Central Finance and Treasury: a marriage to last?

Central Finance (CFin) is an SAP S/4 HANA product launched to activate on an S/4 HANA engine.

Given that it runs on a S/4 HANA engine, it is mainly profiled in the market as a phased approach to adopt SAP S/4HANA, as well as a method to centralize and harmonize local finance processes.

CFin is an SAP S/4 HANA product that was launched in 2015. In its first stage, it enables data collection from multiple ERPs into one S/4 Hana running Central Finance. This also allows opportunities for data harmonization achieved by data cleansing in the source systems and/or by applying derivation rules (during the transfer of data to S/4) to achieve data attributes that have common usage across the organization. Data transfer to CFin occurs in real-time. The harmonized data in one CFin system enables systematic consolidated reporting, removing manual work around consolidating reports (in different formats) from multiple ERPs. CFin provides the most value to an organization where there are multiple older SAP ERP instances or other non-SAP Finance applications.

CFin exploits the capabilities of HANA – real-time, speed and agility to replicate financial documents into the central system – providing a real-time organization-wide financial view. In other words, CFin allows you to create a real-time common finance reporting structure for an organization.

Perceived use cases in the market for CFin are the following:

- Merger and acquisitions: repeatable onboarding for non-organic growth.

- Instance consolidation: credit, accounts payable and collections can be centralized in one instance.

- System consolidation: migrate and decommission selected existing SAP and non-SAP ERP systems.

- Subsidiary onboarding: smaller entities or subsidiaries can be easily onboarded onto the platform.

- SAP & non-SAP: the solution lets you consolidate and harmonize data on the fly, and update enterprise structures across SAP and non-SAP ERP systems like Oracle, PeopleSoft, or JD Edwards.

- Business transformation while staying on the ECC platform but leveraging on the S/4 Hana capabilities around improved processing.

- Enriched user experience via transformed UI and Fiori apps running on S/4.

- Shared service centre optimization through central process execution in one system.

- Centralized treasury through centralized payments, In-House Banking, Bank account management, Cash positioning and forecasting and Exposure identification and measurement

Deployment as Central reporting (release 1511 and onwards)

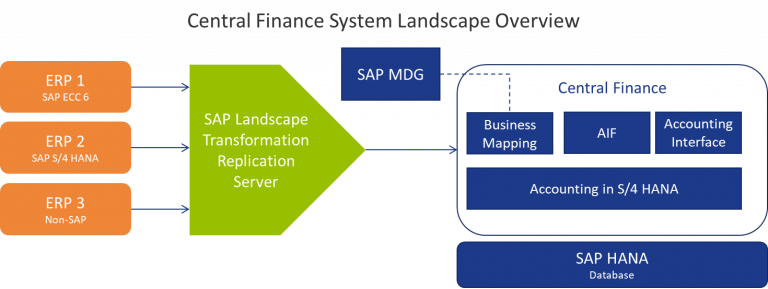

In a first phase, SAP CFin allows real-time replication of FI Documents. The replication of data is enabled via the SAP Landscape Transformation (SLT) replication server. More specifically, SLT is a tool that allows you to load and replicate data in real-time or via batch processing data from the SAP and non-Sap source systems into the SAP S/4 HANA database. This piece of software is a key element of the CFin solution. To provide full visibility on the SLT server, SAP has developed an application interface management framework (AIF). AIF is a monitor that allows error handling and full visibility on the SLT interface, as well as mapping functionality. It is important to highlight that CFin allows both the AIF and SLT for the integration of older SAP and non-SAP ERP systems.

Once an initial load of data is performed out of the various source systems into the CFIN application, continuous replication can be setup. If all systems are setup and connected to the CFin box, CFin can function as a central database of all financial data across the organization. If fully implemented, even a single universal journal can be operated

CFin also includes a Master Data Governance (MDG) application. The MDG allows you to manage all your master data centrally with a workflow and distribution functionality to all connected systems. If MDG is fully deployed, no new master data can be created outside of MDG. While basic functionality is included in CFin license, a separate license is required for full functionality.

To minimize any impact on the source system, CFin offers the functionality to enable mapping. General master data mapping can either be configured in the CFin customizing or by using the MDG functionality. Master data related to cost object is mapped using the cost object mapping framework.

Next to the technical complexity, CFin requires intensive business changes in order to be successful. The following business changes need to occur to unleash CFin’s full potential:

- Clean up master data.

- Clean up transactional data and verify consistency.

- Clean up old processes in source systems.

- Data harmonization of GL Accounts to enable one Universal Journal.

- Harmonization of profit and cost centers across legacy systems.

- Unification of Business partner set.

- Move to standard SAP as much as possible.

Mapping, either via the cost mapping framework, customization or the MDG, can alleviate the burden of harmonization on the source systems.

The key benefits of the deployment of CFin as a central reporting solution are:

- Real-time harmonized global financial reporting on various units and source systems.

- Universal journal for external, internal and management accounting.

Deployment of central processing (release 1809 and onwards)

After the first level of deployment, CFin can be an enabler for central processing. To enable central processing, the CFIN engine needs to be used as the single source of truth. This means that any documents created in the source systems are technically cleared and replicated in the CFin system. Even transactions can be directly entered in the CFin system. As a logical consequence, all status management is executed in the CFin application.

Various processes can be run on the CFIN engine, but in this document we are focusing on the following three relevant processes:

- Central payments.

- Cash application.

- Banking hub.

All three activities are a logical extension of centralizing all financial data. For example, instead of connecting to external banks out of each individual source system, all bank connections can be centrally managed out of the CFin system. Bank connectivity over Swift would further make the connectivity landscape bank agnostic, thereby limiting the connectivity to your Swift partner. Centralizing the bank connection entails outgoing traffic such as payments and collections, and incoming traffic such as bank statements.

The central payments functionality does not replace a treasury payment factory, as transactions are still executed from the debtor accounts, while a payment factory enables the on behalf payments from a centrally held set of accounts supported by an in-house bank structure

As all transactions and bank connections move to CFin, it is also therefore logical to centralize all bank statements in CFin. No distribution to ERP systems is required as all documents are technically cleared in the source systems.

Cash application refers to the management of open items, cash in transit and bank reconciliation. As all transactions are centrally executed, cash application is logically also executed centrally.

As is the case with all centralization exercises, special attention needs to be paid to the support of local payments in a central instance. With card payments, for example, the bill of exchange requires specific data elements to enable matching. If the elements are not mapped correctly to the central instance, the local payment method might not be fully supported in the central instance.

At the time of writing, only a handful of companies are live with central processing. Most CFin clients are still in the first phase of implementation.

Additional key benefits of the deployment of CFin as a central process engine include:

- Central open item management and payments.

- Consolidation.

- Central close.

Interaction Central Finance & Treasury

A key question treasurers ask is how treasury and CFin relate towards each other. Firstly, CFin central processing instance focuses on the centralization and standardization of local finance processes. However, as treasury is a well-connected corporate function in any organization, Zanders expects a sizeable impact from CFin on the treasury function. Let’s look at a few key areas:

Payment factory: Payment factory is defined here as a central structure that facilitates payment on behalf of/in name of and receivables on behalf of for all subsidiaries in the company.

CFin and payment factory applications are independent modules and ring fenced in terms of the functionality they deliver. CFin, however, complements the payment factory by simplifying the integration of source ERPs to the system hosting payment factory (the same system as having CFin). In a CFin world, the payables and receivables (for direct debits) are technically cleared in the source ERPs, as these open items are transferred to the CFin system. The payments (and direct debits) can be then executed in CFin system in a standardized way. The complexities of integrating payment requests from ERPs, particularly non-SAP ERPs, in a non-CFin world do not exist. Therefore a payment factory implementation will require less effort if CFin central processing is fully implemented.

Cash positioning: Cash positioning is defined here as establishing and managing your daily cash position by currency or bank account as well as evaluating the short-term cash needs and liquidity position.

A prerequisite for enabling central cash positioning is the setup of centralized payment processing. This allows cash positioning for subsidiary companies to be enabled in the central system. A major benefit compared to today’s process in the non S/4 HANA source systems is the overhauled user experience. Currently, a sizeable set of new Fiori apps in the cash management space are readily available on S/4, such as a Fiori app on automatic reconciliation of intraday bank movements against cash estimates. Similar apps are available on variance analysis and request bank transfers on the fly from cash position reporting. The real-time availability of data also leads to a more accurate evaluation of the short-term liquidity position.

Cash flow forecasting: Cash flow forecasting is defined as estimating the timing and amounts of cash inflows and outflows over a specific period. Cash flow forecasting tackles a longer-term horizon than cash positioning does. Generally speaking, cash flow forecasting works of provided date from treasury stakeholders combined with historic patterns.

CFin currently does not have the functionality to support cash flow forecasting. However, the real-time integration of ERP documents into the central system provides the capability to do more accurate mid-term cash forecasting. An additional benefit realized by the availability of real-time data is the pre-population of subsidiary forecasts, which leads to more accurate cash flow forecasting. It is important to note that SAP does not offer any standard functionality regarding pre-population of data in subsidiary cash flow forecasting. The interaction for treasury is mostly limited to interfacing cash flow and transaction data.

Risk management: Risk management is any functionality linked to the management of financial risk, to allow the company to meet its financial obligations and ensure predictable business performance. In most companies, treasury actively manages liquidity, credit, FX, interest rate and commodity risk.

Limited functionality is present in CFin to support risk management. The main interaction is limited to interfacing exposure data to treasury. Although all relevant accounting information is available in the CFin system, no risk management functionality is available. Therefore, treasury can help to actively manage the foreign currency risks from any balance sheet position or even from any single item. This feature is supported with the functionality Balance Sheet FX Risk within SAP’s Treasury solution.

Looking further than foreign currency balance sheet risk, as the data from multiple ERPs is now available on one system, with bespoke development it could be linked in real-time to the one exposure table from where it can be managed via SAP standard functionality on exposure, risk and hedge management. The availability of data into the exposure functionality provides significant value in overall risk mitigation. It is important to highlight that attention needs to be paid on mapping when documents are replicated to the central system. Mapping can have a substantial impact on risk management operations if not executed diligently.

Looking at the system architecture, a common question is: “Do Treasury & Central Finance operate on one common platform or as two separate boxes?” Unfortunately, the question does not have a clear-cut answer. To balance the merits of both approaches, a more detailed assessment is required.

Conclusion

CFin will become an important counterparty for treasury to cooperate with. Treasury will be a major consumer of CFin data to run operations such as a payment factory, risk management, and cash flow forecasting. Due to the importance of CFin to treasury and its operations, treasury needs a seat at the table of any CFin implementation. Involvement in the design phase is key to ensuring the information needed for treasury is available. Involvement in the mapping and harmonization exercise is particularly crucial.

Zanders & Central Finance

Given our 25 years of experience in treasury and our renowned SAP Treasury practice, Zanders is well placed to take up the role of treasury at the table. Thanks to our in-depth business expertise, as well as our extensive experience with both systems, we can be the perfect partner for your Central Finance implementation. Would you like to know more? Then contact Sibren Schilders via [email protected].

-

CEO Statement: Delivering Financial Performance When It Counts

-

The Digital Agenda Has Increased the Cybercrime and Fraud Threat Landscape – It's Now Critical for Corporate Treasury to Build Resilience

-

The New Rails: How Stablecoins Are Redefining Cross-Border Payments for Corporate Treasury

-

Risk Mitigation Accounting (RMA) Exposure Draft amending IFRS9: Key Impacts and Practical Challenges

-

Optimizing the Valuation Processes in Modern Banking: A Strategic Approach to Efficiency, Consistency, and Cost Reduction

-

Intra-Group Loans Transfer Pricing: What’s Important in 2026?

-

A Roadmap for Banks to Geopolitical Risk Taxonomy

-

Geopolitical Risk and the ECB 2026 Reverse Stress Test: Mapping Failure Pathways Before It’s Too Late

-

Swiss Climate Scenarios 2025

-

ECB’s 2026 Geopolitical Reverse Stress Test: Why Channels Matter More Than Numbers