Regional optimization in times of corona

Treasury optimization in Asia, Part III

Just as growing companies plan to expand their operations internationally, corporate treasurers seek to identify new opportunities and take on challenges. The two seem to go hand in hand, as new challenges and difficulties materialize around every corner. Certainly the most daunting challenge that the global economy has been presented with recently is the COVID-19 outbreak. The recent outbreak represents a global health emergency and the biggest challenge the global economy has faced in over a decade. The fact that very few saw it coming highlights the shortcomings companies, even successful ones, can face.

In previous articles on Treasury optimization in Asia, we focused on the Treasury and Risk Maturity model, the three optimization phases and how to achieve local optimization for corporate treasuries in the foundation stage in Asia before the contagion had occurred. In this article, we continue to explore Asia, but also look at corporate treasuries (in the developing stage) seeking regional optimization and how regional treasury centers (RTC) can offer a solution as the coronavirus impacts the global economy.

According to an article in the Financial Times , based on data made available by the UN trade and development body (Unctad), Asian economies will grow to be larger than the rest of the world economies combined by 2020. As such, corporate treasurers should actively seek to mitigate risks and seize opportunities to improve their treasury operations in Asia where, as the impact of the contagion has underlined, the economies in the region are well connected.

Potential challenges of international operations range from:

- Regulatory requirements.

- Restricted countries.

- Access to liquidity markets.

- Local bank relationships.

If not properly addressed, these challenges can have financial consequences that will negatively impact the business. Therefore, to manage a company’s international operations effectively from a treasury perspective, one should decide which approach is best suited to managing operations within the region. This needs to be balanced with maintaining the agility to proactively manage unexpected global disruptions, such as the many consequences of the current pandemic.

For large multinational corporations (MNCs), which see Asia becoming increasingly important for their global trade, and Asian firms that have expanded well beyond their home market, both should seek to optimize operational efficiency, mitigate risks through concentrating activities and optimize capital through centralized liquidity management by setting up a regional treasury center (RTC). The challenge is to do that and still remain agile.

Considerations when setting up an RTC in Asia

MNCs have traditionally operated Shared Service Centres (SSC) in Asia because markets in the region were perceived as attractive locations for such ventures. As the Asian economy continues to grow, both global MNCs and Asian companies view the region as top of the list for establishing or expanding strategic RTCs.

According to a 2015 report by Reuters , about half the foreign or Chinese companies based in Hong Kong have set up regional centers that carry out treasury operations. In excess 12,000 European and US companies have set up an RTC in Singapore. With a diverse marketplace, regulatory conditions, market infrastructure and practices, business conventions, cultures, languages and currencies that differ across markets, a number of these traditional business issues must still be considered when entertaining the idea of setting up an RTC in Asia.

Added to that, now as the pandemic unfolds, we could see a restructuring of operations to move closer to the end users. This would require more regionalized centers, increasing the need for digitization and treasury technology to support the regional operations. This would increase agility, but companies still need to allow for a globalized approach, supported by a treasury management system (TMS) that provides global visibility on a regional basis.

A few key enablers can be identified for setting up an RTC, ranging from the introduction and implementation of (treasury) technology, policies and cash pooling, to bank account structures supported by banking tools and a TMS. Changing the treasury framework and reporting structures can also be beneficial.

Long-term view

If a treasury department is to support the organization in its quest for continuous future growth, it needs to adopt a corresponding view. This means it cannot treat the launch of an international subsidiary as a singular event. Future expansion and consistent growth are key elements in the creation of a sustainable perspective, with policies and structures that are scalable and can be easily aligned to an RTC’s operations as the company continues to grow. The organization must, therefore, adopt a long-term view.

That said, it is also important to remember that a long-term view is constantly subject to the set of circumstances in which the company finds itself. In other words, it will need to be re-visited and to evolve over time as the organization grows and changes.

Fast-tracking the process of digitizing the treasury organization can be a benefit here, as it will allow the treasurer to not only react but, in some cases, even proactively adjust course to mitigate the impact of disruptions on their organizations.

Operating within Asia requires treasurers to navigate an ever-changing sea of regulatory requirements, driven by unmatched economic growth. A sound long-term view and approach are vital when considering an RTC.

Strategy

With treasury’s role becoming more strategic, treasurers are frequently called on to provide sound international strategy, navigate local policies specific to situation and regulation, manage technological advancements and maintain a long-term view. As the world enters uncharted territory, regulatory changes might become even more prevalent, as governmental responses to the outbreak may require businesses to maintain certain levels of inventory and production quotas, for example.

It is important that the needs and objectives are correctly addressed from treasury’s perspective, and a seat at the executive table is therefore paramount when establishing regional objectives and policies. What is more, this should interlink with the objectives of the corporation’s TMS in its home country. From our experience, we know that companies encounter issues regarding centralization, governance, bank relations and FX policies, among others.

The extent of centralization is highly important for the overall strategy. The level of centralization that suits an organization can be driven by trade-offs when it comes to local banking and regulations, responsibilities and regional autonomy. Ideally, one consolidates the treasury function under a global treasurer and works from an operating model and infrastructure that aligns the diverse corporate activities. This assures that local treasury groups are able to respond quickly in a volatile market and uphold their reporting capabilities.

These corporate activities can be split into:

- Strategy – determine funding, growth and business model strategy.

- Scope – identify and allocate functions and operations.

- Processes – design operational, tactical or strategic processes.

Depending on the level of treasury maturity, this may not always be feasible. Some companies’ treasury departments have become so mature and efficient that they are considering taking it a step further, closing regional RTCs and further centralizing to a single treasury center. Depending on the level of maturity, complexity (compliance, regulations and local banking), tax, funding requirements and achieved levels of efficiency, an RTC may still be a viable option if an organization has not yet reached that level of maturity. But once again, the current pandemic may have an impact here. As the world takes on the coronavirus, chosen strategies may need to be revisited. It may have even become a more viable option to decentralize from a global treasury center to multiple regional treasury centres to reach the required levels of agility.

Governance and controls within a treasury department must be reinforced during global expansion into developing regions. Given the many financial instruments and accounts that the department has access to, measures to counter fraud and mismanagement must be put in place. This requires a thorough examination of current policies and processes for the core responsibilities, followed by comprehensive testing to verify that they apply properly to realistic situations.

Different regions may have alternative requirements for establishing bank relationships, making the opening and structuring of bank accounts a challenging task. The strategic outset of the company in terms of bank relationships should be closely adhered to when managing these relations. The best course of action in such cases is often to work with someone who has experience in these regions and attribute a specific professional and dedicated staff to manage the entire process.

When working with various currency markets within an organization, it is important to consider the different regulatory requirements that may apply per country. It is possible to draw up a single global FX policy for the entire company that can then be modified to meet region-specific needs. This approach will keep priorities aligned with the company’s central view while also leaving flexibility to help control region-specific situations and support further decentralization, if required. Such cases include dealing with cash sweeps, cross-border payment flows, handling inter-company payments and repatriation of profits. Developing a global policy may prove difficult and considering a risk management framework as the basis of the treasury department’s policy may help in providing clarity in the decision-making process.

Technology and infrastructure

Technological considerations become more important as the assumptions held in the past are now challenged by the contagion. Structural changes become inevitable. International expansion increases the need for reliable reporting, sending and receiving messages and risk management. During the expansion phase, it generally becomes apparent that an enterprise resource planning (ERP) system or a TMS offers greater adequacy than the use of spreadsheet reporting. What is required is always dependent on the RTC’s final scope.

Although powerful, spreadsheet reporting often lacks satisfactory terms of control, validation and interconnectivity of information. All these items are essential for international business. Having a unified database, automated processes, integration, risk avoidance and enhanced management reporting make a strong case for considering technological upgrades. An RTC country’s infrastructure should be sufficiently developed to offer state of the art technological instruments to support the treasury center’s operations.

If we should see a counter movement from globalization towards more regionalization, corporate treasury needs to ensure cash visibility. The use of a TMS will become even more important to improve visibility on cash flows, FX exposures, liquidity and funding across the increased number of regional centers. Through a single TMS, the organization has access to aggregated data at a company-wide level.

Location selection

When selecting an RTC location, the aim of which is to centralize activities in a business-friendly environment, the following criteria should be considered; infrastructure and technology, end-user proximity, availability of general banking services, a large labor pool and relevant experts. In addition, it should also be in a location that reduces friction costs, has open FX-conversion supporting any in-country, cross-border funding requirements and offers access to liquidity markets.

Models and structures have been developed in response to the complexity of treasury organizations. They reveal the extent of functions implicated in the real international business environment, where MNCs are required to carry out extensive studies to ensure their treasury department operates efficiently. The level of maturity, taxes, centralization and regulations will dictate the best treasury center model to use.

Our experience shows that the following criteria should be considered and should serve as a checklist, when guiding your organization through this process:

Throughout the region, many new contenders have joined the race to become the next treasury center hotspot. The familiar names Singapore and Hong Kong still reign as treasury center location champions, but they are feeling the heat with competition now coming from countries such as Malaysia, Philippines, Thailand and Vietnam.

So, what next?

As the COVID-19 outbreak challenges many assumptions held in the past, structural changes are inevitable as we see the impact of the virus on the global economy. In the past, Asian companies have demonstrated dynamism, speed and agility as they not only operate in fast-growing and highly dynamic markets but also need to respond to rapidly evolving customer requirements and digital disruptions. They come well equipped to weather the current storm supported by early signs of successful containment of the virus leaving them a step ahead of the rest of the world. This may provide treasurers in the region an opportunity to start fortifying and upgrading their operations to become more agile.

In our experience, determining a single best practice approach or a one size fits all RTC for all corporations is an impossible task. Many of our projects confirm how unique corporations are in their processes and operations. The same goes for selecting a location for and the setting up of a regional treasury center as opposed to an RTC to cover the EU and its Single Euro Payment Area (SEPA), particularly in a region as diverse and intricate as Asia. Setting up an RTC within Asia necessitates a structural approach that is backed by management.

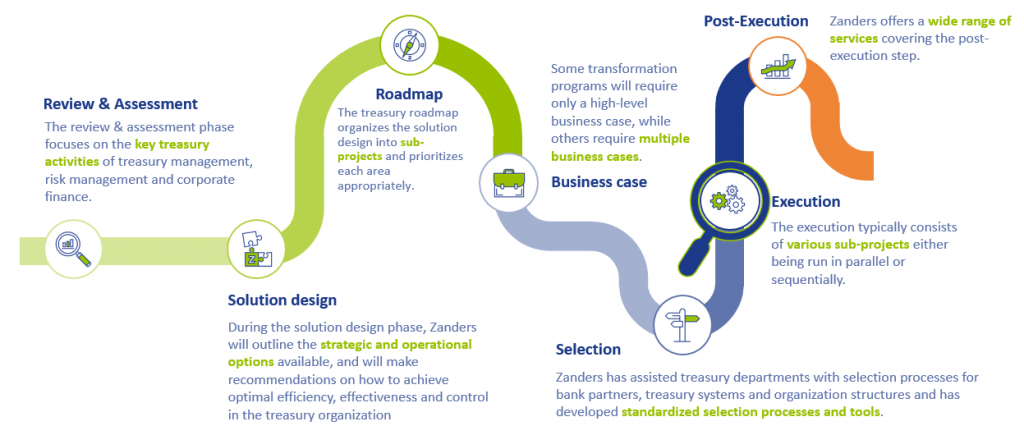

Ultimately, international expansion is a multifaceted undertaking and many of these facets are highly dependent on the individual situation. The key considerations addressed in this article are intended to serve as a guideline on where to start and how to approach setting up an RTC in Asia. If doubts persist, enlisting an experienced party to assist on the complexity of such projects is always an option. Zanders can help corporates in their search for the ideal location using our structured 7-step approach, see below, which is modified to their particular situation. This structured approach is especially helpful in these uncertain times.

-

CEO Statement: Delivering Financial Performance When It Counts

-

The Digital Agenda Has Increased the Cybercrime and Fraud Threat Landscape – It's Now Critical for Corporate Treasury to Build Resilience

-

The New Rails: How Stablecoins Are Redefining Cross-Border Payments for Corporate Treasury

-

Risk Mitigation Accounting (RMA) Exposure Draft amending IFRS9: Key Impacts and Practical Challenges

-

Optimizing the Valuation Processes in Modern Banking: A Strategic Approach to Efficiency, Consistency, and Cost Reduction

-

Intra-Group Loans Transfer Pricing: What’s Important in 2026?

-

A Roadmap for Banks to Geopolitical Risk Taxonomy

-

Geopolitical Risk and the ECB 2026 Reverse Stress Test: Mapping Failure Pathways Before It’s Too Late

-

Swiss Climate Scenarios 2025

-

ECB’s 2026 Geopolitical Reverse Stress Test: Why Channels Matter More Than Numbers