Ultimate Forward Rate: does it create more risk?

Since its introduction in 2012, there has been a great deal of debate about the merits of the Ultimate Forward Rate (UFR). The UFR makes insurers and pension funds less dependent on long-term interest rates and increases funding ratios. However, the recent studies by the Dutch Central Bank (DNB) and the European regulator EIOPA (European Insurance and Occupational Pensions Authority) illustrate that the UFR also brings with it new risks. Does the UFR spell the end of the practical problems associated with market-consistent valuation, or does it actually make them worse?

The UFR is a method of adjusting the market rate at which future commitments are discounted. Interests for durations of more than 20 years are adjusted by converging the one-year forward rate towards the Ultimate Forward Rate of 4.2%.

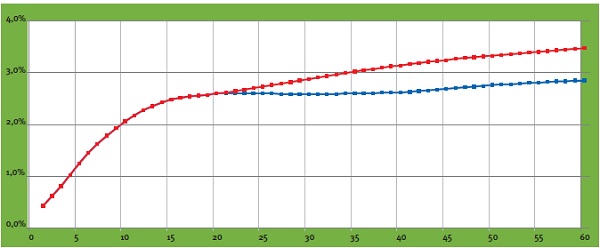

The introduction of the UFR was an attempt to address three problems. Firstly, as interest rates currently stand, applying the UFR has the effect of increasing rates with a maturity of 20 years or more (see figure 1). This causes the present value of long-term liabilities to fall, which means funding ratios and capital ratios rise. Secondly, the interest rate market for long maturities is assumed to be insufficiently liquid to permit a reliable market valuation, which means the value of liabilities may be very volatile.

Figure 1: Spot yield curve with UFR (red) and without UFR (blue) as of September 30, 2013

The third problem addressed by the UFR is the desire to escape the vicious circle which is created when interest rate risks are hedged. Due to demand among pension funds and insurers for swaps with long maturities, these interest rates are falling, necessitating further interest rate hedging and triggering a renewed rise in demand.

Risk management

The UFR, however, is raising questions about risk management by insurers and pension funds, who are required to use the UFR when valuing their liabilities in their regulatory reports. From a risk management perspective, however, there are important arguments against hedging interest rate risks on the basis of the UFR.

The UFR is not an economic reality: there are no instruments on the market which generate the same returns as the UFR-adjusted interest rates. Consequently, there is an imbalance between the value as reported to DNB and the available instruments on the market for managing the risks. Furthermore, the UFR is only applied to the liabilities on the balance sheet, and not to the assets. This creates a discrepancy between the economic reality of the assets and the ‘paper’ UFR reality of the liabilities. If a company’s assets and liabilities have identical interest rate profiles, the company does not run an interest rate risk; nonetheless, its UFR-based funding ratio does change in line with interest rate movements on the market. There is also greater interest rate sensitivity around the 20-year interest rate point: past this point, market interest rates are partially or entirely disregarded. Lastly, there is a political risk (which cannot be hedged) that the UFR method may be revised by the regulator – a fact underlined by recent developments.

Insurers and pension funds are compelled to keep two different sets of records: a ‘UFR report’ for the regulator and an economic version on which the interest rate risk is actually managed. Both records have their own, specific risks.

Insurers: debate and uncertainty

Understandably, the UFR has created quite a furor among insurers. In June 2013, EIOPA published the results of a survey of insurers who offer long-term guarantee products. Interestingly, EIOPA acknowledges in this publication that the UFR entails significant risks. Potentially, the UFR could mislead regulators, meaning that any action is taken too late. Moreover, the design of the UFR – specifically, the speed at which the forward rate converges towards the UFR – has long been a source of uncertainty. EIOPA advises using what is known as the ‘20+40’ convergence (whereby market interest rates are used up to and including 20 years and, 40 years later, the forward rate has converged to the UFR). Both insurers and the European Parliament, however, are pressing for a switch to a ‘20+10’ convergence.

Proponents of this shorter convergence period point to the lower sensitivity to shocks in (long-term) market interest rates, which would help stabilize the valuation of liabilities. One drawback of a short convergence period is the increased volatility of own funds. This is because the assets are discounted at market interest rates and are sensitive to changes in interest rates, whereas the liabilities are not. Moreover, the potential impact of a change in the level of the UFR is greater when the convergence period is shorter.

While the debate continues among European insurers, DNB has already compelled Dutch insurers to use the UFR. In so doing, DNB is largely taking its cue from EIOPA’s latest advice. However, there is a high risk that the convergence period will change in the definitive Solvency II legislation, meaning that, eventually, insurers will have to switch to a different UFR.

Pensions: DNB is pursuing its own course

The UFR committee

In October 2013, the UFR committee advised the Dutch cabinet to abandon the current method for pension funds, which involves a fixed UFR of 4.2%. The committee advises using the UFR as an ultimate rate, based on the average forward rates of the last 120 months, with an infinite convergence period.

The UFR will then become a moving target based on current market rates. As things currently stand, this would mean a UFR of 3.9% – which is significantly different to the current UFR.

The cabinet informed the UFR committee in a response that the recommendation of applying a moving target UFR will be implemented from 2015 onwards. This will only accentuate the contrast between Europe and the Dutch pension landscape. In addition to an economic report and the current UFR report, it will compel pension funds to also prepare an adjusted UFR report for 2015.

The situation as regards pension funds illustrates the political risk. Following criticism in Dutch academic circles about the high sensitivity affecting the 20-year forward rate, DNB adapted the rules specifically for pension funds. These funds must now continue applying the forward rate past the 20-year point (with fixed weightings) and the spot rates are averaged over the last three months.

Since then, in its advisory report, the UFR committee has proposed a completely new calculation method (see insert), which may have a big impact on funding ratios. It is not inconceivable that, if the yield curve fluctuates significantly, the UFR will yet again be changed. In addition, there are also long-term risks to be taken into account. The UFR could potentially create discrepancies between the pension entitlements of current and future pensioners.

The higher funding ratio resulting from the application of the UFR reduces the likelihood of increases in contributions and cuts to pensions at the present time – which is an advantage for current pensioners. If, however, the yield turns out lower than assumed, future pensioners will have fewer funds at their disposal. Potentially, therefore, pension rights may end up being transferred from younger to older generations.

Conclusion

The EIOPA study and the UFR committee illustrate that the introduction of the UFR has made the world of insurance more complex. In risk management terms, it has created two landscapes and it is not yet clear exactly what the UFR landscape will look like. From an economic perspective, the majority of risk managers will give priority to hedging risks. To prevent interference by the regulator, however, the UFR value must always be closely monitored. Furthermore, the impending change to the UFR method for pension funds reaffirms that the political risk is a significant, unmanageable factor.

-

CEO Statement: Delivering Financial Performance When It Counts

-

New challenges for banks’ ESG strategy and risk management

-

Debt Capacity Made Easy with our Latest Transfer Pricing Solution

-

Intra-Group Loan Transfer Pricing: What’s New in 2025?

-

Insights into XVA Calculations: How to Harness the Power of Neural Networks

-

Unlocking Value Through Foreign Exchange (FX) Risk Management: A Blueprint for Private Equity

-

PRA regulation changes in PS9/24

-

How BCBS 239’s RDARR Principles Can Strengthen Risk Data Aggregation and Reporting in Financial Institutions

-

Converging on resilience: Integrating CCR, XVA, and real-time risk management

-

Calibrating deposit models: Using historical data or forward-looking information?