An SAP cockpit for seamless transfer pricing compliance

Entering an interest rate for an intercompany loan in SAP is simple, but determining the interest rate according to the latest transfer pricing regulation is not as easy.

Therefore, we decided to leverage our cloud-based solution and enable SAP users to determine the arm’s length interest rate with just a few clicks.

The pricing of various treasury transactions, as for all intercompany flows, is subject to transfer pricing regulation. In essence, treasury and tax professionals need to ensure that the pricing is in line with market conditions, i.e. the arm’s length principle. To this end, numerous Zanders clients use the Zanders Inside Transfer Pricing Solution (TPS). Our TPS enables them to set interest rates on intercompany transactions in a compliant and automated way. Since its go-live almost three years ago, clients have priced over 1000 intercompany loans with this self-service solution.

Our TPS has been a stand-alone tool on the Zanders Inside platform, but that is about to change. We have selected SAP as the first treasury management system for online integration. The interface uses APIs between the two systems to pull and push the relevant information. This article will elaborate on how the process flow is designed from an end user perspective.

Automated credit rating assessment

Initially, the necessary static data on the borrowing entities needs to be saved on the Zanders Inside platform. This data is used to determine an entity-specific credit rating, a requirement for a compliant transfer pricing assessment. This can be done via the Zanders Inside template, which gives the user a standard framework to capture the financial statements for all entities. Additionally, the user also saves qualitative rating information. Based on this information, the automated credit rating assessment is run in the background. The borrower credit rating will be used as input to the pricing assessment. This first step is the only manual process in the entire end-to-end flow. In addition, adjustments to the static data only need to occur once per year, i.e. when the new financial statements are published.

Overview

Once the static data is set up, the user enters an intercompany loan in the usual way. In the interest condition, the SAP user will indicate that the interest rate will be determined using the Zanders TPS platform. Using the SAP standard functionality, the user can define if the interest rate has to be updated via the Zanders TPS platform regularly or only initially at deal creation. Once the deal is created, the Zanders TPS cockpit offers an overview of all intercompany loans with outstanding pricing status. From this environment, the user can select the individual deals and raise a pricing request to the Zanders TPS platform. This pricing request will include identification of the lender and borrower, which impacts the rating, and the relevant terms and conditions of the loan, which impact the arm’s length interest rate.

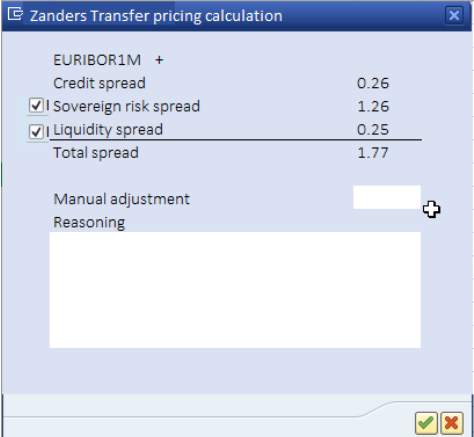

Transferred values

Aside from the rating, the main drivers are the maturity of the loan, the structure of the facility (level of collateral), the currency and the repayment schedule. These values will be transferred into the Zanders Inside TPS. It enables the solution to operate as a calculation engine, i.e. making the necessary calculations in the background.

In the Zanders TPS cockpit, the user is offered the possibility to review the received interest rate and its constituting components. Given the background of the transaction, the user is free to decide which components will be included in the final rate. Additionally, a manual rate adjustment can be added as a separate component, together with an explanatory comment. The manual rate adjustment and its justification is transferred back to the Zanders TPS platform and will be included in the final pricing documentation.

Fully-fledged report

Finally, the output of the transfer pricing solution is twofold. In addition to pulling the interest rate components into SAP, it will automatically create a fully-fledged transfer pricing report. This report will automatically be saved in the solution and includes a reference towards the transaction identifier in SAP. The report contains the methodology as well as all specifics of the calculation and can be used as a reference document later on. This can be used should a tax audit occur, for example.

Determining the interest rate and entering it into the appropriate deal in a TMS system is often a manual and cumbersome process involving different departments. By connecting the Zanders Inside TPS to SAP, the level of straight-through processing (STP) within a treasury department can significantly improve. Additionally, it offers a less error-prone alternative as it removes manual data entry and calculations.

Free Demo

Would you like to learn more on this new initiative or receive a free demo of our solution? Do not hesitate to reach out!

-

CEO Statement: Delivering Financial Performance When It Counts

-

The Digital Agenda Has Increased the Cybercrime and Fraud Threat Landscape – It's Now Critical for Corporate Treasury to Build Resilience

-

The New Rails: How Stablecoins Are Redefining Cross-Border Payments for Corporate Treasury

-

Risk Mitigation Accounting (RMA) Exposure Draft amending IFRS9: Key Impacts and Practical Challenges

-

Optimizing the Valuation Processes in Modern Banking: A Strategic Approach to Efficiency, Consistency, and Cost Reduction

-

Intra-Group Loans Transfer Pricing: What’s Important in 2026?

-

A Roadmap for Banks to Geopolitical Risk Taxonomy

-

Geopolitical Risk and the ECB 2026 Reverse Stress Test: Mapping Failure Pathways Before It’s Too Late

-

Swiss Climate Scenarios 2025

-

ECB’s 2026 Geopolitical Reverse Stress Test: Why Channels Matter More Than Numbers