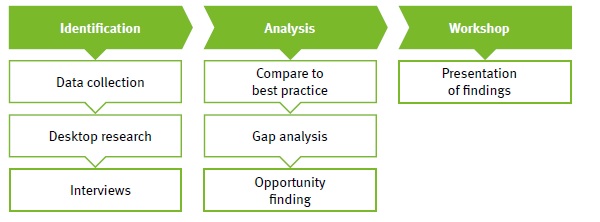

Figure 4 shows Zanders’ approach towards the review and assessment step.

Figure 4: Review & assessment break-down

Typical findings

Based on Zanders’ experience, common findings of a review and assessment are listed below:

Treasury organization & strategy:

- Disjointed sets of policies and procedures

- Organizational structure not sufficiently aligned with required segregation of duties

- Activities being done locally which could be centralized (e.g. into a FSSC), thereby realizing economies of scale

- Treasury resources spending the majority of their time on operational tasks that don’t add value and that could be automated. This prevents treasury from being able to focus sufficiently on strategic tasks, projects and fulfilling its internal consulting role towards the business.

Banking landscape:

- Mismatch between wallet share of core banking partners and credit commitment provided

- No overview of all bank accounts of the company nor of the balances on these bank accounts

- While cash management and control of bank accounts is often highly centralized, local balances can be significant due to missing cash concentration structures

- Lack of standardization of payment types and payment processes and different payment fi le formats per bank

System infrastructure:

- Considerable amount of time spent on manual bank statement reconciliation and manual entry of payments

- The current treasury systems landscape is characterized by extensive use of MS Excel, manual interventions, low level of STP and many different electronic banking systems

- Difficulty in reporting on treasury data due to a scattered system landscape

- Manual up and downloads instead of automated interfaces

- Corporate-to-bank communication (payments and bank statements processes) shows significant weaknesses and risks with regard to security and efficiency

Treasury workflows & processes:

- Monitoring and controls framework (especially of funds/payments) are relatively light

- Paper-based account opening processes

- Lack of standardization and simplification in processes

The outcome of the review & assessment step will be the input for step two: Solution Design.

Step 2: Solution Design

The key objective of this step is to establish the high-level design of the future state of treasury organization. During the solution design phase, Zanders will clearly outline the strategic and operational options available, and will make recommendations on how to achieve optimal efficiency, effectiveness and control, in the areas of treasury organization & strategy, banking landscape, system infrastructure and treasury workflows & processes.

Using the review & assessment report and findings as a starting point, Zanders highlights why certain findings exist and outlines how improvements can be implemented, based on best market practices. The forum for these discussions is a set of workshops. The first workshop focuses on “brainstorming” the various options, while the second workshop is aimed at decision-making on choosing and defining the most suitable and appropriate alternatives and choices.

The outcome of these workshops is the solution design document, a blueprint document which will be the basis for any functional and/or technical requirements document required at a later stage of the project when implementing, for example, a new banking landscape or treasury management system.

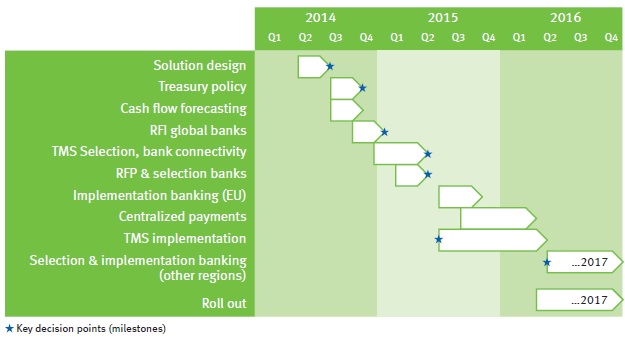

Step 3: Roadmap

The solution design will include several sub-projects, each with a different priority, some more material than others and all with their own risk profile. It is important therefore for the overall success of the transformation that all sub-projects are logically sequenced, incorporating all inter-relationships, and are managed as one coherent program.

The treasury roadmap organizes the solution design into these sub-projects and prioritizes each area appropriately. The roadmap portrays the timeframe, which is typically two to five years, to fully complete the transformation, estimating individually the duration to fully complete each component of the treasury transformation program.

“A Program is a group of related projects managed in a coordinated manner to obtain benefits and control not available from managing them individually”.

Zanders

Figure 5: Sample treasury roadmap

Step 4: Business Case

The next step in the treasury transformation program is to establish a business case.

Depending on the individual organization, some transformation programs will require only a very high-level business case, while others require multiple business cases; a high level business case for the entire program and subsequent more detailed business cases for each of the sub-projects.

Figure 6: Building a business case

The business case for a treasury transformation program will include the following three parts:

- The strategic context identifies the business needs, scope and desired outcomes, resulting from the previous steps

- The analysis and recommendation section forms the significant part of the business case and concerns itself with understanding all of the options available, aligning them with the business requirements, weighing the costs against the benefits and providing a complete risk assessment of the project

- The management and controlling section includes the planning and project governance, interdependencies and overall project management elements

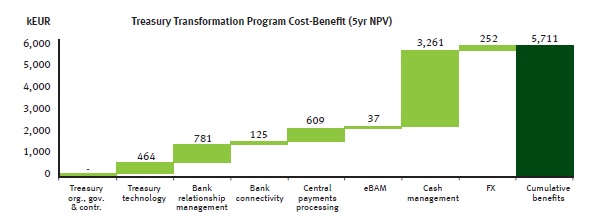

Notwithstanding the financial benefits, there are many common qualitative benefits in transforming the treasury. These intangibles are often more important to the CFO and group treasurer than the financial benefits. Tight control and full compliance are significant features of world-class treasuries and, to this end, they are typically top of the list of reasons for embarking on a treasury transformation program. As companies grow in size and complexity, efficiency is difficult to maintain. After a period of time there may need to be a total overhaul to streamline processes and decrease the level of manual effort throughout the treasury organization. One of the main costs in such multi-year, multi-discipline transformation programs is the change management required over extended periods.

Figure 7: Sample cost-benefit

Figure 7 shows an example of how several sub-projects might contribute to the overall net present value of a treasury transformation program, providing senior management with a tool to assess the priority and resource allocation requirements of each sub-project.

Step 5: Selection(s)

Based on Zanders’ experience gained during previous treasury transformation programs, key evaluation & selection decisions are commonly required for choosing:

- bank partners

- bank connectivity channels

- treasury systems

- organizational structure

Zanders has assisted treasury departments with selection processes for all these components and has developed standardized selection processes and tools.

Selection process for bank partners

Common objectives for including the selection of banking partners in a treasury transformation program include the following:

- to align banks that provide cash and risk management solutions with credit providing banks

- to reduce the number of banks and bank accounts

- to create new banking architecture and cash pooling structures

- to reduce direct and indirect bank charges

- to streamline cash management systems and connectivity

- to meet the service requirements of the business; and

- to provide a robust, scalable electronic platform for future growth/expansion.

Zanders’ approach to bank partner selection is shown in Figure 8 below.

Figure 8: Bank partner selection process

Selection process for bank connectivity providers or treasury systems (treasury management systems, in-house banks, payment factories)

The selection of new treasury technology or a bank connectivity provider will follow the selection process depicted in Figure 9.

Figure 9: Treasury technology selection process

Organizational structure

If change in the organizational structure is part of the solution design, the need for an evaluation and selection of the optimal organizational structure becomes relevant. An example of this would be selecting a location for a FSSC or selecting an outsourcing partner. Based on the high-level direction defined in the solution design and based on Zanders’ extensive experience, we can advise on the best organization structure to be selected, on a functional, strategic and geographical level.

Step 6: Execution

The sixth step of treasury transformation is execution. In this step, the future-state treasury design will be realized. The execution typically consists of various sub-projects either being run in parallel or sequentially.

Zanders’ implementation approach follows the following steps during execution of the various treasury transformation sub-projects. Since treasury transformation entails various types of projects, in the areas of treasury organization, system infrastructure, treasury processes and banking landscape, not all of these steps apply to all projects to the same extent.

For several aspects of a treasury transformation program, such as the implementation of a payment factory, a common and tested approach is to go live with a number of pilot countries or companies first before rolling out the solution across the globe.

Figure 10: Zanders’ execution approach

Step 7: Post-Execution

The post-execution step of a treasury transformation is an important part of the program and includes the following activities:

6-12 months after the execution step:

– project review and lessons learned

– post implementation review focussing on actual benefits realized compared to the initial business case

On an ongoing basis:

– periodic benchmark and continuous improvement review

– ongoing systems maintenance and support

– periodic upgrade of systems

– periodic training of treasury resources

– periodic bank relationship reviews

Zanders offers a wide range of services covering the post-execution step.

Importance of a structured approach

There are many internal and external factors that require treasury organizations to increase efficiency, effectiveness and control. In order to achieve these goals for each of the treasury activities of treasury management, risk management and corporate finance, it is important to take a holistic approach, covering the organizational structure and strategy, the banking landscape, the systems infrastructure and the treasury workflows and processes. Zanders’ seven steps to treasury transformation provides such an approach, by working from a detailed as-is analysis to the implementation of the new treasury organization.

Why Zanders?

Zanders is a completely independent treasury consultancy f rm founded in 1994 by Mr. Chris J. Zanders. Our objective is to create added value for our clients by using our expertise in the areas of treasury management, risk management and corporate finance. Zanders employs over 130 specialist treasury consultants who are the key drivers of our success. At Zanders, our advisory team consists of professionals with different areas of expertise and professional experience in various treasury and finance roles.

Due to our successful growth, Zanders is a leading consulting firm and market leader in independent consulting services in the area of treasury and risk management. Our clients are multinationals, financial institutions and international organizations, all with a global footprint.

Independent advice

Zanders is an independent firm and has no shareholder or ownership relationships with any third party, for example banks, accountancy firms or system vendors. However, we do have good working relationships with the major treasury and risk management system vendors. Due to our strong knowledge of the treasury workstations we have been awarded implementation partnerships by several treasury management system vendors. Next to these partnerships, Zanders is very proud to have been the first consultancy firm to be a certified SWIFTNet management consultant globally.

Thought leader in treasury and finance

Tomorrow’s developments in the areas of treasury and risk management should also have attention focused on them today. Therefore Zanders aims to remain a leading consultant and market leader in this field. We continuously publish articles on topics related to development in treasury strategy and organization, treasury systems and processes, risk management and corporate finance. Furthermore, we organize workshops and seminars for our clients and our consultants speak regularly at treasury conferences organized by the Association of Financial Professionals (AFP), EuroFinance Conferences, International Payments Summit, Economist Intelligence Unit, Association of Corporate Treasurers (UK) and other national treasury associations.

From ideas to implementation

Zanders is supporting its clients in developing ‘best in class’ ideas and solutions on treasury and risk management, but is also committed to implement these solutions. Zanders always strives to deliver, within budget and on time. Our reputation is based on our commitment to the quality of work and client satisfaction. Our goal is to ensure that clients get the optimum benefit of our collective experience.

IOM’s treasury transformation focused on streamlining bank relationships, implementing new systems, and establishing governance frameworks to better support its expanding migration management efforts.

The International Organization for Migration (IOM) is the principal intergovernmental agency in the field of migration. Due to increasing migratory flows over the past decade, which have escalated in recent months, the organization realized that its treasury needed a transformation in order to continue supporting the organization and its cause.

The IOM is committed to the principle that humane and orderly migration benefits both migrants and society. The organization was established in 1951, then known as the Provisional Intergovernmental Committee for the Movement of Migrants from Europe (PICMME), which helped people resettle in Western Europe following the chaos and displacement of the Second World War.

In subsequent years, the organization underwent a succession of name changes to the Intergovernmental Committee for European Migration (ICEM) in 1952, the Intergovernmental Committee for Migration (ICM) in 1980, and the International Organization for Migration (IOM) in 1989. These name changes reflect the organization’s transition from a logistics operation to a migration agency. The IOM’s members currently include 157 states and 10 observer states. It has offices in more than 150 countries and at any one time has more than 2,500 active projects ongoing.

It works to help ensure the orderly and humane management of migration, to promote international cooperation on migration issues, to assist in the search for practical solutions to migration problems, and to provide humanitarian assistance to migrants in need, including refugees, displaced persons, or other uprooted people. The organization works closely with several partners in four broad areas of migration management: migration and development, facilitating migration, regulating migration, and addressing forced migration. The IOM assists in meeting the growing operational challenges of migration management. It aims to advance the understanding of migration issues and encourages social and economic development through migration, while upholding the human dignity and well-being of migrants.

Differing paces

In 2008 and 2009, the organization went through a major transformation. “As recently as 10 years ago, the organization was still executing payments manually at its headquarters – payment by payment,” says Malcolm Grant, head of treasury at the IOM. With a new enterprise resource planning (ERP) system, the IOM took its first step towards improving its treasury. But more change was needed. While migration activities were growing – leading to increases in staff, projects, and donation allocation – treasury didn’t grow at the same pace as the rest of the organization. On top of that, in the years thereafter, the financial crisis resulted in a sharp increase of compliance requirements. “Due to all these developments, our treasury was way behind where it should have been.

The impact of the organization’s growth in an outdated system environment was that people looked for solutions by firefighting; they built up several different systems and various ways of working. For example, new bank accounts were added, instead of using existing bank accounts and relationships. We found ourselves with more than 700 accounts and over 150 bank relationships. We needed to bring treasury back to the heart of the organization – a huge challenge, because we needed more people, more up-to-date technology and improved governance.”

Due to the tight funding in the years following 2009, it was a slow process, says Grant: “From a treasury point of view, we look like a corporate; we get money in, we pay it out and invest it. A corporate has a profit motive, a different set of values and different stakeholders. So there are cultural differences and due to political issues some things don’t happen as quickly.”

A treasury blueprint for the future

Eventually, the organization’s management was persuaded to review its treasury. Grant explains: “So in 2012, we initiated the ‘treasury review’ project. We wanted a comprehensive wide-reaching review that tackled just about all key areas of treasury. Therefore, we asked some consultant firms for treasury advice and after some meetings we hired Zanders to reinforce and challenge our assumptions. And it turned out to be a great step; they added deep knowledge of treasury, markets, and best practices, and together we built a very strong business case showing what needed to be done in our strategic planning to overhaul our treasury.”