In this article, we will delve deeper into some of the key offerings of SAP BTP for treasury and explore how it can contribute to driving innovation within treasury.

The SAP Business Technology Platform (BTP) is not just a standalone product or a conventional module within SAP's suite of ERP systems; rather, it serves as a strategic platform from SAP, serving as the foundational underpinning for all company-wide innovations. In this article, we will delve deeper into some of the key offerings of SAP BTP for treasury and explore how it can contribute to driving innovation within treasury.

The platform is designed to offer a versatile array of tools and services, aiming to enhance, extend, and seamlessly integrate with your existing SAP systems and other applications. Ultimately enabling a more efficient realization of your business objectives, delivering enhanced operational efficacy and flexibility.

Analytics and AI

One of the standout features of SAP BTP for treasury is its analytics and planning solution, SAP Analytics Cloud (SAC). This feature seamlessly connects with different data sources and other SAP applications. It supports Extended Planning & Analysis and Predictive Planning using machine learning models.

At the core of SAC, various planning areas – like finance, supply chain, and workforce – are combined into a cloud-based interconnected plan. This plan is based on a single version of the truth, bringing planning content together. Enhanced by predictive AI and ML models, the plan achieves more accurate forecasting and supports near-real-time planning. Users can also compare different scenarios and perform what-if analysis to evaluate the impact of changes on the plan equipping organizations to prepare for uncertainties effectively.

Application Development and Integration

An organization's treasury architecture landscape often involves numerous systems, custom applications, and enhancements. However, this complexity can result in challenges related to maintenance, technical debt, and operational efficiency.

Addressing these challenges, SAP BTP offers a solution known as the SAP Build apps tool. The tool enables users to adapt standard functionalities and create custom business applications through intuitive no-code/low-code tools. This allows that all custom development takes place outside your SAP ERP system, thereby preserving a ‘clean core’ of your SAP system. This will allow for a simpler, more streamlined maintenance process and a reduced risk of compatibility issues when upgrading to newer versions of SAP.

In addition, SAP BTP facilitates seamless connectivity through a range of connectors and APIs integrated within the SAP Integration Suite. Enabling a harmonious integration of data and processes across diverse systems and applications, whether they are on-premise or cloud-based.

Process Automation and Workflow Management

Efficient process automation and workflow management play a pivotal role in enhancing treasury operations. SAP BTP offers an efficient solution named SAP Build Process Automation which enables users to design and oversee business processes using either low-code or no-code methods. It combines workflow management, robotic process automation, decision management, process visibility, and AI capabilities, all consolidated within a user-friendly interface.

A significant advantage of SAP BTP's workflow approach over conventional SAP workflows is the unification of workflows across diverse systems, including non-SAP systems and increased flexibility, enabling smoother interaction between processes and systems.

The integration of SAP BTP for workflow with different SAP modules such as TRM, IHC, BAM is facilitated through the SAP Workflow Management APIs within your SAP S/4 HANA system.

In the context of treasury functions, SAP Build Process Automation proves invaluable for automating and refining diverse processes such as cash management, risk management, liquidity planning, payment processing, and reporting. For instance, users can leverage the integrated AI functionalities for tasks like collecting bank statements/account balance information from different systems, consolidating information, saving and/or distributing the cash position information to the appropriate people and systems. Furthermore, the automation recorder can be employed to mechanize the extraction and input of data from diverse systems. Finally, the SAP Build Process Automation can also be utilized to create workflows for complex payment approval scenarios, including exceptions and escalations.

Extensions to the Treasury Ecosystem

SAP BTP extends the treasury ecosystem with multiple treasury-specific developed solutions, seamlessly enhancing your treasury SAP S/4 HANA system functionality. These extensions include: Multi-Bank Connectivity for simplified and secure banking interactions, SAP Digital Payment Add-On for efficiently connecting to payment service providers. Trading Platform Integration for streamlined financial instrument trading, SAP Cloud for Credit Integration to assess business partner credit risk, SAP Taulia for Working Capital Management, Cash Application for automatic bank statement processing and cash application, and lastly, SAP Market Rates Management for the reliable retrieving of market data.

Empowering organizations with extensive treasury needs by enabling them to selectively adopt these value-added capabilities and solutions offered by SAP.

Alternatives to SAP BTP

The primary driving factor to consider integrating SAP BTP as an addon to your SAP ERP is when there is an integrated company-wide approach towards adopting BTP. Furthermore, if the standard SAP functionalities fall short of meeting the specific demands of the treasury department, or if the need for seamless integration with other systems arises.

It's important to prioritize the optimization of complex processes whenever feasible first, avoiding the pitfall of optimizing inherently flawed processes using advanced technologies such as SAP BTP. It is worth noting that the standard SAP functionality, which is already substantial, could very well suffice. Consequently, we recommend conducting an analysis of your processes first, utilizing the Zanders best practices process taxonomy, before deciding on possible technology solutions.

Ultimately, while considering technology options, it's wise to explore offerings from best-of-breed treasury solution providers as well – keeping in mind the potential need for integration with SAP.

Getting Started

The above highlights just a glimpse of SAP BTP's capabilities. SAP offers a free trial that allows users to explore its services. Instead of starting from scratch, you can leverage predefined business content such as intelligent RPA bots, workflow packages, predefined decision and business rules and over 170 open connectors with third-party products to get inspired. Some examples relevant for treasury include integration with Trading Brokers, S4HANA SAP Analytics Cloud, workflows designed for managing free-form payments and credit memos, as well as connectors linking to various accounting systems such as Netsuite Finance, Microsoft Dynamics, and Sage.

Conclusion

SAP BTP for Treasury is a powerful platform that can significantly enhance treasury. Its advanced analytics, app development and integration, and process automation capabilities enable organizations to gain valuable insights, automate tasks, and improve overall efficiency. If you are looking to revolutionize your treasury operations, SAP BTP is a compelling option to consider.

With subsidiaries all over the world, ASICS wanted to standardize and make its treasury operations more efficient. To optimize its treasury function, ASICS Europe (AEB) decided to implement the SAP Treasury and Risk Management module in 2017.

With this came the decision to set up a new company code to separate ASICS Europe’s treasury activities from its commercial activities. Apart from the pros, it raised new challenges too.

ASICS stands for ‘Anima Sana In Corpore Sano’, loosely translated ‘a sound mind in a sound body’. This Japanese company was founded by Kihachiro Onitsuka in 1949. He felt that Japanese youth, who had lived through World War II, were in the process of being derailed and had too few pursuits. Onitsuka wanted to bring back the healthy life through sports, which demanded proper sportswear. And so, he decided to produce basketball shoes under the name Onitsuka Tiger.

Inventive like octopus

Onitsuka strived for perfection and innovation. One of the anecdotes about the origin of the ASICS basketball shoes is that he came up with an inventive idea when eating octopus salad from a bowl. During that diner, a leg of the animal stuck to the side of the bowl. When Onitsuka realized this was because of the animal’s suction cups, he decided to design basketball shoes with tiny suction cups on the sole for more grip. It turned out to be a revolutionary idea.

Another remarkable fact is that Nike-founder Phil Knight started his career at ASICS. When he visited the Onitsuka Tiger office in 1963, he was impressed by the inventive sports shoes and asked Onitsuka to become their sales agent in the US. After a few years working for ASICS Knight decided to start his own sports brand.

The tiger stripes go global

During the years after foundation, the range of sports activities provided by Onitsuka expanded to include a variety of Olympic styles used by athletes around the world. The current ASICS brand signature, the crossed stripes that appear on the side of all the shoes, was first introduced in 1966 during the pre-Olympic trials for the 1968 Summer Olympics in Mexico City. Martial arts star Bruce Lee was the first international celebrity to popularize this design. In 1977, Onitsuka Tiger merged with GTO and JELENK to form ASICS Corporation. Despite the name change, a vintage range of ASICS shoes is still produced and sold internationally under the Onitsuka Tiger label.

In 1977, ASICS opened a first small European office in Düsseldorf, in the home garage of a representative. This German city had a relatively large Japanese community and was centrally located in Europe. In 1995, ASICS Europe, Middle East and Africa (EMEA) relocated to a new headquarters in the Netherlands, from where more subsidiaries were established, and the ASICS network further expanded. The company built and rented several large distribution centers in Europe. In addition, the sales channels broadened from traditional wholesale to opening ASICS stores – first outlet stores, followed by a flagship store and e-commerce. Today, the brand sells all items through omnichannel.

The first implementation of the SAP system involved communication with the bank via the SWIFT platform.

Eugene Tjemkes, Head of Global Business Transformation Finance

Challenge

The implementation of SAP modules

In 2017, to further optimize their treasury function, ASICS Europe decided to implement the treasury management functionality of SAP. “That is when our cooperation with Zanders started”, says Eugene Tjemkes, Head of Global Business Transformation Finance. “The first implementation of the SAP system involved communication with the bank via the SWIFT platform, an in-house cash system with all kinds of automatic entries where Treasury acts as a payment factory – also on behalf of the subsidiaries.”

The Japanese headquarters opted for more or less the same treasury solution as those of the EMEA countries. “The other regions did not choose it, either because of their small size, or since they are single country regions (such as Australia) or because foreign currency plays a lesser role, such as in the US. In Europe, on the other hand, we are involved in currency transactions and hedging every day.”

Treasury as a separate company

Besides the SAP Treasury and Risk Management (TRM) module, ASICS Europe also implemented SAP Cash Management (CM), SAP In-House Cash (IHC) and the SAP Bank Communication Manager (BCM) in 2017. With this came the decision to set up a new company code that would separate the treasury functionality of ASICS Europe BV (AEB) from its commercial activities, as tax rules only allowed AEB to provide services and do business in Europe. In addition, the new company code, AEB Treasury, ensured global reach and provided cost savings and standardization due to the foreseen treasury activities in the EMEA region, Japan, and the Americas.

Tjemkes explains: “As a legal part of AEB, it was not possible for Treasury to do anything for ASICS US or ASICS Asia. Transforming our treasury functionality into a separate legal entity would make it possible to develop treasury activities outside the EMEA region too. Therefore, there were plans to separate the treasury functionality from the existing corporate structure and make it a global subsidiary of the Japanese headquarters. From that vision, that treasury functionality would be housed in a separate legal entity, we started implementing our treasury system in 2017. The system was set up accordingly; AEB Treasury became a separate company in SAP, although it was not a legally separated entity.”

Bringing back the treasury activities under AEB

However, the plan to service the company’s entities in other regions with an inhouse bank operating from Europe, did not go as planned. Instead, different regions of ASICS were supported with a local solution. And therefore, splitting into two company codes became irrelevant.

Tjemkes: “Due to the separated treasury functionality, the accounting department had to consolidate the reports to get them into one financial statement. After using SAP TRM, CM, IHC and BCM for a few years, we discovered that a legal entity administered in two different company codes appeared to be time-consuming while executing our day-to-day processes. Initially, the plan was to do this temporarily, with the idea that Treasury would become a separate entity. But unfortunately, the plan was ultimately not adopted by the head office – from their perspective the advantages were not that great.”

This left AEB with the artificial situation that there were still two company codes in which it had to deal with all kinds of currencies, with different balance sheet items, and problems with the redistribution results. “That finally made us decide to remove that artificial separation of company codes and bring the treasury activities back under AEB. That also meant an adjustment in our TMS. We asked Zanders to support us in that project.”

Solution

Streamlining Treasury Processes

To solve the shortcomings of the artificial separation, Zanders proposed various alternatives. After conducting a few workshops with the treasury department, it was decided to discontinue all the current processes (TRM, IHC, GL accounting) in the company code representing AEB Treasury and re-implement it in company code representing AEB. Hence, a single company code for the single legal entity.

Magda Bleker, Treasury Specialist at ASICS EMEA: “This would save us time on labor-intensive activities, such as replicating accounting entries into company code representing AEB. Further, as internal dealing only occurred between company codes representing AEB and AEB treasury, ASICS would no longer have to use the internal dealing functionality by merging the two company codes. Removal of these activities would make the processes more efficient.”

Zanders and ASICS identified that the proposed solution would require high implementation effort. It would also lose the flexibility to quickly split the TRM and IHC processes into a new legal entity. However, as the pros outweighed the cons, ASICS decided to go ahead with the merging of the two company codes. The project started with Zanders updating the decision forms, configuration, and master data conversion documents created in 2017 during the SAP TRM and IHC implementation project, which reflected the changes, risks, and implications of migration. After which, the new functionality was configured and tested in a development system, ensuring that it would not disrupt the treasurers’ daily activities and to keep the payment structure intact and valid. Once the configuration had been updated in the system, the previous configuration documents were also updated to reflect the new changes in the system.

This would save us time on labor-intensive activities, such as replicating accounting entries into company code representing AEB.

Magda Bleker, Treasury Specialist

Performance

Improving further

Tjemkes: “Around 2016, we implemented SAP Fashion management system (FMS) ourselves in our European offices as a pilot for the whole world. FMS is an industry-specific solution, and we were the first company to go live with it. In addition to Europe, our branches in the US, Canada, China and Australia, among others, are now on this platform. But to properly implement the treasury system we really needed a specialist. Zanders is a very professional service provider, who knows very well what modern treasury is and how treasury systems work. We couldn’t have done this without them. They did the project management for us, helped write the project plan and created a test plan.”

Despite the corona pandemic in 2020, ASICS had a turnover of 328,784 million yen, which is more than 2.5 billion euro. The company took a great deal to investigate their current processes and see what was working and what was not. Like in sports, ASICS showed how one can still move forward when taking a step back, improving their processes and making them more efficient.

Next step for AEB is to expand its functionality around hedging. “The hedge contracts are now recorded in the system. We want to further optimize the transparency and efficiency of the closing of our hedge deals with banks, to mitigate all associated risks. We also want to improve the valuation of the hedge contracts. There are functionalities in SAP that allow us to better value hedges. But we have already taken many, very important steps.”

Sony Group implemented the SAP S/4HANA Treasury system successfully around the world in 2020. This project is called METRO Project in Sony Group.

Sony decided to start Digital Transformation (DX) of global treasury functions by launching the METRO Project officially in May 2018 and completed it by October 2020, working remotely under the COVID-19 global pandemic.

One of the biggest achievements of this project is the automation of the FX trading process. It is impressive to see how Sony’s FX dealers can trade large volume of FX deals with banks efficiently and effectively within a few minutes by using SAP S/4HANA Treasury and SAP’s TPI (Trading Platform Integration) connecting automatically with 360T Trading platform.

In this article, Sony’s project management team and Zanders partners will explain about this project.

Power of creativity and technology

Sony strives to fulfil its purpose to “fill the world with emotion, through the power of creativity and technology”, under its corporate direction of “getting closer to people”. To evolve and grow further, Sony strives to provide innovative products and contents full of emotional experiences in order to enrich people’s lives through the power of technology, across its six business segments consist of Game & Network Services, Music, Pictures, Electronics Products & Solutions, Imaging & Sensing Solutions, and Financial Services.

New-generation technologies made it possible for Sony Group to improve the global treasury platforms such as Payment-On-Behalf Of (POBO), Zero Balance Accounts (ZBA) sweeping, and Internal cash-less payments, Internal FX and Money Market deals settled via In-House-Cash accounts.

To improve FX hedging process, Sony introduced cutting-edge technologies such as SAP S/4HANA Treasury, SAP’s TPI connecting automatically with 360T Trading platform, to achieve the end-to-end automation of FX trading process.

To improve banking connectivity, Sony adopted the most advanced generation of banking technologies such as SWIFT for Corporates and ISO 20022 standards to connect with global banks smoothly for payment requests and bank statements via SWIFT network, which makes it possible for Sony’s cash management teams to grasp the latest status of cash position in a timely manner, even when the employees are forced to work from home in a tele-commuting era under COVID-19.

Additionally, Sony has implemented SAP In-House-Cash (IHC) for its treasury centers as In-House-Banks to support Sony subsidiaries in each region.

Sony’s journey for global treasury transformation

Sony Group has been making impressive efforts in the field of finance and treasury for a long time. Since 2000, Sony Global Treasury Services Plc (SGTS UK) has been established and operated in the United Kingdom as a global treasury center for Sony Group. SGTS UK has been providing POBO, ZBA sweeping, Internal cash-less payments, Internal FX and MM deals settled via internal accounts for Sony Group companies based on in-house treasury system developed by the Sony IS team. Cash and FX risk management were centralized in SGTS UK.

As Sony’s business grew in various business segments globally, it was necessary and rational to centralize funds and foreign exchange risks into SGTS UK. Before 1999, each regional finance/treasury center had managed FX and cash management individually, so it was a significant improvement by centralizing into SGTS UK. SGTS UK was deemed to be one of the most advanced in-house-bank of its kind around the world.

In 2016, SGTS UK transferred cash management functions for group companies in the USA to Sony Capital Corporation (SCC), to strengthen access to the US capital market, and to enhance flexibility to any changes in laws and regulations in the USA.

We departed from single global treasury center model and transformed into three main treasury center models by standardizing, simplifying, and automating treasury operations across all the treasury centers.

Hiroyuki Ishiguro, General Manager of Sony Group Corporation HQ Finance

Challenge

Decision to transform

In October 2017, Sony started a project planning to rebuild its global treasury management structures across the globe. By December 2017, after an RFP process among the shortlisted SAP consultants, Sony decided that Zanders would be the best SAP Treasury expert to advise and support in this project. Together with Zanders, Sony opted for SAP S/4HANA Treasury based on ‘Fit & Gap’ analysis.

In May 2018, Sony decided to start the METRO Project officially.

Mr. Hiroyuki Ishiguro, General Manager of Sony Group Corporation HQ Finance (‘SGC HQ Fin’), explains: “We decided to start DX in Sony’s global treasury operations, considering more diversified business segments in Sony Group, rapid changes of corporate treasury and banking activities in each region, innovations of financial technologies, and limitations of legacy treasury systems that could not so effectively support Sony’s group companies especially in the USA and Japan. We departed from single global treasury center model and transformed into three main treasury center models by standardizing, simplifying, and automating treasury operations across all the treasury centers.”

Mr. Ishiguro served as the project owner, led the project management team, and worked together with the project members from overseas based in eight countries. With the introduction of the METRO Project, Sony Group built a Treasury Management System (TMS) that supports all segments of the Sony Group’s business domain, excluding finance segment, providing treasury services for nearly 350 companies worldwide in Sony Group. The METRO Project was set in motion.

Technology risk

The legacy in-house systems had a technology risk, because it was developed with old programming languages and had been in operation since 2000.

Mr. Ishiguro also comments: “In the project planning phase, it was a challenge to justify the importance of METRO Project and to justify IT investment for TMS. Technology risk urged us to start the planning phase to kick off the METRO Project. Our previous legacy treasury systems were in-house systems developed long time ago. The technology risk would be a real risk at the end of December 2020, so we needed to take urgent action to transform the existing legacy systems into a new TMS. We needed to have a very solid and stable TMS to manage the cash management and FX risk management for Sony’s global businesses. This meant a large scale of IT investment.”

Solution

Choosing SAP and Zanders

Sony decided to choose SAP S/4HANA Treasury, as the “best” TMS fitting well with Sony’s requirements based on the FIT & GAP analysis.

Mr. Takehiro Yagi, Senior Project Manager of SGC HQ Fin, explains why: “We performed a fit-gap analysis on various options, including ERP type treasury systems like SAP, treasury-specialized TMS, and an inhouse developments. Zanders gave us a lot of valuable insights into each TMS at the FIT&GAP analysis. SAP S/4HANA Treasury was chosen as the best fit for Sony’s Treasury as a result. SAP S/4 HANA Treasury would ‘FIT’ with most of our requirements to cover Sony’s global treasury services with multiple treasury centers model. SAP had flexibility to achieve Sony’s unique requirements with custom enhancements. Furthermore, SAP S/4HANA Treasury could achieve integration with accounting systems effectively, because a lot of Sony group companies have been using SAP as an accounting platform.”

The most important condition was to choose SAP Treasury experts who have deep knowledge and wide experiences in global implementation of SAP S/4 HANA Treasury for both TRM and IHC modules for regional treasury centers. Zanders won the RFP process in a shortlist of world-famous SAP partner companies. As a result, Sony decided to select Zanders as the SAP implementation partner.

Sony faced serious shortage of SAP Treasury experts. In fact, the lack of SAP experts was one of the biggest challenges for METRO Project. It caused significant delays from the original master schedule, and it caused quality issues from the lack of knowledge and expertise in SAP Treasury. The close collaboration between Sony and Zanders proved to be a key success factor of the METRO Project.

Mr. Ishiguro adds: “As of 2017, there were only few experts in Japan who could develop SAP Treasury related modules in global implementation projects. We evaluated several global consulting firms and analyzed their proposals and considered if they can deliver what we wanted to achieve. However, in many cases their proposals were limited to a general update. Zanders comprehensively understood our treasury requirements in each key operation area and provided appropriate and concrete proposals.”

SAP global implementation in two waves

Then the project started with the planning phase. Mr. Takaaki Miura, Finance Manager in SGC HQ Fin, explains: “In order to obtain official approval, we developed comprehensive project plans. To minimize any impacts to Sony group companies at the ‘Go-Live’, we decided to implement SAP Treasury in two waves, as recommended by Zanders. We started explaining our project plan and built good consensus across the major stakeholders within Sony Group HQ. ROI was the most important factor when discussing with the Sony’s management. METRO Project obtained the official approval from Sony management in May 2018.”

In February 2020, the SAP IHC module was implemented in Sony Group globally as Wave 1. In August 2020, the TRM module was implemented globally as Wave 2.

To finalize user requirements, all the key members gathered in Tokyo from around the world to discuss on a face-to-face basis. Project team also visited Sony IS teams in India to discuss business requirements directly and to resolve critical issues effectively in Wave 1. To kick-start User Acceptance Tests, the project team visited each office of treasury centers for deep-dive discussions and user trainings, also in Wave 1.

Mr. Ishiguro explains: “Wave 1 go-live was just before the COVID-19 global pandemic. Up to the Wave 1 implementation we could do all the work in face-to-face meetings in Tokyo, the Netherlands, USA, UK or India. So, we have accumulated our experiences by implementing Wave 1 on a face-to-face basis. The COVID-19 virus spread around the world, affecting Wave 2 of METRO Project. It was a tough time for us to proceed with all the preparation activities on a remote basis. But by making the best use of our comprehensive implementation experiences from Wave 1, we could successfully proceed with all the activities for Wave 2, even on a remote basis.”

Zanders gave us a lot of valuable insights into each TMS at the FIT&GAP analysis.

Takehiro Yagi, Senior Project Manager of Sony Group Corporation HQ Finance

Performance

More sophisticated treasury operations

Now, Sony’s Treasury team is looking back with satisfaction on the project.

Mr. Yagi explains: “Now, we have visibility into global treasury activities from all regions, which is a real improvement. The treasury management system, METRO, was implemented as our global treasury platform with sophisticated technologies, greatly improved from the previous legacy in-house TMS systems. Our project members gained huge insights and experiences during the project, by working closely together with the Zanders team, all the partner banks, our IT teams and all the treasury members. That proved to be significant contributions to the development of human resources who can globally promote DX projects in the finance and treasury fields, which will continue to be needed in the future.”

Mr. Ishiguro agrees: “It is very important for both finance/treasury members and IT members to collaborate closely. It is also very important to promote young and mid-career employees actively, to provide opportunities for good trainings and for good ‘learning’ by direct and active participation to the project tasks.”

Mr. Miura adds: “One of the benefits of implementing METRO is that we can operate straight-through-processing (STP) in the FX trading process. Previously a lot of manual inputs needed to execute an FX trade with a bank, here and there, for the same deal. Now FX dealers can execute FX deals with banks who quoted best price effectively in a fully automated manner. We experience the improvements every day.”

Mr. Yagi agrees: “Our new SAP S/4HANA Treasury is much more advanced than our previous legacy treasury systems. SAP is much faster, more transparent and designed more effectively and efficiently, fully automated in various operations. Our previous application did not have any payment functionalities, so we had to enter payments separately manually into a separate E-banking system. SAP makes payment runs automatically, with timely status update of payment files. We have fewer issues or errors in METRO, all operations are run in a transparent manner, which prevents from fraud and other risks. The treasury system makes it possible to disclose financial information quickly to Sony management, the external auditor or investors if necessary.”

Mr. Ishiguro: “I strongly feel that we have been enjoying benefits of standardized treasury operations across regional treasury centers after the implementation of SAP Treasury. All three main treasury centers – in Japan, USA and UK – have been using the same treasury platform, and achieved a very good and stable operation, from various perspectives.”

A unique project

Apart from the pandemic restrictions, several elements made this project unique.

Firstly, the METRO Project was the first global IT system implementation project involving all business segments (except the Financial Services segment) of Sony Group. The project was unique because both Wave 1 and Wave 2 went live in a Big-Bang go-live approach around the world.

Secondly, it is unique because it was a ‘GLOBAL’ treasury transformation project with project members from eight countries. Treasury teams were in Tokyo, Singapore, Malaysia, UK, Poland and USA, and IT teams were in Bangalore, India, and the Zanders team was mainly in the Netherlands. As a result, the members of various nationalities have established a truly global project structure in which each project member was in charge of each task across the countries.

Ms Laura Koekkoek, partner at Zanders: “That global approach of this project, in which all regions and their personnel were combined, was really unique. And the whole collaboration between the different regions was really successful.”

Zanders partner, Ms Judith van Paassen adds: “The old systems already had the ambition of best practices processes in them but contained a technology risk. Now that there is a system to fully centralize, standardize and automate all processes is a big achievement.”

Mr. Ishiguro: “Whenever we discuss with Zanders, I remember we had very useful information available on key items, sometimes to deliver to the Sony senior management, or sometimes to resolve critical issues with a reasonable and solid solution, so we were able to proceed with the project with deep insights from SAP treasury experts.”

Next steps: From its new stable treasury basis, Sony's treasury is now ready for further steps for the future. In 2021, the system will be rolled out to Sony Group Corporation in Tokyo. Mr. Ishiguro lastly adds: “SAP S/4 HANA Treasury proved to be a very good TMS application for us. We would like to promote DX further, with close collaborations across our own Treasury members in each treasury center and our own SAP IT members, taking advantage of our experiences cultivated through METRO Project, in line with the mission of Sony Group Corporation, to ’lead and support the evolution of business through people and technology’."

With house bank accounts treated as master data instead of configuration objects including the latest enhancement, the bank account subledger concept, SAP S/4HANA Bank Account Management (BAM) aims to shift responsibility of bank account management life cycle from the technical teams to the cash and banking teams.

Bank accounts can now be created and maintained by the cash and banking responsible team, giving them more control over the timing of opening or closing of an account as well as expediting the overall process and limiting the number of users involved in the maintenance of the accounts.

Figure 1 – Launchpad BankApplications

The advantages of using the full version of BAM are multiple, but below we highlight three of the main reasons full BAM is a must have for the companies using one or multiple SAP environments.

Flexible workflows

Maintenance of bank account data can trigger workflows based on the organization’s requirements and the approval processes in place. With the workflows the segregation of duties can be enforced when maintaining a bank account.

Even though workflows are not a new functionality in S/4HANA, the fact that workflow templates are available and can be amended by defining preconditions, step sequences and recipients improves the approval process of bank accounts.

The workflows can be created and activated as completely new ones or based on the already existing templates . You can create a new workflow by copying an existing one and updating the parameters according to the new requirements.

All the requests to release or approve bank account changes are available as of S/4HANA 2020 in the My Inbox for Bank Accounts app, the dedicated inbox app where users can check the status of each request initiated by the users themselves or sent to them and act upon.

Easy data replication

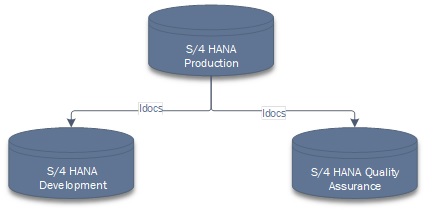

One of the challenges multiple organizations have, especially those operating various SAP environments, is data synchronization and replication. We often come across situations when banks, house banks and bank accounts are not maintained in all relevant environments creating data inconsistencies and making processes more difficult than they already are.

One of the ways of avoiding these types of situations is by replicating banks, house banks and bank accounts from production to quality assurance and to development environments using standard Idocs.

Figure 2 – Bank data replication in S/4 HANA

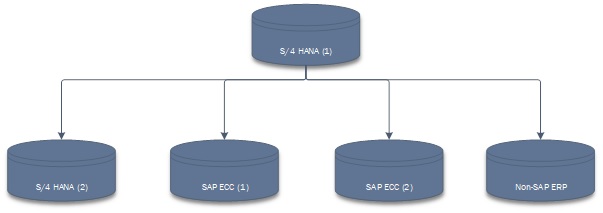

If the organization is operating on multiple SAP and non-SAP instances and running processes in a S/4 HANA side-car solution, the challenge of maintaining banks, house banks and bank accounts grows exponentially. Distributing the data via Idocs will not only keep all the systems coordinated, it will also decrease the amount of manual work and avoid situations when processes fail because of delays in keeping the data up to date in all relevant environments.

Figure 3 -Bank data replication across multiple environments

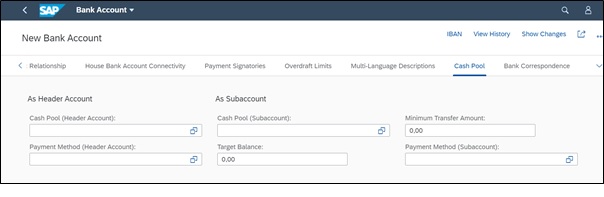

Simple way of managing cash pools

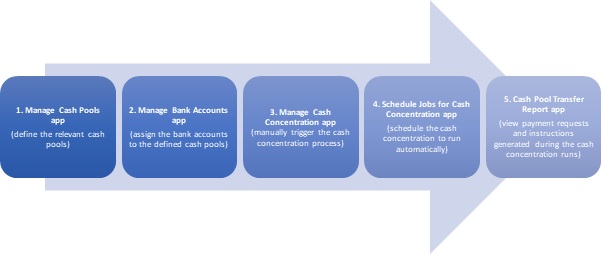

Cash pooling structures can easily be set up by the user and in this way the BAM solution is integrated with the process of making cash management transfers.

Even though the cash pooling and cash concentration in S/4HANA are managed using five different apps (shown in the figure below), the actual structure of the cash pool is defined directly in the Manage Bank Accounts app (Cash Pool tab).

Figure 4 – Five apps to manage cash pooling and cash concentration in S/4HANA

In the Cash Pool tab, the user can define the cash pool structure as per each company’s requirements. It is important to keep in mind the fact that a bank account can be assigned only to two different cash pools: once as the header account of a cash pool, and once in a different cash pool, as a subaccount.

The cash pools created in the system are not restricted to one company code but can be defined using various currency accounts belonging to multiple company codes. For each of the bank accounts included in a cash pool, a target balance as well as a minimum transfer amount can be defined in the Cash Pool tab of the Manage Bank Accounts app, with the mention that both (target balance as well as minimum transfer amounts) must be defined in the bank account currency.

During the cash concentration process, when bank transfers are generated, the payment methods defined in this tab will be picked up. Therefore, if required, two different payment methods can be assigned; the first for the structure where the bank account is acting as a header account and the second for the one where the account in scope is a subaccount. To pick them up from the drop-down list, the assigned payment methods must be initially setup in the system.

To conclude

Maintaining banks, house banks and bank accounts can be a difficult task especially in large organizations operating with different SAP and non-SAP environments. It can be time-consuming; it can involve multiple people from different parts of the organization (IT, master data, cash and banking etc.) and it can easily be prone to errors and mismatches if not correctly maintained and synchronized. Having one single source of truth for the bank accounts – which is easy to maintain, user-friendly, with appropriate controls in place and reporting capabilities, easy to replicate the data across different environments and which allows the user to create and maintain not only the bank accounts but also the cash pool structures – can save time, resources and simplify processes.

SAP provides multiple corporate treasury solutions to streamline, simplify, and standardize your payments, hedging processes, and treasury operations. We can assist you to successfully leverage these SAP solutions in order to simplify processes and converge toward best practice.

As part of an SAP Treasury system implementation or enhancement, we review existing business processes, define bottlenecks and issues, and propose (further) enhancements. Once we have applied these enhancements in your SAP system, we create a series of trainings and user manuals which layout the business process actions needed to correctly use the system.

“It’s only those who do nothing that make no mistakes, I suppose”

Joseph Conrad

This legendary saying of Joseph Conrad is still very valid today, as everyone makes mistakes. Therefore, we help our clients define smooth, seamless and futureproof processes which consider the possibility of mistakes or requirements for correction, and include actions to correct them.

Some common reasons why treasury payments require corrections are:

- No need for a cash management transfer between house bank anymore

- Incorrect house/beneficiary bank details were chosen

- Wrong currency / amount / value date / payment details

- Incorrect payment method

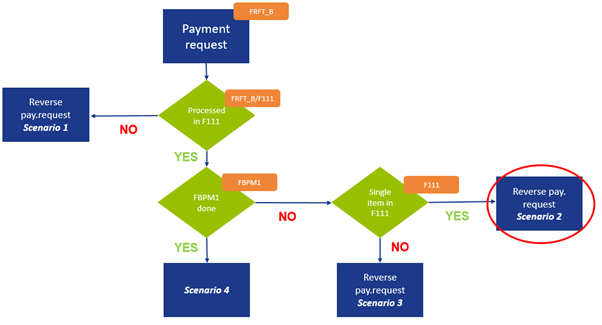

One of our practices is to first define a flowchart structure in form of decision tree, where each node represents either a treasury process (e.g. bank-to-bank transfer, FX deal, MM deal, Securities etc.), a transaction status in SAP, or an outcome which represents a solution scenario.

We must therefore identify the scope of the manual process, which depends on the complexity of the business case. At each stage of the transaction life cycle, we must identify whether it may be stuck and how it can be rectified or reversed.

Each scenario will bring a different set of t-codes to be used in SAP, and a different number of objects to be touched.

Below is an example of a bank-to-bank cash management transfer which is to be cancelled in SAP.

Figure 1: Bank-to-bank payment reversal

Scenario 2: A single payment request created via t-code FRFT_B and an automatic payment run is executed (F111), BCM is used but the payment batching (FBPM1) is not yet executed.

Step 1: define the accounting document to be reversed

T-code F111, choose the payment run created (one of the options) -> go to Menu -> Edit -> Payments -> Display log (display list) -> note the document number posted in the payment run.

Step 2: Reverse the payment document

T-code FB08: Enter the document number defined in step 1, choose company code, fiscal year and reversal reason, and click POST/SAVE.

SAP creates the corresponding offsetting accounting document.

Step 3: Reverse clearing of the payment request

T-code F8BW: Enter the document number defined in step 1, choose company code, fiscal year and click EXECUTE

The result is the payment request is uncleared.

Step 4: Reverse the payment request

T-code F8BV: enter the payment request (taken from FTFR_B or F111 or F8BT) and press REVERSE.

This step will reverse the payment request itself. Also, you may skip this step if you tick “Mark for cancellation” in STEP 3.

Step 5: Optional step, depending on the client setup of OBPM4 (selection variants)

Delete entries in tables: REGUVM and REGUHM. This is required to disable FBPM1 payment batching in SAP BCM for the payment run which is cancelled. The execution of this step depends on the client setup.

Call functional module (SE37): FIBL_PAYMENT_RUN_MERGE_DELETE with:

- I_LAUFD : Date of the payment run as in F111

- I_LAUFI : Identification of the payment run as in F111

- I_XVORL : empty/blank

The number of nodes and branches comprising the decision tree may vary based on the business case of a client. Multiple correctional actions may also be possible, meaning there is no unique set of the correctional steps applicable for all the corporates.

If you interested in a review of your SAP Treasury processes, their possible enhancements and the corresponding business user manuals, please feel free to reach out to us. We are here to support you!

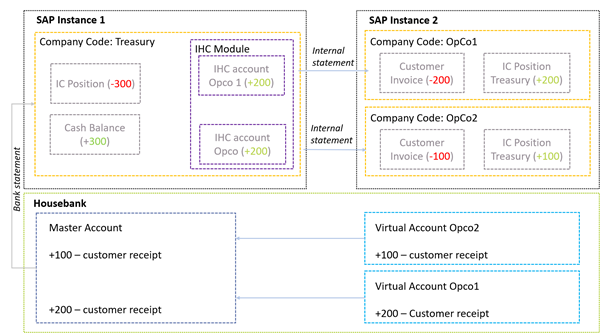

How to setup virtual accounts in SAP, part III. In the previous part of this series on ‘How to setup virtual accounts in SAP’, we delved into the details of a scenario where virtual accounts are managed on GL account level using SAP FI module only. This article investigates how SAP In-house cash (SAP IHC) module can be used to manage virtual accounts in your ERP.

SAP IHC is a module that facilitates a full suite of payment factory processes. It can be seen as an intercompany position subledger with a set of fancy features like POBO payment routing, bank statement allocation, arms-length intercompany interest calculations, out of the box payment and bank statement interfaces with participants (Opco’s) etcetera.

The process where virtual accounts are managed in IHC is depicted below:

In this process, we rely on a simple set of building blocks:

- In-house cash accounts to manage intercompany positions between Treasury and OpCo’s,

- GL accounts to represent external cash and the IC positions.

- Processing of external bank statements,

- Distribution of internal bank statements from IHC towards the OpCo’s ERP system,

- On the external bank statement for the Master Account, an identifier needs to be available that conveys to which virtual account the actual collection was originally credited. This identifier ultimately tells us which OpCo these funds originally belongs to and which IHC account to credit.

The idea here is that Treasury will receive the external bank statement and automatically post the receipts into the correct IHC account using the identifier. By posting items on the IHC account, the intercompany positions are updated. Then, at the end of the day, a set of internal bank statements is generated in IHC and sent through an interface to the OpCo’s ERP. The OpCo’s ERP processes these statements, clears out the customers invoices and updates the IC position with treasury.

The two major benefits of using IHC over the solution as described in the previous articles of this series are:

- The OpCo’s do not require any direct integration with the bank and can rely on internal interfacing with Treasury. Especially in companies with a fragmented ERP landscape this can become a valuable proposition.

- IHC can very aptly integrate virtual account management processes with internal netting payments, payments on behalf of (POBO) and payment in name of processes.

Implementing virtual accounts in SAP

In the explanation below we assume that the basic FI-CO settings for the company code a.o. are already in place. Also, it is by no means a complete inventory of all the settings that are required to get IHC up and running. It focusses more on the configurational parts that specifically cater for the VA requirements specifically.

Master data – general ledger accounts

Three sets of GL accounts need to be created: balance sheet accounts for the representation of the intercompany positions, one set for virtual account clearing purposes between the EBS and the IHC accounting process, and the GL account to represent the cash position with the external bank. These GL accounts need to be assigned to the appropriate company codes and can now be used to in the bank statement import process and the IHC accounting process.

In the Treasury entity we should create a single GL (per position currency) representing the IC position with all its OpCo’s because the granularity of IC position per OpCo is managed in the IHC subledger. This approach results in less of an increase of accounts in the chart of account.

Transaction code FS00

House bank maintenance bank account maintenance

In order to be able to process bank statements and generate GL postings in your SAP system, we need to maintain the house bank data first. A house bank entry comprises of the following information that needs to be maintained carefully:

- The house bank identifier: a 5-digit label that clearly identifies the bank branch.

- Bank country: The ISO country code where the bank branch is located.

- Bank key: The bank key is a separate bank identifier that contains information like SWIFT BIC, local routing code and address related data of your house bank.

Transaction code FI12

Secondly, under the house bank entry, the bank accounts can be created, including:

- The account identifier: a 5-digit label that clearly identifies the bank account.

- Bank account number and IBAN: This represents the bank account number as assigned to you by the bank.

- Currency: the currency of the bank account.

- G/L Account: the general ledger account that is going to be used to represent the balance sheet position on this bank account. Or the IC position with Treasury.

Transaction code FI12 in SAP ECC or NWBC in S/4 HANA

The idea here is that we maintain one house bank and bank account in the treasury company code that represents the Master account as held with your house bank. This house bank will have the G/L account assigned to it that represents the house banks external cash position.

In each of the OpCo’s company codes, we maintain one house bank and bank account that represents each of the IHC bank accounts as held with the treasury center. This house bank will have the G/L account assigned to it that represents the intercompany position with the Treasury entity.

Electronic bank statement settings

The electronic bank statement (EBS) settings will ensure that, based on the information present on the bank statement, SAP is capable of posting the items into the general or sub ledgers according to the requirements. There are a few steps in the configuration process that are important for this to work:

1) Posting rule construction

Posting rules construction starts with setting up Account symbols and assigning GL accounts to it. The idea here is to define at two account symbols, the first one to represent the external Cash position (BANK), and the second one for the virtual account clearing between IHC and EBS (VACLR)

A separate account symbol for customers is not required in SAP.

For the account symbol for BANK we do not assign a GL account number directly in the settings; instead we will assign a so-called mask by entering the value “+++++++++”. What this does in SAP is for every time the posting rule attempts to post to “BANK”, the GL account as assigned in the house bank account settings is used (FI12 or NWBC setting above).

For the account symbol VACLR we can assign a dedicated O/I clearing GL that is used to clear out the EBS posting against the IHC posting (more on that later). These GL accounts should have already been created in the first step (FS00).

Now that we have the account symbols prepared, we can start tying together these symbols into posting rules. We need to create 3 posting rules.

Posting rule 1 is going to debit the BANK symbol and it is going to credit VACLR symbol

Posting rule 2 is going to debit the BANK symbol and it is going to credit a BLANK symbol. The posting type however is going the be set to value 8 “Clear Credit Subledger Account”. What this setting is going to attempt is to clear out any open item sitting in the customer sub-ledger using algorithms. We will explain more on these algorithms below.

As you can imagine, posting rule 1 is applicable for the Treasury entity. Posting rule 2 is going to be used in the OpCo’s EBS process.

Transaction code OT83

2) Posting rule assignment

In the next step we can assign the posting rules to the so-called “Bank Transaction Codes” (or BTC’s like NTRF) that are typically observed in the body of the bank statements to identify the nature of the transactions.

To understand under which Bank Transaction Code these collections are reported on the statement, you typically need to carefully analyze some sample statement output or check with your bank’s implementation team for feedback.

Important to note here is to assign an algorithm to posting rule 2. This algorithm will attempt to search the payment notes of the bank statement for “reference numbers” which it can use to trace back the original customer invoice open item. Once SAP has identified the correct outstanding invoice, it can clear this one off and identify it as being paid.

If SAP is unsuccessful to automatically identify the open item, it can be manually post processed in FEBAN or FEB_BSPROC.

Transaction code OT83

3) Bank account assignment

In the last part, we can assign the posting rules assignments to the bank accounts. This way we can differentiate different rule assignments for different accounts if that is needed.

Transaction code OT83

4) Search strings

If the posting rule assignment needs more granularity than the level provided in step 2 above (on BTC level), we can setup search strings. Search strings can be configured to look at the payment notes section of the bank statement and find certain fixed text or patterns of text. Based on such search strings, we can then modify the posting behavior by for instance overruling the posting rule assignment as defined in step 2.

Whether this is required depends on the level of information that is provided by the bank in its bank statements.

Transaction code OTPM

Prepare IHC to parallel post certain bank statement items into IHC accounts

In IHC there are two ways to parallel post bank statement items into IHC accounts; as payment items or as payment orders.

This can be controlled by setting a specific function module on BTE2810. If we set function module “BKK_IHB_BASTA_IN_POST”, SAP will post an IHC payment item. If we assign “IHC_APPL_XBS_POST”, SAP will post an IHC payment order.

Additional information can be found in note 2370212.

In the subsequent part of the article we assume that we use the payment item logic.

Transaction BF42

IHC account determination from payment notes

In this section of the configuration we can determine which IHC account should be used to post the bank statement items towards using payment notes search strings.

For example, if the master account bank statement payment notes for VA collections for a particular VA contains a string “From VA 54353” and we know this belongs to IHC account “F4000EUR01”, we can setup a rule in this part of the configuration for that. This will ensure that all items on a bank statement containing this text string will get posted into IHC account F4000EUR01.

Maintenance view TBKKIHB1

Assign external BTC to posting category

Here we can identify the external banks BTC codes (NTRF, NCMZ a.o.) which are applicable for the VA movements to post into IHC. Secondly, we can identify with which posting category to post them into the IHC accounts.

Once we identified the BTC code related to our VA collections (e.g. NCMZ), we can link them to the correct posting categories here. You could use standard categories 90 (Balancing Ext. Acct (D)) for debits and 91 (Balancing Ext. Acct (C)) for credits.

Alternatively, you can setup and link your own custom posting categories here to more precisely control how our VA collections are posted into IHC. This is out of scope for this article though.

Importing and processing bank statements

We should now be in good shape to import our first statements. We could download them from our electronic banking platform. We could also be in a situation where we already receive them through some automated H2H interface or even through SWIFT. In any case, the statements need to be imported in SAP. This can be achieved through transaction code FF.5. The most important parameters to understand here are the following:

- File parameters: Here we define the filename and storage path where our statement is saved. We also need to define what format this file is going to be, i.e. MT940, CAMT.053 or one of the many other supported formats

- Posting Parameters: Here we can define whether the line items on the bank statements are going to be posted to general or sub-ledger.

- Algorithms: Here we need to set the range of customer invoice reference number (XBLNR) for the EBS Algorithm to search the payment notes for any such occurrence in a focused manner. If we would leave these fields empty, the algorithm would not work properly and would not find any open invoice for automatic clearing.

Once these parameters are maintained in the import variant, the system will start to load the statements and generate the required postings.

Transaction code FF.5 / FEBP

Display IHC account statement

Now that we successfully loaded an external bank statement, we can now check whether the items are posted into the IHC account. This can be done via transaction code F9K3. For each IHC account we can now look at the “Account Turnover” and observe all the VA collections that are posted on the account.

Transaction code F9K3

Prepare the IHC account for FINSTA statement distribution

We need to enable the distribution of internal IHC statements to the OpCo’s ERP on the IHC account master record. This can be achieved via F9K2. On the “Account Statement” tab we can adjust the statement format to “FINSTA” and dispatch type to “ALE” to ensure we are going to send FINSTA statements over an ALE connection. This would be the most common combination; other combinations can be configured and selected here as well.

Transaction code F9K2

Setting up ALE partner profiles

Finally, we can configure the system to determine to which system the FINSTA’s need to be send. This can be done in WE20, partner type GP (business partner).

Here we need to setup the outbound parameters for the FINSTA message type. An appropriate port needs to be selected that represents the ERP of the OpCo.

Transaction code WE20

Trigger the distribution of a FINSTA statement

Now that we have some transactions posted on the IHC account and the FINSTA settings enabled, we can trigger the system to send the FINSTA statements to the receiving ERP system. This can be done in F9N7.

Here we can select the correct IHC account and statement date and run the program to generate the FINSTA statement.

Once the finsta is generated and sent to the receiving ERP, it can be processed there via FEBP there.

Transaction code F9N7

Closing remarks

This is the third part of a series on how to set up virtual accounts in SAP. Please find below the other articles on this subject:

Intraday bank statement (IBS) reporting, a service that your house bank can provide your company, enables your cash manager to understand which debits and credits have cleared on your bank accounts throughout the current day. We explain how to implement it in SAP.

Intraday Bank Statements offers a cash manager additional insight in estimated closing balances of external bank accounts and therefore provides the information to manage the cash more tightly on the company’s bank accounts.

Compared to intraday bank statement reporting, end-of-day (EOD) bank statement reporting is only available the next calendar day. The information therefore always comes too late to be meaningful for cash management decisions – apart from providing an opening bank balance for the next day.

Business rationale behind IBS reporting

So, why would a Treasury typically start implementing IBS reporting in its cash management processes?

- Cash visibility: In general, IBS reporting will provide your cash management function an additional tool to improve cash visibility. Achieving cash visibility intrinsically might not be a goal of its own, but by achieving visibility, the cash manager now has information to make certain economically relevant decisions in certain situations.

- Managing cash: By creating cash visibility, we now have an opportunity to manage cash on our accounts in an intelligent way. In case we estimate a positive closing balance, we could decide to invest this surplus in, for example, a money market fund or overnight deposit to earn some return. In case of an expected deficit, we need to fund the account to ensure no EOD negative position happens. This can be achieved by transferring funds from another bank account (in same currency), swapping funds from another bank account (in different currency), or funding it from, for example, a facility drawdown.

- Reduced risk of delinquency: As we now implemented a process to increase control over our bank balances, we now have less chance of e.g. rejected payments due to insufficient available funds and therefore less chance of being delinquent on certain obligations to pay.

- Reduced requirements on overdraft facility: By reducing the chance of having insufficient funds on our account, the overdraft facility requirements can also be reduced.

- Timely clearing of open items: IBS can also be used to clear off open items throughout the day, as opposed to only rely on clearing from EOD statements. Benefit here is that KPI’s like days sales outstanding (DSO) will improve and that reconciliation effort is spread out more through time.

This article will now only focus on the cash management side; the IBS reconciliation process may be discussed another time. If you like to know more about bank reconciliation using intraday statements, feel free to reach out to us. We have a pre-developed solution that we can implement at your side.

IBS concepts

There are a few design considerations that need to be looked at before attempting to implementing this solution in SAP.

- Reporting formats: MT942, CAMT.052, BAI2 are formats that can be imported by SAP standard and are also supported by most banks to some degree. There may be some informational or structural benefits that one format has over the other which should be considered in the design.

- Reporting frequency: It is possible to agree with the bank on reporting frequencies of IBS. Ten times through working hours? Or one time only, half an hour before the payment cut-off time? In most cases, the bank will charge a fee for every statement it sends, so this should be considered in the design.

- Delta vs cumulative reporting: As it is possible for the bank to report multiple times a day, it is important to understand how the data is reported. There are two methodologies. In case of delta reporting, only new transactions are reported, relative to the previously distributed IBS. Alternatively, there is cumulative reporting, where all booked items are reported on the statement throughout the day. Delta reporting typically means that the data in your SAP system needs to be appended for every new IBS. Cumulative reporting means that every time you process an IBS in SAP, the data needs to be rebuilt completely.

- Data integration: The intraday data as provided by the bank needs to be integrated with already existing cash-relevant data to compile a proper reporting view of estimated closing balance for the day. This needs to happen in the cash management module of SAP (FF7* reports). The design of the structure of the cash management report should be carefully aligned with the liquidity structure (i.e. ZBA structure).

- Prevention of duplications: Integrating the intraday data with existing data should be designed with data duplication in mind. It is paramount that the data on the same cash movement is not counted twice from two sources and data duplication should always be prevented while designing the solution. For example, if we are not careful, a payment flow can be included in the report twice, once from the intraday statement when it is debited and once from the payment in transit GL in the SAP administration. This would result in a skewed estimated closing balance.

Ultimately, the goal here is to receive and upload intraday bank statements throughout the day and to load cash movement data into your SAP system. This cash-relevant data needs to be made visible through the cash management reports so that the cash manager can better estimate EOD balances and make intelligent decisions related to funding accounts or investing excess funds.

Setting up Intraday Bank Statement reporting in SAP

We will now go into detail on how to setup intraday statement reporting and assume that the basic FI-CO settings for e.g. the company code are already in place. We also assume that the EOD bank statement process has already been implemented. To learn how to set this up, please read this article on virtual accounts.

Cash Management

It is important to understand that intraday statement data is converted into so called ‘Memo Records’ once loaded in SAP. These memo records can be visualized in the cash management reports (FF7AN/FF7BN). We will now explain the necessary settings on the cash management report section to ensure that the intraday data can be made visible in these cash management reports.

Define planning levels

First, we need to define a planning level; a label that is assigned to all cash movements as reported on the intraday statement. The planning level is used to structure the data in the cash management reports.

The level is a two-digit label, freely definable. We set it to C1.

The sign we need to set to blank as cash movements reported on this level can be both positive and negative.

The source will be ‘BNK’. This ensures that this planning level is reported on both ‘cash position’ and ‘liquidity forecast’ in the FF7AN/FF7BN reports.

The descriptions are freely definable. We define it as ‘INTRADAY’.

Define planning types

A planning type is a label under which a ‘memo record’ is stored on the SAP database. A planning type is subsequently linked to a ‘planning level’ to ensure the underlying data can be visualized in the cash management reports.

First, we define the planning type label: we set it identical to the planning level; C1 and link it to planning level C1.

We need to define an archiving category. This defines the data retention period of the memo records. If the period is exceeded and the reorganization program is executed; the memo record data will be cleansed.

The auto-expiry option defines whether the memo record will expire automatically and becomes invisible in the cash management report output. This needs to be enabled. The idea here is that the intraday statement data will be superseded by the EOD statement data once this is loaded after midnight next calendar day. To ensure we do not double count identical cash movements from both sources, the intraday data needs to be expired.

Also, a number range and description need to be entered. No specific functional considerations are needed here.

Define grouping and maintain headers

A ‘grouping’ is a label that is used to structure the cash management report data in a meaningful manner for the user. The grouping can be selected in the cash management reports and is going to dictate how the data is shown to the user.

We will configure a grouping ‘CASHPOS’.

Maintain structure

Under the grouping we can now maintain the structure of the cash management data. For our report, we are including two components. The first component is the planning level., the second will be the GL account under which we record our bank account balances. This is the GL account we typically maintain in the house bank account data (table T012K, transaction FI13, NWBC).

For the first component we are going to add an entry as follows:

The grouping we set to ‘CASHPOS’.

The type we set to ‘E’ for planning level. Now we can define a planning level that is going to be relevant to our cash management report output.

We set the selection to C1 (our intraday planning level we defined earlier).

This setting will ensure all cash management data as stored under C1 planning level is going to be selected in the report output.

For the second component we are going to add an entry as follows:

The grouping we set to ‘CASHPOS’.

The type we set to ‘G’ for GL Account. Now we can define the bank GL account that is going to be relevant for our cash management report output.

The selection we are going to set to a GL account is saved in our bank account entry in table T012K.

This setting will ensure all cash management data as stored under the GL account and relevant for our bank account will be selected in the report output.

The combination of these two lines is going to ensure that we will only see the C1 data for our one bank account. We can add multiple lines to increase the scope of the reports output.

Importing and processing bank statements

We should now be in good shape to import our first intraday statements. We could download these statements from our electronic banking platform. Also, we could be in a situation where we already receive them through some automated H2H interface or even through SWIFT. In any case, the statements need to be imported in SAP. This can be achieved through e.g. transaction code FF.5. The most important parameters to understand here are the following:

- File parameters: Here we define the filename and storage path where our statement is saved. We also need to define what format this file is going to be; MT940, CAMT.053, or one of the many other supported formats

- Posting parameters: Here we can define whether the line items on the bank statements should be posted to general or sub-ledger. This section is not relevant for intraday statements, as SAP does not support GL postings and reconciliation from intraday statements out of the box.

- Cash management: This is the most important section, specifically for intraday statement processing. The fields and tick boxes control a few parameters:

- A/CM payment advice: This needs to be enabled to ensure that SAP creates the memo record data from the intraday statements.

- B/Summarization: This tick box controls whether a single memo record will be created for the whole delta balance as reported on the statement or for each reported debit and credit on the statement. If high volumes are expected, summarization can reduce the number of memo records and improve performance a bit. Obviously, it does reduce the data granularity.

- C/Planning type: Here we set the planning type under which the memo records are going to be recorded. In our sample we set this to C1.

- D/ Account balance: This needs to be set if we are loading intraday statements.

- Algorithms: Here we need to set the range of customer invoice reference number (XBLNR) for the electronic bank statement (EBS) algorithm, to search the payment notes for any such occurrence in a focussed manner. If we would leave these fields empty, the algorithm would not work properly and would not find any open invoice for automatic clearing. This section is not relevant for intraday statements as SAP does not support GL postings and reconciliation from intraday statements out of the box.

Once these parameters are maintained in the import variant, the system will start to load the statements and generate the required postings.

Transaction code: FF.5

Now we can check if the memo records are updated in table FDES.

Subsequently, we can check the FF7BN report for grouping ‘CASHPOS’ and observe the output.

International Financial Reporting Standard 9 (IFRS 9), introduced by the IASB in 2014 as the successor to IAS 39, became mandatory on January 1, 2018, affecting nearly all processes and systems, according to Paul Buijze of FMO, the Dutch development bank. How is this unique bank preparing for the change?

Since 1970, FMO has been investing in the private sector of developing countries and upcoming markets. It does this in sectors in which it believes the long-term impact will be the greatest: financial institutions, energy and agricultural sector. With regard to lending, FMO applies a number of criteria. Is the initiative bankable? Does it contribute to a better world? Is it dependent on FMO or can another bank do it as well?

IFRS 9 concerns a number of new accounting requirements for financial instruments and contains three pillars: classification and measurement of financial instruments, provision for possible credit losses on financial assets (impairment) and hedge accounting. The adjustments within the organization fall under the responsibility of the financial division, which is Buijze’s department. “As far as hedge accounting is concerned, the impact is not so relevant for us, but definitely for the other two,” says Buijze. For example, the rules require the bank to look at expected loan losses differently, including taking into account macroeconomic scenarios.

Auditable and executable

During the credit crunch, banks found that the value of assets or liabilities entered on the balance sheet were often too low. In addition, there was also a delay in adjusting the value in response to market developments. The idea that the value of assets or liabilities should reflect the market more closely only seems logical. The question, however, is whether this regulation will achieve this. “It probably will,” thinks Buijze. “But since it arose from a political discussion, it makes it that much more complex. In order to get a grasp on this complexity, we have appointed an external manager to this project. It affects every part of our organization and is a lot of work to not only process it through all the procedures, systems and reports, but also to make sure it is preserved.”

In 2015, FMO began to prepare at a relatively early stage. “That’s why we were able to take all the necessary steps in a constructive way,” explains Buijze. “That process started with the question: what exactly is IFRS 9 and what are we actually facing? After that we needed to verify which elements were already in place. The probability of default (PD), or the probability that a company will go bankrupt, was something we already had a good idea about. As well as the loss given default (LGD), which is loss through default. You need to build your entire framework on these basic elements. IFRS 9 requires a calculation of expected loss (EL) in the next 12 months. However, if the client’s creditworthiness deteriorates, you are responsible for the EL over the entire life cycle of that credit. But what does ‘deteriorate’ actually mean? Such things must be clear; it’s important that it’s auditable and executable.” That raises the question of how one determines the creditworthiness of a local bank in Zimbabwe, for example. No ratings exist for such a bank. Buijze says: “We do that with all the specialists here, through a ranking of the entire portfolio based on the estimated risks. So it’s a relative rating which we subsequently ‘map out’ from the well-known rating scores of Moody’s and Standard & Poor’s.”

Portfolio diversity

Compared with the Basel guidelines, IFRS 9 requires more a point in time, according to Martijn de Groot, director at Zanders. “We had to take a number of measures, especially when using the existing PDs as proof for IFRS 9. Nothing too major, but it must be well founded to obtain approval from the auditor and to be able to take part in the process.” Buijze nods in agreement, saying: “You have to thoroughly explain why certain decisions were made. A lot of banks have very specific problems. As a bank, we can’t do a lot of back testing because we have relatively few clients, and luckily we don’t lose many. To show the expected loss with only historical figures is difficult. You must also substantiate your findings theoretically.” FMO’s portfolio is much smaller but more diverse than that of the average bank. The balance sheet total exceeds €8 billion, with loans amounting to over €4 billion. However, this is distributed among approximately 700 clients in 80 countries.

“There are countries with a high-risk rating, where we’ve never lost a cent, although the expected loss is higher than zero,” explains Buijze. FMO’s expansive agriculture sector does have some consequences. De Groot says: “It means that you have to find a solution for everything for IFRS 9. Because the portfolio is so diverse, so are the effects. A life cycle or credit cycle needs to be modeled, but the FMO credit cycle, based on the total balance, is muted, less volatile, due to the diversity.”

Classification

In the world of FMO, modeling quickly results in highly theoretical levels, says Buijze. “There are no trustworthy figures from a lot of the countries in which we do business. How do you determine the credit cycle in Ukraine, for example? In any case, we try to find the balance: while complying with the standards of IFRS 9, we don’t want to fall into something which appears great in theory, but hardly relates to what’s happening in a country.” All financial instruments must be classified according to the IFRS 9 guidelines. On the liabilities side, there is no impact for FMO but there are implications for the bank’s financial assets. Buijze explains: “We have to separately determine the classification for each loan.” This classification means that loans are entered at cost price or at market value on the balance sheet. However, the market value decreases as the repayment capacity decreases. Because there is also an interest component, in addition to a credit component, the market value is more complex. “Luckily we haven’t needed to price that many loans at market value. We work with normal loans, mezzanine loans and private equity. And for the latter, very different rules apply.”

Fluctuations

One of the most miraculous things about IFRS 9, according to Buijze, is that you are obliged to make a choice for private equity investments. “Either everything goes through the balance sheet, so you never see anything in your profit and loss account (P&L), with the exception of paid dividends, even if you sell the investment at a nice profit, or everything goes through the P&L. That leads to some uncertainty, because valuations can fluctuate and are not always as accurate as possible. Consequently, you get huge fluctuations in your income statement. We finance

almost no listed companies, and should therefore, in valuation, mainly look at theoretical values based on what other companies are doing. If we finance a bank and all banks in that region are assessed at a lower value, then we will also asses the bank at a lower value. During the crisis, the large Dutch banks significantly decreased in value, while we were actually doing quite well. If FMO was valuated in the same way as ING at the time… Therefore, it is an approach, but it’s not spot-on. And that’s all because of your P&L.”