Providing possible technical solutions for CLS in SAP Treasury

Continuous Linked Settlement (CLS) is an established global system to mitigate settlement risks for FX trades, improving corporate cash and liquidity management among other benefits.

The CLS system was established back in 2002 and since then, the FX market has grown significantly. Therefore, there is a high demand from corporates to leverage CLS to improve corporate treasury efficiency.

In this article we shed some light on the possible technical solutions in SAP Treasury to implement CLS in the corporate treasury operations. This includes CLS deal capture, limit utilization implications in Credit risk analyzer, and changes in the correspondence framework of SAP TRM.

Technical solution in SAP Treasury

There is no SAP standard solution for CLS as such. However, SAP standard functionality can be used to cover major parts of the CLS solution. The solution may vary depending on the existing functionality for hedge management/accounting and limit management as well as the technical landscape accounting for SAP version and SWIFT connectivity.

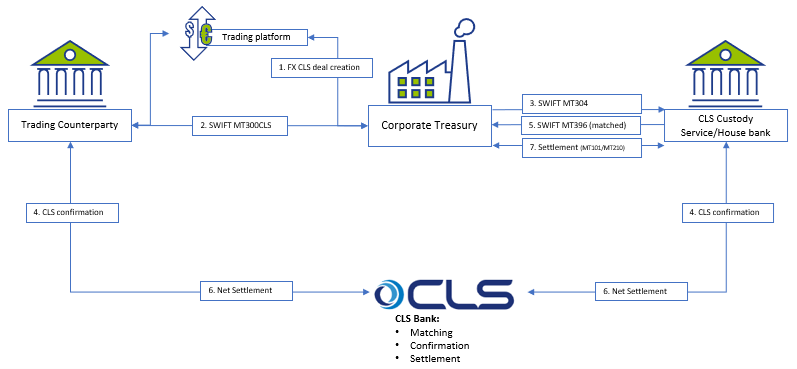

Below is a simplified workflow of CLS deal processing:

The proposed solution may be applicable for a corporate using SAP TRM (ECC to S/4HANA), having Credit risk analyzer activated and using SWIFT connection for connectivity with the banks.

Capturing CLS FX deals

There are a few options on how to register the FX deal as a CLS deal, with two described below:

Option 1: CLS Business partner – a replica of your usual business partner (BP) which would have CLS BIC code and complete settlement instructions.

Option 2: CLS FX product type/transaction type – a replica of normal FX SPOT, FX FORWARD or FX SWAP product type/transaction type.

Each option has pros and cons and may be applied as per a client technical specific.

FX deals trading and capturing may be executed via SAP Trade Platform Integration (TPI), which would improve the processing efficiency, but development may still be required depending on characteristics of the scope of FX dealing. In particular, the currency, product type, counterparty scope and volume of transactions would drive whether additional development is required, or whether standard mapping logic can be used to isolate CLS deals.

For the scenarios where a custom solution is required to convert standard FX deals into CLS FX deals during its creation, a custom program could be created that includes an additional mapping table to help SAP determine CLS eligible deals. The bespoke mapping table could help identify CLS eligibility based on the below characteristics:

- Counterparty

- Currency Pair

- Product Type (Spot, Forward, SWAP)

Correspondence framework

Once CLS deal is captured in SAP TRM, it needs to be counter-confirmed with the trading counterparty and with CLS Bank. Three new types of correspondence need to be configured:

- MT300 with CLS specifics to be used to communicate with the trading counterparty;

- MT304 to communicate with CLS Custody service;

- SWIFT MT396 to get the matching status from CLS bank.

Credit Risk Analyzer (CRA)

FX CLS deals do not bring settlement exposure, thus CLS deals need to be exempt from the settlement risk utilization. Configuration of the limit characteristics must include either business partner number (for CLS Business Partner) or transaction type (for CLS transaction type). This will help determine the limits without FX CLS deals.

No automatic limits creation should be allowed for the respective limit type; this will disable a settlement limit creation based on CLS deal capture in SAP.

CLS Business partner setting must be done with ‘parent <-> subsidiary’ relationship with the regular business partner. This is required to keep a single credit limit utilization and having FX deals being done with two business partners.

Deal execution

Accounting for CLS FX deals is normally the same as for regular FX deals, though it depends on the corporate requirements. We do not see any need for a separate FX unrealized result treatment for CLS deals.

However, settlement of CLS deals is different and standard settlement instructions of CLS deals vary from normal FX deals.

Either the bank’s virtual accounts or separate house bank accounts are opened to settle CLS FX deals.

Since CLS partner performs the net settlement on-behalf of a corporate there is no need to generate payment request for every CLS deal separately. Posting to the bank’s CLS clearing account with cash flow postings (TBB1) is sufficient at this level.

The following day the bank statement will clear the postings on the CLS settlement account on a net basis based on the total amount and posting date.

Cash Management

A liquidity manager needs to know the net result of the CLS deals in advance to replenish the CLS bank account in case the net settlement amount for CLS deal is negative. In addition, the funds would need to be transmitted between the house bank accounts either manually or automatically, with cash concentration requiring transparency on the projected cash position.

The solution may require extra settings in the cash management module with CLS bank accounts to be added to specific groupings.

Conclusion

Designing a CLS solution in SAP requires deep understanding of a client’s treasury operations, bank account structure and SAP TMS specifics. Together with a client and based on the unique business landscape, we review the pros and cons of possible solutions and help choosing the best one. Eventually we can design and implement a solution that makes treasury operations more efficient and transparent.

Our corporate clients are requesting our support with design and implementation of Continuous Linked Settlement (CLS) solutions for FX settlements in their SAP Treasury system. If you are interested, please do not hesitate to contact us.

-

Intra-Group Loans Transfer Pricing: What’s Important in H2 2026?

-

Key SAP Treasury and Cash Management Updates

-

SAP Analytics Cloud for Treasury Liquidity Planning

-

Preventing Payment Fraud with SAP Advanced Payment Management and Business Integrity Screening

-

SAP S/4HANA Treasury Business Partner Design and Maintenance

-

IFRS 9 Study 2026: Steady Coverage, Diverging Signals

-

Margin of Conservatism Explained: Reducing Capital Inflation in IRB Models

-

Cash Is King Again: Why real-time liquidity is the new strategic advantage

-

CEO Statement: Delivering Financial Performance When It Counts

-

The Digital Agenda Has Increased the Cybercrime and Fraud Threat Landscape – It's Now Critical for Corporate Treasury to Build Resilience