ISO 20022 XML (Pain.001.001.09) – Introduction of the Structured Address

The SWIFT MT-MX migration is now underway, with a primary focus on a select number of MT messages within the interbank messaging space.

However, possibly the most important point for corporates to be aware of is the planned move towards explicit use of the structured address block. In this second article in the ISO 20022 series, Zanders experts Eliane Eysackers and Mark Sutton provide some valuable insights around this industry requirement, the challenges that exists and an important update on this core topic.

What is actually happening with the address information?

One of the key drivers around the MT-MX migration are the significant benefits that can be achieved through the use of structured data. E.g., stronger compliance validation and support STP processing. The SWIFT PMPG1 (Payment Market Practice Group) had advised that a number of market infrastructures2 are planning to mandate the full structured address with the SWIFT ISO migration. The SWIFT PMPG had also planned to make the full structured address mandatory for the interbank messages – so effectively all cross-border payments. The most important point to note is that the SWIFT PMPG had also advised of the plan to reject non-compliant cross border payment messages from November 2025 in line with the end of the MT-MX migration. So, if a cross border payment did not include a full structured address, the payment instruction would be rejected.

What are the current challenges around supporting a full structured address?

Whilst the benefits of structured data are broadly recognised and accepted within the industry, a one size approach does not always work, and detailed analysis conducted by the Zanders team revealed mandating a full structured address would create significant friction and may ultimately be unworkable.

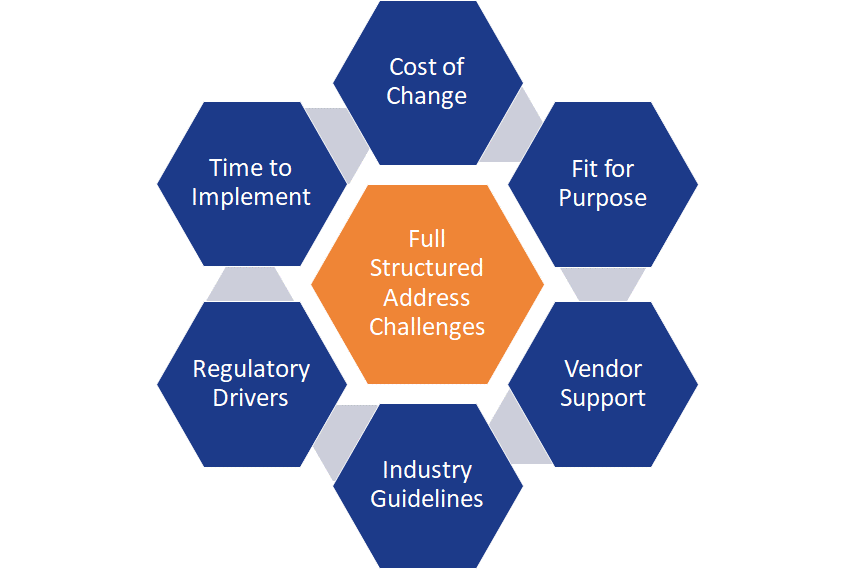

Diagram 1: Challenges around the implementation of the full structured address.

From the detailed analysis performed by the Zanders team, we have identified multiple problems that are all interconnected, and need to be addressed if the industry is to achieve its stated objective of a full structured address. These challenges are summarized below:

- Cost of change: The 2021 online TMI poll highlighted that 70% of respondents confirmed they currently merge the building name, building number, and street name in the same address line field. The key point to note is that the data is not currently separated within the ERP (Enterprise Resource Planning) system. Furthermore, 52% of these respondents highlighted a high impact to change this data, while 26% highlighted a medium impact. As part of Zanders’ continued research, we spoke to two major corporates to gain a better sense of their concerns. Both provided a high-level estimate of the development effort required for them to adapt to the new standard: ½ million euros.

- Fit for Purpose: From the ISO 20022 expert group discussions, it was recognized that the current XML Version 9 message would need a significant re-design to support the level of complexity that exists around the address structure globally.

- Vendor Support: Whilst we have not researched every ERP and TMS (Treasury Management System) system, if you compare the current structured address points including field length in the XML Version 9 message with the master data records currently available in the ERP and TMS systems, you will see gaps in terms of the fields that are supported and the actual field length. This means ERP and TMS software vendors will need to update the current address logic to fully align with the ISO standard for payments – but this software development cannot logically start until the ISO address block has been updated to avoid the need for multiple software upgrades.

- Industry Guidelines: Whilst industry level implementation guidelines are always a positive step, the current published SWIFT PMPG guidelines have primarily focused on the simpler mainstream address structures for which the current address structure is fine. By correctly including the more complex local country address options, it will quickly highlight the gaps that exist, which mean compliance by the November 2025 deadline looks unrealistic at this stage.

- Regulatory Drivers: At this stage, there is still no evidence that any of the in-country payments regulators have actually requested a full structured address. However, we have seen some countries start to request minimum address information (but not structured due to the MT file format), such as Canada and US.

- Time to Implement: We must consider the above dependencies that need to be addressed first before full compliance can logically be considered, which means a new message version would be required. Whilst industry discussions are ongoing, the next ISO maintenance release is November 2023, which will result in XML version 13 being published. If we factor in time for banks to adopt this new version (XML Version 13), time for software vendors to develop the new full structured address including field length and finally, for the corporates to then implement this latest software upgrade and test with their banking partners, the November 2025 timeline looks unrealistic at this point in time.

A very important update

Following a series of focused discussions around the potential address block changes to the XML Version 9 message, including the feedback from the GLEIF3 the ISO payment expert group questioned the need to support a significant redesign of the address block to enable the full structured address to be mandated. The Wolfsberg Group4 also raised concerns about scale of the changes required within the interbank messaging space.

Given this feedback, the SWIFT PMPG completed a survey with the corporate community in April. The survey feedback highlighted a number of the above concerns, and a change request has now been raised with the SWIFT standards working group for discussion at the end of June. The expectation is that the mandatory structured address elements will now be limited to just the Town/City, Postcode, and country, with typical address line 1 complexity continuing to be supported in the unstructured address element. This means a blended address structure will be supported.

Is Corporate Treasury Impacted by this structured address compliance requirement?

There are a number of aspects that need to be considered in answering this question. But at a high level, if you are currently maintaining your address data in a structured format within the ERP/TMS and you are currently providing the core structured address elements to your banking partners, then the impact should be low. However, Zanders recommends each corporate complete a more detailed review of the current address logic as soon as possible, given the current anticipated November 2025 compliance deadline.

In Summary

The ISO 20022 XML financial messages offer significant benefits to the corporate treasury community in terms more structured and richer data combined with a more globally standardised design. The timing is now right to commence the initial analysis so a more informed decision can be made around the key questions.

Notes:

- The PMPG (payment market practice group) is a SWIFT advisory group that reports into the Banking Services Committee (BSC) for all topics related to SWIFT.

- A Market Infrastructure is a system that provides services to the financial industry for trading, clearing and settlement, matching of financial transactions, and depository functions. For example, in-country real-time gross settlement (RTGS) operators (FED, ECB, BoE).

- Global Legal Entity Identifier Foundation (Established by the Financial Stability Board in June 2014, the GLEIF is tasked to support the implementation and use of the Legal Entity Identifier (LEI).

- https://www.wolfsberg-principles.com/sites/default/files/wb/pdfs/wolfsberg-standards/1.%20Wolfsberg-Payment-Transparency-Standards-October-2017.pdf

-

CEO Statement: Delivering Financial Performance When It Counts

-

Swift SCORE Plus: Does the Case for it Stack Up for the Corporate Community?

-

Transforming Cross-Border Payments Through Digital Innovation

-

End of Days: Calling Time on Swift’s Outdated Cross-border Payments Model

-

How BCBS 239’s RDARR Principles Can Strengthen Risk Data Aggregation and Reporting in Financial Institutions

-

Converging on resilience: Integrating CCR, XVA, and real-time risk management

-

Optimizing Global Payments: The Growing Role of EBICS

-

Calibrating deposit models: Using historical data or forward-looking information?

-

Surviving Prepayments: A Comparative Look at Prepayment Modeling Techniques

-

Treasury 4.x – The age of productivity, performance and steering