Time to brush-up your bank’s IRRBB framework

Regulation on interest-rate risk in the banking book (IRRBB) is evolving after being somewhat overlooked in recent years. Banks are now updating their interest-rate risk frameworks and have important choices to make on the design of a new IRRBB framework: what are the risk types that need to be covered and how can a value and earnings measure be created? Nonetheless, this process provides an excellent opportunity for improving regulatory compliance as well as reviewing a financial organization’s benchmarks and best practices.

After a long period of limited regulatory attention for interest-rate risk in the banking book (IRRBB), the subject has moved up the regulatory priority list in the last couple of years. Maybe this is the result of the low interest-rate environment or because an update on the subject was long overdue.

After a long period of limited regulatory attention for interest-rate risk in the banking book (IRRBB), the subject has moved up the regulatory priority list in the last couple of years. Maybe this is the result of the low interest-rate environment or because an update on the subject was long overdue.

It still came as a bit of a surprise when the European Banking Authority (EBA) published an update of their 2006 guidelines in May 2015. The Basel Committee on Banking Supervision (BCBS) was known to be working on an update of their standards too and it is quite uncommon for the EBA to front-run BCBS standards.

When the BCBS standards were finalized in April 2016, the industry was relieved that the regulator did not opt for a Pillar 1 approach for IRRBB (leading to standardized minimum capital requirements), but chose to capture IRRBB as part of Pillar 2 (where the supervisor can tailor capital requirements to the [heterogeneous] IRRBB profile of banks).

All the recent regulatory attention has caused the subject to be high on the agenda of the management board of many European banks. Consequently, IRRBB policies and governance are being reviewed and updated to align them with regulatory requirements, while the measurement of interest-rate risk is also being enhanced. This includes enhancements to the models used to measure interest-rate risk as well as to the Risk Appetite Statement (RAS), which brings it all together.

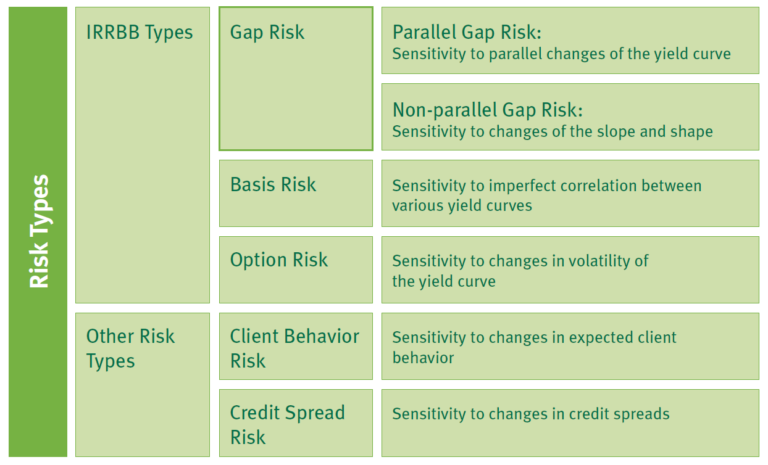

Important choices are to be made in the update of an IRRBB framework: the main ones concern the scope and the balance between the value and earnings perspective.

With respect to the former, the traditional approach was to measure interest-rate risk through a parallel shift of the yield curve. It is clear that this is no longer sufficient and that several other risk types (e.g. non-parallel, basis and optionality risks) should be consistently included in the framework as well.

With respect to the latter, the EBA guidelines and BCBS standards state that interest rate risk needs to be measured both through a value and an earnings perspective. These metrics show two sides of the same coin, but cannot be optimized at the same time.

IRRBB appetite and scope

One of the first decisions in setting up an IRRBB framework is to determine the appetite for both value and earnings risk. This appetite is set in terms of the value and earnings a bank is willing to lose in a pre-determined adverse scenario.

As a first step, typically a parallel scenario is selected for this. The appetite can then be translated into risk limits and one of the common metrics for this is the duration of equity. The appetite for earnings and value risk usually introduces a duration interval in which the balance sheet can be optimized. This poses the question of how this optimization should be achieved.

If a bank aims for low volatility in value, the duration of equity should be low. That, however, will come at the cost of increased earnings volatility. As the majority of the banking book is accounted for at amortized cost, the only way for the profit and loss (P&L) of a bank to be hit is through a loss in earnings. Aiming for low earnings volatility instead of low value volatility therefore seems a more sensible option.

Managing the banking book through the duration of equity also has its shortcomings as it only covers linear interest-rate risk. As already discussed in the introduction, other risk types should also be included in the risk appetite. The difficulty in setting a risk appetite for those types is that it is challenging to create scenarios that cover only the additional risk types, as scenarios usually exhibit some overlap.

The three main additional risk types to be included in a bank’s RAS are:

Non-parallel gap risk

This determines how exposed a bank is to a steepening, flattening or rotation of the curve. Especially when a bank has a duration mismatch between its assets and liabilities it is expected to have an exposure to non-parallel gap risk.

Basis risk

With parallel and non-parallel gap risk, it is usually assumed that all yields in a specific currency move together; this assumption is relaxed in basis risk. Basis risk comes in multiple forms, the most apparent ones being tenor, currency or reference curve basis risk.

Optionality risk

Optionality risk can be included in the framework in different ways. If the cash flows used to calculate the value or earnings risk do not reflect the interest-rate risk dependent behavior of options, this dependency should be reflected here.

This approach aligns with the BCBS standards. It also makes sense, however, to change the interest-rate dependent cash flows when measuring the parallel and non-parallel risk.In that case, the option risk is already captured. In addition, it could be considered to measure the exposure to changes in the volatility of interest rates, especially if interest-rate risk dependent models are used.

Two other risk types that are very much related to IRRBB and that can be captured in the same framework are credit spread risk (in the banking book) and client behavior risk.

The latter measures the sensitivity of value and earnings to unexpected client behavior. The interest-rate risk dependent behavior of options is measured under gap risk or optionality risk and concerns the expected client behavior in, for example, mortgage prepayments.

This expected client behavior is estimated through a model, but the actual behavior will likely differ from the model outcome. Client behavior risk measures this model error. The former, credit spread risk, measures the sensitivity of value and earnings to changes in credit spreads. In general credit spread risk is only measured for the limited part of the banking book that is not accounted for at amortized cost.

When the scope and the appetite for all risk types in scope of IRRBB are determined, the next step is to measure the value and earnings risk.

Value risk

The main challenge in measuring value risk is the approach to determine the value. If, as a starting point, the cash flows and discounting must align, two approaches can be considered:

The first approach we call the ‘pure interest-rate view’, as it only covers the interest-rate component of the cash flows (thus excluding margins and other spread components) and discounts those at the risk-free rate.

This approach aligns well with the way the banking book is managed: the interest-rate risk can easily be hedged and the margin that remains is considered a constant income flow.

Furthermore, it aligns with the way the regulator wants interestrate risk to be disclosed through the economic value of equity (ΔEVE) and how it is limited by means of the standard outlier test. The base valuation that is used to calculate the at-risk numbers is difficult to interpret, however, as it does not link to a market value at all.

The second approach addresses this shortcoming and aims to measure value risk through a mark-tomarket valuation. In this approach, all cash flow components are discounted against a curve that includes margins and other spread components.

This is easier said than done, as for illiquid products, such as savings or mortgages, a market value is not directly available and therefore needs to be estimated based on a model. Taking the second approach implies that the value risk of the banking book’s margin is also captured by the risk measure. As that risk will generally not materialize, one may consider not using this measure as the basis for hedging the interest-rate risk.

Finally, it is important to realize that the resulting duration of equity differs for the two approaches. Consequently, the limit setting will depend on the choices made here. This interplay with setting the RAS should be carefully managed.

Earnings risk

Earnings metrics have increased in popularity in recent years as they better align to the way the banking book is accounted for. Contrary to value risk, no regulatory limits are imposed on earnings volatility and only recently has the BCBS added the disclosure of earnings risk to the standards. While the measurement of value risk is relatively straightforward, with only a limited number of options to model the risk, the measurement of earnings volatility comes with a whole range of parameters that need to be set.

The first decision is on the scope of the earnings measure; will this be a true earnings at risk (covering the entire impact of interest-rate risk on the P&L) or will it only cover interest-rate income and expenses? The latter is often referred to as a net interest income at risk (NII-at-risk), where the former will also include interest-rate dependent commissions and fair value changes in the banking book that have impact on the P&L.

One of the main features of an earnings measure is that it attempts to forecast future earnings. This requires a forecast both of the balance sheet and the interest-rate term structures. Forecasting the balance sheet makes most sense if it aligns with the corporate planning process, where a projection of future earnings is made as well.

Alternatively, it is possible to assume a static balance sheet and although this is prescribed in the BCBS standards, it is not preferred to use this for internal measurement.

For forecasting interest rates, several options exist as well. It is possible to align with the forward interest rates; just use the current interest rates as a future projection or use the forecasted rates that have been used in the corporate planning. Again, the latter makes most sense for internal management.

A final decision is on the forecasting horizon. Not too long ago, most banks calculated earnings risk using a one-year horizon. Extending the horizon to two or three years and defining limits on those longer horizons is a trend, but also comes at an increased dependency on forecasting assumptions. Furthermore, a bank should consider upfront how it can manage its earnings risk in case of limit breaches.

Regulatory requirements

The regulatory requirements with respect to the management of IRRBB are still evolving. Both the EBA guidelines and the BCBS standard list explicit requirements with respect to the use of both value and earnings-based measures.

For a start, banks are required to define their risk appetite, measure their IRRBB, and report on IRRBB, using both perspectives. It is stressed that the two perspectives are complementary, because of their differences in terms of outcomes, assessment horizons and balance sheet assumptions that have been discussed in this article. More detailed requirements with respect to the calculation of value and earnings-based measures are also included in the BCBS standard, to facilitate the comparability of the IRRBB reported by banks.

The BCBS expects banks to implement their latest standard by 1 January 2018 and so far it is expected that the EBA and FINMA (the Swiss regulator) will demand the same timelines for the upcoming update of their guidelines. Due to these evolving regulatory requirements, many banks are currently updating their IRRBB framework.

Such a process is an excellent opportunity to not only aim for regulatory compliance, but to also benchmark your bank’s IRRBB framework to best-market practices.

Quick Scan

Zanders uses its IRRBB Quick Scan to assess your bank’s IRRBB framework. Based on a review of available model documentation, risk reports and interviews with your bank’s risk specialists, the scan provides an independent and objective assessment of your bank’s IRRBB implementation relative to the new IRRBB principles and best-market practices. After having assessed all principles and accompanying requirements, Zanders will state to what extent your bank’s IRRBB framework is compliant with the regulatory requirements.Per IRRBB principle, Zanders will indicate whether your bank’s IRRBB framework is above, at or below the new minimum standards of the BCBS. For the areas of the IRRBB framework that do not meet the minimum standards, recommendations will be presented in the report (including a level of priority that accounts for proportionality and materiality).

-

Margin of Conservatism Explained: Reducing Capital Inflation in IRB Models

-

Cash Is King Again: Why real-time liquidity is the new strategic advantage

-

CEO Statement: Delivering Financial Performance When It Counts

-

The Digital Agenda Has Increased the Cybercrime and Fraud Threat Landscape – It’s Now Critical for Corporate Treasury to Build Resilience

-

The New Rails: How Stablecoins Are Redefining Cross-Border Payments for Corporate Treasury

-

Risk Mitigation Accounting (RMA) Exposure Draft amending IFRS9: Key Impacts and Practical Challenges

-

Optimizing the Valuation Processes in Modern Banking: A Strategic Approach to Efficiency, Consistency, and Cost Reduction

-

Intra-Group Loans Transfer Pricing: What’s Important in 2026?

-

A Roadmap for Banks to Geopolitical Risk Taxonomy

-

Geopolitical Risk and the ECB 2026 Reverse Stress Test: Mapping Failure Pathways Before It’s Too Late