Six years after the introduction of IFRS 9: Where do we stand?

This article describes the current status of the IFRS 9 landscape, six years after the IFRS 9 accounting standards replaced IAS 39.

We touch upon the main difficulties experienced by financial institutions in the Netherlands based on a combination of project experience, results of a survey, main attention points from the eyes of the regulator and observations from publicly available annual reports. Interested to learn more about the IFRS 9 framework components banks struggle with the most and whether these challenges can be easily solved? Find out in the remainder of this article.

Introduction

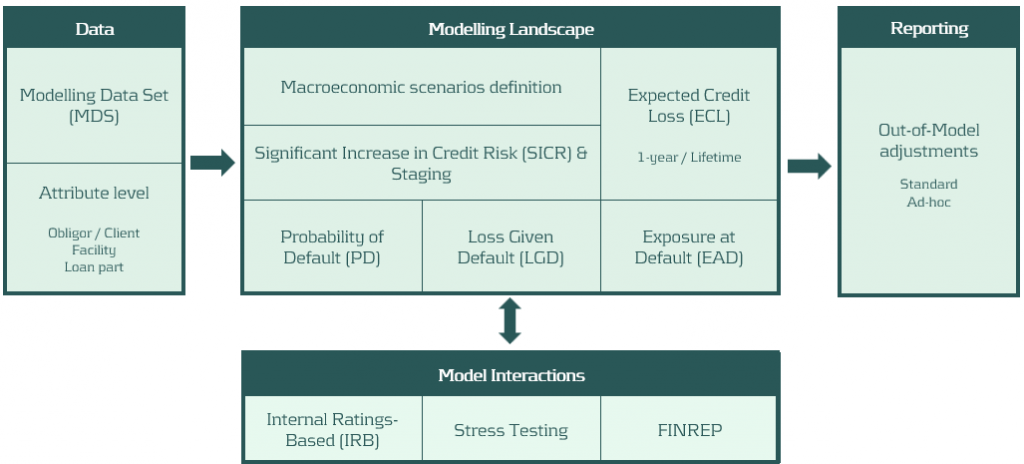

The main objective of this article is to provide insight into market practices and common challenges within the IFRS 9 landscape of Dutch financial institutions. In this light, Zanders conducted a survey amongst Dutch financial institutions. Six main IFRS 9 framework components form the basis of the survey: data quality, model components (PD, LGD, EAD), SICR & staging, macroeconomic scenarios, out-of-model adjustments and the relation between IFRS 9 and other models within the bank. An example of a full IFRS 9 framework overview is presented in Figure 1. The questionnaire was followed up by a roundtable in which the most noticeable results from the survey were discussed with the participants.

Besides the survey, the IFRS 9 monitoring report published by the European Banking Authority (IFRS 9 Monitoring report, EBA (November 2023)) provides insights into the key IFRS 9 attention points from a regulatory perspective (e.g. as identified by EBA). In this article, we discuss the key differences between the difficulties experienced by banks versus attention points highlighted in the monitoring report. Lastly, this article uses publicly available information from annual reports to illustrate the diverging modeling practices and model behavior amongst market peers.

Figure 1: IFRS 9 framework overview.

Survey

The IFRS 9 survey held in Q4 2023 was centered around the six framework components as stated in the introduction section and which are graphically presented in Figure 1. The participating banks were asked in which areas of the framework they experience difficulties. Consequently, each area was explored deeper by means of questions directly related to each area.

All participating banks except one indicate difficulties in the areas of data quality and out-of-model adjustments (e.g. overlays). For data quality, changing policies (e.g. Definition of Default, loan quality assessment), limited loss realizations for LGD (as well as limited detail of the loss realization data) and dealing with unrepresentative data from the Covid-19 period are examples of reasons for the difficulties experienced in this area. With regards to out-of-model adjustments, it becomes apparent that many banks struggle with pressure from the regulator and audit, triggering banks to find an escape in overlays on the IFRS 9 model outcomes. Overlays are applied on a wide variety of topics, in various ways (e.g. calculated, constant, periodic, expert based, etc.) and sometimes constitute the majority of the total provisions. Altogether, this illustrates the need to have out-of-model adjustments in place that are sufficiently qualitatively substantiated and, whenever possible, are applied on the model component level. At the same time, we are of the opinion that out-of-model adjustments are sometimes over-used to make up for model deficiencies. Especially when out-of-model adjustments constitute the majority of the total provisions, compliance of the model with the IFRS 9 best-estimate principle should be questioned.

Surprisingly, only one third of the respondents experiences difficulties in the framework areas that came into existence with the introduction of IFRS 9; SICR & staging and macroeconomic scenarios. A possible explanation for this is that the responsibility for these framework areas is often distributed across multiple departments. Macroeconomic predictions and scenario weights are usually determined by a separate macroeconomic scenario department or committee, and staging assessments are often placed outside the scope of IFRS 9 modeling teams. From a governance perspective, we are of the opinion that more alignment over the full IFRS 9 provisioning chain is desired.

Want to know more about the survey results? Download our white paper.

Regulatory view

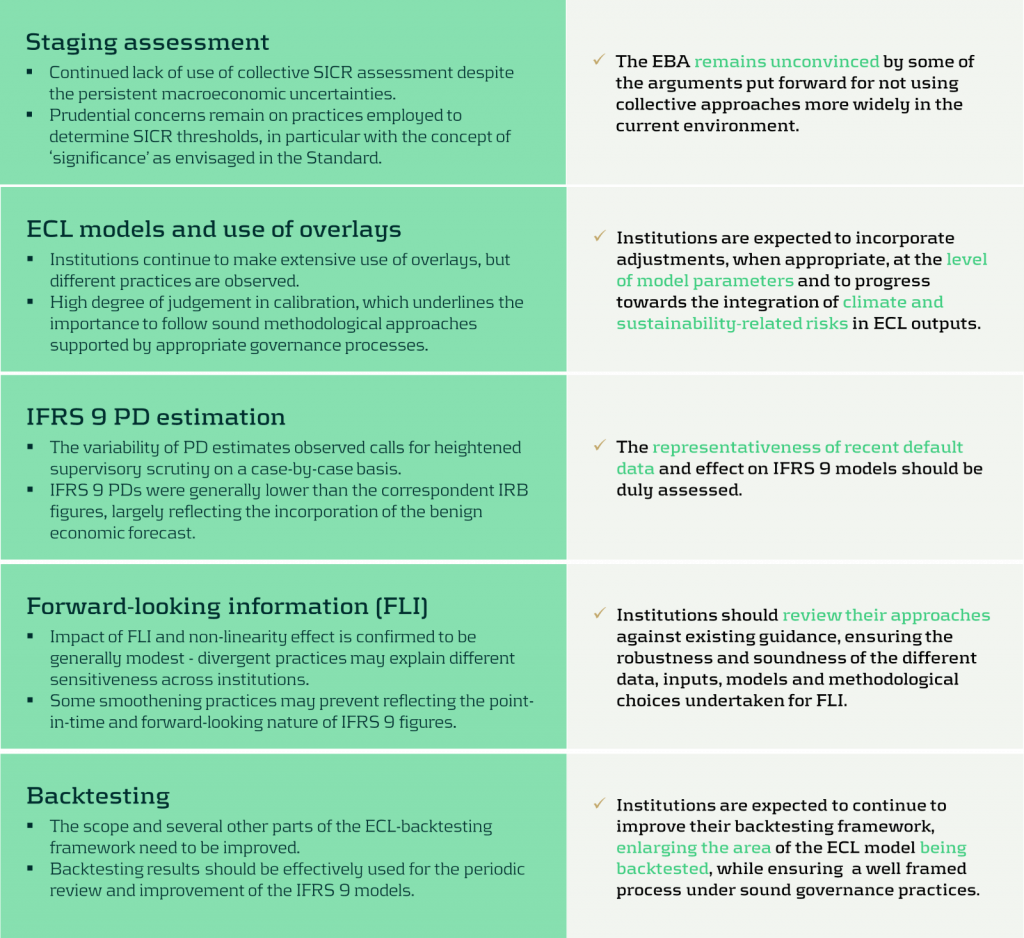

The EBA published a monitoring report in November 2023 on the current status of the IFRS 9 model landscape (IFRS 9 Monitoring report, EBA (November 2023)). In this report the EBA highlights several takeaways, which are shown in Figure 2. One of these takeaways is the manner in which SICR is modelled at the moment. The EBA is not convinced that non-collective approaches are more suitable than collective approaches. In the results of the survey however, it was shown that most respondents did not indicate SICR as one of the main challenges in their IFRS 9 landscape. This raises the question whether banks in the Netherlands are aware of the EBA’s remark on the current SICR approaches, or whether Dutch banks are outliers when it comes to the SICR modeling approaches.

Furthermore, the report indicates that out-of-model adjustments should be applied on the model parameter level and not on the outcome level. During the roundtable it was discussed that several participants recognize this desire from the regulator, but that they still apply it on the outcome level because the available data only allows for this level. This discrepancy could lead to further scrutiny from the regulator in the near future.

Figure 2: Key takeaways from the IFRS 9 monitoring report (EBA, 2023).

Annual report study

In the Dutch banking market, a variety of modeling practices is observed when it comes to IFRS 9 models for calculating credit loss provisions. Besides gaining insights into these IFRS 9 modeling practices via a survey, annual reports are analyzed to identify potential differences (or similarities) from information that is publicly available.

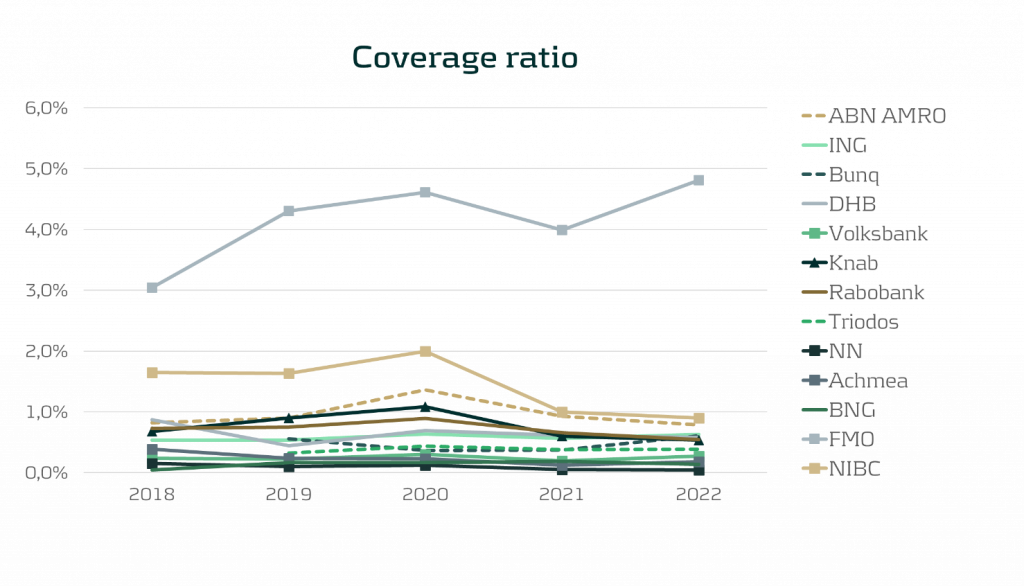

One of the observations from comparing annual reports is that no common level is observed for the Provisioning Coverage Ratio (PCR), i.e. the percentage of funds set aside for covering losses due to bad debts. Characteristics such as portfolio type/composition and loan maturity likely explain these differences. In 2020, almost all banks show an increase in the PCR due to increased allowances in response to the Covid-19 pandemic. Note that this was not necessarily caused by models picking up changing macroeconomic dynamics, but because of model overlays. PCR levels stabilized again in 2021 and 2022.

Figure 3: Coverage ratio over the years 2018 till 2022 . All results were gathered from public annual reports.

Although not all banks report macroeconomic scenario weights in their annual reports, it is worth noting that large differences exist in the scenario weights of banks that do report these figures. Especially weights assigned to the up and down scenarios vary significantly. In 2022, the weight percentage for the base scenario is generally between 40% and 60% (one bank uses a weight of 30%), whereas the weight percentage for the down scenario ranges from 20% to 60%. For the up scenario, percentage weights differ from 2% to 30%. It must be noted that the scenario weights cannot be judged without considering the actual scenario definitions/severity. Nonetheless, the wide variety in scenario weight percentages as well as large differences in the development of these scenario weights over time raises questions on the accuracy of macroeconomic predictions. In addition, it also complicates the comparability of IFRS 9 figures amongst banks.

What can Zanders offer?

We combine deep credit risk modeling expertise with relevant experience in regulation and programming:

- A Risk Advisory Team consisting of 75+ consultants with quantitative backgrounds (e.g. Econometrics and Physics);

- Strong knowledge of IFRS 9 models and developments in the IFRS 9 landscape;

- Extensive experience with calibration, implementation and validation of IFRS 9 models;

- We offer ready-to-use Expected Credit Loss models, Credit Risk Academy modules and expert sessions that can be tailored to the needs of your organization.

Interested to learn more? Contact Kasper Wijshoff or Michiel Harmsen for questions on IFRS 9.

-

CEO Statement: Delivering Financial Performance When It Counts

-

Risk Mitigation Accounting (RMA) Exposure Draft amending IFRS9: Key Impacts and Practical Challenges

-

IFRS 9 Amendments: Settlement-Date Accounting and the End of Distorted Liquidity Positions

-

Annual IFRS 9 Study 2025: Key Developments in the Dutch Banking Sector

-

IFRS 9 – Annual Report Study

-

How BCBS 239’s RDARR Principles Can Strengthen Risk Data Aggregation and Reporting in Financial Institutions

-

Converging on resilience: Integrating CCR, XVA, and real-time risk management

-

Calibrating deposit models: Using historical data or forward-looking information?

-

Basel IV and External Credit Ratings

-

Regulatory exemptions during extreme market stresses: EBA publishes final RTS on extraordinary circumstances for continuing the use of internal models