To help banks manage climate risk over a more relevant time horizon, the NGFS has introduced scenarios focused on the next three to five years.

With extreme weather events becoming more frequent and climate policy tightening across jurisdictions, banks are under increasing pressure to understand how climate change will impact their portfolios. Previously, most climate scenario analyses have focused on long-term trajectories, stretching out to 2050 or beyond. However, these long-term analyses have often been far too abstract for day-to-day risk management.

The new NGFS short-term scenarios investigate the impact of climate risks over the next five years, offering a more practical solution. By isolating the individual impacts from physical and transition risk, and by providing better granularity at both temporal and sectoral levels, the new scenarios provide a new and valuable tool for climate risk modeling.

In this article, we explore what makes these scenarios unique, their benefits and limitations, their impact on future macroeconomic and market trends, and importantly, how banks can utilize them to fulfil regulatory requirements.

Physical and transition risks in the scenarios

The short-term scenarios capture four possible futures, each reflecting a different mix of physical and transition risks. The scenarios show how varying levels of climate policy and climate-related events could shape the economic and financial outcomes over the next 5 years. The four scenarios are summarized in the figure below.

Figure 1: The four NGFS short-term scenarios.

Key benefits and limitations of the new scenarios

The scenarios offer several benefits, including a more practical time horizon and better isolation of physical and transition risks. However, they also come with inherent limitations that should be acknowledged when being used. Below, we summarise the main benefits and limitations of the new scenarios.

Benefits

- Time horizon

- Although NGFS has already released several versions of their long-term scenarios, this is the first release of climate scenarios whose narratives focus on the next few years. Short-term scenarios cover time horizons that are typically more relevant for risk assessment management in banks, such as capital planning, liquidity assessments, and regulatory stress testing exercises. In addition, the uncertainty of climate and macroeconomic variables increase over longer horizons, making the short-term scenarios more dependable.

- Calibrated using recent data

- As with any model which has been recalibrated using the latest data, by incorporating the most recent economic conditions, market trends, and climate policy commitments, the short-term scenarios provide more reliable and accurate forecasts. This allows banks to run more credible stress tests, develop informed strategies, and leads to outputs that are more aligned with current market and policy conditions.

- Isolation of physical and transition risk

- Three of the four scenarios isolate only physical or transition risk, which can provide more targeted insights for climate risk assessment. By separating these risks, banks can identify the specific drivers of financial impact more accurately, whether from policy changes or climate-related events. Unlike scenarios that contain a combination of transition and physical risks, isolating only one of the risks can make the results easier to interpret and act upon.

- Variation across sectors and regions

- NGFS short-term outputs cover up to 15 macro-regions (e.g. EU27, Asia and North America) and up to 46 countries, which is similar to the long-term scenario results. The biggest improvement is found on the temporal granularity: while most of the variables for the long-term scenarios are provided in 5-year intervals, the short-term scenarios are mostly provided on a yearly basis.

Limitations

- Still not short enough?

While the NGFS short-term scenarios aim to address near-term climate-related risks, even shorter time horizons may be necessary for accurate and practical modeling in both credit and, in particular, market risk. More granular timeframes, such as a quarterly projection interval, would support banks to rapidly react to policy changes, market reactions, or acute physical climate events, which can unfold within weeks or months and not years.

- Lack of dispersion within regions or sectors

In some cases, the results show limited differentiation between sectors and regions. This can make it difficult to accurately capture sector-specific or country-specific vulnerabilities. For example, countries with significant geographical and socioeconomic differences, such as Switzerland, Iceland, and Ukraine, are grouped together under the region "Rest of Europe". Similarly, the sector "Market Services" includes a wide range of distinct industries, such as Real Estate, Telecommunications, and Waste and Water Collection.

- Physical risk is still difficult to accurately model

Accurately capturing physical climate risk within a short-term horizon remains methodologically challenging. Acute events like floods or wildfires are based on the estimation of tail risks (e.g. return periods) which can be difficult to model accurately. In addition, physical risks exhibit high spatial variability. For instance, coastal areas can be more vulnerable to hurricanes than inland areas, even if they are in the same country. Therefore, aggregating scenario data on the country or regional level can potentially underestimate the risks in specific areas.

- Over-simplification of policy implementation

Policy pathways in the short-term scenarios tend to assume smooth, linear implementation and immediate effectiveness. In reality, climate policies often face political, social, and economic frictions that delay or prolong their impact. Hence, these assumptions may lead to the underestimation of transition shocks, particularly where abrupt or uncoordinated policy actions could trigger market volatility.

Impact of the new scenarios on important modeling variables

To take a look at the NGFS short-term scenarios in action, we can examine the impact of the scenarios on key macroeconomic variables. Figure 2 shows the behavior of GDP and carbon price (with respect to baseline values) within Europe and Asia for all four scenarios. There are clear negative shocks which are seen in the GDP for all the scenarios. Similarly, we see a positive spike in the carbon price for both regions, however the effect in Asia is much greater than in Europe. Asia experiences a sharper percentage increase in carbon prices because it starts from a much lower baseline compared to Europe, where carbon prices are already high and policies have been in place for years. Additionally, in general, Asia is more emissions-intensive and heavily reliant on fossil fuels (particularly coal) which means more aggressive changes to carbon pricing are required to reduce emissions.

Figure 2: Top – YoY change in GDP (compared to baseline). Bottom – change in carbon price (compared to baseline).

Although the impact to variables such as macroeconomic indicators, emissions trends, and shifts in production offer essential context, they are usually only the first step in climate risk modeling. Ultimately, we are interested in how these variables translate into changes in market-based metrics, such as corporate bond spreads or PDs, which directly affect portfolio valuation. For example, for stress testing purposes, macro and sectoral outputs must be mapped onto these market-based metrics to assess potential losses and capital impacts.

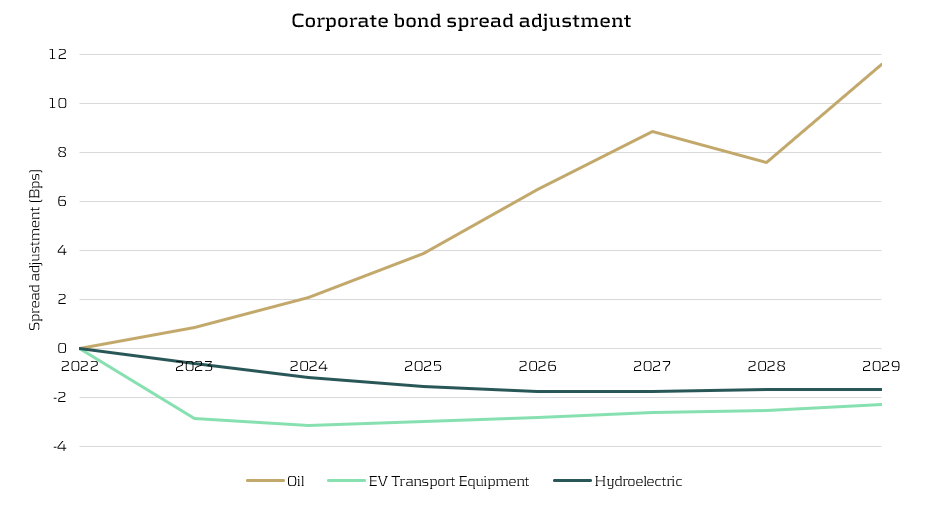

Figure 3 compares the corporate bond spread adjustments for the Oil, EV Transport Equipment, and Hydroelectric sectors under the HWTP scenario. The results illustrate a shifting investor sentiment in the corporate bond market. The Oil sector experiences a significant increase in spread adjustments over the time horizon due to an increase in perceived risk and a decline in investor favorability. In contrast, the EV Transport Equipment and Hydroelectric sectors maintain negative spread adjustments, highlighting that they are viewed more favorably. Overall, these results capture a market preference for cleaner and more sustainable industries and the scenarios clearly distinguish between sectors that are carbon-intensive and those aligned with low-carbon technologies.

Figure 3: Adjustment to corporate bond spreads for the Oil, EV Transport Equipment, and Hydroelectric sectors (HWTP scenario).

Zanders’ opinion

Although the five-year horizon of the new scenarios is still somewhat too long for direct application to market risk modeling (where exposures fluctuate on much shorter timescales), it aligns far better with the lifecycle of most credit products, especially those with relatively short maturities such as personal loans. Banks should utilise the scenarios as starting points for modeling the effects of near-term climate shocks on the performance of their credit products. However, the new scenarios can still provide valuable insights for market risk modeling. The scenarios can help identify sectoral sensitivities, adjust volatility and correlation assumptions, and enrich the narratives of existing scenarios.

The scenarios also help to standardise climate stress testing by providing a consistent set of assumptions, variables, and modeling frameworks that financial institutions can use as a common reference. This alignment reduces discrepancies in inputs and methodologies, enabling more comparable results across banks and jurisdictions. As a result, institutions and supervisors can more effectively benchmark climate-related risks, identify outliers, and support coordinated regulatory responses, ultimately improving the credibility and usefulness of climate stress tests.

Importantly, the new scenarios are well-suited to meet the needs of regulatory frameworks like the Internal Capital Adequacy Assessment Process (ICAAP), which typically considers a 3-to-5-year horizon. This makes them far more applicable than traditional long-term scenarios, which typically look out to 2050. Similarly, the ECB climate stress testing framework requires banks to use a variety of time horizons and both physical and transition risk scenarios. With ever-growing regulatory expectations, such as the recent CP10/25 consultation paper from the PRA on managing climate-related risks, the new short-term scenarios provide a timely and relevant tool for banks.

Conclusion

The new NGFS short-term scenarios are an important addition to climate risk modeling frameworks, offering a direct focus on the next five years – a time period which is far more aligned with capital planning, liquidity assessments, and regulatory stress. However, the scenarios are not intended to replace existing long-term scenarios. Rather, they complement them by providing a near-term view of climate risk that is highly relevant for all banks.

For more information on how Zanders can support you to understand the impact of climate risk on your business, please contact Steyn Verhoeven and Polly Wong.

A regulatory change in CRR3 may significantly impact the capital treatment of NHG-covered Dutch mortgages.

With the introduction of CRR3, effective from January 1, 2025, the ‘extra’ guarantee on Dutch mortgages – known as the Dutch National Mortgage Guarantee (NHG) – will no longer be automatically eligible for the modeling approach. This requires institutions to apply the substitution approach instead. Although this may seem like a minor change, it can have far-reaching consequences. In this article, we provide a background on this change in the treatment of NHG and discuss the potential implications and challenges it may bring.

Introduction Dutch National Mortgage guarantee (NHG)

The Dutch National Mortgage Guarantee (NHG) serves as a safety net for borrowers and lenders of mortgage loans in the Netherlands. It is designed to provide protection in cases of financial distress caused by circumstances such as divorce, disability, or unemployment [1] [2] [3]. If these situations require the sale of the residential property and a residual debt remains after all other collection sources have been exhausted, the NHG will cover this remaining debt when contractual conditions are met1.

The NHG guarantee is provided by the Stichting Waarborgfonds Eigen Woning (WEW) [1] [4]. Although Stichting WEW is not state-owned, the Dutch state acts as a suretyship provider. This arrangement ensures that if Stichting WEW’s capital is insufficient to meet its guarantee claims, the state will supply unlimited interest-free loans. These loans must be repaid only after the foundation’s assets have been restored [5].

Following the Capital Requirements Regulation (CRR), the NHG guarantee classifies as Unfunded Credit Protection (UFCP) Credit Risk Mitigation (CRM) and should be treated accordingly.

Exposure class of Stichting WEW

As outlined in the previous text, the direct protection provider of the NHG is Stichting WEW. In the event that NHG fails to make payments, the Dutch sovereign state provides a suretyship to Stichting WEW, essentially serving as a counter-guarantee for the NHG guarantee extended by Stichting WEW.

CRR III article 4(8) [6] defines a public sector entity (PSE) as: “a non-commercial administrative body responsible to central governments, regional governments or local authorities, or to authorities that exercise the same responsibilities as regional governments and local authorities, or a non-commercial undertaking that is owned by or set up and sponsored by central governments, regional governments or local authorities, and that has explicit guarantee arrangements, and may include self-administered bodies governed by law that are under public supervision;”

Stichting WEW satisfies the definition of PSE in CRR III article 4(8), as it is a non-commercial undertaking (stichting) established2 by the central government, with an explicit guarantee arrangement from the Dutch central government. However, the CRR does not clearly define the sponsoring of the central government. Should it be determined that the sponsoring requirement is not met, Stichting WEW must instead be classified as a corporate exposure class3.

The remainder of the text assumes that Stichting WEW can be classified under the PSE exposure class as defined in CRR III article 112(c) (SA) and 147(2)(aa)(ii) (IRB). Nonetheless, the validity of the arguments throughout the following chapters remains intact, regardless of whether Stichting WEW is classified under the corporate or PSE exposure class.

Stichting WEW may not be classified as an exposure to a central government following CRR III articles 116 (SA) and 147(3)(a) (IRB), which specify that only specific public sector entities should be allocated to the central government exposure class. Given that Stichting WEW does not appear on the list published by the European Banking Authority (EBA) [7], it cannot be classified as an exposure to the central government under these articles.

There is no market consensus in the Dutch mortgage market on how to classify Stichting WEW: whether as a PSE or as a Corporate exposure. During our recently hosted roundtable discussing the implications of regulatory changes concerning NHG, participating banks indicated that it might be challenging to clearly classify Stichting WEW as a PSE due to the inconclusive regulatory guidance noted in this chapter. Banks are encouraged to engage in discussions with their Joint Supervisory Team (JST) and/or National Competent Authority (NCA) to determine the appropriate treatment of Stichting WEW.

Allowed UFCP approaches for NHG guarantees

According to CRR III article 108(3), if the AIRB approach is used for similar direct exposures to the protection provider, the UFCP modeling approach is required. In this context, similar direct exposure refers to exposure to the Stichting WEW4. With the competent authorities’ approval, the AIRB approach can be used for PSEs (and corporates), as specified in CRR III article 151(8-9). Therefore, if the AIRB approach is used for exposures to Stichting WEW, then the UFCP modeling approach is applicable. Conversely, if the SA or FIRB approach is used instead, then the UFCP substitution approach is mandatory.

Applying the effect of NHG guarantees

Under the substitution approach, the counter-guarantee provided by the Dutch central government can be recognized. CRR III article 214 states that guarantees backed by the central government may be treated as exposures within the central government exposure class, as defined in CRR III articles 112(a) (SA) and 147(2)(a) (IRB). This implies that the NHG guarantee can be classified under the central government exposure class [8]. Consequently, while capitalizing the NHG guarantee using the SA approach for the Dutch central government, it is possible, though not obligatory, to apply a 0% risk weight associated with the Dutch central government5.

If the institution employs the AIRB approach for exposures to to Stichting WEW, the modeling approach can be applied. In this scenario, risk weights for Stichting WEW and the Dutch central government (CRR article 214) are not used, as the effect of the NHG guarantee is modelled directly.

Substitution approach for banks without AIRB PSE models

For banks without AIRB models for Stichting WEW, the above argumentation does not apply, and the UFCP substitution approach for NHG presents several challenges.

The following list provides a non-exhaustive overview of these challenges:

1. Reconsideration of methodologies: Many banks model NHG separately, possibly through a specifically calibrated segment.

2. Level of application: Implementing the substitution approach within the reporting stream poses difficulties, as it requires separating the NHG-covered portion of the exposure from the uncovered portion. This could necessitate changes in data delivery and processing.

3. Changing coverage amounts over time: The NHG coverage percentage has changed from 100% to 90%, requiring at least two different implementations/calculations.

4. Unknown claimable amount: The exact amount that can be claimed is only known once the residential property is sold.

5. Loss-sharing exclusion: The substitution approach cannot incorporate the loss-sharing characteristic.

6. Mismatch between 0% substitution and actual losses of 5-10%: This is typically due to:

- Failed NHG claims, which cannot be integrated into the substitution approach.

- Discounting of cash-flows.

In summary, the substitution approach for banks without AIRB PSE models presents significant practical and methodological challenges. Effectively addressing these is essential to ensure a reliable implementation of the revised NHG treatment and maintain regulatory compliance.

Conclusion

Although the change in the CRR may seem minor at first glance, its consequences can be far-reaching. This article has outlined the key aspects of the revised NHG treatment, along with potential implications and challenges. However, it is not possible to provide a one-size-fits-all overview that fully captures the impact for every financial institution affected by this change.

If you would like to understand what the revised NHG treatment means specifically for your organization, feel free to contact our experts: Rick Stuhmer & Victor van Dongen.

Bibliography

[1] NHG, „Voorwaarden en normen [NHG conditions 2024],” 2024. [Online]. Available: https://www.nhg.nl/voorwaarden-en-normen/#id-18478.

[2] NHG, „Kwijtschelding van een restschuld [NHG conditions 2024],” 2024. [Online]. Available: https://www.nhg.nl/hulp-van-nhg/kwijtschelding-van-een-restschuld/.

[3] Rijksoverheid, „Nationale Hypotheek Garantie (NHG),” 2024. [Online]. Available: https://www.rijksoverheid.nl/onderwerpen/huis-kopen/vraag-en-antwoord/nationale-hypotheek-garantie-nhg.

[4] NHG, „Over de stichting [NHG annual report 2022],” 2022. [Online]. Available: https://www.nhg.nl/media/1bgf13fd/nhg_jaarverslag2022-hr.pdf.

[5] Stichting Waarborgfonds Eigen Woningen, „Memorie van toelichting bij de Wet herziening eigendomsgrenzen 2023, onderdeel 1477577. Rijksfinanciën.,” 2023. [Online]. Available here.

[6] European Parliament and European Council, „Amending Regulation (EU) No 575/2013 as regards requirements for credit risk, credit valuation adjustment risk, operational risk, market risk and the output floor,” 2024. [Online]. Available: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=OJ:L_202401623.

[7] European Banking Authority, „Lists for the calculation of capital requirements for credit risk,” 2024. [Online]. Available: https://www.eba.europa.eu/activities/supervisory-convergence/supervisory-disclosure/rules-and-guidance.

[8] Nauta Dutilh, „Toelaatbaarheid Nationale Hypotheek Garantie als kredietprotectie onder de CRR,” 2020. [Online]. Available: https://www.nhg.nl/media/rhkhtqbx/nhg-memorandum-over-crr-toelaatbaarheid-31-maart-2020-pdf.pdf

[9] Stichting Waarborgfonds Eigen Woningen, „Statuten NHG,” 2019. [Online]. Available: https://www.nhg.nl/media/4vvcjw4p/statuten-wew-per-23-december-2019.pdf

Citations

- As of January 2014, a 10% loss sharing rule was introduced, meaning NHG guarantees only 90% of the residual debt. ↩︎

- NHG statutes article 11 allow Dutch ministers to appoint 3 out of 5 members of the supervisory board, which together appoint the 6th member. This effectively means that the Dutch government controls 4 out of 6 members [9]. ↩︎

- As fallback, Stichting WEW must be allocated to the corporate exposure class following CRR III article 147(7). ↩︎

- Article 214 does not influence the exposure class of direct exposure to the protection provider, only the exposure class of the NHG guarantee itself. ↩︎

- The alternatives are not recognizing the counter-guarantee, and either using the 20% risk weight implied by Stichting WEW’s AAA rating following CRR III article 116 using the SA approach, or using the IRB risk weight of Stichting WEW using the IRB approach. Both will lead to higher risk weights than 0% and lead to higher capital requirements. ↩︎

In the rapidly shifting landscape of financial risk management, accurate estimation of default probabilities is crucial for informed decision-making.

According to the IFRS 9 standards, financial institutions are required to model probability of default (PD) using a Point-in-Time (PiT) measurement approach — a reflection of present macroeconomic conditions. In practice, PiT PD estimates are most often obtained through the conversion of their Through-the-Cycle (TtC) counterpart. As the Vasicek model has long stood as the industry-standard for this conversion, Zanders is continuously driving model enhancements through novel research. This research delves into modern adaptations of the industry-standard Vasicek methodology.

This article highlights collaborative research involving 17 students from Erasmus University Rotterdam, aiming to infuse greater granularity into credit risk modeling. Research was conducted by four student teams in the form of a group seminar project. Additionally, one student investigated this topic as part of her master thesis. By integrating both advanced statistical and machine learning techniques, this research showcases how modern adaptations could be introduced to redefine the traditional Vasicek framework, offering deeper insights into PD conversion methodologies. These enhancements provide flexibility and interpretability and contribute to a more extensive modeling toolkit.

Background

Compliance with International Financial Reporting Standard (IFRS 9) requires companies to obtain PiT PD estimates, which are influenced by macroeconomic variables. Banks reporting under IFRS 9 often use the TtC counterpart as a starting point, making use of various different conversion techniques to obtain the PiT PD (also our previous blog post A comparison between Survival Analysis and Migration Matrix Models). The industry-standard methodology to obtain these is by means of conversion through the Vasicek framework. The TtC PD reflects the PD irrespective of systemic factors, thereby reflecting the long-term average of the PD. Contrarily, the PiT PD reflects the probability that a party defaults at a specific point in the macroeconomic cycle, implying that PiT PD estimates fluctuate throughout the macroeconomic cycle. The mathematical technique introduced by Vasicek in 1977 and formalized in 2002 (Vasicek, An equilibrium characterization of the term structure, 1977; Vasicek, The distribution of loan portfolio value, 2002), serves as the industry-standard method for performing this conversion, integrating both systematic and idiosyncratic risks.

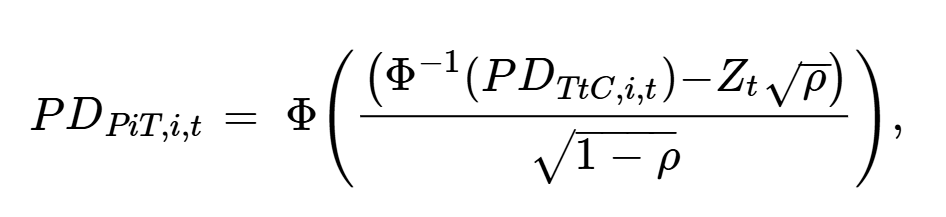

Understanding the Vasicek Model

Under the Vasicek model, the PiT PD can be derived from the TtC PD with the use of the Z-factor, which is defined as the state of the economy. The Z-factor corresponds to the systematic factor within the Vasicek framework and should be modeled as a function of macroeconomic variables. The linear regression constitutes a benchmark for modeling the Z-factor within the IFRS 9 framework due to its simplicity and the interpretability of its predictions. Formally, the Vasicek model is denoted as:

where PDPiT,i,t represents the PiT PD of firm i at time t. The economic state at time t is denoted as Zt, with ρ representing the correlation between firm i’s asset returns and the economic state. The Vasicek model assumes normality in asset returns and integrates both systematic and idiosyncratic risk, making it suitable for a broad range of applications.

Despite its simplicity and theoretical consistency, the model also faces critiques for its limitations under certain conditions (Basson & Van Vuuren, 2023), such as:

- Simplistic Linearity Assumptions

- Distributional Assumptions

- Static Correlation Structure

These limitations can cause inaccurate PD estimations resulting in poor risk management, which could be detrimental for financial institutions. The industry-standard model often struggles with the extreme economic scenarios or sector-specific variations that are the most informative to predict. As the IFRS 9 principles allow for more freedom with regards to the modeling usage (while still being explainable), these limitations lead to ongoing exploration for enhancements.

Extending the Vasicek Model

To improve the Vasicek model, three different approaches were considered. The first approach covers extending the Vasicek model to a non-linear model which does not rely on linear assumptions. Secondly, granularity is added to the Vasicek model by considering a multitude of Copula functions. Finally, the correlation between a firms asset returns and the economic state is made time- and industry dependent in order to relax the assumption of a static correlation structure.

Non-linear Techniques: Enhancing Z-Factor Modeling

The Z-factor is heavily influenced by many interconnected variables, with regulations and policies leading to increasingly complex dynamics that are difficult to accurately model. As of now, the industry-standard method to model the Z-factor is through the use of linear regression. However, one could argue that the real-world state of the economy rather exhibits non-linear patterns.

To introduce this non-linearity, many methodologies were considered, including statistical models such as regularized regressions and regime-switching models. Additionally, Machine Learning (ML) techniques, ranging from Gradient Boosting to Neural Network approaches, have been proposed to better capture the intricate relationships that cannot be captured by linear models. These techniques (partly) relax assumptions on the underlying data structures and help in understanding complex patterns in the data, offering improved estimation accuracy while minimizing overfitting risks. Such models are particularly beneficial when dealing with high-dimensional data where traditional approaches tend to underfit.

Our findings indicate that Z-factor estimation accuracy can significantly be improved upon, using models such as the regime-switching model or the long short-term memory neural network. These models showed significantly more accurate Z-factor estimation, both in-sample and out-of-sample. Other ML models included in this research do not show a significant increase in prediction accuracy as compared to the single factor Vasicek model. However, the use of these models also adds an extra layer of complexity to the modeling approach.

As IFRS 9 regulations require model predictions to be interpretable, frameworks such as SHapley Additive exPlanations (SHAP) can be introduced as a measurement tool. Although SHAP values do not equal full explainability, they can be used to assess feature importance and general insights into the identity and magnitude of important macroeconomic variables used for Z-factor prediction. This increased complexity and decreased interpretability of the modeling process, makes that additional academic and/or regulatory advancements need to be made before ML methods can be used within IFRS 9 frameworks. One could argue whether the additional complexity introduced by using ML models justifies the marginal increase in estimation accuracy.

Copula Approach: Distributional Flexibility

Risks are often aggregated over broad sectors or asset classes without considering nuances at more granular levels. Such a model may overlook specific risk drivers relevant to particular firms or industries, leading to less accurate PD estimates.

The second research direction involves using Copula-based methodologies to inject granularity into PiT PD estimations. Within the Copula approach, dependencies between random macroeconomic variables can be captured independently of their respective distributions. This approach thus allows for a more accurate description of the system’s behavior, where the system consists of m macroeconomic variables and the Z-factor. Moreover, each (macroeconomic) variable can be modeled by its empirical CDF, avoiding the need for parametric assumptions. The option to avoid making any distributional assumptions makes the copula approach very flexible.

By allowing for more flexible dependency structures, Copula models can provide a better representation of tail risks. This is particularly relevant for IFRS Stage 2 loans, which includes financial instruments that have shown a significant increase in credit risk since initial recognition. In this research a variety of conditional Copula models are considered and tested. The conditional Copula computes the distribution of the Z-factor conditional on the m macroeconomic variables in the system. Despite challenges like the Gaussian Copula’s inability to model joint extreme events effectively, alternatives such as the t-Copula show a statistically significant improvement over the benchmark Vasicek model. In particular, the copula models significantly reduce the amount of underestimation, a crucial advantage in the context of credit risk modeling.

In conclusion, results indicate that this approach significantly improves PD estimation, as compared to the benchmark Vasicek model, while interpretability and marginal flexibility stays intact. However, it does introduce a higher degree of complexity within the model compared to the linear benchmark model. Hence, we consider this method to be a promising area of future research for PD estimation.

Time and Industry Varying Correlation Structure

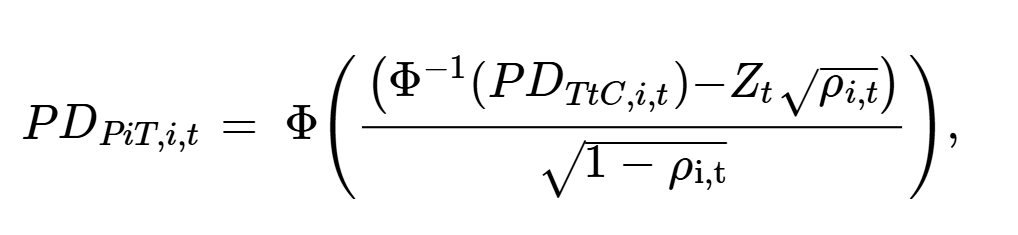

The industry-standard Vasicek model assumes a constant correlation across industries and time periods. In reality, correlations among default events can change over time and/or vary across industries due to economic cycles or industry specific shocks. This presents a research opportunity to enhance the practical applicability by incorporating sectoral dynamics and temporal variations within the correlation parameter of the model. Resulting in the following equation:

where the correlation parameter ρi,t is unique for firm i at time t. This segmentation is not limited to industries and time periods, but could also be extended across different regions or size classes, depending on the specific portfolio that is being considered. The correlation parameter ρi,t is modeled with a beta-distribution with time-varying mean and is defined on the interval between 0 and 1. The mean of the beta distribution is modelled as a logit link function driven by company-specific data (Ferrari & Francisco, 2004). This method thus allows for the temporal dependency to change over time, taking into account that the underlying relationship of the data does not remain identical across different time periods. Implementing varying correlations allows PD models to adapt and reflect real-world scenarios more precisely, ultimately leading to more robust credit risk predictions.

Results indicate that this approach significantly improves PD estimation accuracy, as compared to the benchmark Vasicek model. Moreover, this improvement is realized while the interpretability and logic of the benchmark model stays intact. Therefore, we consider this improvement to be a general improvement to existing Vasicek frameworks!

Conclusion

In this research, we have examined several different improvements with regards to PD modeling under IFRS 9 by using a Vasicek model, which is the industry standard. The first approach focused on extending the Vasicek framework by including non-linearity through advanced statistical and machine learning models. It was found that the regime-switching model and the long short-term memory neural network significantly improved Z-factor prediction accuracy. However, the increased complexity and the decreased interpretability of these models raises the question whether the gains of these approaches outweigh the additional efforts in practical applications.

Secondly, a conditional copula approach was introduced to capture the dependencies between macroeconomic variables and the Z-factor. The Copula models demonstrated exceptionally good relative performance in certain industries. Overall, the t-Copula proved to be the best Copula model in terms of overall predictive accuracy, significantly outperforming the standard Vasicek model. However, introducing a Copula model does lead to a higher degree of complexity within the model framework.

Lastly, we have incorporated a time and industry varying correlation parameter into the standard Vasicek model, thereby relaxing the static assumption implied by the original model. The use of this approach shows promising results, with PD estimation accuracy increasing significantly. This methodology is a simple yet important extension of the Vasicek framework that improves estimation accuracy while maintaining a level of simplicity and interpretability.

To conclude, we find that various methodologies can be introduced to challenge the existing Vasicek framework. Findings indicate that a number of models improve estimation accuracy, However, in some cases the marginal increase in accuracy does not weigh up against the additional efforts that are necessary to use these models in practice. The methodology that we would focus on in actual use-cases is the inclusion of time- and industry-varying correlations, which has shown positive results that are both theoretically consistent and remain interpretable and compliant with IFRS 9 regulations.

By extending the Vasicek model, Zanders continues to contribute valuable insights, supporting the financial industry's shift to a more comprehensive modeling toolkit. These advancements highlight our commitment to developing solutions that meet modern accounting and regulatory standards while providing financial risk managers with enhanced tools for risk estimation.

Are you interested in how you could leverage these methodologies to enhance your PD modeling approach? Contact Kasper Wijshoff, Kyle Gartner or Mila van den Bergh for more information.

Bibliography

Basson, L. J., & Van Vuuren, G. (2023). Through-the-cycle to Point-in-time Probabilities of Default Conversion: Inconsistencies in the Vasicek Approach. International Journal of Economics, 13(6), 42-52.

Ferrari, S., & Francisco, C.-N. (2004). Beta regression for modeling rates and proportions. Journal of applied statistics, 31(7), 799-815.

Vasicek, O. (1977). An equilibrium characterization of the term structure. Journal of financial economics, 177-188.

Vasicek, O. (2002). The distribution of loan portfolio value. Risk, 160-162.

On May 14th 2025, the European Banking Authority (EBA) published the fourth report on the monitoring of the liquidity coverage ratio (LCR) and net stable funding ratio (NSFR) in the European Union. The report includes an assessment and updated guidance for four topics, which are discussed in this article.

Inflows from open reverse repos

In May 2024 the EBA stated1 that inflows from open reverse repos cannot be recognised in LCR calculations unless the call option has already been exercised, or the institution can demonstrate that the repos would be called under specific circumstances Given the ambiguity and interpretive room in the initial statement, the EBA now provides two approaches that institutions may use to substantiate when such repos would be called.

- The first approach is forward-looking and states that banks can include the inflows in case they clearly specify events whose occurrence triggers the call of the option of the repo. The deadline of calling the option should also be shorter than 30 days.

- The second approach is backward-looking and allows banks to use their historic data. If banks can show that certain events have historically led to calling the option within 30 days, the inflows from the repos can be included in LCR calculations. The EBA stresses that the historical observations must have occurred during a period of stress of at least 30 days to ensure that reputational issues under such scenario are taken into account.

Operational deposits and excess operational deposits

Outflows of operational deposits, defined as deposits received for the purposes of obtaining clearing, custody, cash management or other comparable services, are significantly lower than those of non-operational deposits. Moreover, operational deposits are generally less vulnerable to significant withdrawals during a period of idiosyncratic or market-wide stress. As a result, operational deposits may be treated differently from non-operational deposits in LCR calculations. EBA’s first report (2019)2 on the monitoring of the LCR implementation already provided additional guidance on identifying operational deposits. However, based on a recent survey of competent authorities, the EBA found there may be divergence in the way institutions demonstrate the existence of legal or operational limitations that make significant withdrawals within 30 calendar days unlikely. Additionally, quite some heterogeneity was observed in the modeling techniques used to identify excess operational deposits.

To promote a level-playing field, the EBA now provides further regulatory guidance. It emphasizes the importance that institutions have a framework in place that provides a proper and evidence-based mapping of deposits to the different deposit types recognized in the LCR regulation (i.e. stable retail deposits, non-stable retail deposits and operational deposits). It is also noted that the length of the trade cycle used to identify excess operational deposits should reflect the specific characteristics of the client’s business model. Finally, prudent statistical measures should be applied when analysing historical deposit balances or payment flows.

Retail deposits excluded from outflows

Retail term deposits with a maturity beyond 30 days may be exempted from outflows in LCR calculations. Institution may exclude such deposits if they can demonstrate, on economic or contractual grounds, that the deposits will mature beyond 30 days. EBA’s first report on the monitoring of the LCR implementation (2019) already provided guidance on how to assess whether deposits mature beyond 30 days for economic reasons. Given the significant increase in term deposits in recent years, the EBA has reviewed whether this guidance remains adequate.

Overall, competent authorities report that the 2019 guidelines are properly implemented across the industry. However, the definition of a ‘material’ penalty for early termination under the LCR still leaves room for interpretation. This may lead to wrongly classifying term deposits as having a maturity beyond 30 days. To address this, the EBA now requires that historical data show a material penalty was applied to all early redemptions of exempted retail term deposits, even during periods of rising interest rates.

Interdependent assets and liabilities in NSFR

Under the CRR, banks can exclude assets and liabilities from NSFR calculations if they appear on the balance sheet only because the bank serves as a pass-through unit to channel the funding from the liability into the corresponding asset.3 Often times, these are derivatives from clients that are passed through to Central Counterparties (CCPs) in order to provide the client access to central clearing.

In the report, the EBA highlighted some unclarities around the eligibility of indirect client clearing activities where affiliated institutions are used to clear derivatives. To further clarify when such activities are eligible to be excluded from NSFR calculations, the EBA suggested a slight adjustment to the regulatory CRR text. This does not have any practical implications to the requirements around NSFR.

Conclusion

The fourth report on the monitoring of LCR and NSFR by the EBA provides additional guidance on four regulatory unclarities around LCR and NSFR. For three of the topics, all related to LCR, there is an impact on the implementation of the liquidity metric:

1- Banks may include inflows from open reserve repos when they demonstrate that the repos would be called within 30 days in a period of stress. This can be done by clearly stating this in the liquidity risk management policy or by showing that this has historically been the case.

2- Banks should have proper frameworks in place to map deposits to different deposit types, should ensure that the length of the trade cycle used to identify excess operational deposits reflects the client’s business model and should ensure that prudent statistical measures are applied when analyzing historical deposit balances.

3- Banks have to show with historical data that material penalties were applied to prematurely terminated retail term deposits before the term deposits can be excluded from LCR outflows.

The EBA provided clear instructions to follow up for the inflows from open reverse repos and the outflows from retail term deposits, but the additional guidance for (excess) operational deposits still leaves some ambiguity. Especially the statement that institutions should refer to ‘prudent statistical measures’ leaves room for interpretation. Nevertheless, the additional remarks made by the EBA indicate that competent authorities are likely to increase focus on the (liquidity-typical) modeling of operational deposits and on the calculation of LCRs in general.

Zanders has extensive experience within the field of liquidity risk and supported clients on:

- Developing a model to split operational and non-operational deposits on account-by-account level, together with the incorporation in LCR.

- Validating liquidity risk models (LCR and NSFR) as independent validator, delivering clear reports including substantiated findings and pragmatic recommendations.

- Designing a liquidity risk roadmap to obtain regulatory compliance and to set a solid foundation for managing liquidity risk.

Reach out to Erik Vijlbrief or Jelle Thijssen for more information.

Citations

- See Q&A 2024_7053 for more information. ↩︎

- EBA reports on the monitoring of the LCR implementation in the EU | European Banking Authority ↩︎

- The conditions set out in Article 428f of the CRR must be met. ↩︎

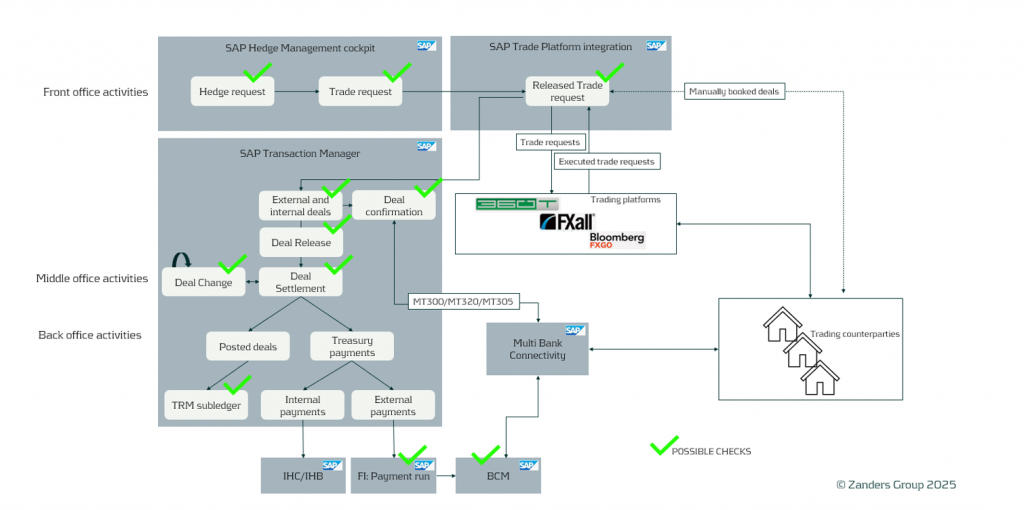

This article explores SAP Treasury and Risk Management (TRM) controls and automation frameworks, with a focus on design and implementation challenges, as well as on the ongoing validation of the controls to ensure they are efficient, seamless and reliable.

This article is intended for finance, risk, and compliance professionals with business and system integration knowledge of SAP, but also includes contextual guidance for broader audiences.

1. Introduction

SAP Treasury and Risk Management (SAP TRM) provides a robust framework to meet the need for enhanced transparency, mitigate financial risks, and ensure regulatory compliance, but its effectiveness depends on the correct implementation of control mechanisms and automated checks.

In Japan, the approach to financial and treasury management is influenced by principles of Kaizen (continuous improvement) and high-quality process control. The core emphasis is on minimizing errors, enhancing efficiency, and ensuring the reliability of Treasury management systems.

The approach aligns with the necessity of seamless internal controls in SAP TRM, where even minor inconsistencies can lead to significant financial risks and losses.

This article outlines key controls within SAP TRM, provides practical implementation steps, and explores AI-driven enhancements that improve compliance, security, and operational efficiency.

2. SAP TRM: Key Areas Requiring Controls

SAP TRM covers a broad range of treasury functions, each requiring specific control mechanisms:

- Transaction Management: Handling financial instruments such as FX, money markets, securities, derivatives, etc.

- Risk Management: Identifying and mitigating market and credit risks.

- Cash and Liquidity Management: Real-time cash positioning and cash flow forecasting, and optimization.

- Hedge Management and Accounting: Compliance with IFRS 9 and other standards.

3. How SAP TRM Supports Real-Time Risk Control

A solid control framework requires detailed analysis, alignment, and structured implementation. Below are some key controls that should be assessed and implemented within transaction management of SAP TRM. In the picture, the areas where possible checks can be applied are highlighted:

Deal Release (Approval) Control

Ensuring proper authorization and validation before a deal is released (approved internally) is essential to prevent unauthorized or erroneous transactions from being booked, modified, and processed in SAP.

Proposed configuration objects to consider:

- Business Rule Framework Plus (BRFplus): Define validation checks, such as ensuring that only authorized users can release deals above a certain value.

Deal Settlement Control

Settlement is SAP term for the deal confirmation with counterparties. The deal status is changed to "Settlement" immediately after confirmation.

Accurate deal confirmation is crucial to avoid financial mismatches or discrepancies in payment details. The settlement process is required for all external deals and may also be needed for intercompany deals. Settlement is required for every key lifecycle step of a deal: creation, NDF fixing, rollover, option exercise, etc. Settlement can be done manually or automatically upon counter-confirmation of the correspondence (MT300, MT320, MT305, or deal confirmation messages).

Proposed configuration objects to consider:

- Set up automated reports to track unsettled deals within a specific timeframe (as of today or as of the current week).

- SAP Fiori app “Display Treasury alerts” is an effective solution for this.

Ensuring Transaction Integrity: Key Checks in SAP

Automating the matching process minimizes manual errors and improves operational efficiency, reducing the time required for this process.

Proposed configuration objects to consider:

- Define a report to show all pending unmatched correspondences. This is often proposed as a control over the matching process. It can be implemented using the Correspondence Monitor or the Fiori app "Display Treasury Alerts."

Restricted Deal Modifications

To prevent unauthorized modifications of the treasury transactions that could lead to fraudulent or erroneous results, deal changes should be strictly controlled. We do not recommend allowing deals in status Settlement (after confirmation matching process) to be changed—especially key matching fields such as amounts, value dates, and currencies. However, modifications may be required from time to time. In such cases, they need to be controlled and may require another round of verification and counter-confirmation matching.

Proposed configuration objects to consider:

- Enable Change Log Activation: Use SAP Audit Information System (AIS) to track modifications and maintain audit trails for TRM.

- Implement SAP TRM Deal Approval Workflow: Require validation and approval for all deal amendments and reversals.

- Restrict critical field modifications: Configure SAP field selection variant to lock key fields of the deals from being altered after deal approval/settlement.

- Enforce Segregation of Duties (SoD): Ensure different users handle deal creation, approval, settlement processing, and modifications to prevent errors or fraud.

Deal Payment Controls Using BCM Approvers

Ensuring that deal payments go through the correct approval process reduces financial risk and enhances security. It is important to define unusual treasury payment scenarios, such as when cash flow processing occurs outside normal business hours.

Proposed configuration objects to consider:

- Implement a Payment Block Mechanism: Ensure that payments are blocked unless predefined criteria are met, or review and approval is done/granted.

- Automated Exception Handling: Configure Bank Communication Management (BCM) rules to flag transactions that deviate from standard payment behavior, requiring manual review before processing (e.g., payments to a new business partner or deals posted outside normal business hours).

4. AI-Driven Enhancements for Treasury Control

AI is transforming treasury processes by automating risk detection, optimizing forecasting, and enhancing decision-making. Key AI-powered enhancements in SAP TRM include:

- Fraud Detection: Machine learning models in SAP Business Technology Platform (BTP) to detect suspicious transactions.

- SAP Business Integrity Screening: AI-driven software from SAP that improves anomaly detection, risk identification, and compliance checks.

- Automated Matching: AI-powered bots in SAP Intelligent RPA match transactions (especially when non-SWIFT correspondence is used), helping eliminate manual errors.

5. Best Practices for SAP TRM Control Optimization

The following best practices are recommended as part of the business-as-usual process:

- Conduct regular Role & Authorization reviews: Update SAP GRC, Governance, Risk, and Compliance, settings to align with changes in Treasury team structure.

- Leverage SAP Fiori apps for real-time analytics and visibility into treasury processes, ensuring that no payments are stuck and that all back-to-back and mirroring deals are in place and processed on time.

- Create and integrate AI-powered tools: Deploy SAP AI solutions to enhance risk analysis, compliance monitoring and decision-making.

- Adopt a Kaizen approach: Continuously monitor and refine TRM controls to improve efficiency and accuracy, as technology is rapidly evolving and controls must remain valid and preventive.

6. Conclusion

Implementing strong controls in SAP TRM is critical for maintaining compliance, minimizing financial risks, and improving operational efficiency.

By leveraging SAP’s built-in functionalities—along with AI-driven enhancements—corporate treasurers can create a secure, transparent, and highly automated treasury management process. By integrating Kaizen principles and AI-driven automation, companies can transform their treasury operations into a continuously improving and highly efficient Treasury Management System.

Zanders consultants are deeply involved in this crucial topic, which can be addressed as a standalone initiative to improve controls, as part of ongoing treasury support, or within an SAP TMS implementation project. We are ready and eager to help your company enhance system controls and checks in SAP TRM.

For more information, please contact Aleksei Abakumov.

Case Study: SAP TRM in Practice

A multinational, multibillion-dollar company operating across the globe, with its HQ in Tokyo, Japan, implemented SAP TRM. By using J-SOX controls (both business and system) in SAP TRM, the company managed to build world-class, secure control mechanisms that are used and applied throughout the entire organization, across all markets. The company regularly validates these controls and challenges them when they are obsolete or adds new controls if needed due to changing external conditions.

In today’s rapidly evolving financial landscape, organizations are seeking efficient and secure solutions for payment processing.

Our team at Zanders has been at the forefront of implementing BACS AUDDIS (Automated Direct Debit Instruction Service) with SAP S/4HANA, helping clients to streamline their direct debit management while ensuring regulatory compliance.

Why BACS AUDDIS Matters

BACS Direct Debit is the UK's electronic direct debit service, enabling organizations to collect payments directly from customers' bank accounts. This service offers numerous advantages, including predictable cash flow, reduced administrative overhead, and improved operational efficiency.

The implementation of AUDDIS enhances this process by allowing organizations to electronically send Direct Debit instructions to the banking system. This digitization eliminates paper-based processes, reduces operational costs, and improves overall processing speed.

The Advantage

Our approach for AUDDIS implementation with SAP S/4HANA provides a bespoke solution that supports AUDDIS requirements, built on top of the standard SAP S/4HANA functionality. What sets our approach apart is our deep expertise in complex, mission-critical financial system implementations specifically tailored for market leading organizations.

The solution development leverages the full range of SAP's Direct Debit (DD) capabilities supplemented by our extensive experience in Treasury and Payment systems. This creates a seamless integration with existing SAP finance processes while ensuring full compliance with BACS standards.

The Solution

The solution developed supports the full cycle of BACS Direct Debit (DD) mandate management in SAP, from new mandate registration to mandate amendments, cancellation, and dormancy assessment.

Mandate information and amendments are automatically interfaced in XML format (PAIN.008) in compliance with BACS requirements, transmitting from the SAP Payment Hub to BACS through a BACSTEL-IP service provider.

Furthermore, to ensure a smooth and streamlined direct debit collection process, the custom solution enhances SAP’s automatic payment program with additional features.

These include verifying the validity of the customer or alternative payee’s mandate status at the payment proposal stage, considering DD collection lead periods.

This ensures that only customers with an active mandate status are included in the payment run. In addition, SAP’s Data Medium Exchange (DME) engine has been extended to include the mandatory mandate reference attributes in the bank interface.

Our Four-Phase Implementation Approach

Every AUDDIS implementation follows four key stages:

1 - Application: The corporate entity applies to its sponsoring payment service provider for AUDDIS approval.

2 - Preparation: After approval, the corporate prepares its internal systems, ensuring software, processes, and infrastructure are in place for AUDDIS integration.

3 - Testing: The corporate submits test files to BACS to validate both compliance and successful transmission.

4 - Go-Live: The corporate transitions to using the AUDDIS service either as a ‘live’ user from the start or by migrating first before going live. This is the final stage of the AUDDIS implementation process, and exactly what this entails depends on whether the corporate is joining AUDDIS with a new Service User Number or with an existing one, and therefore, has a migration (to onboard existing customer mandates to AUDDIS) to complete.

AUDDIS implementation projects require ongoing coordination with Banking Partners, System Integrators and Business Process Teams. This includes the process of creating BACS Service User Numbers, extensively testing bank interfaces for AUDDIS and Direct Debit Instruction files. At go-live, detailed coordination is required to support penny testing.

The results after implementation

Our clients report significant benefits from implementing BACS AUDDIS with our support, including:

- Enhanced management of Direct Debit (DD) mandates

- Reduced processing costs and improved operational efficiency

- Ensured compliance with banking and regulatory requirements

- Accelerated payment cycles through streamlined processes

By partnering with Zanders, organizations gain a trusted advisor in BACS AUDDIS implementations. Our expertise ensures smooth transitions while maintaining business continuity throughout the process.

For more information on how we can support your organization's transition to BACS AUDDIS with SAP S/4HANA, please contact Eliane Eysackers or Nadezda Zanevskaja.

Electronic Withholding Tax System Modernizes Payment Processes.

Thailand's e-Withholding Tax (e-WHT) system officially launched on October 27, 2020, in collaboration with 11 banks, marking a significant digital transformation with far-reaching benefits for corporate treasurers. This system was introduced to streamline the process of withholding tax by allowing taxpayers to remit taxes electronically through participating banks. The initiative aimed to enhance convenience for taxpayers and reduce the administrative burden associated with traditional tax filing methods. To encourage adoption, the government implemented measures such as reducing withholding tax rates for those utilizing the e-WHT system.

Thailand's Digital Tax Evolution

The e-WHT system aligns with Thailand's digital transformation strategy, offering corporate treasurers an opportunity to modernize tax processes and enhance cash flow management. This initiative reflects Thailand's commitment to creating a more efficient business environment through technology.

What Corporates Need to Know

Companies conducting business in Thailand are required to withhold tax on certain payments including:

- Service fees

- Professional fees

- Royalties

- Interest

- Dividends

- Rent/Lease

Once the tax is withheld, businesses must submit the amount to The Revenue Department, part of the Thai Ministry of Finance. This requirement applies to both domestic and foreign companies conducting business in Thailand.

e-WHT only applies to domestic electronic payments. Paper cheques must continue to follow the traditional paper WHT model.

Key Benefits for Treasury Departments

The adoption of e-WHT offers multiple strategic advantages:

- Improved cash flow visibility – provides real-time status of tax-related movements, enabling more efficient WHT monitoring

- Simplified documentation – reduces the risk of human error in tax calculations and documentation procedures

- Accelerated processing times – shortens the tax filing and refund cycles

- Enhanced compliance – reduces the risk of non-compliance

- Better reconciliation – enables real-time verification of taxes withheld and credits

Implementation Insights

Our treasury technology specialists have assisted companies operating in Thailand with the successful implementation of e-WHT submissions, covering domestic payment types such as ACH and RTGS via Standard Chartered Bank (SCB).

Key insights from these implementations include the importance of establishing dedicated interfaces from ERP S/4 HANA systems to the banking file gateway linked to Thailand's Revenue Department for seamless e-WHT processing.

Impact on Corporate Operations and User Experience

The introduction of e-WHT has streamlined tax filing for companies in Thailand, marking a significant shift toward digital transformation and compliance.

From a user experience perspective, companies can expect the following:

- No need to issue or store paper-based withholding tax certificates

- No manual month-end tax submissions to the Revenue Department

- Reduced document handling and storage costs

- Verification of withholding tax records by beneficiaries via the Revenue Department’s website

- Reduced withholding tax rates for eligible businesses

Looking Ahead: Strategic Implementation Considerations

When planning for e-WHT implementation, treasurers should keep the following in mind:

- Errors in tax rates cannot be corrected once submitted

- Faster tax payment cycles may require adjustments in cash flow planning

- Managing both paper and electronic WHT processes requires additional oversight and potential training for finance teams

For corporate treasurers, e-WHT represents an opportunity to modernize tax procedures, improve processing efficiency, and embrace digital transformation. Companies that properly plan the adoption of this initiative will align with Thailand's digital tax strategy while gaining operational benefits.

For more information on navigating Thailand's e-WHT implementation for your organization, please contact our Treasury Technology specialists.

Heightened market uncertainty means that Financial Risk Management remains a key focus for multinational corporations.

In today’s rapidly evolving financial landscape, fortifying the Financial Risk Management (FRM) function remains a top priority for CFOs. Zanders has identified a growing trend among corporations striving to modernize their current FRM practices to achieve comprehensive risk visibility, advanced risk quantification, and a holistic, proactive and integrated approach to risk management. These efforts aim ultimately to boost shareholder value. The Zanders Financial Risk Management Framework offers multinational corporations a tested and structured methodology to meet these objectives. In this article, we delve into this approach and explore the benefits it can bring to your organization.

Financial Risks as a Collateral Effect:

To better understand the role of FRM in a corporate setting, it's helpful to define its scope. FRM involves identifying, measuring, and managing financial risks such as market risk (including foreign exchange, interest rate, and commodity risk), liquidity risk, and credit risk. These risks often arise as side effects of inherent business risks. Business risks originate from core activities like international trade, working capital investments, capital expenditures, and supply chain design. Shareholders typically invest in companies to gain exposure to and be compensated for these specific business risks, while often viewing financial risks as unfavorable side effects. Therefore, aligning a company’s FRM practices with shareholders’ expectations is crucial.

Increased market volatility often triggers FRM initiatives. Additionally, several internal and external factors prompt companies to reevaluate their FRM frameworks, including:

- Geopolitical instability

- MADS events (Mergers, Acquisitions, Divestitures, Spin-offs)

- Organic growth, especially expansion into emerging markets

- Changes in the regulatory landscape

- Aspirations to adopt innovative, best-in-class practices

A well-defined FRM framework is important for any organization, as it provides clarity on how financial risks are managed. By maintaining an up-to-date and well-structured FRM framework, companies can respond more proactively to changing market conditions and ensure better alignment with shareholder goals.

Holistic vs. Integrated Financial Risk Management

The landscape of FRM is evolving, with multinational corporations (MNCs) shifting from a silo-based approach to a more holistic strategy. In this modernized approach, various market risks, along with their connections to liquidity risk and the company's credit profile, are analyzed comprehensively. The new standard for treasurers increasingly involves quantitative methodologies to measure the potential impact of financial risks on key financial metrics—such as earnings, net income, and financial covenants—using "at-risk" quantification measures like earnings-at-risk (EaR). These "at-risk" methodologies are increasingly utilized to inform strategic decisions or reduce hedging costs. An illustration of this is the utilization of efficient frontier analysis to achieve optimal hedging costs for a particular "at-risk" level.

In addition to adopting a holistic FRM approach, Zanders has observed a growing trend towards greater business integration. Effective FRM requires seamless integration between the treasury function and the broader business organization. By embedding treasury within the business processes, companies can add significant value through the early identification of financial exposures and by anticipating the financial risk implications of business decisions at their inception. Tools such as Risk Adjusted Return on Sales (RAROS) exemplify this integrated approach. With RAROS, FRM becomes an integral part of the commercial process, where the financial risks of specific transactions are quantified to determine their true economic value-add.

The shift towards holistic and integrated FRM empowers organizations to not only manage risks more effectively but also to drive value creation and enhance financial resilience.

Zander’s Risk Management Framework

As financial risk managers, it's important to take a holistic approach to FRM. At Zanders, we suggest that our clients use a structured 5-step FRM framework.

The framework is applied as follows:

1- Identification: Establish the risk exposure profile by identifying all potential sources of financial exposure, classifying their likelihood and impact on the organization, and prioritizing them accordingly.

2- Measurement: Risk quantification involves a detailed quantitative analysis of the exposure profile. This includes assessing the probability of market events and quantifying their potential impact on financial parameters using techniques such as sensitivity analysis, scenario analysis, and simulation analysis (for example, cash flow at risk, value at risk).

3- Strategy & Policy: With a clear understanding of the existing risk profile, the objectives of the risk management framework are defined, considering the specific goals of various departments such as finance, operations, and procurement. A hedging strategy is then developed in alignment with these established financial risk management objectives.

4- Process & Execution: This phase follows the development of the hedging strategy, where the toolbox for hedging is defined, and roles and responsibilities are clearly allocated within the organization.

5- Monitoring & Reporting: All activities should be supported by consistent monitoring and reporting, with exception handling capabilities and risk assessments shared across departments.

Conclusion

Amid today's unpredictable financial markets, organizations are placing greater emphasis on FRM. Establishing a future-proof FRM framework is necessary not only for safeguarding key financial parameters and enhancing risk visibility but also to support long-term business sustainability. A robust FRM framework empowers companies to communicate more effectively with debt and equity investors, as well as other stakeholders, about their financial risks. Additionally, effective financial risk control can lead to better credit ratings, thereby improving access to liquidity under more favorable conditions.

To achieve a comprehensive and successful transformation of all key areas in FRM, a structured and proven project approach is indispensable.

Why Choose Zanders?

- Comprehensive, Integrated, and Strategic Approach: Our focus is on managing financial risk to enhance shareholder value.

- Advanced Tools: We utilize extensive proprietary benchmarking and advanced risk modeling tools.

- Expertise and Experience: With over 500 treasury and risk professionals, we cover the full spectrum of FRM with deep subject matter expertise.

- Proven Track Record: Excellent references and client testimonials underscore our extensive knowledge base and successful track record in Financial Risk Management.

- Strategic Insight and Implementation Capability: We combine strategic knowledge of treasury and risk best practices with the ability to implement these solutions effectively.

In an ever-changing financial landscape, Zanders provides the expertise and structured approach necessary to build a resilient FRM framework, ensuring your organization is well-equipped to navigate future challenges while enhancing financial stability and shareholder value. To learn more, contact us.

Emergence of Artificial Intelligence and Machine Learning

The rise of ChatGPT has brought generative artificial intelligence (GenAI) into the mainstream, accelerating adoption across industries ranging from healthcare to banking. The pace at which (Gen)AI is being used is outpacing prior technological advances, putting pressure on individuals and companies to adapt their ways of working to this new technology. While GenAI uses data to create new content, traditional AI is typically designed to perform specific tasks such as making predictions or classifications. Both approaches are built on complex machine learning (ML) models which, when applied correctly, can be highly effective even on a stand-alone basis.

Figure 1: Model development steps

Though ML techniques are known for their accuracy, a major challenge lies in their complexity and limited interpretability. Unlocking the full potential of ML requires not only technical expertise, but also deep domain knowledge. Asset and Liability Management (ALM) departments can benefit from ML, for example in the area of behavioral modeling. In this article, we explore the application of ML in prepayment modeling (data processing, segmentation, estimation) based on research conducted at a Dutch bank. The findings demonstrate how ML can improve the accuracy of prepayment models, leading to better cashflow forecasts and, consequently, a more accurate hedge. By building ML capabilities in this context, ALM teams can play a key role in shaping the future of behavioral modeling throughout the whole model development process.

Prepayment Modeling and Machine Learning

Prepayment risk is a critical concern for financial institutions, particularly in the mortgage sector, where borrowers have the option to repay (a part of) their loans earlier than contractually agreed. While prepayments can be beneficial for borrowers (allowing them to refinance at lower interest rates or reduce their debt obligations) they present several challenges for financial institutions. Uncertainty in prepayment behaviour makes it harder to predict the duration mismatch and the corresponding interest rate hedge.

Effective prepayment modeling by accurately forecasting borrower behavior is crucial for financial institutions seeking to manage interest rate risks. Improved forecasting enables institutions to better anticipate cash flow fluctuations and implement more robust hedging strategies. To facilitate the modeling, data is segmented based on similar prepayment characteristics. This segmentation is often based on expert judgment and extensive data analysis, accounting for factors like loan age, interest rate, type, and borrower characteristics. Each segment is then analyzed through tailored prepayment models, such as a logistic regression or survival models.1

ML techniques offer significant potential to enhance segmentation and estimation in prepayment modeling. In rapidly changing interest rate environments, traditional models often struggle to accurately capture borrower behavior that deviates from conventional financial logic. In contrast, ML models can detect complex, non-linear patterns and adapt to changing behaviour, improving predictive accuracy by uncovering hidden relationships. Investigating such relationships becomes particularly relevant when borrower actions undermine traditional assumptions, as was the case in early 2021, when interest rates began to rise but prepayment rates did not decline immediately.

Real-world application

In collaboration with a Dutch bank, we conducted research on the application of ML in prepayment modeling within the Dutch mortgage market. The applications include data processing, segmentation, and estimation followed by an interpretation of the results with the use of ML specific interpretability metrics. Despite being constrained by limited computational power, the ML-based approaches outperformed the traditional methods, demonstrating superior predictive accuracy and stronger ability to capture complex patterns in the data. The specific applications are highlighted below.

Data processing

One of the first steps in model development is ensuring that the data is fit for use. An ML technique that can be commonly applied for outlier detection is the DBSCAN algorithm. This clustering method relies on the concept of distance to identify groups of observations, flagging those that do not fit well into any cluster as potential outliers. Since DBSCAN requires the user to define specific parameters, it offers flexibility and robustness in detecting outliers across a wide range of datasets.

Another example is an isolation forest algorithm. It detects outliers by randomly splitting the data and measuring how quickly a point becomes isolated. Outliers tend to be separated faster, since they share fewer similarities with the rest of the data. The model assigns an anomaly score based on how few splits were needed to isolate each point, where fewer splits suggest a higher likelihood of being an outlier. The isolation forest method is computationally efficient, performs well with large datasets, and does not require labelled data.

Segmentation

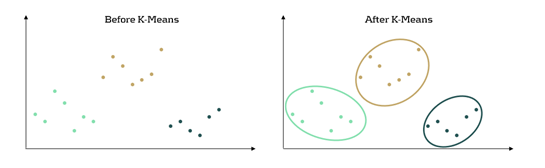

Following the data processing step, where outliers are identified, evaluated, and treated appropriately, the next phase in model development involves analyzing the dataset to define economically meaningful segments. ML-based clustering techniques are well-suited for deriving segments from data. It is important to note that mortgage data is generally high-dimensional and contains a large number of observations. As a result, clustering techniques must be carefully selected to ensure they can handle high-volume data efficiently within reasonable timelines. Two effective techniques for this purpose are K-means clustering and decision trees.

K-means clustering is an ML algorithm used to partition data into distinct segments based on similarity. Data points that are close to each other in a multi-dimensional space are grouped together, as illustrated in Figure 2. In the context of mortgage portfolio segmentation, K-means enables the grouping of loans with similar characteristics, making the segmentation process data-driven rather than based on predefined rules.

Figure 2: K-Means concept in a 2-dimensional space. Before, the dataset is seen as a whole unstructured dataset while K-means reveals three different segments in the data

Another ML technique useful for segmentation is the decision tree. This method involves splitting the dataset based on certain variables in a way that optimizes a predefined objective. A key advantage of tree-based methods is their interpretability: it is easy to see which variables drive the splits and to assess whether those splits make economic sense. Variable importance measures, like Information Gain, help interpret the decision tree by showing how much each split reduces the entropy (uncertainty). Lower entropy means the data is more organized, allowing for clearer and more meaningful segments to be created.

Estimation

Once the segments are defined, the final step involves applying prediction models to each segment. While the segments resulting from ML models can be used in traditional estimation models such as a logistic regression or a survival model, ML-based estimation models can also be used. An example of such an ML estimation technique is XGBoost. The method combines multiple small decision trees, learning from previous errors, and continuously improving its predictions. It was observed that applying this estimation method in combination with ML-based segments outperformed traditional methods on the used dataset.

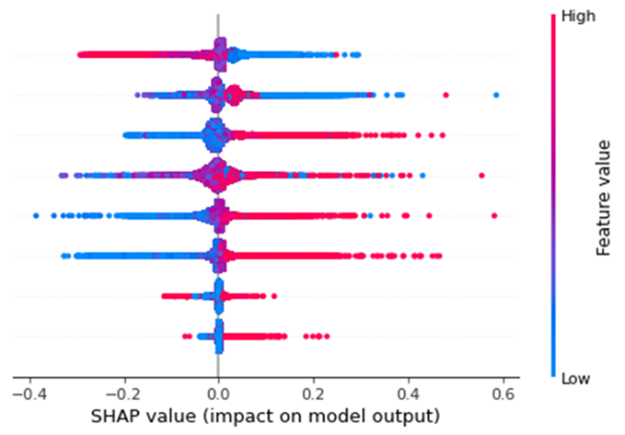

Interpretability

Though the techniques show added value, a significant drawback of using ML models for both segmentation and estimation is their tendency to be perceived as black-boxes. A lack of transparency can be problematic for financial institutions, where interpretability is crucial to ensure compliance with regulatory and internal requirements. The SHapley Additive exPlanations (SHAP) method provides an insightful way for explaining predictions made by ML models. The method provides an understanding of a prediction model by showing the average contribution of features across many predictions. SHAP values highlight which features are most important for the model and how they affect the model outcome. This makes it a powerful tool for explaining complex models, by enhancing interpretability and enabling practical use in regulated industries and decision-making processes.