Cash Positioning in a multi ERP landscape

It is without a grain of doubt that cash positioning is at the forefront of successful cash & liquidity management.

There are various sources from which treasurers obtain information that forms accurate cash position within the company’s ERP or Treasury Management System. The most important of these sources is the current available balance, most often obtained from bank statements which are reported by various banks through numerous protocols.

Depending on the system an enterprise is using, the cash position can be updated in two main ways; directly from the balance which has been reported on the bank statement by the bank, or through making appropriate accounting postings of bank statement items to relevant GL accounts. For a long time, in SAP only the latter was possible. The very least that needed to happen was the posting in so-called posting area 1, whereby the bank statements were posted to the Bank GL Balance Sheet account, with opposing entry posted to the Bank GL Clearing Account.

New feature in SAP: Cash positioning without posting

A new functionality has been introduced as of SAP S/4HANA 2111 (Cloud version) and SAP S/4HANA 2021 (On-Premises version) releases. With the new functionality it is no longer required to post the items from the bank statements to have the cash position updated within a selection of Fiori Applications. It is important to note that the feature only applies to the bank EOD (end of day) bank statements, with Intraday bank statements still relying on creating memo records to update cash position.

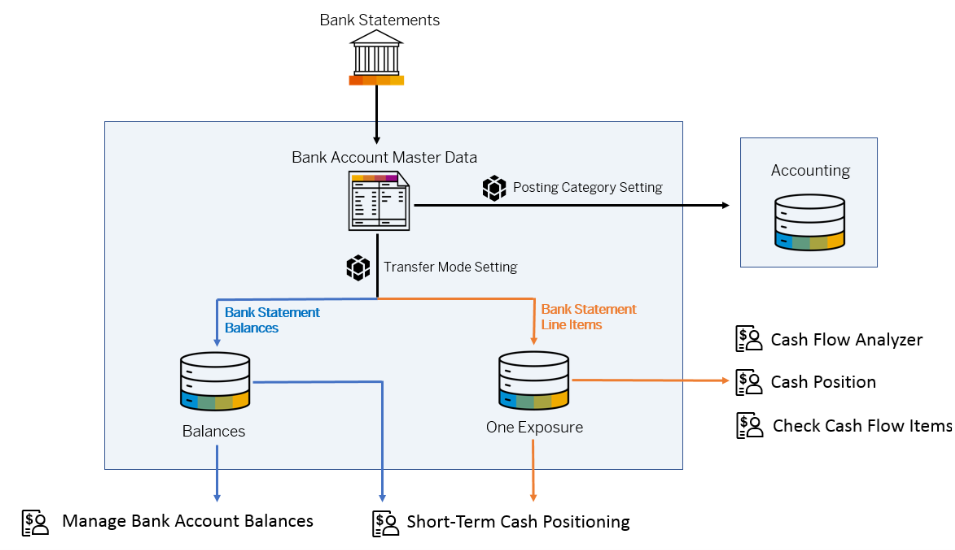

Depending on the settings maintained within the S/4 environment, one can then view the cash position in either of the 5 Fiori apps. It is possible to use only the balance that is reported by the bank on the bank statement to update the cash position, or use the individual bank statement line items, or both. The picture below shows the sources of information that can be used to update the cash position, as well as which Fiori apps can be used to view the cash position.

Figure 1: How bank statement data can be integrated and processed in cash management. Source

The functionality can prove especially useful in a scattered entity landscape, where multiple accounting systems are used, but only one central system should be used for cash positioning. With this new functionality, where bank statements do not need to be posted, and a minimal setup is sufficient on company code level (no GL accounts are even needed), the enterprise will be able to achieve a consolidated cash position overview in one SAP S/4 environment.

Updating the cash position

How important is it to base the cash position on reconciled accounting entries rather than what the bank has reported on the bank statement? One might argue that using cash position that was updated via the means of the latter process can carry a risk of an unaccounted transaction making its way onto a bank statement, and thus skewing the cash position. But how many times as a treasurer have you actually seen that the bank statement contained transactions that should not be there? What is more, within the current bank connectivity landscape, whereby bank statements are delivered in a secure manner via either SWIFT, H2H, EBICS, instead of a manual upload, the risk of bank statements being tampered with is very low, or even non-existent. So, there we have it, a new means of updating your cash position in SAP.

Supportive API

What is in store for the future for Cash & Liquidity Management within SAP S/4HANA? Do we even need the bank statements if the goal is only to update the cash position? With the increasing presence of APIs within the treasury world, SAP has been also making efforts to allow the cash position to be updated via means other than bank statements. With an API, one would be able to connect to the bank to obtain the information on the current available balance, either on a schedule, or whenever desired, with a click on a button. With the ever-increasing need for up-to-date immediate cash position information, this seems like a logical way forward.

-

Intra-Group Loans Transfer Pricing: What’s Important in H2 2026?

-

Key SAP Treasury and Cash Management Updates

-

SAP Analytics Cloud for Treasury Liquidity Planning

-

Preventing Payment Fraud with SAP Advanced Payment Management and Business Integrity Screening

-

SAP S/4HANA Treasury Business Partner Design and Maintenance

-

IFRS 9 Study 2026: Steady Coverage, Diverging Signals

-

Margin of Conservatism Explained: Reducing Capital Inflation in IRB Models

-

Cash Is King Again: Why real-time liquidity is the new strategic advantage

-

CEO Statement: Delivering Financial Performance When It Counts

-

The Digital Agenda Has Increased the Cybercrime and Fraud Threat Landscape – It's Now Critical for Corporate Treasury to Build Resilience