In a fast-paced gaming and esports market, optimizing cash management was critical to empowering Savvy Games with the financial clarity and agility to surge forward with its ambitious investment strategy.

The games market just keeps getting bigger. And with limits on this growth seemingly uncharted, interest from governments and private sector investors is at an all-time high. Savvy Games Group is a global gaming and esports business, wholly owned by Saudi Arabia’s Public Investment Fund (PIF). Tasked with transforming the Kingdom of Saudi Arabia (KSA) into a global games hub, the Riyadh-based group is pursuing an ambitious investment strategy aimed to rapidly accelerate growth of the sector and maximize the opportunities the Kingdom offers.

Acquisition-driven growth

Savvy is clear in its intention to be the leading force in global games investment. At first glance, this could appear a bold claim for a three-year-old company operating in one of the world’s most buoyant and exciting markets. But it’s a challenge Savvy has already proven it’s well-equipped to deliver. Despite being a relative newcomer to the games sector, through high-profile acquisitions—including Scopely in the US and EFG Group in Europe and the US—Savvy has quickly established itself as an active investor. This has led to fast growth for the business. In just a few years, the Group has expanded to become a global enterprise of more than 3,500 employees across 69 locations in 22 countries.

While the scale and speed of Savvy’s development successfully solidified its reputation and investor profile, it also created a disparate banking and cash management structure. With the Group’s cashflows spanning a global network of more than 40 banks and 400 bank accounts, cash management was cumbersome and inefficient.

A rapid bank rationalization

With centralization as the clear goal, the starting point was to consolidate Savvy’s banking services and implement an inhouse bank in order to harmonize disparate cash management processes. To enable this, in June 2024, Savvy issued a request for proposal (RfP) for the provision of banking services to the Savvy Group.

“After a competitive RfP, we chose Citibank for our global cash management and HSBC for our cash management in the US and in Saudi Arabia,” Saleh Alfadhel, Savvy’s Group CFO, recounts. “We then had to go from 40 banks and 400 bank accounts to two banks and 50 bank accounts in one year.” This was a complex project, involving the establishment of three cash pools—a multi-currency notional pool in London, a US dollar and Saudi Arabian Riyal (SAR) pool in KSA, and a virtual US Dollar pool in the US. But this was only one part of establishing the Group’s treasury function. While bank rationalization and cash pooling created the foundations for a more streamlined and centralized treasury organization, to extract maximum value from this new structure, they also needed full visibility of the group’s cash balances and positions worldwide. This is where a second RfP came in—the selection and implementation of a global treasury management system (TMS).

From selection to solution

Driving Savvy’s treasury technology project was the target to have a new, global TMS for the Group in place by December 2024.

By leveraging Zanders’ technical expertise of Kyriba and deep treasury experience, we successfully developed and implemented best-in-class processes across cash management, payment processing, and in-house banking. Harnessing Kyriba’s functionality, we streamlined and automated our treasury operations for greater efficiency and control.

Dheeraj Parmar (Assistant Treasurer at Savvy Games Group)

With Zanders leading the technical conversations with the vendors, Savvy was able to explore and compare the different solutions on offer in a highly structured, relevant, and informed way. This ensured the selection of a TMS that was the best-fit to deliver high levels of transparency and central control of cash management. The outcome was the selection of Kyriba and the appointment of Zanders to advise on the implementation of the first five modules. The deadline set for completing this was December 2024.

“Between June and December, Zanders implemented five modules of Kyriba,” Saleh says. “In six months, we had a full implementation of Kyriba across our operating companies, the headquarters in KSA, and the three inhouse banks.”

Between June and December 2024, Zanders implemented five modules of Kyriba. In six months, we had a full implementation of Kyriba across our operating companies, the headquarters in KSA, and the three inhouse banks.

Saleh Alfadhel (CFO at Savvy Games Group)

With clarity comes cash control

Savvy’s Kyriba journey may still be in its early stages but the value of the visibility it gives them over their cash position globally is already evident. “As of December 2024, we have a liquidity pool set up, and we have a dashboard in Kyriba showing us 100% of our in-scope balances,” Saleh says. “We estimate that by having full visibility and cash concentration, we can operate the Savvy Games Group with circa 45% less cash globally.”

And there is still more value-driving performance for Savvy to unlock from operating a centralized, digital treasury. Kyriba cloud-based treasury management solutions offer a powerful way for businesses to connect banks, ERPs, apps, and portals. This unifies data, providing not only the clarity and insight to improve liquidity, but also the opportunity to automate processes and improve efficiency. Unlocking this enhanced performance is where Zanders’ work with the group turns to next. “Once we add host-to-host, straight through processing and a shared service center to Kyriba, we should have full automation between our ERPs—SAP in Germany and Oracle in KSA and the US,” Saleh says. “With this, we will be able to automate accounts payable and the treasury department completely.”

Continuing our transformation journey in collaboration with Zanders will allow us to further optimize our treasury operating model while ensuring scalability to support the company’s growth—both organically and through strategic M&A actions.

Dheeraj Parmar (Assistant Treasurer at Savvy Games Group)

To find out more about our treasury transformation services and the benefits we can offer your business, please contact our Partner Mark van Ommen.

Is the grass always greener on the other side? Observing a tendency to change from “best of breed treasury management systems” to best “integrated treasury management systems” and vice versa.

In large organizations, the tendency is to select large scale ERP systems to support as much of the organization's business processes within this system. This is a goal that is driven typically by the IT department as this approach reduces the number of different technologies and minimizes the integration between systems. Such a streamlined and simplified system architecture looks to mitigate risk by reducing the potential points of failure and total cost of ownership.

Over the years the treasury department has at times chosen to rather deploy “best of breed” treasury management systems and integrate this separate system to the ERP system. The treasury business processes and therefore systems also come with some significant integration points in terms of trading platforms, market data and bank integration for tasks such as trade confirmations, payments, bank statements and payment monitoring messaging.

The IT department may view this integration complexity as an opportunity for simplification if the ERP systems are able to provide acceptable treasury and risk management functionalities. Especially if some of the integrations that the treasury requires does overlap with the needs of the rest of the business – i.e. payments, bank statements and market data.

Meanwhile, the treasury department will want to ensure that they have as much straight through processing and automation as possible with robust integration. Since their high value transactions are time sensitive, a breakdown in processing would result in negative transactional cost implications with their bank counterparts.

Deciphering Treasury System Selection: Below the Surface

The decision-making process for selecting a system for treasury operations is complex and involves various factors. Some are very much driven by unique financial business risks, leading to a functional based decision process. However, there are often underlying organizational challenges that play a far more significant role in this process than you would expect. Some challenges stem from behavioral dimensions like the desire for autonomy and control from the treasury. While others are based on an age-old perception that the “grass is greener on the other side” – meaning the current system frustrations result in a preference to move away from current systems.

An added and lesser appreciated perspective is that most organizations tend to mainly focus on technical upgrades but not often functional upgrades on systems that are implemented. Meaning that existing systems tend to resemble the version of the system based on when the original implementation took place. This will also lead to a comparison of the current (older version) system against the competing offerings latest and greatest.

Another key observation is that with implementing integrated TMS solutions like the SAP TRM solution in the context of the same ERP environment, the requirements can become more extensive as the possibilities for automating more with all source information increase. Consider for example the FX hedging processes where the source exposure information is readily available and potential to access and rebalance hedge positions becomes more dynamic.

Closing thoughts

There is no single right answer to this question for all cases. However, it is important to ensure that the process you follow in making this decision is sound, informed and fair. Involving an external specialist with experience in navigating such decisions and exposure to various offerings is invaluable.

To support these activities, Zanders has also built solutions to make the process as easy as it can possibly be, including a cloud-based system selection tool.

Moreover for longer term satisfaction, enabling the evolution of the current treasury system (be it best of breed or integrated) is essential. The system should evolve with time and not remain locked into its origin based on the original implementation. Here engaging with a specialist partner with the right expertise to support the treasury and IT organizations is key. This can improve the experience of the system and this increased satisfaction can ensure decision making is not driven or led by negativity.

In support of this area Zanders has a dedicated service called TTS which can come alongside your existing IT support organization and inject the necessary skill and insight to enable incremental improvements alongside improved resolution timeframes for day-to-day systems issues.

For more information about out Treasury Technology Service, reach out to Warren Epstein.

Revolutionizing Bolt’s Treasury: Efficiency, Reliability, and Growth

Mid 2023, Bolt successfully implemented its new full-fledged treasury management system (TMS). With assistance of Zanders consultants, the mobility company implemented Kyriba – a necessity to support Bolt’s small treasury team. As a result, all daily processes are almost completely automated. “It's about reliability.”

Bolt is the leading European mobility platform that’s focused on more efficient, convenient and sustainable solutions for urban travelling. With more than 150 million customers in at least 45 countries, it offers a range of mobility services including ride-hailing, shared cars and scooters, food and grocery delivery. “Bolt was founded by Markus Villig, a young Estonian guy who quit his school to start this business with €5,000 that he borrowed from his parents,” says Mahmoud Iskandarani, Group Treasurer at Bolt. “He built an app and started to ask drivers on the street to download it and try it out. Now we have millions of drivers and passengers, almost 4,000 employees and several business lines. Last August, we celebrated our 10th anniversary. So, we have one of the fastest growing businesses in Europe. And our ambition is to grow even faster than so far.”

Driven by technology

Because of its fast growth, Bolt’s Treasury team decided to look for a scalable solution to cope with the further expansion of the business. Freek van den Engel, Treasury manager at Bolt: “We needed a system that could automate most of our daily processes and add value. Doing things manually is not efficient and risks are high. To help us scale up while maintaining efficiency, we needed our Treasury to be driven by technology.”

Iskandarani adds: “Meanwhile, our macro environment is changing and we had some bank events. In the past years, startups or scale-ups have seen big growth and didn't focus too much on working capital management. Interest rates were low, which made it easy to raise money from investors. Now, we need to make sure that we manage our working capital the right way so that we can access our money, mitigate risks, and that we get a decent return on our cash. That’s when it's controlled by Treasury and invested correctly.”

Choosing Kyriba

Van den Engel led a treasury system selection process three years ago for his previous employer, where he also worked together with Iskandarani. “That experience helped us to come up with a shortlist of three providers, instead of having a very long RfP process looking at a long list of vendors. We started the selection process in June 2022 and two months later we chose Kyriba because of its strong functionality. Also, it’s a solution offered as SaaS, which means we don't have to worry about upgrades – a very important reason for us. Kyriba has been working with tech companies similar to ours. Another decisive factor was their format library, called Open Format Studio. It allows us to use self-service when it comes to configuring payment formats, reducing our costs and turn-around time when expanding to new geographies.”

Implementation partner

For Bolt, Kyriba will function as in-house bank system, and support its European cash pool. During the selection process, the team had some reference calls with other Kyriba users to discuss experiences with the system and the implementation. “One piece of feedback we received was that it works very well to bring in implementation partners to complete such a project successfully. Zanders stood out, because of its proven track record and the awards it had won. Also, Mahmoud and I both had experience with Zanders during some projects at our previous employer. That’s why we asked them to be our implementation partner.”

In October 2022, the implementation process started. In July 2023, the system went live. Kyriba’s TMS solution covered all treasury core processes, including cash position reporting (including intra-day balance information), liquidity management, funding, foreign exchange with automatic integration to 360T and Finastra, investments, payment settlements and risk management.

Trained towards independency

As part of the implementation process, Zanders trained Bolt on how to use the new tool, and assisted in using the Open Format Studio. In this way, the team built the knowledge and experience needed to roll out to new countries more independently.

Van den Engel: “We aimed to be independent and do as much as possible ourselves to reduce costs and build up in-house expertise on the system. Zanders helped us figuring out what we wanted, explained and guided us, and showed what the system can do and how to align that with our needs in the best possible way. Once we were clear on the blueprint, they helped us with our static data, connectivity and initial system set-up. After the training they led, we were able to do most of it ourselves, including the actual system configuration work, for which Zanders had laid the foundation.”

Rolling out the payment hub

With assistance of Zanders consultants, Bolt also set up a framework to roll out the payment hub, for the vendor payments from its ERP system called Workday and its payroll provider, Immedis. The consultants assisted with configuration of initial payment scenarios and workflows. “We made the connections, tested them and did a pilot with Workday last summer. After training and with the experience that we've built up using Open Format Studio, we can roll out to new countries and expand it ourselves. Starting in August, we continued to roll out Kyriba’s payment hub to more countries, and to implement Payroll. With the payment hub we are now live in 16 countries and that's basically fully self-serviced. Apart from some support for specialized cases, we don’t need support anymore for the payment hub.”

Many material benefits

Having a small hands-on project team meant no need for a complex project management organization to be set-up. Naturally Bolt and Zanders started using agile project management, with refocus of priorities to different streams as necessary. The Kyriba implementation project was closed within the set budget in 9 months’ time.

Iskandarani is happy with the results. “It is clear there are benefits of this implementation when it comes to efficiency and risk management. We now have the visibility over our cash and the fact that we have a system telling us that there’s an exposure that we should get rid of, that has a lot of value. Also, we have some financial benefits that we could not have achieved without the system. Today we can pool our cash better, we can invest it better, and we can handle our foreign exchange in a better way. Before this, we have overpaid banks.”

Reliability and control

“We could have hired more people”, Van den Engel adds. “But some things are just very difficult to do without this system. It's also about reliability. Even if you have a manual process in place that works, you will see it breaking down from time to time. If someone deletes a formula, or a macro stops working, that becomes very risky. It’s also about the control environment. As a company we're looking to become more mature and implement controls that should be there – that too is very difficult to do without a proper system that can generate these reports, be properly secured with all the right standards that we need to adhere to, or do fraud detection based on machine learning in the future. It's impossible to do all that manually. Those are material benefits, but hard to quantify.”

After taking a long hard look at its treasury function, Accell Group took the plunge by investing in a treasury management system (TMS) and improving bank connectivity with a payment hub solution.

So how exactly did the European market leader in bicycles achieve these goals? Accell Group is the European market leader in the mid- and upper-segments for high-quality bicycles and associated parts and accessories (XLC). Employing over 3,000 people across 18 countries, Accell Group manages a strong portfolio of national and international (sports) brands, each with its own distinctive positioning.

In 2018 the company sold 1.1 million bicycles, realizing a turnover of €1.1 billion and a net profit of €20.3 million. The bicycle brands in the Accell Group stable include Haibike, Winora, Ghost, Lapierre, Babboe, Batavus, Sparta, Koga, Diamondback and Raleigh. They are manufactured in several locations in the Netherlands, Hungary, Turkey and China.

Bicycles, and particularly e-bikes, are increasingly being seen as a key contributor in addressing issues such as urban congestion, hazardous city traffic, rising CO₂ emissions and our desire to live healthier lifestyles. For this reason, the bicycle market represents excellent potential for further worldwide growth.

“Given that we focus on new, clean and safe mobility solutions, we are certainly in the right business in terms of market potential,” agrees Jonas Fehlhaber, Treasurer at Accell Group, “Furthermore, there is a growing trend for large cities to adapt their infrastructures to offer cyclists more space and make them safer.”

Given that we focus on new, clean and safe mobility solutions, we are certainly in the right business in terms of market potential.

Jonas Fehlhaber, Treasurer at Accell Group

Omnichannel approach

Initially, Accell Group was a small holding company with decentralized management. Fehlhaber joined the Group in 2013 as its first treasurer, but his responsibilities soon expanded to encompass cash management, currency risk management and credit insurance. At the same time, the structure of the company changed. Based on a new strategy defined in 2016, the most important change was that the company wanted to shift from a manufacturing-driven approach to a consumer-centric one. In other words, everything must revolve around the consumer.

“In the past our sales channel was mainly defined by the dealers but now, thanks to experience centers and the use of e-commerce, this is changing into an omnichannel approach,” says Fehlhaber. “The dealers still play the most important role, but with more and more functions being provided centrally, the size of the holding has grown substantially. For the past two-and-a-half years we have had a strong supply chain organization, and our finance team, just like the Treasury, has expanded.”

Challenge

Treasury roadmap

After centralizing several components and rationalizing the bank portfolio, Accell asked Zanders to carry out a quick scan of the Treasury department. In the context of this scan, the treasury function was examined and several potential risks and possible improvement areas were identified.

“To further professionalize the Treasury, we worked with Zanders to start a project in 2017 to establish a treasury roadmap,” adds Fehlhaber. “In this project our strategic goals, along with what we wanted to achieve with them, were laid out. All in all it was an intensive undertaking in which all the respective processes were documented.”

The outcome was reconciled into three pillars: organization, systems and treasury policy. To limit the organizational vulnerability of what would otherwise have been a single-person department, Accell used Zanders’ Treasury Continuity Service (TCS) and appointed an additional treasury employee. An element of the Treasury Continuity Service is a TMS, Integrity, with which processes can be automated and standardized, while risks are simultaneously minimized.

“The Treasury Continuity Service allowed us to implement the system quickly, without the need to go through an RfP [Request for Proposal] process,” says Fehlhaber. “Zanders had already made advance agreements with the supplier, FIS, giving us a partially pre-configured system that could be quickly implemented. Moreover, the support days that we are allocated can be used for advice, for example, or if there is temporary understaffing. We acted on the advice to start up our new payment hub, from the RfP to the actual selection and, if necessary, the implementation too.”

The final improvement was to set up a comprehensive treasury policy, which has injected more structure and transparency into the daily treasury activities.

Solution

More Complete and more interactive

The new TMS and the extra support have meant that Accell’s treasury department is now less vulnerable. “While Excel allows you to work flexibly, sharing information is more difficult because it is much more personal,” continues Fehlhaber. “The owner of the Excel file will be aware of all the details, but issues can quickly arise during transfer. A complicating factor is that there is no audit trail in Excel, making it generally more risky to work with. A TMS, on the other hand, is more complete and interactive, and the transfer is much easier. It has more functionalities and provides daily bank updates, so you always have a good overview of your latest cash positions. What’s more, it records all transactions, such as FX instruments and bank- and inter-company loans, with settlements being done from within Integrity. Above all, though, the TMS offers the option of creating bespoke reports, which in itself saves a lot of time.”

Payments via TIS

A key requirement of Accell was for the payment landscape to be organized more efficiently and controlled more centrally. What we tend to see is that corporates have masses of bank cards, for everyone involved in the authorization of payments. Not only is this very inefficient, it also makes it difficult to effectively manage these processes centrally. This is why Accell decided to implement a payment hub solution [TIS; Treasury Intelligence Solutions]. The payment hub serves as an interface, to replace the banking applications. A further advantage is that TIS offers the option of single sign-on, greatly improving the on-and off-boarding process for users.

Rolling out a TIS project takes between 18 and 24 months. It is a separate system to FIS Integrity, but they are connected in terms of infrastructure. “Bank statements arrive through the payment hub and then interface software distributes them to the systems that need the information, such as the ERP system and Integrity,” explains Fehlhaber. “Furthermore, all systems are fed current market data from our terminal, while payment files, for example, are sent from Integrity via TIS to the bank.”

The once-humble bicycle has evolved into a true lifestyle product.

Tjitze Auke Rijpkema, Treasury Team

Performance

The road to the future

The increasing need to reduce exhaust emissions in major urban areas is fuelling further growth potential for the bicycle market. “The market is still growing,” agrees Fehlhaber, “especially when it comes to e-bikes. We are focusing on the mid- and upper-market segments and doing particularly well with the so-called e-performance bikes, the power-assisted mountain bikes catered for by brands such as Haibike, Ghost and Lapierre.”

In 2018, Accell acquired Velosophy, a fast-growing innovative player in e-cargo biking solutions that serves both consumer and business markets. The Velosophy stable includes Babboe, the market leader in Europe for family cargo bikes, CarQon, the new premium cargo bike brand, and Centaur Cargo. The latter of these three is a specialist in B2B cargo bikes for the so-called ‘last-mile deliveries‘. These are typically to locations that are either impossible or very difficult to reach by car, such as city centers, for example. The acquisition of Velosophy has enabled Accell Group to accelerate its innovation strategy, which is focused, among other things, on the development of urban mobility solutions.

Bicycles are becoming increasingly bespoke products, reveals Fehlhaber. Mobility as a service (offering a service concept rather than just a bicycle), lease options or special, self-selected elements are all maintaining the current momentum in the bicycle market.

“The once-humble bicycle has evolved into a true lifestyle product,” insists Tjitze Auke Rijpkema, who joined the treasury team in 2018. “Smart internet technology and handy connectivity apps are further enriching the cycling experience and making bicycles better and safer in all kinds of ways. Just like treasury, the bicycle is constantly moving with the times.”

We are excited to announce that Zanders has been listed on the Swift Customer Security Programme (CSP) Assessment Providers directory*.

The CSP helps reinforce the controls protecting participants from cyberattack and ensures their effectivity and that they adhere to the current Swift security requirements.

*Swift does not certify, warrant, endorse or recommend any service provider listed in its directory and Swift customers are not required to use providers listed in the directory.

Swift Customer Security Programme

A new attestation must be submitted at least once a year between July and December, and also any time a change in architecture or compliance status occurs. Customer attestation and independent assessment of the CSCF v2023 version is now open and valid until 31 December 2023. July 2023 also marks the release of Swifts CSCF v2024 for early consultation, which is valid until 31 December 2024.

Swift introduced the Customer Security Programme to promote cybersecurity amongst its customers with the core component of the CSP being the Customer Security Controls Framework (CSCF). Independent assessment has been introduced as a prerequisite for attestation to enhance the integrity, consistency, and accuracy of attestations. Each year, Swift releases an updated version of the CSCF that needs to be attested to with support of an independent assessment.

The Attestation is a declaration of compliance with the Swift Customer Security Controls Policy and is submitted via the Swift KYC-SA tool. Dependent on the Swift Architecture used, the number of controls to be implemented vary; of which certain are mandatory, and others advisory.

Further details on the Swift CSCF can be found on their website:

- https://www.swift.com/myswift/customer-security-programme-csp

- https://www.swift.com/myswift/customer-security-programme-csp/find-external-support/directory-csp-assessment-providers

Our services

Do you have arrangements in place to complete the independent assessment required to support the attestation?

Zanders has experience with and can support the completion of an independent external assessment of your compliance to the Swift Customer Security Control Framework that can then be used to fully complete and sign-off the Swift attestation for this year.

With an extensive track record of designing and deploying bank integrations, our intricate knowledge of treasury systems across both IT architecture as well as business processes positions us well to be a trusted independent assessor. We draw on past projects and assessments to ask the right questions during the assessment phase, aligning our customers with the framework provided by Swift.

The Swift attestation can also form part of a wider initiative to further optimise your banking landscape, whether that be increasing the use of Swift within your organisation, bank rationalization or improving your existing processes. The availability of your published attestation and its possible consultation with counterparties (upon request) helps equally in performing day-to-day risk management.

Approach

Planning

We start with rigorous planning of the assessment project, developing a scope of work and planning resources accordingly. Our team of experts will work with clients to formulate an Impact Assessment based on the most recent version of the Swift Customer Security Controls Framework.

Architecture Classification

A key part of our support will be working with the client to formulate a comprehensive overview of the system architecture and identify the applicable controls dictated by the CSCF.

Perform Assessment

Using our wide-ranging experience, we will test the individual controls against specific scenarios designed to root out any weaknesses and document evidence of their compliance or where they can be improved.

Independent Assessment Report

Based on the evidence collected, we will prepare an Independent Assessment report which includes status of the compliance against individual controls, baselining them against the CSCF and recommendations for improvement areas within the system architecture.

Post Assessment Activities

Once completed, the Independent Assessment report will support you with the submission of the Attestation in line with the requirements of the CSCF version in force, which is required annually by Swift. In tandem, Zanders can deliver a plan for implementation of the recommendations within the report to ensure compliance with current and future years’ attestations. Swift expects controls compliance annually, together with the submission of the attestation by 31 December at the latest, in order to avoid being reported to your supervisor. Non-compliant status is visible to your counterparties.

Do you need support with your Swift CSP Independent Assessment?

We are thrilled to offer a Swift CSP Independent Assessment service and look forward to supporting our clients with their attestations, continuing their commitment to protecting the integrity of the Swift network, and in doing so supporting their businesses too. If you are interested in learning more about our services, please contact us directly below.

Get performance now

- Contact me

You are currently viewing a placeholder content from HubSpot. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information

The SWIFT MT-MX migration is now underway, with a primary focus on a select number of MT messages within the interbank messaging space.

However, possibly the most important point for corporates to be aware of is the planned move towards explicit use of the structured address block. In this second article in the ISO 20022 series, Zanders experts Eliane Eysackers and Mark Sutton provide some valuable insights around this industry requirement, the challenges that exists and an important update on this core topic.

What is actually happening with the address information?

One of the key drivers around the MT-MX migration are the significant benefits that can be achieved through the use of structured data. E.g., stronger compliance validation and support STP processing. The SWIFT PMPG1 (Payment Market Practice Group) had advised that a number of market infrastructures2 are planning to mandate the full structured address with the SWIFT ISO migration. The SWIFT PMPG had also planned to make the full structured address mandatory for the interbank messages – so effectively all cross-border payments. The most important point to note is that the SWIFT PMPG had also advised of the plan to reject non-compliant cross border payment messages from November 2025 in line with the end of the MT-MX migration. So, if a cross border payment did not include a full structured address, the payment instruction would be rejected.

What are the current challenges around supporting a full structured address?

Whilst the benefits of structured data are broadly recognised and accepted within the industry, a one size approach does not always work, and detailed analysis conducted by the Zanders team revealed mandating a full structured address would create significant friction and may ultimately be unworkable.

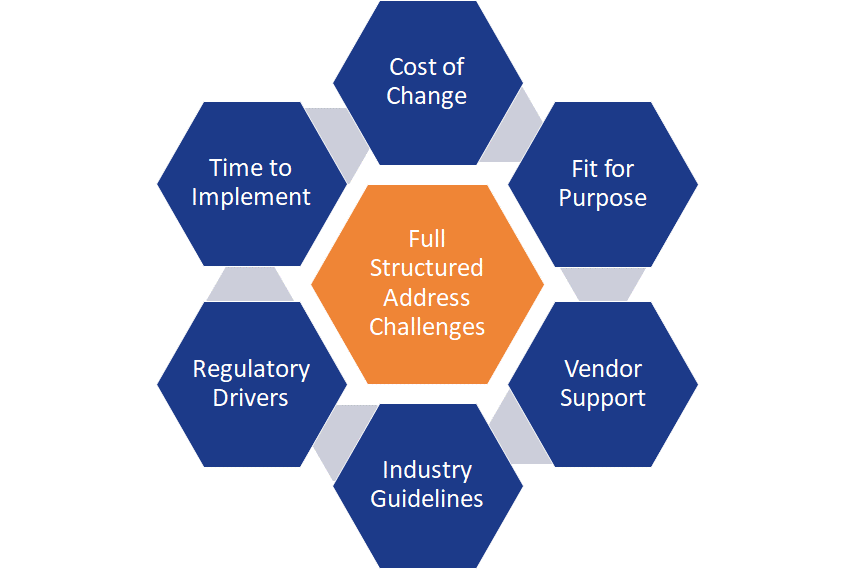

Diagram 1: Challenges around the implementation of the full structured address.

From the detailed analysis performed by the Zanders team, we have identified multiple problems that are all interconnected, and need to be addressed if the industry is to achieve its stated objective of a full structured address. These challenges are summarized below:

- Cost of change: The 2021 online TMI poll highlighted that 70% of respondents confirmed they currently merge the building name, building number, and street name in the same address line field. The key point to note is that the data is not currently separated within the ERP (Enterprise Resource Planning) system. Furthermore, 52% of these respondents highlighted a high impact to change this data, while 26% highlighted a medium impact. As part of Zanders’ continued research, we spoke to two major corporates to gain a better sense of their concerns. Both provided a high-level estimate of the development effort required for them to adapt to the new standard: ½ million euros.

- Fit for Purpose: From the ISO 20022 expert group discussions, it was recognized that the current XML Version 9 message would need a significant re-design to support the level of complexity that exists around the address structure globally.

- Vendor Support: Whilst we have not researched every ERP and TMS (Treasury Management System) system, if you compare the current structured address points including field length in the XML Version 9 message with the master data records currently available in the ERP and TMS systems, you will see gaps in terms of the fields that are supported and the actual field length. This means ERP and TMS software vendors will need to update the current address logic to fully align with the ISO standard for payments – but this software development cannot logically start until the ISO address block has been updated to avoid the need for multiple software upgrades.

- Industry Guidelines: Whilst industry level implementation guidelines are always a positive step, the current published SWIFT PMPG guidelines have primarily focused on the simpler mainstream address structures for which the current address structure is fine. By correctly including the more complex local country address options, it will quickly highlight the gaps that exist, which mean compliance by the November 2025 deadline looks unrealistic at this stage.

- Regulatory Drivers: At this stage, there is still no evidence that any of the in-country payments regulators have actually requested a full structured address. However, we have seen some countries start to request minimum address information (but not structured due to the MT file format), such as Canada and US.

- Time to Implement: We must consider the above dependencies that need to be addressed first before full compliance can logically be considered, which means a new message version would be required. Whilst industry discussions are ongoing, the next ISO maintenance release is November 2023, which will result in XML version 13 being published. If we factor in time for banks to adopt this new version (XML Version 13), time for software vendors to develop the new full structured address including field length and finally, for the corporates to then implement this latest software upgrade and test with their banking partners, the November 2025 timeline looks unrealistic at this point in time.

A very important update

Following a series of focused discussions around the potential address block changes to the XML Version 9 message, including the feedback from the GLEIF3 the ISO payment expert group questioned the need to support a significant redesign of the address block to enable the full structured address to be mandated. The Wolfsberg Group4 also raised concerns about scale of the changes required within the interbank messaging space.

Given this feedback, the SWIFT PMPG completed a survey with the corporate community in April. The survey feedback highlighted a number of the above concerns, and a change request has now been raised with the SWIFT standards working group for discussion at the end of June. The expectation is that the mandatory structured address elements will now be limited to just the Town/City, Postcode, and country, with typical address line 1 complexity continuing to be supported in the unstructured address element. This means a blended address structure will be supported.

Is Corporate Treasury Impacted by this structured address compliance requirement?

There are a number of aspects that need to be considered in answering this question. But at a high level, if you are currently maintaining your address data in a structured format within the ERP/TMS and you are currently providing the core structured address elements to your banking partners, then the impact should be low. However, Zanders recommends each corporate complete a more detailed review of the current address logic as soon as possible, given the current anticipated November 2025 compliance deadline.

In Summary

The ISO 20022 XML financial messages offer significant benefits to the corporate treasury community in terms more structured and richer data combined with a more globally standardised design. The timing is now right to commence the initial analysis so a more informed decision can be made around the key questions.

Notes:

- The PMPG (payment market practice group) is a SWIFT advisory group that reports into the Banking Services Committee (BSC) for all topics related to SWIFT.

- A Market Infrastructure is a system that provides services to the financial industry for trading, clearing and settlement, matching of financial transactions, and depository functions. For example, in-country real-time gross settlement (RTGS) operators (FED, ECB, BoE).

- Global Legal Entity Identifier Foundation (Established by the Financial Stability Board in June 2014, the GLEIF is tasked to support the implementation and use of the Legal Entity Identifier (LEI).

- https://www.wolfsberg-principles.com/sites/default/files/wb/pdfs/wolfsberg-standards/1.%20Wolfsberg-Payment-Transparency-Standards-October-2017.pdf

Remote partnered with Zanders to simplify bank onboarding, enabling seamless global operations and innovative remote work solutions.

Remote offers global employment services for internationally distributed workforce. It takes care of payroll, benefits, compliance, taxes, equity incentives and more, so that companies can employ someone internationally as easily as they do at home. The company’s vision is to make it simple to manage, employ, and pay anyone, anywhere. Founded in 2019, Remote is growing quickly and expanding into different markets. In 2022, Zanders supported the company to accelerate the onboarding of new banks. Ana de Sousa, Director and Global Head of Treasury at Remote, explains the collaboration in this Q&A.

"We tackle some of the biggest challenges involved in building distributed teams, which are the risk, cost, and complexity of employing international employees and contractors,” De Sousa clarifies. “Our customers include GitLab, DoorDash, Loom, Paystack, and thousands of other companies around the world.”

You have been Director Global Treasurer at Remote for a year now. What attracted you to join the company?

“At Remote we often say that ‘talent is everywhere, but opportunities aren’t.’ I grew up in a very small village in Portugal so I personally identify with this. I saw that Remote is changing the world and I wanted to be part of this change. Beyond the mission, it’s also exciting to be part of a company that is applying technology and automation to bring efficiency to an area as complex as global employment. I am also very aligned with Remote’s values. The value of kindness is very special for me, as I believe that we can always make extraordinary things when we are kind.”

How would you describe the company’s corporate culture?

“Because Remote is a fully distributed virtual company with no offices, most roles are country-agnostic and our employees can work from their chosen locations around the world. That means we have Remoters from 75+ different nationalities, coming from all different cultures, backgrounds and experiences. This contributes to a diverse work environment where everyone is encouraged to share their culture and interests with everyone.”

What would you say drives the need for remote work/remote hiring and remote services in general?

“Over the past few years, many companies turned to remote work as a solution to a problem. What they are discovering now is that it can provide significant business advantages as well. Remote work enables you to build a team without being constrained by geography, meaning companies can tap into wider pools of talent while also supporting greater flexibility and work-life balance.”

What is your experience within different regions/markets?

“Remote has a global presence with around 80 legal entities on six continents. I started my career overseeing cash management for the EMEA region. Later, I moved to a new job with a global scope. Here at Remote, every single member of the Treasury team has global coverage. This means we can leverage asynchronous and flexible work for the entire team to be effective.”

You are working completely remotely, without having a physical company office. What has been your experience with this setup and do you miss meeting your colleagues in person?

“I do miss team birthday parties with cake sometimes. I advocate freedom of choice, based on whatever is best for you. Working from an office is still offered by plenty of companies. For me, remote work has allowed me to keep my career in an international environment while prioritizing family and flexibility. It’s certainly still possible to meet up with colleagues without a company office. I recently met one of my team members in person for the first time, and it was just like catching up with a friend.”

In terms of managing family/work time, are there days where you would prefer to work in a physical company office?

“No, I manage my time according to my priorities. If my kids need me, I will be available for them. If my work is my priority, that is my focus. It is not a physical place that defines my commitment or my capacity of producing results. It is important to have the right structure that supports your professional career independently of the place.”

What are the communication tools you use internally and externally?

“We use tools like Slack, Notion, Loom, and Asana for communication and documentation. Beyond the tools, Remoters are trained in asynchronous communication, documentation, inclusive language, meeting best practices, and even to use the UTC time zone companywide. These are all essential for a team that is as distributed as ours.”

What would you say are treasury-specific challenges when working remotely?

“The biggest challenges of remote work arise when we try to take the old office-centric methods of doing things and expect them to work just as well in a remote setting. Remote work does require some different considerations. Treasury teams in particular need to be rigorous about documentation and practicing ‘overcommunication’ given the critical nature of our work.”

What is the company’s approach for creating an integrated team and what is your personal approach to build a team spirit while working completely remotely?

“As a fully remote company, Remote works hard to build belonging and a sense of community throughout the company. There are numerous opportunities for social connection, including bonding times, games, and even virtual reality time. We have more than 1,700 Slack channels including channels for music, TV, pets, food, sports and much more. At the same time, our culture is asynchronous, so people can participate on their own time and all scheduled events rotate across time zones.”

Expanding into new markets is part of Remote’s core strategy. What role does Treasury play to enable new country operations?

“At Remote, Treasury is part of the backbone of our operations and an enabler of international growth. In the majority of cases, without a bank account, we cannot launch in a country. In addition, domestic bank accounts are also critical to offer better experience to our customers.”

How did Zanders support you to accelerate the onboarding of new banks?

“Zanders helped streamline what could be a very complicated process with banking partners. We appreciated their continuous communication and follow-up on progress, as well as their advocacy on our behalf to challenge some of the requirements we faced and even get a few of them waived.”

How did you perceive the collaboration between Remote and Zanders, given the project was delivered on a fully remote basis?

“It worked very well. We would not have been able to work with a partner that didn’t know how to collaborate remotely. Working with the Zanders team, we were able to apply the same operating principles we use internally – clearly defining guidelines and expectations, overcommunicating, and building a high degree of trust between our teams.”

To round off, what advice would you give anyone starting to work 100% remotely?

“Life is too short to waste time commuting. Remote work is all about freedom, flexibility and happiness. When we do what we like, we’ll get great results, regardless of where the work is done.”

The collaboration between Remote and Zanders

Viktorija Janevska, manager at Zanders: “Account opening and KYC has been a challenge for many corporates in recent years, given the increasing KYC requirements and rather cumbersome onboarding experience. We at Zanders have been happy to support Remote with this interim project, taking the workload from the team and being the first point of contact for the banks with regards to the account opening and onboarding documentation requests. Key success factors for the project were the open and transparent communication between the two teams, regular update calls and priority setting.

Remote not only demonstrates an innovative working approach when it comes to working remotely, but also by using chats for most of their internal communication rather than email communication. During the project, the transition from email to chat communication required some adaptation and from time to time a reminder to use the preferred channel. It has been a great experience to accompany Remote on its journey and are looking forward to see the company’s further success.”

Lee-Ann Perkins shares expert insights on mastering risk and project management, empowering treasury teams to future-proof their strategies and drive impactful change.

As one of our key clients, we had the opportunity to speak with Lee-Ann Perkins to gain some insight on two topics that almost every treasury team at one point or another will have to grapple with – risk management and project management.

During one of our discussions, you mentioned how risk management is perhaps not given the appropriate level of consideration that it demands. Can you please elaborate on this and explain how the treasury team of an organization can address this issue?

"The treasury department’s purpose is to safeguard the financial assets of the company. In doing so, we control the financial risks by conforming with board and internal policies and shareholder needs. Risk is inherent in the treasurers position and often this is overlooked and undervalued until a crisis hits.

We address and highlight the importance of risk management by ensuring our teams are curious, well trained, and informed. Start by allowing treasury the opportunity to ask questions and gather as much information as possible to ensure small misjudgments don’t lead to material costs down the road.

Treasury departments must be rigorous in ensuring compliance with established policies, procedures, and financial regulations. This is a non-negotiable aspect inherent in the position. We should guide conversations with the goal of strengthening processes to safeguard the company and its reputation.

I like the saying ‘A tsunami starts with small detectable waves’. And I believe that treasury departments are in a unique position to identify and evaluate risks and possible solutions. Treasury department is a financial function that both front faces (with banks, vendors, investors, rating agencies to name a few) and interfaces as partner of many internal stakeholders and areas of the business. These relationships, if well nurtured, can help the company to send solutions down the road to meet us when we most need them.

If given the resources, information and voice, Treasury can help the company manage and mitigate the causes of risk and not just the symptoms. Treasury departments have often been involved and brought to the table when a crisis has occurred. My mission statement for treasury departments, to use the Covid analogy, is: be the vaccine instead of the medicine! If you don’t manage risk, it will ultimately manage you!”

In addition to risk management, you also mentioned the importance of effective project management. Can you please share your experience in this area and what you learned through the process?

“It’s a well-known fact that treasury departments are often small and lack resources. Automation is a way to free up resources and allow treasury professionals to focus on strategy and risk management. Therefore, as we strive to automate and mature the function, projects have become integral in the treasury department’s strategy. Treasury professionals should have skills and abilities to effectively manage projects to success. We all know the saying ‘the devil is in the details’, which I agree with. But I take it one step further by stating that ‘the devil is in the details, but the success is in the strategy’.

In my experiences, project management has not been a part of treasury teams training. Due to the changing responsibilities of treasury professionals, we are often called upon to implement, change or enhance processes and/or systems. These projects require managing resources, selling ideas, implementing changes, and ensuring this is all done within the required budget and timeline. Success requires the practice of sound project management processes. These steps include planning (develop the project charter), organizing (create the organizational chart), leading (direct the resources) and controlling (continuous review of metrics). I learned this skillset in my MBA program, and it has served me well in leading multiple projects to successful outcomes. As this is most often a learned skill, I believe treasurers should advocate for training and development of this much needed skillset to ensure we follow the steps for successful project management.”

The topic of project management is quite often on the minds of treasury teams when they first contemplate the need to automate their systems. What advice would you give to an organization’s senior leadership that is forward-looking and seeking to adopt the benefits of technology but is cost-conscientious due to budgetary constraints?

“Firstly, I would say that this is the right attitude to embrace in the pursuit of future proofing and maturing the treasury department. Leaders have to manage company resources for the best and highest use of time and money. To compete for resources, treasury departments have to convince the leaders that their projects are in line with the company’s goals and strategy. Resource constraints are a real concern in companies. However, with proper planning and data-driven cost benefit analysis, these projects sell themselves when Treasury is able to demonstrate the quantifiable advantages.

Leaders should empower employees to utilize technologies for the intended purpose of creating efficiencies, providing information, and managing financial and operational risk through data and insights. Automation and dynamic forecasting systems proved particularly useful during the pandemic, when liquidity and short-term forecasts were crucial to run the business through unprecedented difficulties. Manually consolidating data can lead to missed opportunities and inaccurate information.

While treasury automation projects yield many benefits, they should be approached though a realistic lens. Projects should have a clear project charter, org chart, timeline and agreed-upon metrics to measure and demonstrate success. Automation projects have many stakeholders who need to provide input, assistance, and resources to ensure the desirable outcome. This requires thoughtful and deliberate planning and honest dialogue with all stakeholders.

When evaluating automation projects, the teams should ensure the systems are fit for purpose, scalable, and provide standardization, controls and audit infrastructure that will benefit the company. This approach allows companies to implement modules or systems that provide the most immediate beneficial impact and then scale up as they see the needs and benefits. I also suggest cloud-based systems for security, ease of implementation and cost.

My takeaway is to encourage leaders to ‘take the bot out of the human’, and allow treasury professionals to focus on capital structure, liquidity, risk management and meeting shareholder needs, and use technology to do repetitive transactions that help to simplify processes and reduce costs and errors while improving accuracy of information, data security and global standards.”

As versatile financial services professional, Lee-Ann Perkins has more than 19 years of domestic and international treasury management experience working in mid- to large-sized public and private organizations. She currently works as treasury professional at a global sporting and recreational goods and supplies company. Additionally, she is an Advisory Board member for Nacha, which governs the ACH Network, a member of the AFP CTP exam committee and treasury advisory group (TAG) and was previously the president of the Houston Treasury management Association.

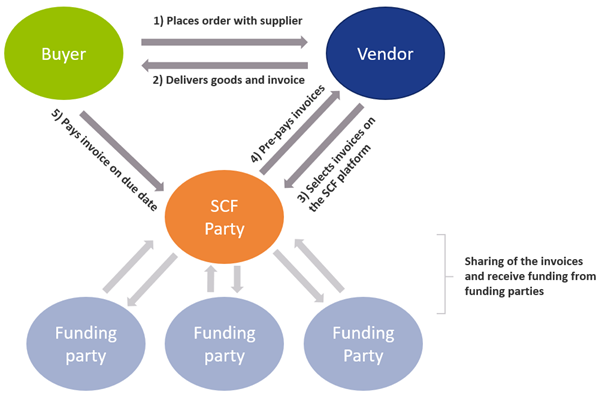

Vendor Supply Chain Finance (SCF) constitutes the transfer of a (trade) payable position towards the SCF underwriter (i.e. the bank). The beneficiary of the payment can then decide either to receive an invoice payment on due date or to receive the funds before, at the cost of a pre-determined fee.

The debtor’s bank account will only be debited on due date of the payable; hence the bank finances the differential between the due date and the actual payment date towards the beneficiary for this pre-determined fee. This article elaborates on why and how corporates set-up an SCF scheme with their suppliers.

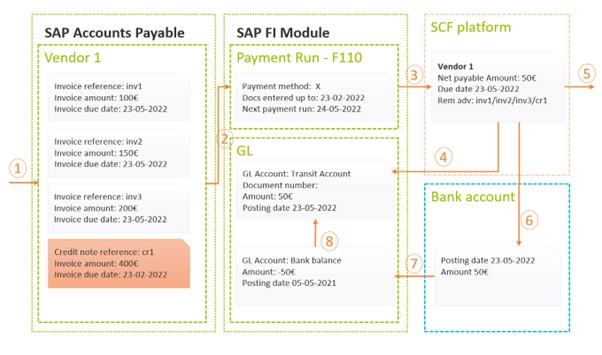

The Vendor SCF construction can be depicted as:

There are multiple business rationales behind Supply Chain Finance. Why would a corporate want to setup an SCF scheme with its suppliers? The most prominent rationales are:

- Reduction of the need of more traditional trade finance

The need for individual line of credits and bank guarantees for each trade transaction is removed, making the trade process more efficient. - Sellers can flexibly and quickly fund short term financing needs

If working capital or financing is needed, the seller can quickly request for outstanding invoices to be paid out early (minus a fee). - Sharing the benefits of better credit rating from buyer towards seller

Because the financing is arranged by the buyer, the seller can enjoy the credit terms that were negotiated between buyer and financier/bank. - Streamlining the AP process

By onboarding various vendors into the SCF process, the buyer can enjoy a singular and streamlined payment process for these vendors. - Strengthening of trade relations

Because of the benefits of SCF, more competitive terms on the trade agreement itself can be negotiated.

SCF is typically considered a tool to improve the working capital position of a company, specifically to decrease the cash conversion cycle by increasing the payment terms with its suppliers without weakening the supply chain.

Set-up and onboarding

Typically, a set-up and onboarding process consists of the following steps. First a financing for SCF is obtained from, for example, a bank. In addition, an SCF provider must be selected and contracted. Most major banks have their own solutions but there are many third parties, for example fintechs, that provide solutions as well. Consequently, the SCF terms are negotiated, and the suppliers are onboarded to the SCF process. Lastly, your system should of course be able to process/register it. Therefore, the ERP accounts payable module needs to be adjusted, such that the AP positions eligible for SCF are interfaced into the SCF platform. Besides, your ERP system needs to be adjusted to be able to reconcile the SCF reports and bank statements.

Design considerations and Processing SCF in SAP

In the picture below we provide a high-level example of how a basic SCF process can work using basic modules in SAP. Note that, based on the design considerations and capabilities of the SCF provider, the picture may look a bit different. For each of the steps denoted by a number, we provide an explanation below the figure, going a little deeper into some of the possible considerations on which a decision must be made.

- Invoice and credit note data entry; In the first step, the invoices/credit notes will be entered, typically with payment terms sometime in the future, i.e. 90 days. Once entered and approved, these invoices are now available to the payment program.

- Payment run: The payment run needs to be engineered such that the invoices that are due in the future (i.e. 90 days from now) will be picked up already in today’s run. Some important considerations in this area are:

- Payment netting logic: the netting of invoices and credit notes is an important design consideration. Typically, credit notes are due immediate and the SCF invoices are due sometime in the future, i.e. 90 days from now. If one would decide to net a credit note due immediate with an invoice due in 90 days, this would have some adverse impact on working capital. An alternative is to exclude credit notes from being netted with SCF invoices and have them settled separately (i.e. request the vendor to pay it out separately or via a direct debit). Additionally, some SCF providers have certain netting logic embedded in their platform. In this case, the SAP netting logic should be fully disabled and all invoices should be paid out gross. Careful considerations should be taken when trying to reconcile the SCF settled items report as mentioned in step 4 though.

- Payment run posting: When executing the SAP payment run it is possible to either clear the underlying invoices on payment run date or to leave them open until invoice due date. If the invoices are kept open, they will be cleared once the SCF reporting is imported in SAP (see step 4). This is decision-driven by the accounting team and depends on where the open items should be rolling up in the balance sheet (i.e. payable against the vendor or payable against the SCF supplier).

- Payment file transfer: At this step, the payment file will be generated and sent to the SCF supplier. The design considerations are dependent on the SCF supplier’s capabilities and should be considered carefully while selecting an appropriate partner.

- File format: Most often we advise to implement a best practice payment file format like ISO pain.001. This format has a logical structure, is supported out of the box in SAP, while most SCF partners will support it too.

- Interface technology: The payment files need to be transferred into the SCF platform. This can be done via a multitude of ways; i.e. manual upload, automatically via SWIFT or Host2Host. This decision is often driven internally. Often the existing payment infrastructure can be leveraged for SCF payments as well.

- Remittance information: By following ISO pain.001 standard, the remittance information that remits which invoices are paid and cleared, can be provided in a structured format, irrespective of the volume of invoices that got cleared. This ensures that the beneficiary exactly knows which invoices were paid under this payment. Alternatively, an unstructured remittance can be provided but this often is limited to 140 characters maximum.

- Payment status reporting: Some SCF supplier will support some form of payment status reporting to provide immediate feedback on whether the payments were processed correctly. These reports can be imported in SAP; SAP can subsequently send notifications of payment errors to the key users who can then take corrective actions.

- SCF payment clearing reporting: At this step, the SCF platform will send back a report that contains information on all the cleared payments and underlying invoices for that specific due date. Most typically, these reports are imported in SAP to auto reconcile against the open items sitting in the administration.

- Auto import: If import of the statement into SAP is required, the report should be in one of SAP’s standard-supported formats like MT940 or CAMT.053.

- Auto reconciliation: If auto reconciliation of this report against line items in SAP is required, the reports line items should be matchable with the open line items in the SAP administration. Secondly, a pre-agreed identifier needs to be reported such that SAP can find the open item automatically (i.e. invoice reference, document number, end2endId, etc.). Very careful alignment is needed here, as slight differences in structure in the administration versus the reporting structure of SCF can lead to failed auto reconciliation and tedious manual post processing.

- Pay out to the beneficiary: Onboarded vendors can access the SCF platform and report on the pending payments and invoices. The vendor has the flexibility to have the invoices paid out early (before due date) by accepting the deduction of a pre-agreed fee. The SCF provider should ensure payment is made.

- Debiting bank account: At due date of the original invoice, the SCF provider will want to receive the funds.

- Payment initiation vs direct debit: The payment of funds can in principle be handled via two processes; either the SCF customer initiates the payment himself, or an agreement is made that the SCF provider direct debits the account automatically.

- Lump debit vs line items: Most typically, one would make a lump payment (or direct debit) of the total amount of all invoices due on that day. Some SCF providers may support line by line direct debiting although this might result in high transaction costs. Line by line debiting might be beneficial for the auto reconciliation process in SAP though (see step 7)

- Bank statement reporting: The bank statement of the cash account will be received and imported into SAP. Most often, the statements are received over the existing banking interface.

- Bank statement processing: Based on pre-configured posting rules and reconciliation algorithms in SAP, the open items in the administration are cleared and the bank balance is updated appropriately.

To conclude

If the appropriate SCF provider is selected and the process design and implementation in SAP is sound, the benefits of SCF can be achieved without introducing new processes and therefore creating a burden on the existing accounts payable team. It is fully possible to integrate the SCF processes with the regular accounts payable payments processes without adding additional manual process steps or cumbersome workarounds.

For more information, contact Ivo Postma at +31 88 991 02 00.

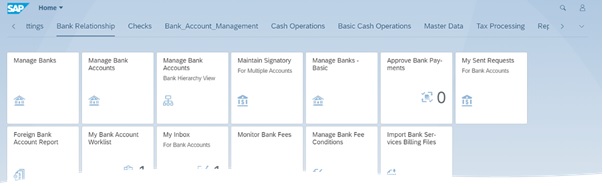

With house bank accounts treated as master data instead of configuration objects including the latest enhancement, the bank account subledger concept, SAP S/4HANA Bank Account Management (BAM) aims to shift responsibility of bank account management life cycle from the technical teams to the cash and banking teams.

Bank accounts can now be created and maintained by the cash and banking responsible team, giving them more control over the timing of opening or closing of an account as well as expediting the overall process and limiting the number of users involved in the maintenance of the accounts.

Figure 1 – Launchpad BankApplications

The advantages of using the full version of BAM are multiple, but below we highlight three of the main reasons full BAM is a must have for the companies using one or multiple SAP environments.

Flexible workflows

Maintenance of bank account data can trigger workflows based on the organization’s requirements and the approval processes in place. With the workflows the segregation of duties can be enforced when maintaining a bank account.

Even though workflows are not a new functionality in S/4HANA, the fact that workflow templates are available and can be amended by defining preconditions, step sequences and recipients improves the approval process of bank accounts.

The workflows can be created and activated as completely new ones or based on the already existing templates . You can create a new workflow by copying an existing one and updating the parameters according to the new requirements.

All the requests to release or approve bank account changes are available as of S/4HANA 2020 in the My Inbox for Bank Accounts app, the dedicated inbox app where users can check the status of each request initiated by the users themselves or sent to them and act upon.

Easy data replication

One of the challenges multiple organizations have, especially those operating various SAP environments, is data synchronization and replication. We often come across situations when banks, house banks and bank accounts are not maintained in all relevant environments creating data inconsistencies and making processes more difficult than they already are.

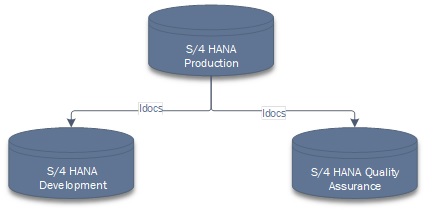

One of the ways of avoiding these types of situations is by replicating banks, house banks and bank accounts from production to quality assurance and to development environments using standard Idocs.

Figure 2 – Bank data replication in S/4 HANA

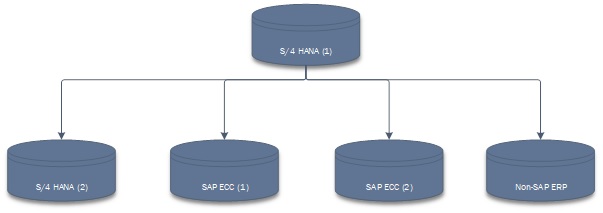

If the organization is operating on multiple SAP and non-SAP instances and running processes in a S/4 HANA side-car solution, the challenge of maintaining banks, house banks and bank accounts grows exponentially. Distributing the data via Idocs will not only keep all the systems coordinated, it will also decrease the amount of manual work and avoid situations when processes fail because of delays in keeping the data up to date in all relevant environments.

Figure 3 -Bank data replication across multiple environments

Simple way of managing cash pools

Cash pooling structures can easily be set up by the user and in this way the BAM solution is integrated with the process of making cash management transfers.

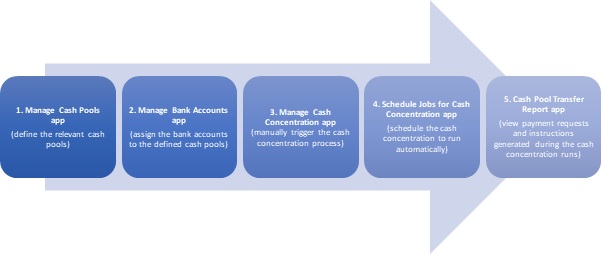

Even though the cash pooling and cash concentration in S/4HANA are managed using five different apps (shown in the figure below), the actual structure of the cash pool is defined directly in the Manage Bank Accounts app (Cash Pool tab).

Figure 4 – Five apps to manage cash pooling and cash concentration in S/4HANA

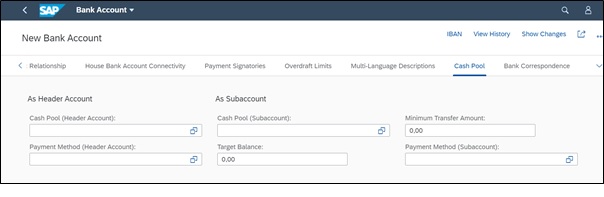

In the Cash Pool tab, the user can define the cash pool structure as per each company’s requirements. It is important to keep in mind the fact that a bank account can be assigned only to two different cash pools: once as the header account of a cash pool, and once in a different cash pool, as a subaccount.

The cash pools created in the system are not restricted to one company code but can be defined using various currency accounts belonging to multiple company codes. For each of the bank accounts included in a cash pool, a target balance as well as a minimum transfer amount can be defined in the Cash Pool tab of the Manage Bank Accounts app, with the mention that both (target balance as well as minimum transfer amounts) must be defined in the bank account currency.

During the cash concentration process, when bank transfers are generated, the payment methods defined in this tab will be picked up. Therefore, if required, two different payment methods can be assigned; the first for the structure where the bank account is acting as a header account and the second for the one where the account in scope is a subaccount. To pick them up from the drop-down list, the assigned payment methods must be initially setup in the system.

To conclude

Maintaining banks, house banks and bank accounts can be a difficult task especially in large organizations operating with different SAP and non-SAP environments. It can be time-consuming; it can involve multiple people from different parts of the organization (IT, master data, cash and banking etc.) and it can easily be prone to errors and mismatches if not correctly maintained and synchronized. Having one single source of truth for the bank accounts – which is easy to maintain, user-friendly, with appropriate controls in place and reporting capabilities, easy to replicate the data across different environments and which allows the user to create and maintain not only the bank accounts but also the cash pool structures – can save time, resources and simplify processes.