As tax authorities intensify their scrutiny of intercompany financing transactions, multinational enterprises must anticipate emerging trends and strengthen their transfer pricing positions.

Recent case law and regulatory developments provide useful guidance on what to expect in 2026 and on the approach that should be followed to mitigate the risk of challenges on intra-group loans.

Historically, tax authorities focused primarily on interest rate benchmarks when reviewing intra-group loans, cash pools and guarantees. Today, however, their analysis has become significantly broader and more sophisticated, extending to a range of interrelated factors such as contractual terms, debt capacity, and creditworthiness.

The sections below outline the key trends and risks shaping intra-group loan transfer pricing and highlight what multinational groups should address as part of their planning and compliance efforts for 2026.

Arm’s Length Terms & Conditions for Intra-Group Loans

Verifying that the terms and conditions of intra-group loans are consistent with how independent parties would contract remains a critical focus. In addition to establishing an arm’s length interest rate and the appropriate amount of debt (further explained below), it is also necessary to assess whether the other terms and conditions are at arm’s length. This involves considering the main features of the loan, and evaluating their impact on the risk profile of both the borrower and the lender, as well as on the arm’s length interest rate. Relevant terms that should be considered include currency, maturity, repayment schedule, and callability.

In 2025, courts emphasized that Transfer Pricing documentation must not only include a benchmark analysis but also a clear explanation of the contractual features agreed, especially for features such as subordination, maturity, interest structures, and repayment conditions. These features should align with the actual conduct of the parties and with the economic reality.

Multinationals have also seen a rise in challenges derived from discrepancies between the legal agreements drafted, the price applied between the entities involved, and the information presented in the Transfer Pricing report. A clear example is one-year loans that are automatically renewed, with the same price being applied and with no repayments being made, where tax authorities may reclassify them as longer-term arrangements, which typically carry a higher interest rate.

What to consider in 2026: It is important for multinational enterprises to carefully assess these terms and conditions before issuing a loan, as they will have a direct impact on the interest rate applied to the transaction. Drafting a comprehensive loan agreement that clearly outlines these terms, aligns with the conditions applied in practice, and is supported by a robust Transfer Pricing analysis is recommended to mitigate the risk of challenges by tax authorities.

Debt Capacity Analyses for Intra-Group Loans

Tax authorities are increasingly scrutinizing whether the amount of intra-group debt is economically justified and supported by a clear business purpose. They are also evaluating whether the debt aligns with arm’s length principles and serves a legitimate economic function consistent with the borrower’s overall business strategy.

A debt capacity analysis is often conducted to determine whether the borrower has the financial capacity to repay the loan and whether an unrelated party would provide a similar amount of financing under comparable conditions. If tax authorities consider that the amount of debt is excessive, adverse tax consequences could arise, such as the requalification of the debt as equity and/or the denial of a portion of the interest expense deduction.

Over the last two years, jurisdictions such as Germany and Australia introduced administrative guidelines formalizing debt capacity considerations. This trend has been further reinforced by case law in different countries over the past year. For example, in Luxembourg, a major hub for treasury companies and investment funds, the Luxembourg Administrative Court in 2025 issued a pivotal decision in case No. 50602C rejecting an automatic 85:15 debt-to-equity standard and holding that arm’s length analyses must be fact-specific and supported by data rather than mechanical ratios.

What to consider in 2026: Multinationals are expected to prepare robust debt capacity analyses for each borrower entity, demonstrating that independent lenders would extend a similar amount of debt. The debt quantum should be supported by financial projections, coverage ratios, and a documented business purpose, all included in the corresponding Transfer Pricing report.

Debt Capacity Analysis

A guide to demonstrating the arm’s length principle in debt financing

Get the whitepaperCredit Rating Analyses for Financial Transactions: Stand-Alone vs Group Rating

Both tax administrations, and subsequently, courts, are scrutinizing the credit rating approaches applied by taxpayers in the context of intra-group loans. Credit rating analyses are a core step when pricing intra-group loans, as the risk profile of the borrower has a material impact on the applicable interest rate.

While simplified blanket ratings across a group were once tolerated, tax authorities and courts are now emphasizing the importance of entity-specific ratings adjusted for implicit support.

In Belgium, on June 6, 2025, the Court of First Instance of Leuven clarified that credit ratings must be substantiated and not merely assumed based on group affiliation. Based on this ruling, the borrower should be assessed on a stand-alone basis, taking into account the impact of the new debt quantum on its financial position. Where implicit group support is considered, it must be properly substantiated through a thorough implicit support analysis and cannot be assumed by default our automatically applied.

In the Netherlands, the Court of Appeal of Amsterdam, in its judgment of 11 September 2025, addressed, among other topics, the guarantee fees applied by the taxpayer and rejected their payment, emphasizing the importance of factoring implicit support into the credit rating applied to the borrower. This once again highlights the relevance of a two-step process: first, the calculation of the stand-alone rating, and second, the adjustment of this rating for implicit support.

As this is a highly relevant topic, and both the lender’s jurisdiction (seeking a lower credit rating, which drives higher interest income) and the borrower’s jurisdiction (seeking a higher credit rating, which drives lower interest expense) have opposing incentives, multinationals need to have a robust and consistent process in place.

What to consider in 2026: Companies should apply a consistent methodology for credit rating analyses based on the principles and best practices set out in Chapter X of the OECD Transfer Pricing Guidelines. Where possible, this involves performing an individual credit rating analysis for each borrower, adjusted for group implicit or explicit support. In addition, this analysis should be properly documented in the Transfer Pricing report.

Cash Pooling Structures and Synergy Allocation

Cash pooling structures remain an area of intense scrutiny by tax authorities worldwide. Cash pool Transfer Pricing analyses can be complex and time-consuming for a variety of reasons.

On the one hand, the participants’ accounts need to be priced on an arm’s length basis (considering the specific currency and the risk profile of each entity). This also includes identifying long-term structural balances and pricing them separately, where relevant. On the other hand, the cash pool leader needs to receive appropriate remuneration for the functions performed, risks assumed, and assets employed.

In addition, the OECD Transfer Pricing Guidelines state in paragraph 10.143 that: “The remuneration of the cash pool members will be calculated through the determination of the arm’s length interest rates applicable to the debit and credit positions within the pool. This determination will allocate the synergy benefits arising from the cash pool arrangement amongst the pool members and will generally be done once the remuneration of the cash pool leader has been calculated.”

Tax authorities are increasingly considering these recommendations, and this is becoming particularly relevant in jurisdictions where multinational enterprises have cash-rich pool entities, as tax authorities may expect that a portion of the synergies generated is allocated to them.

Finally, the involvement of multiple countries adds further complexity, as local jurisdiction-specific interpretations of the OECD Transfer Pricing Guidelines may arise. Over the past year, for example, a notable case was issued by the Spanish Supreme Court on July 15, 2025 (ruling 3721/2025). In its decision, the Court rejected the asymmetry of interest rates depending on whether they related to deposits made by the Spanish subsidiary or to amounts received by it as a loan, and emphasized that the remuneration of the leading entity must be consistent with its functions as a mere treasury centralization entity. This highlights the importance of following a coherent methodology based on the OECD Transfer Pricing Guidelines in order to support the position adopted in the event of a challenge by local tax authorities.

What to consider in 2026: Multinationals with cash pooling structures, especially where the amounts involved are material, should perform a Transfer Pricing analysis in line with the best practices set out in the OECD Transfer Pricing Guidelines. This includes: 1) pricing the debit and credit positions of the participants, identifying structural balances; 2) calculating the synergy benefits generated by the structure; and 3) allocating these synergies between the cash pool leader and the participants.

Key Takeaways for Intra-Group Loans Transfer Pricing in 2026

- Tax authorities are moving beyond interest rate benchmarking and increasingly focusing on the full arm’s length characterization of intra-group loans, including contractual terms and economic substance.

- Debt capacity analyses are becoming increasingly important, as evidenced by recent regulatory developments and case law.

- Credit rating analyses should be performed on a stand-alone basis and adjusted for implicit or explicit group support, in line with the OECD Transfer Pricing Guidelines.

- Cash pooling arrangements require careful allocation of synergies between participants and the cash pool leader based on functions, risks, and realistic alternatives.

- Robust and consistent transfer pricing documentation remains essential to mitigate the risk of challenges in an environment of heightened scrutiny.

Zanders Transfer Pricing Solution

As tax authorities intensify their scrutiny of loans, cash pools, and guarantees, it is essential for companies to carefully adhere to the recommendations outlined above.Does this mean that additional time and resources are required? Not necessarily.

Technology provides an opportunity to minimize compliance risks while freeing up valuable time and resources. The Zanders Transfer Pricing Suite is an innovative, cloud-based solution designed to automate the Transfer Pricing compliance of financial transactions.

With over eight years of experience and trusted by more than 100 multinational corporations, our platform is the market-leading solution for compliance with OECD Transfer Pricing Guidelines for intra-group loans, guarantees, and cash pooling arrangements

Our clients trust us because we provide:

- Transparent and high-quality embedded intercompany credit rating models.

- A pricing model based on an automated search for comparable transactions.

- Automatically generated, 40-page OECD-compliant Transfer Pricing reports.

- Debt capacity analyses to support the quantum of debt.

- Cash Pool Solution which calculates the synergies generated by the structure.

- Legal documentation aligned with the Transfer Pricing analysis.

- Benchmark rates, sovereign spreads, and bond data included in the subscription.

- Expert support from our Transfer Pricing specialists.

- Quick and easy onboarding—completed within a day!

Get a free trial of the Zanders Transfer Pricing Suite

Get your free trial

As Transfer Pricing compliance becomes increasingly important, discover how treasury can streamline UAE loan pricing with the right tools.

Until recently, most UAE corporate entities were not subject to corporate income tax. This changed with the Ministry of Finance’s announcement on 31 January 2022, introducing a federal corporate tax regime applicable to financial years starting on or after 1 June 2023. The new regime also formalised the UAE’s transfer pricing framework as part of its commitment to the OECD BEPS standards.

Federal Decree-Law No. 47 of 2022 sets out the corporate tax rules and embeds transfer pricing requirements under Articles 34–36 and 55. In addition to the Federal Decree-Law No. 47, the UAE’s Ministry of Finance and Federal Tax Authority also issued additional rules and guidance specific to transfer pricing:

- Ministerial Decision No. 97 of 2023 – Sets out the conditions for the preparation of Master Files and Local Files in line with OECD BEPS Action 13.

- UAE Transfer Pricing Guide – Detailed guidance on the practical impact and implementation of transfer pricing regulations. The guide was prepared in alignment with the OECD’s Transfer Pricing Guidelines.

The incorporation of these rules, together with the growing attention from tax authorities on the Transfer Pricing of Intra-Group Loans, has significantly increased the focus of tax and treasury teams on the importance of transfer pricing in the region.

Importance for treasury teams

Over two years on from the UAE’s adoption of a formal corporate income tax regime, the region has positioned itself as a potential financial hub for multinationals to set up their centralised group finance and treasury functions. The UAE’s economic reforms and growing alignment with international financial standards further strengthen its case as a pragmatic and effective financial hub.

Multinationals are increasingly looking towards centralised, in-house financing functions to more effectively navigate variables between markets such as regulatory requirements, currency exposures, and broader liquidity and cash flow targets.

As more multinationals set up financing hubs in the UAE, scrutiny from the Federal Tax Authority will increase accordingly, particularly with a legitimate transfer pricing regime now in place. This means that both treasury teams and tax departments need to price intra-group loans on an arm’s length basis.

Alignment with the OECD TP Guidelines

The UAE follows the OECD TP Guidelines Chapter X for the transfer pricing of intra-group financial transactions, with additional local guidance provided in section 7.1.3.2 of the UAE Transfer Pricing Guide. Intercompany loans must reflect arm’s length terms, including loan amount, maturity, repayment terms, and arm’s length interest rates.

In practice, a 4-step process should be followed to comply with these requirements:

Step 1: As a first step, the terms and conditions should be reviewed to ensure their commercial rationale and that they reflect the actual economic reality of the parties. In this sense, special consideration should be given to the loan amount and whether an independent party would extend such an amount to the borrower. To this end, the so-called Debt Capacity Analyses are performed.

Step 2: As a second step, a credit rating analysis should be performed. While the recommended approach is to follow a bottom-up approach, based on the standalone credit rating of the entity adjusted for group support, in some cases a more simplified top-down credit rating approach can also be considered acceptable.

Step 3: As a third step, the pricing analysis is performed, typically by application of the external CUP method, identifying comparable third-party transactions with similar characteristics. Of course, the necessary comparability adjustments should be performed to reflect the differences between the external comparables and the loan under analysis.

Step 4: Finally, the analysis should be documented in a Transfer Pricing Report, explaining in a transparent manner the analysis performed in the previous steps. It is important to have legal documentation in place, reflecting the terms and conditions of the loan that have been considered during the analysis.

Interest limitation rules:

Alongside traditional transfer pricing regulations, the UAE also enacted interest deductibility rules in Article 30 of the Ministerial Decision No. 120 of 2023. The provisions are broadly modelled after the OECD’s BEPS Action 4. These interest limitation rules should be considered alongside transfer pricing regulations. In principle, net interest expense in the UAE is deductible only up to 30% of the borrower’s adjusted EBITDA. This rule only applies to cumulative interest expense greater than AED 12 million in a given year.

Article 28(1)(b) provides further rules that should apply specifically to intercompany arrangements. In addition to the foundational rule, any intercompany interest expense is non-deductible if:

- The financial arrangement lacks economic substance or commercial purpose; and

- The lender is not subject to a corporate tax rate of more than 9%; and

- The main purpose or one of the main purposes of the loan was to obtain a tax advantage.

Each of these must be proven for any interest deductions to be denied. These rules function to mitigate intergroup profit shifting and hybrid arrangements.

Zanders Transfer Pricing Software as a tool:

As tax authorities intensify their scrutiny, it is essential for companies to carefully adhere to the recommendations outlined above.

Does this mean additional time and resources are required? Not necessarily. Technology provides an opportunity to minimize compliance risks while freeing up valuable time and resources. The Zanders Transfer Pricing Software is an innovative, cloud-based solution designed to automate the transfer pricing compliance of financial transactions.

With over eight years of experience and trusted by more than 90 multinational corporations, our platform is the market-leading solution for intra-group loans, guarantees, and cash pool transactions.

Our clients trust us because we provide:

- Transparent and high-quality embedded intercompany rating models.

- A pricing model based on an automated search for comparable transactions.

- Automatically generated, 40-page OECD-compliant Transfer Pricing reports.

- Debt capacity analyses to support the quantum of debt.

- Legal documentation aligned with the Transfer Pricing analysis.

- Benchmark rates, sovereign spreads, and bond data included in the subscription.

- Expert support from our Transfer Pricing specialists.

- Quick and easy onboarding—completed within a day!

If you are interested in exploring how the Transfer Pricing Software could optimize your transfer pricing processes for financial arrangements, let us know in the contact form below.

Book a demo

Contact us

AI is everywhere – but many treasurers still struggle to move beyond the hype and identify real, value-adding applications. Here is one real way to leverage AI for real value in treasury.

AI is everywhere – but many treasurers still struggle to move beyond the hype and identify real, value-adding applications. That’s why in this blog series, we’ll explore four practical use cases in depth, each resulting in a concrete, actionable application you could begin implementing tomorrow.

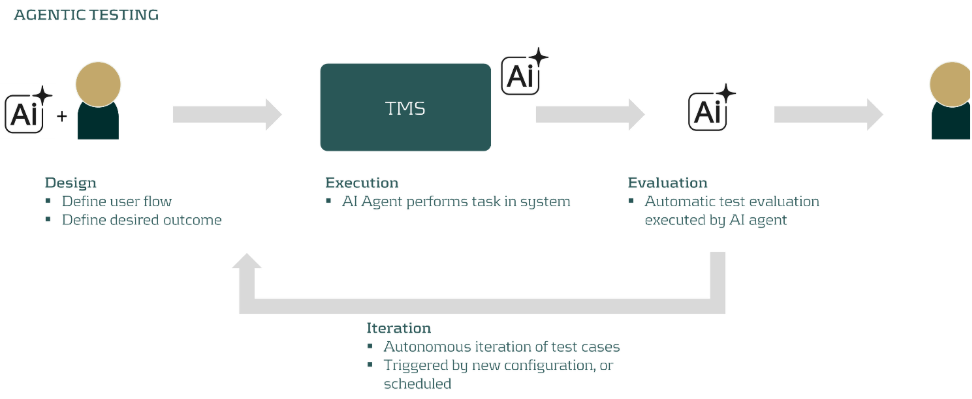

In this blog, we focus on one of the most time-consuming challenges in any treasury transformation: system testing. Testing remains highly manual, repetitive, and resource-intensive. But the rise of AI agents is changing the game, offering a way to make testing faster, more intuitive, and highly repeatable.

The Challenge

Testing is at the heart of every treasury transformation. It’s a meticulous, iterative process: before you even begin, you need a robust set of test cases that reflects your specific workflow to ensure every critical scenario is covered, without drowning in an endless list. Then comes the manual execution, documentation, and feedback cycles, repeated again and again until every issue is resolved.

Even after go-live, the work isn’t over. Regular system updates and configuration changes mean more rounds of regression testing to catch any unexpected side effects. It’s essential work, but it can be a real drain on time and resources.

Now, thanks to AI, there’s a smarter way.

The Solution

AI agents are autonomous actors that can interact directly with your web browser and through that with your Treasury Management System (TMS) to complete tasks and resolve issues. Imagine instructing an AI agent in plain language, and watching it execute complex test cases right in the user interface. The agent is able to navigate to the right page, fill in information in the forms, the buttons, and record output. The flexibility of these agents even allow them to identify error messages and validate the result of a set of actions.

Armed with vendor documentation, solution designs, and implementation blueprints, the AI agent proposes a comprehensive set of test cases and relates those to actions in your system of choice. Users can easily add their own scenarios by simply describing the workflow. The agent then navigates the system, executes the tests, and records the results, all autonomously.

Worried about safety? Don’t be. Today’s test automation tools come with robust guardrails:

- Test environments only: No risk to production.

- Controlled user rights: The agent gets only the permissions it needs.

- Plan mode: The agent presents its action plan for human approval before anything runs.

With these safeguards, the risk of unintended actions is virtually eliminated—while the efficiency gains are game-changing.

You can build AI agents in-house, but many organizations will benefit even more from cloud-based platforms. These solutions:

- Lower deployment costs and speed up implementation

- Offer ready-made integrations

- Enable users to share successful test scenarios

At Zanders, we’ve developed an AI-powered test suite that plugs directly into leading cloud TMS platforms—empowering treasurers to accelerate testing without sacrificing control.

A Real-World Example

Let’s make this tangible. Suppose you want to test a workflow for adjusting FX exposure and generating a report. The AI agent, using system documentation and blueprints, proposes relevant user flows. One test case might be:

“Change the EUR/USD exchange rate to 1.12, create a new EUR/USD FX Forward with a six-month maturity, and run the FX Exposure report.”

The agent executes these steps, records the results, and once the optimal route is captured, can repeat the test autonomously and even evaluate the outputs itself. Over time, you build a powerful, reusable suite of automated test scenarios for both transformation projects and ongoing regression testing.

Conclusion

AI in treasury is no longer a futuristic possibility, it’s a practical, high-impact technology that treasury teams can start leveraging today. Do you want to explore automated testing? Contact us! Are you interested in other concrete use cases, learn more about transforming your treasury operations for the digital age.

Automate your testing

Get in touch to talk to us about automating your treasury testing and how we can help.

Contact us

As AI transforms business at record speed, treasurers can now harness its power to automate one of their most complex tasks: intercompany loan pricing.

The interest in AI has been increasing at record pace, with new technology releases every month and an impressive number of new use cases for chatbots or agents. However, many treasurers still struggle to translate this hype into value-added implementations for their business. These upcoming blog series explore practical use cases for AI that delivers concrete value to treasurers. This article specifically shares an implementation of AI agents to automate the pricing, review and documentation of intercompany loans.

The challenge

One of the core functions for many treasury departments is the distribution of cash in their group. Intra-group loans are one of the tools used by treasurers to distribute cash, but their use comes with challenges. The interest rate on intercompany loans has a significant impact on the tax expense incurred by the subsidiary and taxable income received by the head-office and therefore should be based on an arm's length approach.

Arm’s length pricing of intercompany loans requires a detailed analysis of the credit standing of the borrower, the influence of the group on the borrower’s credit risk, and a review of the debt market to determine a price. Due to the tax implications, this process should be documented in detail including sources and models. Regulations surrounding transfer pricing of financial transactions have been expanding in many countries in the past years, posing greater challenges for treasury teams to perform a complex process with high compliance requirements. As a result, many have resorted to advisors or build complex Excel models to perform the recurring pricing analyses.

The solution

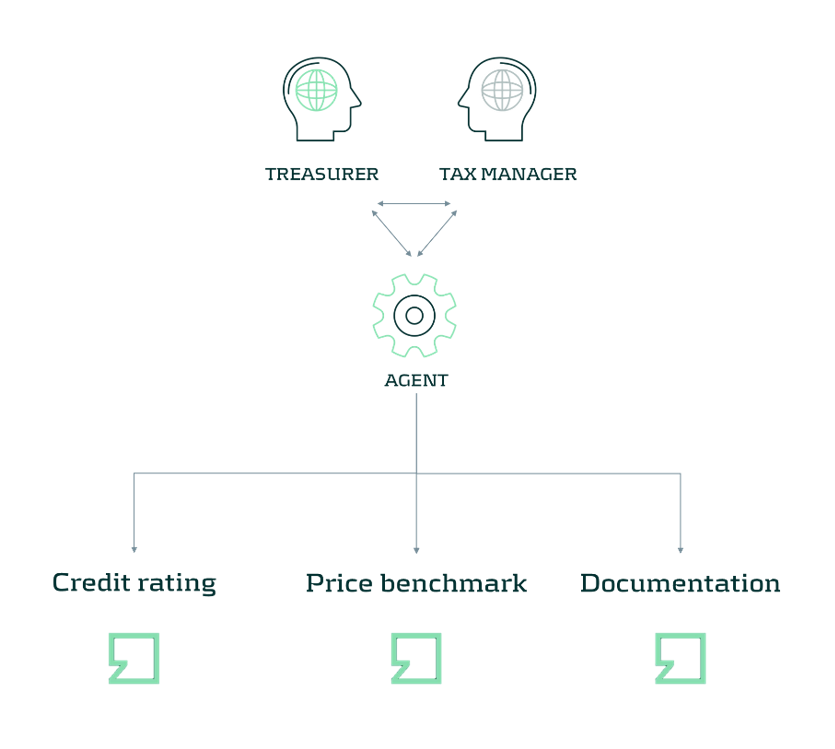

The main challenge when automating the pricing of intercompany loans is the access to data and models. A compliant process relies on the periodic retrieval of benchmark transactions to set an interest rate – for example with bonds, loans, or a Credit Default Swap (CDS). On the other hand, an objective calculation of the credit risk requires a model that is explainable and is filled with company data.

AI Agents are a powerful tool that can be used to automate the retrieval of data and execution of tools in a complex process with changing inputs. In the diagram below, an AI Agent is coupled with a credit rating model, a tool to gather benchmarking data, and a documentation method. In our implementation, we have used the modules in the Zanders Transfer Pricing Solution to provide this functionality to the agent. Next to the tools, it is important to provide the Agent with sufficient context on what role it should play and how it should execute a pricing analysis. The agent should understand the compliance requirements and the tools before it can reliably run the process. For this use case, this is done through context engineering by providing example cases, differences in methods, and checks that the agent should perform.

In the resulting setup, the Agent can automate the full pricing step: identifying entities, calculating a credit rating, and running a pricing benchmark. As a result, the Agent provides a report that is generated according to our template.

With the same tools, we can extend the system even further, by reviewing past calculations versus policies and tax regulations to spot high risk cases or evaluating the credit position of entities to set borrowing limits or update credit ratings. By automating these processes, treasurers can move away from the operational hassle of pricing intercompany loans and instead focus on managing the funding mix of their group. Agents take care of automatic handling of loans and the importing or exporting of data, where treasurers set the objectives of the pricing approach and funding.

AI in Treasury is no longer a futuristic possibility - it's a practical, high-impact technology that Treasury teams can start leveraging today. Do you want to explore intercompany pricing? Let us know in this contact form below.

If you are interested in more use cases, read more here.

Explore intercompany pricing

Get in touch to talk to us about intercompany loan pricing and how we can help.

Contact usManaging over 80 intercompany loans annually and with a wide geographical scope, Royal Philips faced the challenge of complying with their Transfer Pricing obligations.

Zanders Transfer Pricing Suite is an innovative, cloud-based solution designed for companies looking to automate the Transfer Pricing compliance of financial transactions. With over five years of experience and trusted by more than 60 multinational corporations, the platform is the market-leading solution for financial transactions Transfer Pricing. On March 31, 2023, Zanders and Royal Philips jointly presented the conference "How Philips Automated Its Transfer Pricing Process for Group Financing" at the DACT (Dutch Association of Corporate Treasurers) Treasury Fair 2023.

Context

The publication of Chapter X of Financial Transactions by the OECD, as well as its incorporation into the 2022 OECD Transfer Pricing Guidelines, has led to an increased scrutiny by tax authorities. Consequently, transfer pricing for financial transactions, such as intra-group loans, guarantees, cash pools, and in-house banks, has become a critical focus for treasury and tax departments.

ZANDERS TRANSFER PRICING SOLUTION

As compliance with Transfer Pricing regulations gains greater significance, many companies find that the associated analyses consume excessive time and resources from their in-house tax and treasury departments. Several struggle to automate the end-to-end process, from initiating intercompany loans to determining the arm's length interest, recording the loans in their Treasury Management System (TMS), and storing the Transfer Pricing documentation.

Since 2018, Zanders Transfer Pricing Solution has supported multinational corporations in automating their Transfer Pricing compliance processes for financial transactions.

ROYAL PHILIPS CASE STUDY

Managing over 80 intercompany loans annually and with a wide geographical scope, Royal Philips faced the challenge of complying with their Transfer Pricing obligations. During the conference, Joris Van Mierlo, Corporate Finance Manager at Philips, detailed how Royal Philips implemented a fully integrated solution to determine and record the arm's length interest rates applicable to its intra-group loans.

An update on the new transfer pricing regulations

In January 2022, the OECD incorporated Chapter X to the latest edition of their Transfer Pricing Guidelines, a pivotal step in regulating financial transactions globally. This addition aimed to set a global standard for transfer pricing of intercompany financial transactions, an area long scrutinized for its potential for profit shifting and tax avoidance. In the years since, we have seen various jurisdictions explicitly incorporating these principles and providing further guidance in this area. Notably, in the last year, we saw new guidance in South Africa, Germany, and the United Arab Emirates (UAE), while the Swiss and American tax authorities offered more explanations on this topic. In this article we will take you through the most important updates for the coming years.

Finding the right comparable

The arm's length principle established in the OECD Transfer Pricing Guidelines stipulates that the price applied in any intra-group transaction should be as if the parties were independent.1 This principle applies equally to financial transactions: every intra-group loan, guarantee, and cash pool should be priced in a manner that would be reasonable for independent market participants. Chapter X of the OECD Guidelines provided for the first time a detailed guidance on applying the arm's length principle to financial transactions. Since its publication, achieving arm's length pricing for financial transactions has become a significant regulatory challenge for many multinational corporations. At the same time the increased interest rates have encouraged tax authorities to pay increased attention to the topic – strengthened with the guidelines from Chapter X.

To determine the arm’s length price of an intra-group financial transaction, the most common methodology is to search for comparable market transactions that share the characteristics of the internal transaction under analysis. For example, in terms of credit risk, maturity, currency or the presence of embedded options. In the case of financial transactions, these comparable market transactions are often loans, traded bonds, or publicly available deposit facilities. Using these comparable observations, an estimate is made on the appropriate price of a transaction as a compensation for the risk taken by either party in a transaction. The risk-adjusted rate of return incorporates the impact of the borrower’s credit rating, any security present, the time to maturity of the transaction, and any other features that are deemed relevant. This methodology has been explicitly incorporated in many publications including in the guidance from the South African Revenue Service (SARS)2 and the Administrative Principles 2023 from the German Federal Ministry of Finance.3

The recently published Corporate Tax Guide of the UAE also implements OECD Chapter X, but does not explicitly mention a preference for market instruments. Instead, the tax guide prefers the use of “comparable debt instruments” without offering examples of appropriate instruments. This nuance requires taxpayers to describe and defend their selection of instruments for each type of transaction. Although the regulation allows for comparability adjustments for differences in terms and conditions, the added complexity poses an additional challenge for many taxpayers.

A special case of financial transaction for transfer pricing are cash pooling structures. Due to the multilateral nature of cash pools, a single benchmark study might be insufficient. OECD Chapter X introduced the principle of synergy allocation in a cash pool, where the benefits of the pool are shared between its leader and the participants of the pool based on the functions performed and risks assumed. This synergy allocation approach is also found in the recent guidance of SARS, but not in the German Administrative Principles. Instead, the German authorities suggest a cost-plus compensation for a leader of a cash pool with limited risks and functionality. Surprisingly, approaches for complex cash pooling structures such as an in-house bank are not described by the new German Administrative Principles.

To find out more about the search for the best comparable, have a look at our white paper. You can download a free copy here.

Moving towards new credit rating analyses

Before pricing an intra-group financial transaction, it is paramount to determine the credit risks attached to the transaction under analysis. This can be a challenging exercise, as the borrowing entity is rarely a stand-alone entity which has public debt outstanding or a public credit rating. As a result, corporates typically rely on a top-down or bottom-up rating analysis to estimate the appropriate credit risk in a transaction. In a top-down analysis, the credit rating is largely based on the strength of the group: the subsidiary credit rating is derived by downgrading the group rating by one or two notches. An alternative approach is the bottom-up analysis, where the stand-alone creditworthiness of the borrower is first assessed through its financial statements. Afterwards, the stand-alone credit rating is adjusted with the group’s credit rating based on the level of support that the subsidiary can derive from the group.

The group support assessment is an important consideration in the credit rating assessment of subsidiaries. Although explicit guarantees or formal support between an entity and the group are often absent, it should still be assessed whether the entity benefits from association with the group: implicit group support. Authorities in the United States, Switzerland, and Germany have provided more insight into their views on the role of the implicit group support, all of them recognizing it as a significant factor that needs to be considered in the credit rating analysis. For instance, the American Internal Revenue Service emphasized the impact of passive association of an entity with the group in the memorandum issued in December 2023.4

The Swiss tax authorities have also stressed the importance of implicit support for rating analyses in the Q&A released in February 2024.5 In this guidance, the authorities did not only emphasize the importance of factoring the implicit group support, but also expressed a preference for the bottom-up approach. This contrasts with the top-down approach followed by many multinationals in the past, which are now encouraged to adopt a more comprehensive method aligned with the bottom-up approach.

Interested in learning more about credit ratings? Our latest white paper has got you covered!

Grab a free copy here.

Standardization for success

Although the standards set by the OECD have been explicitly adopted by numerous jurisdictions, the additional guidance further develops the requirements in complex transfer pricing areas. Navigating such a complex and demanding environment under increasing interest rates is a challenge for many multinational corporations. Perhaps the best advice is found in the German publication: in its Administrative Principles, it is stressed that the transfer price determination should occur before completion of the transaction and the guidelines prefer a standardized methodology. To get a head start, it is important to put in place an easy to execute process for intra-group financial transactions with comprehensive transfer pricing documentation.

Despite the complexity of the topic involved, such a standardized method will always be easier to defend. One thing is for certain: the details of transfer pricing studies for financial transactions, such as the analysis of ratings and the debt market, will continue to be a part of every transfer pricing and tax manager agenda for 2024.

For more information on Mastering Financial Transaction Transfer Pricing, download our white paper.

Citations

- Chapter X, transfer pricing guidance on financial transactions, was published in February 2020 and incorporated in the 2022 edition of the OECD TP Guidelines. ↩︎

- Interpretation Note 127 issued in 17 January 2023 by the South African Revenue Service. ↩︎

- Administrative Principles on Transfer Pricing issued by the German Ministry of Finance, published on 6 June 2023. ↩︎

- Memorandum (AM 2023-008) issued on 19 December 2023 by the US Internal Revenue Service (IRS) Deputy Associate Chief Counsel on Effect of Group membership on Financial Transactions under Section 482 and Treas. Reg. § 1.482-2(a). ↩︎

- Practical Q&A Guidance published on 23 February 2024 by the Swiss Federal Tax Authorities. ↩︎

Estee Lauder’s European Treasury Center is responsible for managing cash and liquidity management for the group and its subsidiaries over multiple continents by providing intercompany loans and liquidity facilities to local entities.

In an effort to continuously improve and automate its internal processes, the American multinational cosmetics company wanted to leverage technology and further enhance the Transfer Pricing compliance of financial transactions. As a result, it engaged Zanders to use its cloud-based Transfer Pricing Suite.

Estee Lauder has been Zanders’ client for quite some years. “We have been working with Zanders before in some projects and that always worked very well. In this instance too”, says Bart Taeymans, Vice President Global Treasury Operations. “They helped to draft and execute the bank selection RfP and restructure our European banking structure, and supported with the implementation of SAP Inhouse Cash and Bank Communication Management. And recently, they supported us with their Zanders Inside Transfer Pricing Suite.”

In view of the changed regulatory environment, we wanted to increase control of the entire process. Zanders Transfer Pricing Suite looked as a sustainable tool to automatize the process, while maintaining a robust technical methodology compliant with the OECD TP Guidelines.

Bart Taeymans, Vice President Global Treasury Operations

Challenge

New OECD Transfer Pricing guidelines

With the release of Chapter X by the OECD, the company wanted to implement a new process in order to comply with its Transfer Pricing obligations in-house, without depending on external parties, Taeymans explains. “In view of the changed regulatory environment, we wanted to increase control of the entire process. Zanders Transfer Pricing Suite looked as a sustainable tool to automatize the process, while maintaining a robust technical methodology compliant with the OECD TP Guidelines’’.

Solution

Sophisticated tool

Treasury Director Marc Vandewaeter: “Zanders’ Transfer Pricing Suite is very sophisticated. In addition, during the onboarding process, Zanders added some additional currencies to the tool that were not there yet for us to cover additional regions. Another important thing for us is that we are able to instantly generate the Transfer Pricing reports – including the supporting documents providing details on the economic analyses.”

Due to the tool’s flexibility, Estee Lauder had a managed transition phase. “It’s challenging to change processes, but the tool supported the transition phase in a controlled manner.”

Having all the information in one tool helps us understanding the approach followed and financial information considered for each case. This is important for us as we need to make sure that we fully understand the details.

Marc Vandewaeter, Treasury Director

Performance

Timely implementation

Taeymans: “I think it’s been a great integrated implementation. The team was very supportive, providing clarifications where needed and support when required – all to ensure timely implementation of the new procedure, focused on the start of our new fiscal year.”

Vandewaeter: “The challenge of importing the financial data was that it needed to be implemented in the Zanders Inside tool format, which is required to determine a rating. Luckily all financial data from all our affiliates is already standardized. That makes it easier to reproduce and implement this data. That saves quite a lot of time.”

“The benefit we have is that we are on one SAP instance globally”, adds Taeymans. “That helps us to great extent in retrieving the financial information in a structured manner. So once we had the templates to convert to the information required by Zanders, everything went very well.”

The entire process in one user-friendly platform

Vandewaeter has been intimately involved in working with the tool. “We wanted to make sure that Zanders’ tool would provide a consistent approach for all transactions, in line with what we had done before, and that potential differences in the results could be explained. Having all the information in one tool helps us understanding the approach followed and financial information considered for each case. This is important for us as we need to make sure that we fully understand the details.”

Taeymans: “To have that entire process – from the financial information, credit rating analyses, benchmark rates, to the final reports – featured in one tool is obviously what we’ve been looking for. It’s very important to have it all in one system generating a full report on an entity basis. Of course, you need to know what to enter and what to select. But as a web-based tool it is very user-friendly, easy to navigate and well designed. It is quite easy to extract the pricing for a certain loan. And from an operational point of view, it is also useful to do a simulation and it doesn’t take much time to do that. You need to upload all the financial statements, but it is more dynamic and the pricing update is based on current data. In addition, the support received from Zanders team is very good.”