EBA published final package of IRRBB/CSRBB guidelines

On 20 October 2022, the European Banking Authority (EBA) published the final package of guidelines for the management of Interest Rate Risk in the Banking Book (IRRBB) and the Credit Spread Risk in the Banking Book (CSRBB). The package includes:

- Final guidelines for IRRBB and CSRBB (link)i

- Regulatory Technical Standards (RTS) on the IRRBB supervisory outlier tests (SOT), which updates the SOT for the Economic Value of Equity (EVE) and introduces an SOT for Net Interest Income (NII) (link)ii.

- RTS on the IRRBB standardized approach, which should for example be applied when a competent authority deems the internal model for IRRBB management of a bank not satisfactory (link).

Compared to the draft versions, published in December 2021, the most notable topics and changes are:

- CSRBB: Despite of significant concerns raised by many banks in response to the consultation papers, no significant changes have been made to the draft CSRBB guidelines. Hence, compared to the CSRBB guidelines of 2019, the scope of CSRBB is extended to the whole balance sheet unless it can be argued by the bank that a certain portfolio is not subject to credit spread risk.

- IRRBB: The EBA still expects banks to measure NII at risk including the market value change for positions that are accounted at fair value on the balance sheet.

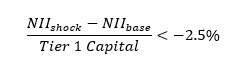

The EBA relaxed the constraint on the maximum weighted average repricing date (of 5 years) for retail and non-financial non maturing deposits (NMD) as introduced in the draft guidelines. Retail deposits with economic or fiscal constraints to withdrawal are now exempted from this specific guideline. The guideline on deposits taken from financial institutions is also relaxed. The maximum weighted average repricing date for operational deposits is changed from overnight to 5 years in the final guidelines (following the definition in the LCR regulation). The weighted average repricing date for other deposits taken from financial institutions remains constrained to an overnight repricing. - NII SOT: In the consultation paper, the EBA requested feedback on different approaches to report the NII SOT. In the final document the EBA made the choice to define the NII SOT as:

- implying that the decline in the 1-year NII must be below 2.5% of the Tier 1 capital.

Further, the EBA decided that the NII SOT should be calculated based on a narrow definition, where NII is defined as the difference between interest income and interest expense. Market value changes in instruments accounted for at Fair Value, and interest rate sensitive fees and commissions are excluded from the scope of the NII SOT. - EVE SOT: In the consultation paper, the EBA used the swap curve as an example for the risk-free curve that can be used for discounting. This has now been changed to OIS curve. The EBA indicates, however, that the bank can choose the risk-free yield curve according to their business model, provided that it is deemed appropriate. This leaves room for banks to keep using a non-overnight swap curve.

- IRRBB Standardized approach: The most notable change compared to the consultation paper is the fact that the EBA decided to not include the impact of instruments accounted at fair value in the standardized NII (at risk). Next to this, some minor clarifications have been included.

The IRRBB guidelines are effective as of 30 June 2023 and the CSRBB guidelines are effective as of 31 December 2023. When banks must apply the RTS on SOT will depend on the approval by the European Commission.

i Earlier, Zanders published an article describing the main changes for the measurement of IRRBB and CSRBB based on the draft publication.

ii Earlier, Zanders published an article describing the main changes for reporting the EVE and NII SOT based on the draft publication.

-

Key SAP Treasury and Cash Management Updates

-

SAP Analytics Cloud for Treasury Liquidity Planning

-

Preventing Payment Fraud with SAP Advanced Payment Management and Business Integrity Screening

-

SAP S/4HANA Treasury Business Partner Design and Maintenance

-

IFRS 9 Study 2026: Steady Coverage, Diverging Signals

-

Margin of Conservatism Explained: Reducing Capital Inflation in IRB Models

-

Cash Is King Again: Why real-time liquidity is the new strategic advantage

-

CEO Statement: Delivering Financial Performance When It Counts

-

The Digital Agenda Has Increased the Cybercrime and Fraud Threat Landscape – It’s Now Critical for Corporate Treasury to Build Resilience

-

The New Rails: How Stablecoins Are Redefining Cross-Border Payments for Corporate Treasury