A closer look at how banks quantify the Margin of Conservatism, and where the methods are starting to improve.

Zanders guided research by students at Erasmus University Rotterdam into emerging modeling techniques for the Margin of Conservatism (MoC) categories, and the results point to real opportunities for banks. The research has shown promising new techniques, particularly for MoC categories A and B, and for the aggregation of MoC into a single total figure. In this article, we examine how each MoC category is defined, how banks approach them today, and what innovative techniques are available to improve the balance between conservatism and capital requirements.

Category A - Data & Methodology Deficiencies

MoC addresses situations where known issues in data or model design could bias risk estimates. For example, a bank might discover gaps or errors in historical data or realize that a simplifying assumption in the model (like a coarse segmentation or incomplete risk drivers) introduces a bias. According to EBA's definitions, MoC A should cover "data and methodological deficiencies" identified in the modeling or calibration process (EBA, 2017).

If you find a material deficiency in your data or method, you should first try to address it directly via Appropriate Adjustments (AA) to your data or model (e.g. imputing missing values). However, if some bias or shortcoming remains unaddressed, you then quantify a conservative add-on to compensate for the residual uncertainty. The aim is to offset any potential underestimation of risk caused by known issues.

Current Market Practices

Banks often rely on expert judgment and simple scenario analyses to set MoC A adjustments. For instance:

1- If certain older data is deemed less reliable, common practices are to:

- Benchmark model results using a cleaner subset of data (or external data) to gauge the impact. The difference might be added as MoC A.

- Model the upper confidence bound of the parameter estimate and consequently set the add-on equal to the distance between the point estimate and the upper bound.

2- In some instances, analysts may even apply a qualitative add-on to risk parameters based on their expert judgment, sometimes amounting to a flat increase or a scaling factor.

These simpler approaches are easy to communicate but can be somewhat simple and subjective, making it hard to defend the resulting values to model validation and the regulator.

Emerging Techniques

Recent research has helped to quantify MoC A more objectively. One such is the probabilistic quantification approach proposed by (Biche, 2022). They establish a closed-form expression that does not rely on an arbitrarily predefined significance level, to model uncertainty arising from missing values in the calibration sample. Instead, the Biche-approach defines a quantification of MoC A which is derived from a purely probabilistic perspective, increasing consistency across institutions.

Another direction we have explored is a framework based on influence functions, a statistical technique introduced in (Hampel, 1974), that examines how small changes in individual data points or model inputs affect the final estimate. By measuring influence on model output, one can identify where data issues or outliers might be biasing the estimates and then derive an MoC A to counteract that bias. This method allows the user to identify observations that drive MoC adjustments without repeated model re-estimation.

Conclusion

While market practices still lean on simple and judgment-driven approaches, these are increasingly challenged from a regulatory perspective. Emerging quantitative techniques offer a more structured and transparent way to capture identified biases, helping institutions move toward more unified MoC A calibration.

Category B – Changes in Environment & Policies

Category B MoC addresses structural breaks or shifts in legal- and/or macro-economic policy. These breaks between the past and the present (or expected future) would imply that your historical calibration data is (partially) out-of-date. In practice, such shifts can stem from any relevant changes to underwriting standards, risk appetite, collection and recovery policies, or any other source of additional uncertainty about the future. Even if your data and model are flawless, the future may not resemble the past.

Suppose your bank significantly tightened its lending standards, or a new economic regime (like a financial crisis or pandemic) emerged. Your PD, LGD or EAD models, built on the last decade of data, might now be too optimistic or not fully relevant for today's portfolio and/or economic state. Regulation requires you to ensure that if tomorrow's world differs from yesterday's, your risk estimates have a buffer to cover that gap. This is achieved through MoC B.

One key challenge is that Category B issues often overlap with Category C or even Category A. For instance, a structural break (Category B) usually reduces the usable data length, which in turn increases estimation error (Category C). Some banks attempt to model these overlaps explicitly. Nevertheless, modelling the co-movement of the different MoC categories is still a novel area for most banks. Section 5 covers this topic in more detail.

Current Market Practices

Banks usually handle MoC B by blending statistical tests and scenario analysis:

1- Some use structural break tests on historical default or loss data to detect if and when behavior changed (for example, a Chow test might reveal a significant shift in default rates after a certain year or policy change). If a break is detected, this flags a deficiency.

2- Others apply simple ratio comparisons (scaling factors): e.g. comparing post-change default rates to pre-change. If the model calibration sample underrepresents a recent adverse period, they might scale up PDs or LGDs by the observed difference (or by an expert-determined factor) to be conservative.

Emerging Techniques

Advanced frameworks propose quantifying MoC B via scenario modeling: first create scenarios that reflect new processes or extreme macroeconomic conditions, then measure how much PD, LGD or EAD might change under those scenarios. The weighted differences from the base forecast can serve as the MoC B. This is more dynamic and connects modeling directly to the business.

Conclusion

While current practices often rely on relatively simple diagnostics and scaling approaches, these can struggle to fully capture shifts. More advanced, scenario-based frameworks offer a forward-looking and economically grounded alternative, enabling banks to align their MoC B quantification more closely with evolving portfolio characteristics and external conditions.

Category C – General Estimation Error

Finally, Category C MoC addresses the inherent statistical uncertainty present in risk parameter estimates. Regulation states that MoC C "should reflect the dispersion of the distribution of the statistical estimator" (EBA, 2017). As econometric models are estimated on finite data samples, there will always be a margin of error surrounding the estimated PD, LGD, or EAD. This error, also referred to as noise, is most prevalent in low-default portfolios.

Current Market Practices

There is a spectrum of approaches that each have pros and cons; the most common techniques are summarized in Table 1.

Many banks choose a confidence level (α) and compute MoC C so that the final estimate corresponds to a high-end confidence bound. For example, for PD one could use a binomial distribution of default rates to determine that the upper bound of the 95% confidence interval is X% higher than the observed long-run average default rate (LRADR). MoC C is then set equal to the difference between the two.

A simplified approach is the k·σ ("k-sigma") method: choose a multiplier k for the standard error (σ) of the risk parameter, and set MoC C = k × σ. For example, if a PD's standard error is 0.2 percentage points, applying k=1.96 (approx. 95% confidence) leads to a MoC of 0.39 percentage points.

Emerging Techniques

Category C is the most well-developed MoC category as it relates to the general estimation uncertainty, present in every econometric model. Hence, many quantification techniques have already been developed and are already in use.

Conclusion

Unlike Categories A and B, MoC C is methodologically well established, leading to widespread use of standardized techniques such as confidence intervals and k‑sigma approaches. The key challenge therefore lies less in innovation and more in selecting appropriate confidence levels and ensuring a consistent level of conservatism across portfolios.

| Technique | Pros | Cons |

| Parametric distribution | Assume defaults or losses follow a known statistical model. These often give higher, more stable MoCs and never result in zero or negative MoC. | Relies on model assumptions. |

| Empirical variance estimation | This is model-free and often simply uses the sample standard deviation of historical default rates. | Tends to give volatile results if data is scarce or correlated. |

| Resampling/Bootstrapping | Flexible (doesn't impose a parametric form) and ensures MoC is always positive. | Can be computationally heavy and may not improve accuracy if data is very limited. |

Aggregation – Beyond Simple Summation

After estimating MoC A, B, and C, how should banks combine them?

The simplest (and, in regulatory landscape, the default) approach is to sum the margins over the categories: MoC_Total = MoC_A + MoC_B + MoC_C. This straightforward sum ensures a conservative outcome and is in line with: "Institutions should quantify the final MoC as the sum of MoC A, MoC B and MoC C" (EBA, 2017). But this conservative simplicity comes at a cost.

Key issues with simple summation

1- Double Counting: The categories are not guaranteed to be truly independent. For example, a structural break (Category B) often reduces the data sample, increasing the estimation error (Category C). Simply adding margins implicitly assumes worst-case alignment of all uncertainties, that every deficiency, future change, and statistical error all push the risk estimate in the same adverse direction simultaneously. However, in practice some uncertainties might overlap or partially offset.

2- Confidence Level Mismatch: If each margin is set to cover a high percentile of uncertainty, then summing them could yield a combined cushion far beyond that percentile. If MoC A and B each target an approx. 90% confidence level, adding them to MoC C could result in overall conservatism beyond 99.9%, which is more than intended. This excess conservatism means higher capital requirements.

Emerging Techniques

At Zanders, we are conducting ongoing research to explore methods to aggregate MoC more analytically. One idea is to treat overall MoC as a target confidence interval problem: define the desired overall safety level (e.g. 90% or 95% confidence that the true risk parameter is below [PD+MoC]) and then calculate MoC collectively rather than category by category. This might involve joint simulations or analytical combination of uncertainties:

1- Integrated Models: Simulate scenarios that incorporate data issues, policy changes, and statistical noise together. Compute the required MoC as the difference between the base estimate and a desired/high percentile of the simulated risk parameter distribution. This would inherently account for any interdependence between MoC A, B, and C factors (avoiding simple over-addition).

2- Variance-Covariance Aggregation: If one can estimate the variance contribution of each category and their correlations, the total uncertainty could be aggregated using statistical rules (like summing variances for independent factors, or more general formulas when not independent). Such approaches yield a smaller composite MoC than raw summation, aligning with a specified confidence level.

3- Calibration of k-Factor: Another approach (as suggested by some industry studies) is to adjust the k multiplier in the k·σ method to implicitly capture some effects of A and B. For instance, a higher k can be chosen in segments known to have Category A/B issues, rather than adding separate chunks.

Conclusion

These advanced methods can be complex to implement and justify. Regulators have so far preferred simplicity to ensure consistency across banks (hence the official recommendation of summation). The onus is on banks to demonstrate that any alternative approach is sound, transparent, and doesn't understate capital.

Toward a more calibrated Margin of Conservatism

The Margin of Conservatism is a crucial but challenging element of IRB credit risk modelling. It ensures a safety net for risk estimation by addressing known data issues (A), evolving business environments (B), and statistical uncertainties (C) that could otherwise lead to underestimation of risk. As we have seen, implementing MoC requires balancing rigor vs. simplicity: applying enough conservatism to satisfy regulatory standards and absorb model risk, but not so much that it overrules true risk differentiation or double counts uncertainties.

The state of practice is still evolving. Banks have adopted a variety of methods, from straightforward confidence interval calculations to the innovative use of influence functions, structural break analyses, and bootstrap simulations, each with its pros and cons. Meanwhile, supervisors, like the ECB, have pointed out inconsistencies between the way banks have implemented the MoC, encouraging them to refine their frameworks.

A key open question remains: what's the best way to aggregate different MoC components without introducing unintended excess conservatism? Forward-looking institutions are exploring ways to jointly model categories A, B, and C into a unified measure that respects their overlaps.

In the end, the MoC discipline forces modelers to explicitly confront model risk within Pillar 1 capital. By continuously improving how we quantify and aggregate these conservatism margins, the banking industry can meet regulatory expectations while preserving the integrity of their models. If you're an IRB modeler or validator, now is a great time to re-examine your MoC approach – ensuring it captures all relevant uncertainties without sinking your model's risk differentiation. Embracing rigorous yet practical techniques for MoC can turn a source of capital inflation into a well-calibrated guardrail for robust, credible credit risk models.

Are you interested in how you could leverage these methodologies to enhance your Credit Risk modeling approach? Contact Kyle Gartner, John de Kroon or Kasper Wijshoff for more information.

References

BCBS. (2004). International Convergence of Capital Measurement and Capital Standards. Bank for International Settlements.

Biche, E. (2022). A Probabilistic Approach to Quantify Margin of Conservatism for Data Deficiencies in a Calibration Sample for Credit Scoring Models.

EBA. (2017). Guidelines on PD estimation, LGD estimation and the treatment of defaulted exposures. European Banking Authority.

Hampel, F. (1974). The influence curve and its role in robust estimation.

Risk Trends 2026 Whitepaper

Read Zanders leadership's strategic outlook on risk's most crucial trends.

Download

Cash is back at the top of the agenda.

In a more volatile, fast-moving environment, treasurers are expected to make faster, better-informed liquidity decisions. Yet many organizations still rely on end-of-day visibility, fragmented systems and manual processes. This gap creates both risk and opportunity. Real-time liquidity is emerging as a practical way to strengthen control, reduce inefficiencies and support better financial decision-making.

Why treasurers are rethinking liquidity

For many years, treasury operated in a relatively stable environment. Payment cycles were predictable, processes were structured, and end-of-day visibility was sufficient to support most liquidity decisions.

Today, that model is under pressure. Funding conditions can tighten quickly, business needs can shift suddenly, and critical payment flows often require faster response times. At the same time, liquidity is no longer confined to traditional business hours. In a 24/7 economy, money can move at any moment, creating both new opportunities and additional complexity. This shift is not only driven by uncertainty. It also reflects a broader transformation in how businesses operate. Speed, immediacy and availability have become the norm, and expectations of treasury have evolved accordingly.

As a result, treasury is taking on a broader role. Beyond managing payments and reporting balances, treasurers are increasingly expected to support funding decisions, capital allocation and overall business resilience. This growing responsibility requires more timely, accurate and actionable information. This evolution is also reflected in recent industry research, highlighting the increasing strategic importance of treasury within the CFO organization with 63% of survey respondents indicating that the priority of Treasury function within CFO Office has increased over the past 5-10 years.

However, many treasury functions still rely on limited visibility, fragmented banking and ERP landscapes, manual processes and static, backward-looking forecasts. To compensate for this, organizations often maintain significant precautionary cash buffers. While these buffers reduce risk and ensure operational continuity, they also trap liquidity and increase inefficiencies. In practice, capital is not always deployed where it creates most value.

Why is liquidity management changing?

The environment is becoming more supportive of a more dynamic approach to liquidity management. Instant payments are a clear example. As they become increasingly standard across the euro area, liquidity can move more quickly and more flexibly, with less reliance on cut-off times.

At the same time, improvements in connectivity are reshaping treasury operations. APIs, host-to-host solutions and integrated banking platforms make it easier to access timely and reliable data. Intraday reporting provides better visibility throughout the day, rather than only at the end of the day. Treasury systems have also evolved, with stronger forecasting and automation capabilities. While none of these developments alone fundamentally transforms treasury, together they create the opportunity to manage liquidity in a more pro-active and flexible way.

What real-time liquidity actually means

Real-time liquidity is not about making every treasury activity instantaneous. Its value lies in increased certainty and control when it matters most. In practice, this means having better visibility on cash positions during the day, knowing whether payments have been made, and being able to act without delay when needed. This allows treasury teams to move from reacting after events to actively steering outcomes.

The value becomes particularly clear in high-impact situations. Payroll, critical supplier payments, debt servicing or M&A-related transactions all require a high degree of confidence that liquidity is available at the right place and at the right moment. In these situations, delays or manual interventions are not just inefficient. They can create real risk.

At the same time, real-time liquidity is not purely a technology question. Data availability, internal processes, governance and system integration all play a key role in determining whether the potential benefits can be realized.

A pragmatic path forward: How can organizations implement real-time liquidity?

For most organizations, real-time liquidity is best approached as a gradual evolution rather than a one-off transformation. A first step is to identify where faster and more accurate liquidity insights would create the most value. This helps prioritize efforts and ensures a clear link with business needs. The next step is to strengthen the foundations. Improving visibility across accounts, ensuring timely access to payment status information and simplifying account structures are essential building blocks.

Equally important is the treasury operating model. Faster infrastructure only delivers value if decision-making processes and governance are aligned. Clear roles, responsibilities and escalation paths make it possible to translate improved visibility into effective action.

Finally, forecasting remains a key complementary capability. A forward-looking view allows treasury to anticipate liquidity needs, reduce reliance on buffers and make better use of available cash.

Rather than aiming for a large-scale transformation from the onset, many organizations benefit from focusing on a limited number of high-impact use cases. This makes it possible to demonstrate value quickly and build momentum over time.

What's next

Real-time liquidity is a maturity journey rather than a destination, guided by business objectives and organizational complexity. It starts with better visibility and builds through greater confidence, stronger processes and improved control.

Value is created when better visibility builds confidence - confidence enables timely action and better decisions. Organizations that move early and pragmatically will not only manage volatility more effectively but also position treasury as a stronger strategic partner to the business.

Cash may be king again, but the real prize lies in what organizations can do with it when they are able to act in time.

This article was developed jointly by ING and Zanders, combining a banking perspective on real-time liquidity infrastructure with practical treasury transformation expertise.

ING Wholesale Banking serves large corporate clients, financial institutions, and governments across the globe, providing tailored solutions in areas such as lending, transaction services, and financial markets. With deep sector and sustainable finance expertise and people on the ground in many markets, ING Wholesale Banking supports its clients in navigating complex financial challenges and achieving their strategic objectives.

Zanders is a global advisory specialized in treasury management, financial risk management and treasury technology. It advises corporates, financial institutions and public sector organizations on treasury strategy, operating models, technology selection and implementation, and risk management.

Curious how real-time liquidity could apply to your organization?

Contact us

CEO and Managing Partner Laurens Tijdhof describes the origins and importance of Zanders’ purpose.

In 1994, Zanders was born in complexity.

From our very first clients, we worked in environments defined by large, capital-intensive balance sheets, fundamental transformation, and a growing need for professional treasury and risk management. These were never simple situations, and they never pretended to be.

That early exposure shaped our DNA.

Our clients operated where the stakes were high, decisions had real consequences, and financial performance truly mattered. They didn't need generic advice or temporary capacity. They needed a trusted advisor, someone who could make sense of complexity and help them act with confidence. That is where Zanders learned to be who we are today.

More than thirty years on, the world has changed, but the nature of the challenge has not.

Volatility is no longer cyclical, it is structural. Geopolitical tension, financial market disruption, regulatory pressure, and rapid technological change now converge. And they show up directly in the decisions CFOs, CROs, and leaders across treasury and risk have to make.

In that environment, the key question is no longer "What is happening?"

It is "What should we do about it, now?"

Our purpose speaks directly to that moment.

We help clients solve complex problems. We add value by delivering financial performance. Not when it is easy, but when it counts. And we help leaders strengthen liquidity, manage risk, and optimize capital to make better decisions today and stay in control tomorrow.

Complexity is also where opportunity lives. Digitalization, tokenization, and artificial intelligence are reshaping treasury and risk functions. When approached strategically, they unlock real advantage - in efficiency, resilience, performance, and decision speed.

At Zanders, we help clients reduce exposure where it matters most and unlock value where it truly exists. Always anchored in real-world challenges. Always focused on outcomes.

Laurens Tijdhof

CEO & Managing Partner, Zanders

Digital transformation is reshaping corporate treasury, but it is also exposing organizations to a faster, more sophisticated fraud and cybercrime threat landscape.

Whilst embarking on a digital transformation journey will bring operational and financial efficiencies, it also expands the attack surface and introduces new vulnerabilities, which allow cyber criminals and bad actors to operate with greater sophistication and speed.

Current projections indicate that global Authorized Push Payment (APP) fraud losses could reach US$331bn by 20271. In the US alone, the FBI's IC3 reported over 859,00 complaints in 2024, with $16.6 billion in losses. Phishing and social engineering dominate as entry vectors, but compromised credentials are becoming more common with approximately 22% of breaches now starting with stolen login data2. Finally, the average cost of ransomware recovery in 2024 reached $2.73 million, with an average of 21 days of downtime for organizations.

These are concerning numbers and in this joint article Mark Sutton (Zanders) and Andrew Compton (Cortida) highlight some of the key risks within both the systems landscape and the underlying operational processes and provide some suggestions around possible risk mitigation.

What are the Key Risks

The current cybercrime and payment-fraud risk landscape is being shaped by four foundational forces linked to:

- The rise of the digital agenda, including instant payments within corporate treasury,

- The darker side of AI which is enabling fraud,

- The increase in professionalized cybercrime,

- and lastly, an increasingly interconnected and complex ecosystem.

As the above foundational forces converge, we see the manifestation in corporate treasury through various risk categories (including but not limited to):

- Business email compromise (BEC) and impersonation fraud.

- AI-enabled social engineering and identity fraud.

- Real-time payment fraud risk.

- Vendor / supplier payment fraud and master-data compromise.

- Malware and ransomware.

- Supply-chain compromise.

Possible Risk Mitigation Options

Practical mitigation options are based on a combination of process, technology and governance measures that must:

- Include a strategy that removes the reliance on email or voice as a trusted payment instruction channel.

- Require design controls that assume identity signals can be spoofed.

- Accelerate fraud detection to before payment release rather than after.

- Elevate controls to protect vendor master data as a critical financial asset.

- Ensure treasury and payments endpoints are recognised as critical payment infrastructure.

- Extend treasury control framework beyond organizational boundaries.

How can Zanders/Cortida Help?

Corporate treasurers now need to move away from a reactive approach to an "always-on" monitoring, control and mitigation operating model. Effective risk mitigation now requires a layered control model that combines process, technology, governance, and behavioural controls. The Zanders/Cortida partnership considers the full end-to-end payment risks landscape through a structured payment and systems security framework.

If you would like to learn more about this new service, please speak to your Zanders relationship contact to arrange a more focused discussion.

Ready to strengthen your treasury’s cyber and payment fraud resilience?

Speak to an expert

Zanders examines why tokenized settlement infrastructure represents the most significant shift in cross-border payments since the introduction of Swift.

This article was first published on: TMI (Treasury Management International).

Cross-border payments remain one of the last great friction points in global finance. Despite decades of incremental improvement, corporate treasurers at the world's largest companies still contend with settlement delays measured in days, opaque fee structures, and an architecture that separates messaging from settlement in ways that create cost, risk and operational complexity.

This is not a new observation. The G20 made enhancing cross-border payments a priority in 20201, and every major industry body has published recommendations since. What is new is that a credible alternative infrastructure now exists; not in theory, but in production. Stablecoin-based settlement rails, underpinned by distributed ledger technology and institutional-grade custody, are moving from proof of concept to live deployment.

This article examines why the current correspondent banking model creates persistent friction, how stablecoin settlement infrastructure addresses each pain point, and what this means for corporate treasury teams preparing for the next generation of payment rails.

The Correspondent Banking Model: Persistent Friction at Scale

The architecture of cross-border payments has remained fundamentally unchanged for decades. When a corporate treasurer in London needs to pay a supplier in Singapore, the payment traverses a chain of correspondent banks, each maintaining bilateral relationships, each potentially applying fees, each adding processing time.

This model creates four categories of friction that corporate treasury teams manage daily:

1. Cost Accumulation

Each bank in the cross-border chain can apply fees, including intermediary and beneficiary banks. For multinationals managing thousands of payments monthly, these costs compound into millions annually.

2. Settlement Latency

Swift GPI2 improved visibility through payment tracking, but tracking a slow payment does not make it faster. Cross-border payments routinely take 24 to 48 hours to reach the beneficiary.

3. Principal Integrity

Intermediary banks frequently deduct fees from the payment itself. The supplier receives less than invoiced, triggering reconciliation queries and damaged supplier relationships.

4. Settlement Risk

CLS3 Bank covers only 18 currencies, leaving large swathes of global trade exposed to overnight and multi-day settlement risk in the correspondent banking model.

These are not edge cases. They are structural features of the correspondent banking model, experienced daily by every corporate treasury function operating internationally.

It is worth emphasizing that this is not a criticism of the banks and institutions that operate within the correspondent banking framework. These institutions have invested heavily in modernization; the Swift MT to MX migration4, GPI tracking, pre-validation services. These investments have delivered genuine improvements. The point is structural: the separation of messaging from settlement, the reliance on chains of bilateral banking relationships, and the batch-processing cadence of traditional payment systems create inherent limitations that no amount of incremental optimization can fully resolve.

Stablecoin Settlement: A New Architecture

Stablecoin-based payment infrastructure does not incrementally improve the correspondent banking model. It replaces the underlying architecture with one designed for the requirements of modern treasury operations.

Atomic Settlement

The transfer of value and its confirmation occur in a single, indivisible operation. Settlement finality is measured in seconds, not days. Settlement risk is eliminated entirely.

Continuous Operations

24 hours a day, 365 days a year. No cut-off times, no batch processing windows, no weekend closures. Genuine real-time liquidity management across every time zone.

Transparent Costs

Visible, predictable fee structures with no hidden intermediary charges. The sender knows the cost upfront; the beneficiary receives the full amount.

Programmability

Smart contracts enable conditional payments, automated sweeps, threshold-triggered distributions and rules-based treasury operations as native capabilities.

Programmability transforms payment operations from a sequence of manual instructions into an automated, rules-based system. The implications for cash management, working capital optimisation and supply chain finance are substantial.

The Institutional Infrastructure Is Ready

A common objection, particularly from risk-conscious treasury functions, has been that stablecoin infrastructure lacks the institutional controls required for corporate use. This objection was valid two years ago. It is no longer accurate.

Regulated instruments. MiCA5 in Europe and emerging frameworks in the US, Singapore and the UAE have created regulatory clarity for stablecoin issuance, reserve management and redemption. Corporate treasurers can now evaluate stablecoins within established regulatory frameworks rather than operating in a legal grey area.

Institutional custody. Qualified custodians now offer segregated custody, insurance coverage and the maker-checker controls that corporate treasury functions require. The custody infrastructure for digital assets has converged with the operational standards of traditional securities custody.

Settlement venues. Institutional-grade settlement venues provide the compliance, onboarding and operational frameworks that connect regulated financial institutions with stablecoin infrastructure. These are not experimental platforms; they are production environments designed for institutional throughput.

Network diversity. Corporate treasurers are not limited to a single blockchain network or a single type of digital money. The toolkit now spans regulated stablecoins, tokenized bank deposits, and tokenized money market funds; providing the diversification across risk, yield and liquidity dimensions that prudent treasury management requires.

What This Means for Corporate Treasury

The practical implications for corporate treasury teams are significant and near-term:

- Working capital release

Reducing settlement times from days to seconds releases trapped liquidity across the payment cycle. For a multinational with billions in transit, even a one-day reduction can release hundreds of millions in working capital.

- Operational simplification

Programmable payments reduce manual intervention for conditional payments, multi-currency sweeps and intercompany settlements. More automated, more auditable, less error-prone.

- Risk reduction

Atomic settlement eliminates counterparty exposure inherent in multi-day settlement windows. Capital currently reserved against settlement risk can be redeployed.

- Cost reduction

Fewer intermediaries, transparent fee structures and automated processing reduce the total cost of cross-border payment operations.

- New capabilities

Automated liquidity rebalancing, conditional supply chain payments, real-time cash concentration across entities and jurisdictions; strategies simply not possible on current rails.

The Transition Has Begun

Global cross-border payment flows are projected to grow from $190 trillion in 2023 to $290 trillion by 20306. The infrastructure that processes these flows will determine the cost, speed and risk profile of international commerce for the next decade.

The correspondent banking model served global trade well for half a century. But the structural separation of messaging from settlement, the reliance on chains of bilateral relationships, and the batch-processing architecture of legacy systems create friction that incremental improvement cannot fully resolve.

Stablecoin settlement infrastructure offers a genuine architectural alternative; one that delivers atomic settlement, continuous operations, cost transparency and programmability. The regulatory frameworks are in place. The institutional infrastructure is ready. The instruments exist.

For corporate treasury teams, the question is no longer whether stablecoin-based settlement will play a role in cross-border payments. It is how quickly to develop the internal capabilities, governance frameworks and banking relationships needed to access these new rails.

The transition has begun. The treasurers and institutions that engage now will shape the standards. Those that wait will adopt them.

What treasurers should do to prepare

Identify the use cases based on high-friction corridors (for example, cross-border payments to emerging markets or intercompany funding) where traditional payment rails struggle. This process will highlight both the business need and potential urgency around experimentation.

The next step is to engage in more detailed conversations with possible partners and vendors to determine any key dependencies, critical actions and potential timelines. This detailed analysis will help treasury take the transformational step from being a passive observer to an active participant in the new, real-time digital financial landscape.

Treasury Trends 2026 Whitepaper

Dive deeper into tokenization, AI, and digitalization's impact on Treasury in the highly anticipated annual Zanders whitepaper.

Download the whitepaperCitations

- https://www.fsb.org/2020/10/enhancing-cross-border-payments-stage-3-roadmap/ ↩︎

- SWIFT gpi (Global Payments Innovation) is the industry standard for cross-border payments, transforming international transfers by offering real-time tracking, enhanced speed, and fee transparency. ↩︎

- Continuous Linked Settlement (CLS) is a specialized financial infrastructure that eliminates settlement risk in foreign exchange (FX) transactions by using a "payment-versus-payment" (PvP) mechanism. Launched in 2002 to mitigate "Herstatt risk" (the risk of one party paying a currency but not receiving the other), CLS enables simultaneous, multi-currency, gross settlement across central bank accounts. ↩︎

- The Swift MT-MX migration project is the industry-wide transition from the legacy Swift MT (Message Type) standard to the modern, XML-based ISO 20022 (MX) standard for financial messaging. ↩︎

- The Markets in Crypto-Assets Regulation (MiCA) is the European Union’s comprehensive legal framework, fully applicable as of December 30, 2024, designed to regulate crypto-assets, issuers, and service providers (CASPs) across all 27 EU member states. ↩︎

- FXC Intelligence, Cross-border payments market sizing data. ↩︎

The IASB has published the exposure draft (ED) on Risk Mitigation Accounting (RMA), previously Dynamic Risk Management (DRM), that will change how banks account for managing interest rate risk across their balance sheet.

Executive Summary

RMA will be an optional model within IFRS 9 for net interest rate repricing risk1 in dynamic, open portfolios (for example, where new deposits or loans are continually added and existing positions mature or reprice). The IASB also proposes withdrawing the IAS 39 macro hedge requirements (and the IFRS 9 option to apply them) and adding related IFRS 7 disclosures.

Compared with current IFRS 9 hedge accounting, RMA shifts from item-level hedges to portfolio net-position accounting, better aligned to typical banking book features (for example, non-maturity deposits and pipeline exposures). Compared with IAS 39 macro hedging (including the EU carve-out), it replaces bucket-based rules and carve-out reliefs with a principles-based net exposure model.

At a high level, the RMA model works as follows:

- Set the target: the entity specifies how much net interest rate risk it aims to mitigate over time, within defined risk limits and not exceeding the net exposure in each time band (bucket). The target can be updated prospectively as the balance sheet evolves.

- Link to derivatives: external interest rate derivatives can be designated. The model uses benchmark derivatives (hypothetical instruments with zero fair value at inception) to represent the risk the entity intends to mitigate.

- Recognize an adjustment: a risk mitigation adjustment is recognized on the balance sheet. It equals the lower of (I) the cumulative value change of the designated derivatives and (II) the cumulative value change of the benchmark derivatives. Any remaining derivative gains or losses (and any ‘excess’ adjustment) go to profit or loss.

- Release to earnings: the risk mitigation adjustment is released to profit or loss as the underlying repricing effects occur.

RMA is a meaningful step toward aligning accounting with how banks manage banking-book interest rate risk in dynamic, open portfolios. At the same time, the ED leaves important practical questions open, notably on benchmark-derivative construction, operation of the excess test, and the level of data, systems, and governance needed for ongoing application.

After the 31 July 2026 deadline, the IASB will review comment letters and fieldwork feedback and decide whether further deliberations are needed, so finalization is likely to take several years. Even once the IASB issues a final standard, application in the EU would still depend on completion of the endorsement process (EFRAG advice, Commission adoption, and Parliament/Council scrutiny).

Introduction

On December 3rd, 2025, the IASB published the ED proposing RMA for interest rate risk in dynamic portfolios. RMA is the result of the IASB’s long-running efforts on accounting for dynamic interest rate risk management, previously referred to as DRM. RMA focuses on repricing risk, which is the interest rate risk that arises when the timing and amount of repricing differ between assets and liabilities.

The aim is to better reflect how banks manage interest rate risk in the banking book at a portfolio level, an area where existing hedge accounting requirements have long been seen as difficult to apply in a way that aligns with real-world balance sheet management.

The IASB presents RMA as a step forward, to better reflect how banks manage interest rate risk in the banking book at a portfolio level, an area in which existing IAS 39 and IFRS 9 hedge accounting requirements have long been viewed as difficult to apply in a way that aligns with real-world, dynamic balance sheet management. In the IASB’s view, RMA is intended to improve that alignment, increase transparency about the effects of repricing-risk management on future cash flows, strengthen consistency between what is managed and what is eligible for accounting treatment, and recognize in the financial statements the extent to which repricing risk has actually been mitigated and the related economic effects.

This article provides a structured overview of the proposed RMA model and its key mechanics. Throughout the article, Zanders provides practical insights on the impact on entities, highlighting the key areas that will shape implementation challenges and accounting results. These insights draw on Zanders' 2025 survey on interest rate risk management and hedge accounting, as well as analysis of stakeholder feedback such as EFRAG's draft comment letter2. The practical implications will depend in part on the outcome of field testing.

Overview of RMA

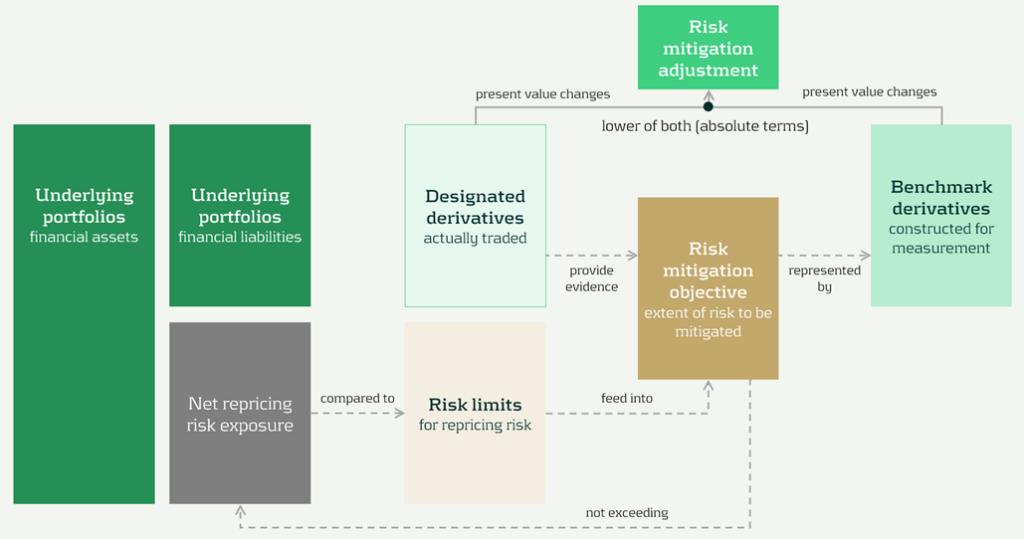

The model components and their relationships are presented in Figure 1 below:

Figure 1: RMA model component overview (source: IASB ED – Snapshot, December 2025)

The RMA model is built around a small set of linked building blocks that start with the bank’s balance-sheet exposures and end with the accounting adjustment that reflects risk management in the financial statements:

- Underlying portfolios: the managed portfolios that expose the entity to repricing risk.

- Net repricing risk exposure: the net position created by the interaction of asset and liability repricing profiles (i.e., the aggregate repricing mismatch the bank is exposed to).

- Risk limits: the bank’s risk appetite and constraints for the managed exposure. In the model, these limits act as an important boundary.

- Risk mitigation objective: the clearly articulated target for how much of the net repricing risk exposure management intends to mitigate (within risk limits). This objective is the central anchor in the model.

- Designated derivatives: the derivatives the bank trades to achieve the risk mitigation objective.

- Benchmark derivatives: hypothetical derivatives constructed to represent the risk mitigation objective for measurement purposes. They translate the objective into a measurable reference profile against which fair value changes can be assessed.

- Risk mitigation adjustment: the accounting output of the model, which is the lower of the change in fair value of the benchmark derivatives and the designated derivatives (in absolute terms).

The section headers contain the relevant paragraph of the ED. The body of the text refers to the ED amendments to IFRS 9 [7.x.), application guidance [B7.x.x), basis for conclusions [BCx), and illustrative examples [IEx), and amendments to IFRS 7 [30x).

Objective and scope [ED 7.1]

IFRS 9 hedge accounting improves alignment for many strategies, but it does not fully capture dynamic, open-portfolio (macro) management of banking book repricing risk—where entities manage interest rate risk of net open positions rather than hedging individual instruments. The RMA model is intended to reflect this more directly and reduce reliance on proxy hedges that can obscure transparency and comparability.

The objective and scope of RMA can be summarized as follows:

- Objective: RMA is, like current hedge accounting under IAS 39 and IFRS 9, an optional model within IFRS 9. The objective is to reflect the economic effect of risk management activities and improve transparency by explaining why and how derivatives are used to mitigate repricing risk and how effectively they do so —bringing reporting closer to actual interest rate risk management practices [7.1.3]. It is the IASB’s intention to withdraw the requirements in IAS 39 for macro hedge accounting and the option in paragraph 6.1.3 of IFRS 9 to apply the requirements in IAS 39 to a portfolio hedge of interest rate risk.

- Scope/eligibility: An entity may apply RMA if, and only if, all of the following are met [7.1.4]:

- Business activities give rise to repricing risk through the recognition and derecognition of financial instruments that expose the entity to repricing risk.The risk management strategy specifies risk limits within which repricing risk, based on a mitigated rate, is to be mitigated, including the time bands and frequency.

- The entity mitigates repricing risk arising from underlying portfolios on a net basis using derivatives, consistent with the entity’s risk management strategy.

- Application discipline: RMA is applied at the level where repricing risk is actually managed and requires robust formal documentation (strategy, mitigated rate, mitigated time horizon, risk limits, and methods for determining exposures and benchmark derivatives) [7.1.6, 7.1.7].

| Key considerations and insights |

| 1. Objective: RMA’s objective to reflect the economic effect of risk management activities may not always coincide with eliminating accounting mismatches (as suggested by other key considerations and insights later in this article). For example, EFRAG’s draft comment letter agrees that faithful representation is a key objective and could improve current accounting, for example, by reducing reliance on proxy hedging. However, it questions whether this should be treated as equally important as eliminating accounting mismatches. This aligns with the concerns expressed around the impact on the hedge effectiveness by several European banks in Zanders’ 2025 survey on interest rate risk management and hedge accounting3, while more than 80% of the participants assessed its effectiveness under the current hedge accounting approach as acceptable. |

Net repricing risk exposure [ED 7.2]

Entities are required to determine a net repricing risk exposure across underlying portfolios by aggregating repricing risk exposure using expected repricing dates, within each repricing time band as required to be defined in formal documentation.

Key requirements include:

- Eligible items Underlying portfolios can include [7.2.1; B7.2.1–B7.2.2]:

- Financial assets measured at amortized cost or FVOCI,

- Financial liabilities at amortized cost, and,

- Eligible future transactions that may result in recognition/derecognition of such items.

- Portfolio view and behavioral profiles: Items that may not show sensitivity on an individual basis (for example, demand deposits) can still contribute to repricing risk on a portfolio basis. A stable ‘core’ portion may be treated as behaving like longer-term funding if supported by reasonable and supportable assumptions and consistent with risk management [B7.2.2].

- Expected repricing dates and time bands: Expected repricing dates must be measured reliably using reasonable and supportable information (including behavioral characteristics such as prepayments and deposit stability). Time bands and risk measures (e.g., maturity gap or PV01) must be consistent with actual risk management [7.2.5–7.2.9; B7.2.10–B7.2.16].

- Equity modeling as a proxy: Own equity is not eligible for inclusion in underlying portfolios, but the model acknowledges that some entities assess repricing risk from cash/highly liquid variable-rate assets only to the extent they are ‘funded by equity’. If internal equity modeling (e.g., replicating portfolios) is used for risk management, it can serve as a proxy to determine how much of those exposures are included in net repricing risk exposure [B7.2.17; IE184-IE191].

| Key considerations and insights |

| 2. Eligibility: RMA aims to reflect net repricing risk management, but eligibility rules can make the net repricing risk exposure only a partial proxy for the position Treasury actually manages. For example, banks might include fair value through profit or loss (FVTPL) items for interest rate risk management but these are not allowed as underlying items in the net repricing risk exposure (also noted by EFRAG). |

| 3. Risk management by time bands (1/2): RMA requires a risk mitigation objective based on the net repricing risk exposure determined for each repricing time band, but it is unclear how entities that do not manage their interest rate risk across time bands would then apply the RMA model, as noted by EFRAG. |

| 4. Risk management by time bands (1/2): RMA requires the same risk measure (e.g., maturity gap or PV01) for all exposures within each repricing time band [B7.2.13], but banks’ risk management practice might deviate from this. |

| 5. Equity treatment: RMA introduces an equity proxy approach that allows partial inclusion of variable-rate assets based on modelled equity, viewing equity as residual and ineligible for direct inclusion. This is an addition compared to the DRM staff papers. Banks' risk management practices might treat equity differently (e.g., by modeling it). |

Designated derivatives [ED 7.3]

Under RMA, banks can designate external derivatives (e.g., interest rate swaps, forwards, futures, options) used to manage net repricing risk as hedging instruments. Eligible derivatives are generally consistent with IFRS 9. All designated derivatives collectively mitigate the net portfolio risk and remain recognized at fair value.

Eligibility depends on the following items:

- Mitigation: Derivatives can only be designated to the extent that they mitigate the net repricing risk exposure [7.3.6].

- External counterparty: Derivatives must be with a counterparty external to the reporting entity. Intragroup derivatives may qualify only in the separate or individual financial statements of the relevant entities, and are not eligible in the consolidated financial statements of the group [7.3.4].

- Designate once: Derivatives already in a hedging relationship for interest rate risk in accordance with Chapter 6 of IFRS 9 are not eligible [7.3.5].

- Options: Written options are generally excluded, unless part of a net written option position that offsets a purchased option, resulting in a net purchased position overall [7.3.2(a), 7.3.3].

Banks can designate derivatives in full or in part (e.g., designating 80% of a swap if only that portion manages interest rate risk), but the selected portion must align with the documented risk mitigation objective.

Once derivatives are designated, they can only be removed from RMA if they are no longer held to mitigate the net repricing risk exposure under the entity’s risk management strategy.

| Key considerations and insights |

| As the EFRAG comment letter notes: 6. Options and off-market derivatives: Further guidance is needed on how to treat options (for example, time value) and off-market derivatives (non-zero initial fair value) within the designation mechanics. |

| 7. De-designation: The ED does not allow voluntary de-designation, but banks often manage changes by entering into offsetting trades rather than settling existing positions. |

Risk mitigation objective [ED 7.4]

The risk mitigation objective is the bridge between risk mitigation intent and what’s actually executed: it sets how much net repricing risk exposure the entity aims to mitigate within risk limits [7.4.2]. The benchmark derivatives and consequently the risk mitigation adjustment are built from this risk mitigation objective (see next sections), enabling partial hedging while avoiding objectives that aren’t supported by actual designated hedges. [ED 7.4.1, B7.4.2–B7.4.3].

Key requirements:

- Evidence-based: The objective must be consistent with the repricing risk mitigated by designated derivatives—it’s a matter of fact, not a free choice. [ED 7.4.1, B7.4.2–B7.4.3]

- Absolute, not proportional: It’s stated as an absolute amount of risk (e.g., PV01), not ‘X% of each instrument’ [B7.4.2].

- Capped by exposure: It cannot exceed net repricing risk exposure (overhedge) in any time band [7.4.1, B7.4.2–B7.4.3].

- Measurement basis: The risk mitigation objective should be set using the same risk measure (e.g., DV01) used to quantify exposure [ED B7.4.1].

| Key considerations and insights |

| 8. Repricing time bands are a key design choice: the risk mitigation objective is specified and capped by the net repricing risk exposure in each time band. Executing (and designating) hedges in neighboring tenors (a common practice) can create residual P&L volatility, because only the portion aligned to that time band’s net repricing risk exposure is reflected in the risk mitigation adjustment. |

| 9. Degree of freedom risk limits: While RMA imposes strict alignment requirements between net repricing risk exposure, risk mitigation objective, and designated derivatives on measures and time bands, entities retain strategic flexibility on risk limits. Risk limits do not need to be specified per time band [B7.4.6], allowing entities to set overarching frameworks rather than granular constraints. |

Benchmark derivatives [ED 7.4]

Benchmark derivatives are introduced to measure hedge performance: modelled (hypothetical) derivatives that are not executed and not recognized on the balance sheet, but are constructed to replicate the timing and amount of repricing risk captured in the risk mitigation objective, as presented in Figure 1 above and Figure 2 below.

In practice, the benchmark derivative is designed to mirror the bank’s target risk position (e.g., a swap profile that matches the repricing ‘gap’ being mitigated), so its fair value movement represents how the net repricing risk exposure would change when interest rates move. If an entity intends to mitigate 70 of the 100 units of repricing risk in the 9-year time band by a 10-year swap, the benchmark derivative is based on 70 units and 9 year maturity [B7.4.8].

Benchmark derivatives should have an initial fair value of zero based on the mitigated rate [7.4.5]. These benchmark derivatives are therefore similar to the hypothetical derivative used in cash flow hedging [B6.5.5–B6.5.6 of IFRS 9].

| Key considerations and insights |

| 10. Operational burden (1/3) – benchmark derivatives: RMA intentionally separates designated derivatives from benchmark derivatives (constructed to start at zero fair value at the mitigated rate), so they won’t always share the same terms. This can become operationally heavy, as also noted by EFRAG. |

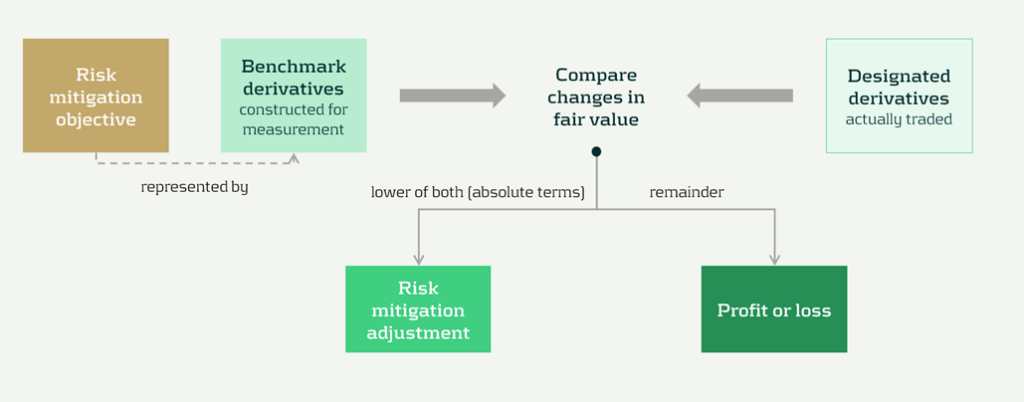

Risk mitigation adjustment [ED 7.4]

The risk mitigation adjustment is the accounting output of the model and is presented as a single line item on the balance sheet (asset or liability). At each reporting date (so not necessarily the hedging date), the entity compares the cumulative fair value change of all designated derivatives with the cumulative fair value change of all the benchmark derivatives, and recognizes the lower of those two amounts (in absolute terms) [7.4.8] as the risk mitigation adjustment. That balance sheet adjustment is the mechanism that offsets the designated derivatives’ fair value changes in profit or loss; any remaining gain or loss (i.e., the portion not captured by the lower-of) is recognized directly in profit or loss as residual volatility/ineffectiveness [7.4.9]. This is visualized in Figure 2 below.

Figure 2 Recognition and measurement of risk mitigation adjustment (source: IASB ED – Snapshot, December 2025)

The 'lower of' mechanism ensures the risk mitigation adjustment never exceeds what's actually supported by either (I) the designated derivatives or (ii) the net exposure being hedged. This prevents over-recognition of hedging effects.

The risk mitigation adjustment is then recognized in profit or loss over time on a systematic basis that follows the repricing profile of the underlying portfolios [7.4.10], so the hedging effect shows up in the same periods in which the hedged repricing differences affect earnings.

| Key considerations and insights |

| 11. Operational burden (2/3) – risk mitigation adjustment: Heavy tracking requirements (including effects of settling vs offsetting trades), unclear calculation granularity, and complexity over time as the risk mitigation adjustment can flip between debit and credit, as noted by EFRAG. |

| 12. RMA as a balance sheet item: The RMA model creates a separate balance sheet asset/liability (unlike current hedge accounting that adjusts hedged items or uses equity), introducing uncertainty around whether this item will attract RWA or require capital deductions until regulators provide guidance. |

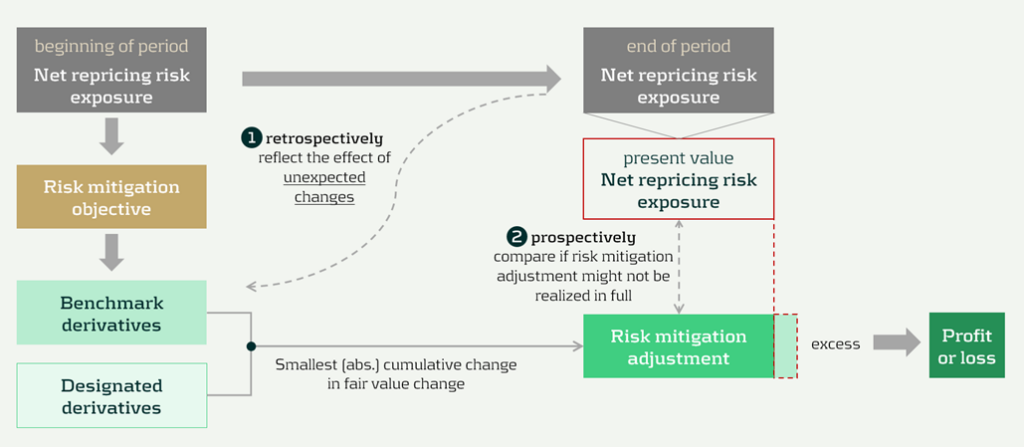

Prospective (RMA excess) and retrospective (unexpected changes) testing [ED 7.4]

RMA is designed to keep the accounting mechanics anchored to the net repricing risk exposure that actually remains in the underlying portfolios over time. Two tests can lead to changes to the risk mitigation adjustment. These tests are visualized in Figure 3 below, indicated by ① and ②.

Figure 3 Risk mitigation adjustment and prospective and retrospective testing (source: IASB ED – Snapshot, December 2025)

The two tests are:

- Benchmark adjustments for unexpected changes (retrospectively): First, benchmark derivatives must be adjusted when unexpected changes in the underlying portfolios reduce the net repricing risk exposure below the risk mitigation objective in a repricing time band (i.e., correction of overhedge), as they would otherwise no longer represent the repricing risk specified in the risk mitigation objective [7.4.6, B7.4.10].

- Excess test to prevent unrealizable adjustments (prospectively): Second, an explicit excess assessment to prevent the risk mitigation adjustment from accumulating beyond what can be supported by the remaining net repricing risk exposure. If there is an indication that the accumulated risk mitigation adjustment may not be realized in full, the entity compares the risk mitigation adjustment to the present value of the net repricing risk exposure at the reporting date (discounted at the mitigated rate) [7.4.11–7.4.13]. This would happen if unexpected changes have not been fully reflected in the adjustments to the benchmark derivatives.

Any excess is recognized immediately in profit or loss by reducing the risk mitigation adjustment, and it cannot be reversed [7.4.14; BC101–BC103]. It acts like a safeguard: if revised behavioral assumptions shrink future repricing exposure, the unearned portion of the adjustment is released to P&L straight away.

| Key considerations and insights |

| 13. Operational burden (3/3) – benchmark derivatives: The reliance on ‘unexpected changes’ and time-band caps may force highly granular, frequently re-constructed benchmark derivatives, creating a mismatch versus designated derivatives. This could be operationally heavy, as noted by EFRAG. |

| 14. Unclear testing and adjustment mechanics: The ‘excess’ framework is under-specified. Triggers and documentation expectations are unclear, and the present value test for net exposure is conceptually and operationally challenging, especially for modelled items (e.g., NMDs), as noted by EFRAG. |

Discontinuation [ED 7.5]

Discontinuation is intentionally rare. RMA is not switched off because hedging activity changes. It only stops when the risk management strategy changes, and it stops prospectively from the date of change.

Key requirements include:

- Strategy: strategy triggers a change; activity does not. A change in how repricing risk is managed, such as changing the mitigated rate, changing the level at which repricing risk is managed (group vs entity), or changing the mitigated time horizon [7.5.1, 7.5.2].

- Prospective application: discontinue from the date the strategy change is made. No restatement of prior periods [7.5.1].

After discontinuation, the existing balance is recognized in profit or loss, either:

- Over time, on a systematic basis aligned to the repricing profile, if repricing differences are still expected to affect profit or loss [7.5.3(a)], or,

- Immediately if those repricing differences are no longer expected to affect profit or loss [7.5.3(b)].

Disclosures [IFRS 7]

The disclosures are meant to show, in a compact way, what risk is being mitigated, what derivatives are used, and what the model produced in the financial statements.

Key disclosures include:

- RMA balance sheet and P&L: risk mitigation adjustment closing balance and current-period P&L impact [30E].

- Risk strategy and exposure: repricing risk managed, portfolios in scope, mitigated rate and horizon, risk measure, and exposure profile [30H–30L].

- Designated derivatives: timing profile and key terms, notional amounts, carrying amounts, and line items, and FV change used in measuring the adjustment [30I, 30M].

- Sensitivity: effect of reasonably possible changes in the mitigated rate [30J].

Volatility and roll-forward: FV changes not captured and where presented, plus reconciliation including excess amounts and discontinued balances [30N–30P].

| Key considerations and insights |

| 15- More, and more sensitive, disclosures: RMA adds extensive requirements (profiles, sensitivities, roll-forwards) that may reveal non-public positioning, so aggregation and materiality judgment matter. |

Conclusions

The RMA proposal appears to be a constructive development toward reflecting the management of interest rate risk in dynamic portfolios more faithfully in financial reporting. Compared with existing approaches, it offers a clearer conceptual link between net repricing-risk management and accounting outcomes.

At the same time, several core mechanics might prove challenging in practice. In particular, further clarification would be helpful on the benchmark-derivative mechanism, the operation and trigger logic of the excess test, and the level of granularity and governance expected for the ongoing application. These areas will likely be central to implementation efforts, earnings volatility outcomes, and cross-bank comparability.

At this stage, practical outcomes may therefore differ significantly depending on interpretation and system design choices. Additional IASB guidance, informed by field testing and stakeholder feedback, could reduce that uncertainty and support more consistent application. Overall, RMA can be seen as a promising direction that improves conceptual alignment with risk management, while still requiring further clarification before its operational and reporting implications are fully settled.

Citations

- Repricing risk is the risk that assets and liabilities will reprice at different times or in different amounts. For purposes of risk mitigation accounting, repricing risk is a type of interest rate risk that arises from differences in the timing and amount of financial instruments that reprice to benchmark interest rates ↩︎

- https://www.efrag.org/sites/default/files/media/document/2026-02/RMA%20-%20Draft%20Comment%20Letter%20-%20FINAL.pdf ↩︎

- The reports are confidential, and each participating bank received the same report presenting the benchmark results on an anonymized basis. If you would like to discuss the main results or conduct a benchmark, please reach out. ↩︎

Dive deeper into Risk Mitigation Accounting

Speak to an expert

How financial institutions can move from siloed valuation models to a cohesive framework that enhances transparency and operational efficiency.

The Proliferation of Valuation Models

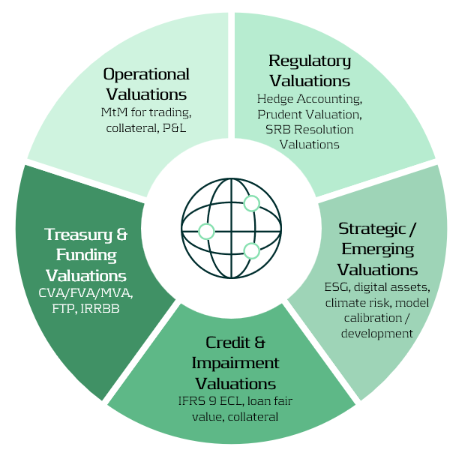

Valuation lies at the heart of financial institutions — informing decisions in trading, risk management, collateral management, accounting, and financial reporting. Yet across many banks, these valuations are performed in fragmented silos for different purposes, using different models, data sources, and systems. In addition to these core applications, valuations also support a broader range of activities, including treasury, regulatory reporting, and emerging domains such as ESG and digital assets.

As illustrated in the Valuation Map (Figure 1), we observe that in many cases different departments conduct their own valuations, often for their own distinct purposes and using distinct valuation processes. Survey evidence shows that finance and FP&A teams devote roughly 65% of their time to data gathering, cleaning, and reconciliation, leaving only about 35% for value-adding analysis1.

The Cost of Fragmentation

Fragmented valuation architectures translate directly into higher costs and operational drag. In practice, three effects are most pronounced:

- High data vendor spend – market-data pricing surveys found that some firms were paying “many multiples” more than peers for similar products and use cases, reflecting redundant sourcing and poor usage visibility2.

- Model proliferation – large banks often operate with hundreds to thousands of models across the enterprise, creating overlap in purpose and increasing governance, maintenance, and compute costs3.

- Inconsistent and time-consuming valuations – disparate models and data feeds lead to unclear ownership of valuation “truth” and significant manual reconciliation between accounting, risk, and front-office views.

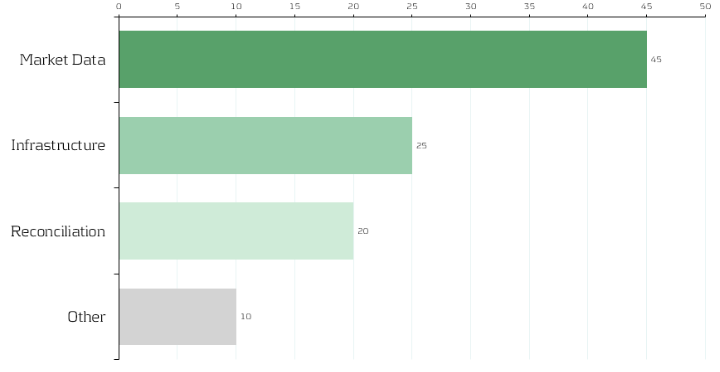

Although no public benchmark precisely mirrors our allocation, multiple industry surveys converge on the same conclusion: market data represents a dominant share of valuation costs, and fragmented reconciliation processes account for a significant portion of non-value-adding effort. Figure 2 therefore shows an indicative distribution — 45% market data, 25% infrastructure, 20% reconciliation, 10% other — to convey the relative scale of each component. Institutions will vary in mix, yet the implication is consistent: rationalizing data sourcing and automating reconciliation are among the highest-impact levers for reducing total valuation cost.

Strategic Imperative: Centralizing and Standardizing Valuation

Banks can unlock substantial efficiency gains by centralizing valuation logic and governing data flows. Similar to how treasury departments manage liquidity, banks should treat valuation processes as coordinated enterprise capabilities rather than fragmented operational activities.

Key levers include:

1-Valuation as a Service (VaaS):

Establish a centralized valuation engine providing consistent pricing APIs for all functions (risk, finance, collateral, etc.).

2-Unified Market Data Platform:

Integrate vendor feeds into a single validated golden source with standardized identifiers and governance.

3-Model Consolidation and Validation:

Maintain one approved model per product type with clear ownership and lifecycle management.

4- Process Automation:

Automate reconciliation between accounting and risk views via shared data lineage and valuation transparency.

5- Cost Transparency:

Track valuation and data usage per business unit to encourage accountability and optimization.

Together, these measures reduce duplication, accelerate reporting cycles, and improve consistency across valuation outcomes.

Building the Foundation

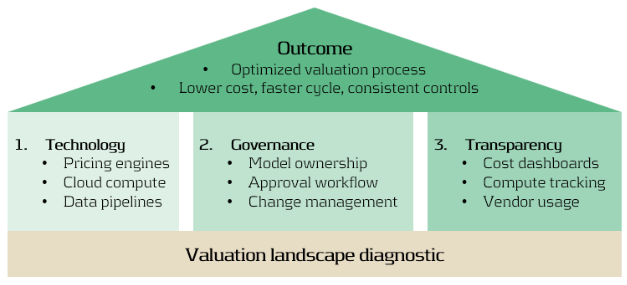

An optimized valuation operating model rests on three mutually reinforcing foundations:

- Technology: Scalable pricing engines, cloud compute elasticity, and efficient data pipelines.

- Governance: Clear model ownership, approval, and change management across risk and finance.

- Transparency: Dashboards tracking valuation cost, compute time, and data provider usage.

A practical first step: Zanders can perform a valuation landscape diagnostic, mapping all valuation types, systems, and data sources. Such analysis typically reveals 10–20% potential overlap and quick wins in data consolidation4.

Conclusion: Elevating Valuation Processes to an Enterprise Capability

In today’s environment of cost pressure and regulatory scrutiny, optimizing valuation processes is not only about efficiency—it is about strengthening consistency, transparency, and trust across the organization. Institutions that unify valuation workflows, data, and governance are better positioned to:

- Reduce operational costs and reconciliation workloads.

- Rationalize compute power – costs of running multiple models unnecessarily.

- Strengthen governance and auditability.

- Accelerate model deployment and reporting cycles.

- Enable transparent, sustainable, and data-driven decision-making.

At Zanders, we design and implement integrated valuation frameworks at leading financial institutions, that combine operational efficiency with regulatory robustness.

If your organization is looking to streamline valuation processes, harmonize market data, or reduce reconciliation workloads, we invite you to connect with our experts.

Citations

- FP&A Trends (2024), FP&A Trends Survey 2024 (FP&A Trends Survey 2024: Empowering Decisions with Data: How FP&A Supports Organisations in Uncertainty | FP&A Trends) ↩︎

- Substantive Research (2024), Market Data Pricing (Market Data Pricing - 2023 In Review - Edited Highlights) ↩︎

- UK Finance (2023), Prudential Regulation Authority (PRM), SS1/23 (Prudential Regulation Authority (PRA), SS1/23 - what you don’t know can hurt you | Insights | UK Finance) ↩︎

- TRG Screen (2023), Market data spend hits another record as complexity grows (WP | Market data spend hits another record as complexity grows) ↩︎

Dive deeper into the strategy of compute

The Strategic Role of Compute in Modern Banking

As tax authorities intensify their scrutiny of intercompany financing transactions, multinational enterprises must anticipate emerging trends and strengthen their transfer pricing positions.

Recent case law and regulatory developments provide useful guidance on what to expect in 2026 and on the approach that should be followed to mitigate the risk of challenges on intra-group loans.

Historically, tax authorities focused primarily on interest rate benchmarks when reviewing intra-group loans, cash pools and guarantees. Today, however, their analysis has become significantly broader and more sophisticated, extending to a range of interrelated factors such as contractual terms, debt capacity, and creditworthiness.

The sections below outline the key trends and risks shaping intra-group loan transfer pricing and highlight what multinational groups should address as part of their planning and compliance efforts for 2026.

Arm’s Length Terms & Conditions for Intra-Group Loans

Verifying that the terms and conditions of intra-group loans are consistent with how independent parties would contract remains a critical focus. In addition to establishing an arm’s length interest rate and the appropriate amount of debt (further explained below), it is also necessary to assess whether the other terms and conditions are at arm’s length. This involves considering the main features of the loan, and evaluating their impact on the risk profile of both the borrower and the lender, as well as on the arm’s length interest rate. Relevant terms that should be considered include currency, maturity, repayment schedule, and callability.

In 2025, courts emphasized that Transfer Pricing documentation must not only include a benchmark analysis but also a clear explanation of the contractual features agreed, especially for features such as subordination, maturity, interest structures, and repayment conditions. These features should align with the actual conduct of the parties and with the economic reality.

Multinationals have also seen a rise in challenges derived from discrepancies between the legal agreements drafted, the price applied between the entities involved, and the information presented in the Transfer Pricing report. A clear example is one-year loans that are automatically renewed, with the same price being applied and with no repayments being made, where tax authorities may reclassify them as longer-term arrangements, which typically carry a higher interest rate.

What to consider in 2026: It is important for multinational enterprises to carefully assess these terms and conditions before issuing a loan, as they will have a direct impact on the interest rate applied to the transaction. Drafting a comprehensive loan agreement that clearly outlines these terms, aligns with the conditions applied in practice, and is supported by a robust Transfer Pricing analysis is recommended to mitigate the risk of challenges by tax authorities.

Debt Capacity Analyses for Intra-Group Loans

Tax authorities are increasingly scrutinizing whether the amount of intra-group debt is economically justified and supported by a clear business purpose. They are also evaluating whether the debt aligns with arm’s length principles and serves a legitimate economic function consistent with the borrower’s overall business strategy.

A debt capacity analysis is often conducted to determine whether the borrower has the financial capacity to repay the loan and whether an unrelated party would provide a similar amount of financing under comparable conditions. If tax authorities consider that the amount of debt is excessive, adverse tax consequences could arise, such as the requalification of the debt as equity and/or the denial of a portion of the interest expense deduction.

Over the last two years, jurisdictions such as Germany and Australia introduced administrative guidelines formalizing debt capacity considerations. This trend has been further reinforced by case law in different countries over the past year. For example, in Luxembourg, a major hub for treasury companies and investment funds, the Luxembourg Administrative Court in 2025 issued a pivotal decision in case No. 50602C rejecting an automatic 85:15 debt-to-equity standard and holding that arm’s length analyses must be fact-specific and supported by data rather than mechanical ratios.

What to consider in 2026: Multinationals are expected to prepare robust debt capacity analyses for each borrower entity, demonstrating that independent lenders would extend a similar amount of debt. The debt quantum should be supported by financial projections, coverage ratios, and a documented business purpose, all included in the corresponding Transfer Pricing report.

Debt Capacity Analysis

A guide to demonstrating the arm’s length principle in debt financing

Credit Rating Analyses for Financial Transactions: Stand-Alone vs Group Rating

Both tax administrations, and subsequently, courts, are scrutinizing the credit rating approaches applied by taxpayers in the context of intra-group loans. Credit rating analyses are a core step when pricing intra-group loans, as the risk profile of the borrower has a material impact on the applicable interest rate.

While simplified blanket ratings across a group were once tolerated, tax authorities and courts are now emphasizing the importance of entity-specific ratings adjusted for implicit support.

In Belgium, on June 6, 2025, the Court of First Instance of Leuven clarified that credit ratings must be substantiated and not merely assumed based on group affiliation. Based on this ruling, the borrower should be assessed on a stand-alone basis, taking into account the impact of the new debt quantum on its financial position. Where implicit group support is considered, it must be properly substantiated through a thorough implicit support analysis and cannot be assumed by default our automatically applied.

In the Netherlands, the Court of Appeal of Amsterdam, in its judgment of 11 September 2025, addressed, among other topics, the guarantee fees applied by the taxpayer and rejected their payment, emphasizing the importance of factoring implicit support into the credit rating applied to the borrower. This once again highlights the relevance of a two-step process: first, the calculation of the stand-alone rating, and second, the adjustment of this rating for implicit support.