Is the grass always greener on the other side? Observing a tendency to change from “best of breed treasury management systems” to best “integrated treasury management systems” and vice versa.

In large organizations, the tendency is to select large scale ERP systems to support as much of the organization's business processes within this system. This is a goal that is driven typically by the IT department as this approach reduces the number of different technologies and minimizes the integration between systems. Such a streamlined and simplified system architecture looks to mitigate risk by reducing the potential points of failure and total cost of ownership.

Over the years the treasury department has at times chosen to rather deploy “best of breed” treasury management systems and integrate this separate system to the ERP system. The treasury business processes and therefore systems also come with some significant integration points in terms of trading platforms, market data and bank integration for tasks such as trade confirmations, payments, bank statements and payment monitoring messaging.

The IT department may view this integration complexity as an opportunity for simplification if the ERP systems are able to provide acceptable treasury and risk management functionalities. Especially if some of the integrations that the treasury requires does overlap with the needs of the rest of the business – i.e. payments, bank statements and market data.

Meanwhile, the treasury department will want to ensure that they have as much straight through processing and automation as possible with robust integration. Since their high value transactions are time sensitive, a breakdown in processing would result in negative transactional cost implications with their bank counterparts.

Deciphering Treasury System Selection: Below the Surface

The decision-making process for selecting a system for treasury operations is complex and involves various factors. Some are very much driven by unique financial business risks, leading to a functional based decision process. However, there are often underlying organizational challenges that play a far more significant role in this process than you would expect. Some challenges stem from behavioral dimensions like the desire for autonomy and control from the treasury. While others are based on an age-old perception that the “grass is greener on the other side” – meaning the current system frustrations result in a preference to move away from current systems.

An added and lesser appreciated perspective is that most organizations tend to mainly focus on technical upgrades but not often functional upgrades on systems that are implemented. Meaning that existing systems tend to resemble the version of the system based on when the original implementation took place. This will also lead to a comparison of the current (older version) system against the competing offerings latest and greatest.

Another key observation is that with implementing integrated TMS solutions like the SAP TRM solution in the context of the same ERP environment, the requirements can become more extensive as the possibilities for automating more with all source information increase. Consider for example the FX hedging processes where the source exposure information is readily available and potential to access and rebalance hedge positions becomes more dynamic.

Closing thoughts

There is no single right answer to this question for all cases. However, it is important to ensure that the process you follow in making this decision is sound, informed and fair. Involving an external specialist with experience in navigating such decisions and exposure to various offerings is invaluable.

To support these activities, Zanders has also built solutions to make the process as easy as it can possibly be, including a cloud-based system selection tool.

Moreover for longer term satisfaction, enabling the evolution of the current treasury system (be it best of breed or integrated) is essential. The system should evolve with time and not remain locked into its origin based on the original implementation. Here engaging with a specialist partner with the right expertise to support the treasury and IT organizations is key. This can improve the experience of the system and this increased satisfaction can ensure decision making is not driven or led by negativity.

In support of this area Zanders has a dedicated service called TTS which can come alongside your existing IT support organization and inject the necessary skill and insight to enable incremental improvements alongside improved resolution timeframes for day-to-day systems issues.

For more information about out Treasury Technology Service, reach out to Warren Epstein.

First in a series of articles by Zanders introducing the Dynamic Risk Management model proposed by the IASB to revolutionize hedge accounting for dynamic portfolios

The current standards for hedge accounting present significant challenges for financial institutions engaged in dynamically hedging their portfolios. The corresponding type of hedging accounting, known as “macro fair value hedge accounting”, is covered under IAS 39; however, the regulations fall short as they are unable to accurately reflect an organization’s risk management strategies in its financial reporting. In some instances, companies cannot apply hedge accounting as their hedge is deemed to be ineligible unless they perform some form of proxy hedging strategies. To address these issues, the international Accounting Standards Board (“IASB”) have introduced the Dynamic Risk Management (“DRM”) approach, which is intended to offer a more effective method for entities to apply macro hedging.

The current timeline by the IASB is for a first draft to be released in 2025. This article forms the first in a series of three that will delve into the DRM model, explore its improvements over the current regulations and provide a demonstration of a practical implementation of the current proposal. The insights provided within this series, are Zanders’ understanding drawn from the discussion papers that the IASB has released and so the information is subject to change before the publication of the draft in 2025.

The IASB is aiming for the DRM model to allow readers of the financial statement to gain the following insights:

- The entity’s interest rate risk management strategy and how it is applied to manage interest rate risk.

- How the entity’s interest rate risk management activities may affect the amount, timing and uncertainty of future cash flows.

- The effect of the DRM model on the entity’s financial position and financial performance.

Within the May 2022 Staff Paper1, the IASB staff have identified a list of deficiencies of the current IAS 39 and IFRS 9 standards. The main limitations identified were:

| Number | Area | Description of limitation |

| 1 | Closed Portfolios | The current regulations are designed for “closed portfolios” and requires the direct linkage of hedged items with a hedge. This causes problems as currently an “open portfolio” would be viewed as a set of multiple “closed portfolios”, each with short periodic lifespans. This leads to challenges, as any “open portfolio” hedge relationships need to be tracked individually and its hedge adjustments amortized accordingly. |

| 2 | Risk Management on a net basis | Generally, entities will manage their exposures to interest rate risk on a net basis. However, currently hedges need to be managed on a gross basis. This means that interest rate risk management can be incorrectly represented to achieve the accounting requirements. |

| 3 | Dual character of net interest rate risk position | The repricing risk of the net interest rate risk position arises from a combination of variable and fixed-rate exposures. The economic mismatch has both fair value and cash flow variability when interest rates change, and entities try to mitigate both aspects economically. However, the current hedge accounting requirements state that the hedging relationship must be designated as either a fair value hedge with the fixed rate item or as a cash flow hedge with the variable item. |

| 4 | Demand deposits | Under the current regulations demand deposits cannot be hedged by banks as, from an accounting perspective, the fair value is constant. Since banks are unable to apply hedge accounting to demand deposits, they cannot accurately portray their risk management within the financial statements. |

The next two articles in this series will provide a comprehensive exploration of the DRM model and introduce the new concepts that the IASB has proposed. The next article offers a breakdown of the Risk Management Strategy (“RMS”) within the DRM model, how it factors into a company’s overarching strategy for managing their interest rate risk. It will cover the new concepts that the IASB have established. The third and final article in this series will provide an overview of the DRM cycle as well as an example taken from the IASB of how the DRM model would be applied in practice for a singular accounting period. Stay tuned!

What can Zanders offer?

Transitioning to the new DRM model can be difficult due to the dynamic nature of the model, especially with a more complex balance sheet. Zanders can provide a wide range of expertise to support in the onboarding of the DRM model into your company’s hedging and accounting. We have supported various clients with hedge accounting– including impact analyses, derivative pricing and model validation, and are familiar with the underlying challenges. Zanders can manage the whole project lifecycle from strategizing the implementation, alignment with key stakeholders and then helping design and implement the required models to successfully carry out the hedge accounting at every valuation period.

For further information, please contact Pierre Wernert, or Alexander Oldroyd.

Read our other blogs and learn more on The DRM Cycle: The Model in Action, and Rethinking Macro Hedging: What are the Key Components of the DRM Model?

Economic instability, a pandemic, geopolitical turbulence, rising urgency to get to net zero – a continuousstream of demands and disruption have pushed businesses to their limits in recent years.

Economic instability, a pandemic, geopolitical turbulence, rising urgency to get to net zero – a continuousstream of demands and disruption have pushed businesses to their limits in recent years. What this has proven without doubt is that treasury can no longer continue to be an invisible part of the finance function. After all, accurate cash flow forecasting, working capital and liquidity management are all critical C-suite issues. So, with the case for a more strategic treasury accepted, CFOs are now looking to their corporate treasurer more than ever for help with building financial resilience and steering the business towards success.

The future form of corporate treasury is evolving at pace to meet the demands, so to bring you up to speed, we discuss in this article five key observations we believe will have the most significant impact on the treasury function in the coming year(s).

1. A sharper focus on productivity and performance

Except for some headcount reductions, treasury has remained fairly protected from the harsh cost-cutting measures of recent years. However, with many OPEX and CAPEX budgets for corporate functions under pressure, corporate treasurers need to be prepared to justify or quantify the added value of their function and demonstrate how treasury technology is contributing to operational efficiencies and cost savings. This requires a sharper focus on improving productivity and enhancing performance.

To deliver maximum performance in 2024, treasury must focus on optimizing structures, processes, and implementation methods. Further digitalization (guided by the blueprint provided by Treasury 4.0) will naturally have an influential role in process optimization and workflow efficiency. But to maintain treasury budgets and escape an endless spiral of cost-cutting programs will take a more holistic approach to improving productivity. This needs to incorporate developments in three factors of production – personnel, capital, and data (in this context, knowledge).

In addition, a stronger emphasis on the contribution of treasury to financial performance is also required. Creating this direct link between treasury output and company financial performance strengthens the function’s position in budget discussions and reinforces its role both in finance transformation processes and throughout the financial supply chain.

2. Treasury resilience, geopolitical risk and glocalization

Elevated levels of geopolitical risk are triggering heightened caution around operational and financial resilience within multinationals. As a result, many corporations are rethinking their geographical footprint and seeking ways to tackle overdependence on certain geographical markets and core suppliers. This has led to the rise of ‘glocalization’ strategies, which typically involve moving away from the traditional approach of offshoring operations to low-cost destinations to a more regional approach that’s closer to the end market.

The rise of glocalization is forcing treasury to recalibrate its target operating model to adopt a more regionalized approach. This typically involves changing from a ‘hub and spoke’ model to multiple hubs. But the impact on treasury is not only structural. Operating in many emerging and frontier markets creates heightened risks around currency restrictions, lack of local funding and the inability to repatriate cash. Geopolitical tensions can also have spillover effects to the financial markets in these countries. This necessitates the application of more financial resilience thinking from treasury.

3. Cash is king, data is queen

Cash flow forecasting remains a top priority for corporate treasurers. This is driving the rise of technology capable of producing more accurate cash flow predictions, faster and more efficiently. Predictive and prescriptive analytics and AI-based forecasting provide more precise and detailed outcomes compared to human forecasting. While interfaces or APIs can be applied to accelerate information gathering, facilitating faster and automated decision-making. But to leverage the benefits of these advanced applications of technology requires robust data foundations. In other words, while technology plays a role in improving the cash flow forecasting process, it relies on an accurate and timely source of real-time data. As such, one can say that cash may still be king, but data is queen.

In addition, a 2023 Zanders survey underscored the critical importance of high-quality data in financial risk management. In particular, the survey highlighted the criticality of accurate exposure data and pointed out the difficulties faced by multinational corporations in consolidating and interpreting information. This stressed the necessity of robust financial risk management through organizational data design, leveraging existing ERP or TMS technology or establishing a data lake for processing unstructured data.

4. The third wave of treasury digitalization

We’ve taken the three waves of digitalization coined by Steve Case (former CEO of US internet giant AOL) and applied them to the treasury function. The first wave was the development of stand-alone treasury and finance solutions, followed by the second wave bringing internal interfaces and external connectivity between treasury systems. The third wave is about how to leverage all the data coming from this connected treasury ecosystem. With generative AI predicted to have an influential role in this third phase, corporate treasurers need to incorporate the opportunities and challenges it poses into their organizations' digital transformation journeys and into discussions and decisions related to other technologies within their companies, such as TMS, ERP, and banking tools.

We also predict the impact and success of this third wave in treasury digitalization will be dependent on having the right regulatory frameworks to support its implementation and operation. The reality is, although we all aspire to work in a digital, connected world, we must be prepared to encounter many analogue frictions – like regulatory requirements for paper-based proof, sometimes in combination with ‘wet’ signatures and stamped documents. This makes the adoption of mandates, such as the MLETR (Model Law on Electronic Transferable Records) a priority.

5. Fragmentation and interoperability of the payment landscape

A side effect of the increasing momentum around digital transformation is fragmentation across the payments ecosystem. This is largely triggered by a rapid acceleration in the use of digital payments in various forms. We’ve now seen successful trials of Central Bank Digital Currency, Distributed Ledger Technology to enable cross border payments, a rise in the use of digital wallets not requiring a bank account, and the application of cross border instant payments. All of these developments lead us to believe that international banking via SWIFT will be challenged in the future and treasurers should prepare for a more fragmented international payment ecosystem that supports a multitude of different payment types. To benefit from this development, interoperability will be crucial.

Conclusion: A turning point for treasury

A succession of black swan events in recent years has exposed a deep need for greater financial resilience. The treasury function plays a vital role in helping their CFO build this. This is accelerating both the scale and pace of transformation across the treasury function, with wide-ranging effects on its role in the C-suite, position in finance, the priorities and structure of the function, and the investment required to support much-needed digitalization.

For more information on the five observations outline here, you can read the extended version of this article.

The European Committee has approved the NII SOT proposed by the EBA. Meanwhile the EBA has also published its focus areas for IRRBB in 2024 and 2025.

The European Committee (EC) has approved the regulatory technical standards (RTS) that include the specification of the Net Interest Income (NII) Supervisory Outlier Test (SOT). The SOT limit for the decrease in NII is set at 5% of Tier 1 capital. Since the three-month scrutiny period has ended it is expected that the final RTS will be published soon. 20 days after the publication the RTS will go into force. The acceptance of the NII SOT took longer than expected among others due to heavy pushback from the banking sector. The SOT, and the fact that some banks rely heavily on it for their internal limit framework is also one of the key topics on the heatmap IRRBB published by the European Banking Authority (EBA). The heatmap detailing its scrutiny plans for implementing interest rate risk in the banking book (IRRBB) standards across the EU. In the short to medium term (2024/Mid-2025), the focus is on

- The EBA has noted that some banks use the as an internal limit without identifying other internal limits. The EBA will explore the development of complementary indicators useful for SREP purposes and supervisory stress testing.

- The different practices on behavioral modeling of NMDs reported by the institutions.

- The variety of hedging strategies that institutions have implemented.

- Contribute to the Dynamic Risk Management project of the International Accounting Standards Board (IASB), which will replace the macro hedge accounting standard.

In the medium to long-term objectives (beyond mid-2025) the EBA mentions it will monitor the five-year cap on NMDs and CSRBB definition used by banks. No mention is made by the EBA on the consultation started by the Basel Committee on Banking Supervision, on the newly calibrated interest rate scenarios methodology and levels. In the coming weeks, Zanders will publish a series of articles on the Dynamic Risk Management project of the IASB and what implications it will have for banks. Please contact us if you have any questions on this topic or others such as NMD modeling or the internal limit framework/ risk appetite statements.

The European Banking Authority (EBA) published its roadmap on the Banking Package, which implements the final Basel III reforms in the European Union.

The European Banking Authority (EBA) published its roadmap on the Banking Package, which implements the final Basel III reforms in the European Union. This roadmap develops over four phases, and it is expected to be completed as follows:

- Phase 1: Covers 32 mandates in the areas of credit, market and operational risk, which predominantly result from the transition to Basel III. In addition, this first phase will also see the first mandates under the Capital Requirements Directive (CRD) in the area of ESG.

- Phase 2: This phase will further progress in covering Capital Requirements Regulation (CRR) mandates related to credit, operational and market risk. Furthermore, a considerable number of CRD mandates related to high EU standards in terms of governance and access to the single market with regard to third-country branches will be developed in this phase.

- Phase 3: It includes most of the remaining mandates related to regulatory products as well as a number of reports, whereby further perspectives and initial monitoring efforts regarding banking regulation implementation are worth considering.•

- Phase 4: In this last phase, a number of products, mostly consisting of reports, will be developed, providing information on the implementation progress, results and challenges.

In addition, there are some mandates that are ongoing and reoccurring and are not part of any of the four phases but will be made operational at the date of implementation in 2025. As part of phase 1, the EBA has published multiple consultation papers, which form the first step in the implementation of the Banking Package. The three main consultation papers published are:

- A public consultation on two draft ITS amending Pillar 3 disclosure requirements and supervisory reporting requirements. The suggested amendments on the reporting obligations cover a wide range of topics such as the output floor, standardized and internal ratings-based models (IRB) for credit risk, the three new approaches for own funds requirements for CVA risk and the (simplified) standardized approach for market risk.

- A public consultation launched by the EBA on the Regulatory Technical Standards (RTS) determining the conditions for an instrument with residual risk to be classified as a hedge. This consultation, on the standardized approach under the FRTB framework, focuses on the residual risk add-on (RRAO). Introduced by the Capital Requirements Regulation (CRR3), the RRAO framework allows exemptions for instruments hedging residual risks. The proposed RTS outline criteria for identifying hedges, distinguishing between non-sensitivity-based method risk factors and other reasons for RRAO charges.

- A public consultation on two draft Implementing Technical Standards (ITS) amending Pillar 3 disclosures and supervisory reporting requirements for operational risk. These revisions align with the new Capital Requirements Regulation (CRR3) and aim to consolidate reporting and disclosure requirements for operational risk and broader CRR3 changes. These consultation papers should be read in conjunction with the consultation papers on the new framework for the business indicator for operational risk, published at the same time.

This paper explores vital infrastructure decisions, regulatory scrutiny, and proposes a flexible risk approach for financial institutions in crypto asset navigation by 2025.

This paper offers a straightforward analysis of the Basel Committee on Banking Supervision's standards on crypto asset exposures and their adoption by 2025. It critically assesses infrastructure risks, categorizes crypto assets for regulatory purposes, and proposes a flexible approach to managing these risks based on the blockchain network's stability. Through expert interviews, key risk drivers are identified, leading to a framework for quantifying infrastructure risks. This concise overview provides essential insights for financial institutions navigating the complex regulatory and technological landscape of crypto assets.

This article explores the growing interest in sustainability among consumers and investors, the role of financial institutions in supporting green initiatives, and the rising concern about “greenwashing” – deceptive claims regarding environmental efforts by some financial institutions.

In recent years, consumers’ and investors’ interest in sustainability has been growing. Since 2015, assets under management in ESG funds have nearly tripled, the outstanding value of green bonds issued by residents of the euro area has surged eightfold, and emission-related derivatives have seen a more than sevenfold increase1.

The global push for sustainable and environmentally responsible practices has led to an increased focus on the role of financial institutions in supporting green initiatives. One of the ways financial institutions use to incentivise sustainable investments, is by designing new products, such as blue bonds to protect marine areas and other sustainability-linked bonds2, or by transitioning to funding sectors with positive sustainability impact.

However, amidst the growing wave of environmental consciousness, the credibility of "green" claims made by some financial institutions is a point of concern. This phenomenon, known as greenwashing, is gaining attention, not only within financial institutions, but also with regulators. Financial regulators, including the European Supervisory Authorities (ESAs) and UK’s Financial Conduct Authority (FCA) have taken action against potentially misleading green statements made by institutions. Despite these regulatory interventions, the persistent risk of greenwashing persists, primarily due to the absence of consistent standards governing sustainability claims and disclosures. The lack of uniform criteria poses an ongoing challenge to effectively combatting greenwashing practices within the financial landscape.

Defining Greenwashing

The ESAs describe greenwashing as “a practice where sustainability-related statements, declarations, actions, or communications do not clearly and fairly reflect the underlying sustainability profile of an entity, a financial product, or financial services. This practice may be misleading to consumers, investors, or other market participants” 3.

Financial institutions, as key players in the global economy, play a crucial role in fostering sustainability. However, some have been accused of using deceptive practices to push their green image without making substantial changes. This practice may be misleading to consumers, investors, and other market participants.

In practice, greenwashing can take different forms depending on the institution. For insurance companies, the European Insurance and Occupational Pensions Authority (EIOPA) found in their Advise to the European Commission on Greenwashing4 various examples where insurers misleadingly claimed to be transitioning their underwriting activities to net zero by 2050 without any credible plans to do so. Other examples include insurance companies falsely claiming to plant trees for each life insurance policy sold but failing to fulfil this promise, or products being marketed as sustainable merely because of a positive "ESG rating," despite the rating not taking into account any actual sustainability factors and focusing solely on financial risks.

Withing the banking sector, the EBA reported5 that the most common misleading claims relate to the current approach to integrating sustainability into the business strategy, claims on the sustainability results and the real-world impact, and claims on future commitments on medium and long-term plans.

Finally, for investment companies and pension funds, the European Securities and Markets Authority (ESMA) reported6 that most the common greenwashing practices result from exaggerated claims without any proven link between and ESG metric and the real-world impact.

Key Indicators of Greenwashing:

- Vague and Ambiguous Language: Financial institutions engaging in greenwashing often use vague terms and ambiguous language in their marketing materials. This lack of clarity makes it challenging for consumers to discern the actual environmental impact of their investments.

- Lack of Transparency: Genuine commitment to sustainability involves transparency about investment choices and the environmental impact of financial products. Institutions that are less forthcoming about their practices may be concealing less-than-green investments.

- Inconsistent Policies: Greenwashing is also evident when there is a misalignment between a financial institution's sustainability claims and its actual policies and practices. Actions, or lack thereof, can speak louder than words.

The Role of Regulatory Bodies

Greenwashing poses potential reputational and financial risks for the institutions involved. Addressing greenwashing might not only improve consumer’s trust in the products and services offered by financial institutions, but also will allow customers to make informed decisions that are align with their sustainability preferences and increase the capital into products that genuinely represent a more sustainable choice and drive a positive change. Tackling greenwashing should therefore be a priority for regulatory supervisors.

The introduction of the EU’s Taxonomy Regulation and the Sustainable Finance Disclosure Regulation (SFDR) addresses the initial concerns of greenwashing within the financial sector. The Taxonomy determines which economic activities are environmentally sustainable and addresses greenwashing by enabling market participants to identify and invest in sustainable assets with more confidence. SFDR promotes openness and transparency in sustainable finance transactions and requires Financial Market Participants to share the environmental and social impact of their transactions with stakeholders. In May 2023, the ESA published their progress report on greenwashing monitoring and supervision7. The report aims to provide insights into an understanding of greenwashing and identify the specific forms it can take within banking. It also evaluates greenwashing risk within the EU banking sector and determines the extend to which it might be and issue from a regulatory perspective.

In the UK, the FCA published in November 2023 a guidance consultation on the Anti-Greenwashing Rule8. The anti-greenwashing rule is one part of a package of measures introduced through the Sustainability Disclosure Requirements (SDR). The anti-greenwashing rule requires FCA-authorised firms to ensure that any claims they make to the sustainability characteristics of their financial products and services are consistent with the actual sustainability characteristics of the product or service and are fair, clear and not misleading, and have evidence to back them up. The propose rule will come into force on 31 May 2024.

While the existing and planned regulation contributes to addressing aspects of greenwashing, several measures have not yet fully entered into application, making the impact of the frameworks not visible yet. Beyond disclosures, regulators should also focus on tightening requirements on sustainability data and ratings, and creating mandates to prevent misleading statements and unfair commercial practices.

Going forward, as regulators gain more experience to comprehensively address greenwashing, financial institutions should expect increased supervision and enforcement of sustainable finance policies aimed at preventing misleading sustainability claims.

Actions to mitigate greenwashing risk

One of the biggest challenges financial institutions faced in relation to sustainability is that scientific progress, policy development and social values are in constant evolution. What was a well-supported green initiative two years ago can potentially be considered as greenwashing today.

In the meantime that stricter regulations and guidance is in place, financial institutions should take a broad view on how to develop and communicate sustainability strategies to mitigate greenwashing risk.

Here are three ways on how to prevent greenwashing:

- Promote disclosure: financial institutions should publish comprehensive sustainability reports and disclose ESG information as part of their financial reports.

- Commit to transparency: claims about environmental aspects or performance of their products should be justified with science-based and verifiable methods. Financial institutions should be transparent about their ambitions, status, and be open about any shortcomings they identified.

- Align business practices with purpose: financial institutions should determine which climate-related and environmental risks impact business strategy in the short, medium and long term. They should reflect climate-related and environmental risks in business strategies and its implementation. In addition, they should balance sustainability ambitions with the reality of real transformation.

Zanders’ approach to managing reputational risk

Avoiding greenwashing should always be a priority for institutions. If a risk arises in this area, reputational risk management can help to limit negative effects. Due to the interdependencies between ESG, reputational, business and liquidity risk, the supervisory authorities are also increasingly focusing on this area.

In the context of reputational risk management, we recommend a holistic approach that includes both existing and new business in the analysis. In addition to identifying critical transactions from a reputational perspective, the focus is also on active stakeholder management. This requires cross-departmental cooperation between various units within the institution. In many cases, the establishment of a reputation risk management committee is key to manage that topic properly within the institution.

Conclusion

While many financial institutions genuinely strive for sustainability, the rise of greenwashing highlights the need for increased vigilance and scrutiny. Consumers, regulators, and industry stakeholders must work together to ensure that financial institutions align their actions with their environmental claims, fostering a truly sustainable and responsible financial sector.

Curious to learn more? Please contact: Elena Paniagua-Avila or Martin Ruf

Citations

- European Central Bank, Climate-related risks to fiancial stability, 2021. ↩︎

- European Central Bank, Climate-related risks to fiancial stability, 2021. ↩︎

- European Banking Authority, Progress report on greenwashing monitoring and supervision, 2023. ↩︎

- European Banking Authority, Progress report on greenwashing monitoring and supervision, 2023. ↩︎

- European Banking Authority, Progress report on greenwashing monitoring and supervision, 2023. ↩︎

- European Securities and Markets Authority, Progress report on greenwashing, 2023. ↩︎

- European Banking Authority, Progress report on greenwashing monitoring and supervision, 2023. ↩︎

- Financial Conduct Authority, Guidance on the Anti-Greenwashing rule, 2023. ↩︎

Model risk from risk models has become a focal point of discussion between regulators and the banking industry.

Model risk from risk models has become a focal point of discussion between regulators and the banking industry. As financial institutions strive to enhance their model risk management practices, the need for robust model risk quantification becomes paramount.

An introduction to model risk quantification

Many firms already have comprehensive model risk management frameworks that tier models using an ordinal rating (such as high/medium/low risk). However, this provides limited information on potential losses due to model risk or the capital cost of already identified model risks. Model risk quantification uses quantitative techniques to bridge this gap and calculate the potential impact of model risk on a business.

The goal of a model risk quantification framework

As with many other sources of risk within a financial institute, the aim is to manage risk by holding capital against potential losses from the use of individual models across the firm. This can be achieved by including model risk as a component of Pillar 2 within the Internal Capital Adequacy Assessment Process (ICAAP).

Key components of a quantification framework

An effective model risk quantification framework should be:

- Risk-based: By utilising model tiering results to identify models with risk worth the cost of quantifying.

- Process driven: By providing a system for identifying, measuring and classifying the impact of model risks.

- Aggregable: By producing results that can be aggregated and including a methodology for aggregating model results to a firm level.

- Transparent & capitalised: By regularly reporting aggregated firm-wide model risk and managing it using capitalisation.

Blockers impeding model risk quantification

Complications of quantification include:

- Implementation and running costs: Setting up and regularly running any quantification test involves significant resource costs.

- Uncovered risk: Trying to quantify all potential model risk is a Sisyphean task.

- Internal resistance: Quantification and capitalisation of model risks will require increased resources to produce, leading to higher costs, making it a hard initiative to motivate individuals to follow.

Concepts in Model Risk Quantification

Impacts of Model Risk

Model risk significantly influences financial institutions through valuations, capital requirements, and overall risk management strategies. The uncertainties tied to model outcomes can have profound impacts on regulatory compliance, economic capital, and the firm's standing in the financial ecosystem.

Model tiering

Model tiering is a qualitative exercise that assesses the holistic risk of a model by considering various factors (e.g. materiality, importance, complexity, transparency, operational intricacies, and controls).

The tiering output grades the risk of a model on an ordinal scale, comparing it to other models within the institute. However, it doesn't provide a quantitative metric that can be aggregated with other models.

Overlap with quantitative regulations

Most firms already perform quantitative processes to measure the performance of Pillar 1 models that impact the regulatory capital held (such as the VaR backtesting multiplier applied to market risk RWA).

Model Risk Quantification Framework - The Model Uncertainty Approach

A crucial step in building a robust model risk quantification framework is classifying and assessing the impact of model risk. The model uncertainty approach is an internal quantitative approach in which model risks are identified and quantified on an individual level. Individual model risks are subsequently aggregated and translated into a monetary impact on the bank.

Regulatory Model Risk Quantificaiton Methods - RNIV, Backtesting Multiplier, Prudent Valuation and MoC

Most banks are already familiar with quantification techniques recommend by regulators for risk management. Below we highlight some of these techniques that can be used as the basis for expansion of quantification within a firm.

Expanding Model Risk Quantification

Our approach to efficient measurement relies on two key components. The first is model risk classifications to prioritize models to quantify, and the second is a knowledge base of already implemented regulatory and internally developed techniques to quantify that risk. This approach provides good risk coverage whilst also being extremely resource efficient.

Looking to learn more about Model Risk Management? Reach out to our experts Dr. Andreas Peter, Alexander Mottram, Hisham Mirza.

This article describes the current status of the IFRS 9 landscape, six years after the IFRS 9 accounting standards replaced IAS 39.

We touch upon the main difficulties experienced by financial institutions in the Netherlands based on a combination of project experience, results of a survey, main attention points from the eyes of the regulator and observations from publicly available annual reports. Interested to learn more about the IFRS 9 framework components banks struggle with the most and whether these challenges can be easily solved? Find out in the remainder of this article.

Introduction

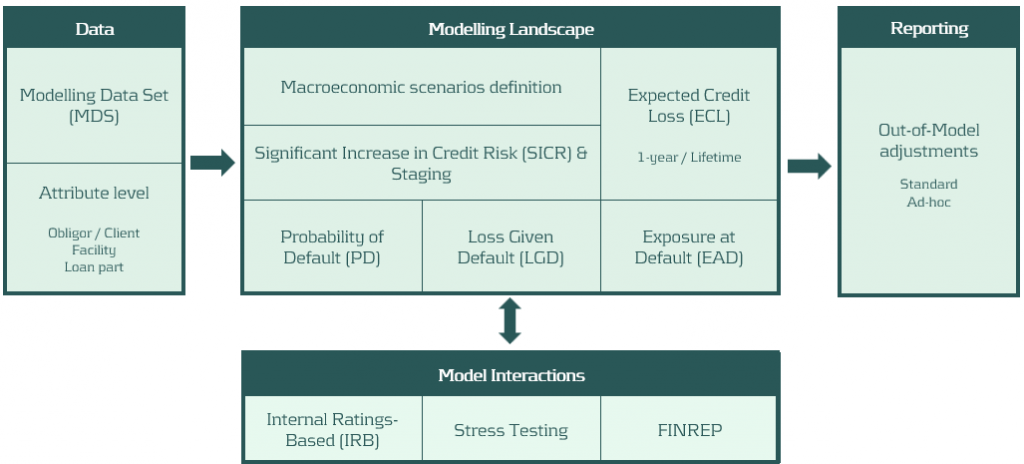

The main objective of this article is to provide insight into market practices and common challenges within the IFRS 9 landscape of Dutch financial institutions. In this light, Zanders conducted a survey amongst Dutch financial institutions. Six main IFRS 9 framework components form the basis of the survey: data quality, model components (PD, LGD, EAD), SICR & staging, macroeconomic scenarios, out-of-model adjustments and the relation between IFRS 9 and other models within the bank. An example of a full IFRS 9 framework overview is presented in Figure 1. The questionnaire was followed up by a roundtable in which the most noticeable results from the survey were discussed with the participants.

Besides the survey, the IFRS 9 monitoring report published by the European Banking Authority (IFRS 9 Monitoring report, EBA (November 2023)) provides insights into the key IFRS 9 attention points from a regulatory perspective (e.g. as identified by EBA). In this article, we discuss the key differences between the difficulties experienced by banks versus attention points highlighted in the monitoring report. Lastly, this article uses publicly available information from annual reports to illustrate the diverging modeling practices and model behavior amongst market peers.

Figure 1: IFRS 9 framework overview.

Survey

The IFRS 9 survey held in Q4 2023 was centered around the six framework components as stated in the introduction section and which are graphically presented in Figure 1. The participating banks were asked in which areas of the framework they experience difficulties. Consequently, each area was explored deeper by means of questions directly related to each area.

All participating banks except one indicate difficulties in the areas of data quality and out-of-model adjustments (e.g. overlays). For data quality, changing policies (e.g. Definition of Default, loan quality assessment), limited loss realizations for LGD (as well as limited detail of the loss realization data) and dealing with unrepresentative data from the Covid-19 period are examples of reasons for the difficulties experienced in this area. With regards to out-of-model adjustments, it becomes apparent that many banks struggle with pressure from the regulator and audit, triggering banks to find an escape in overlays on the IFRS 9 model outcomes. Overlays are applied on a wide variety of topics, in various ways (e.g. calculated, constant, periodic, expert based, etc.) and sometimes constitute the majority of the total provisions. Altogether, this illustrates the need to have out-of-model adjustments in place that are sufficiently qualitatively substantiated and, whenever possible, are applied on the model component level. At the same time, we are of the opinion that out-of-model adjustments are sometimes over-used to make up for model deficiencies. Especially when out-of-model adjustments constitute the majority of the total provisions, compliance of the model with the IFRS 9 best-estimate principle should be questioned.

Surprisingly, only one third of the respondents experiences difficulties in the framework areas that came into existence with the introduction of IFRS 9; SICR & staging and macroeconomic scenarios. A possible explanation for this is that the responsibility for these framework areas is often distributed across multiple departments. Macroeconomic predictions and scenario weights are usually determined by a separate macroeconomic scenario department or committee, and staging assessments are often placed outside the scope of IFRS 9 modeling teams. From a governance perspective, we are of the opinion that more alignment over the full IFRS 9 provisioning chain is desired.

Want to know more about the survey results? Download our white paper.

Regulatory view

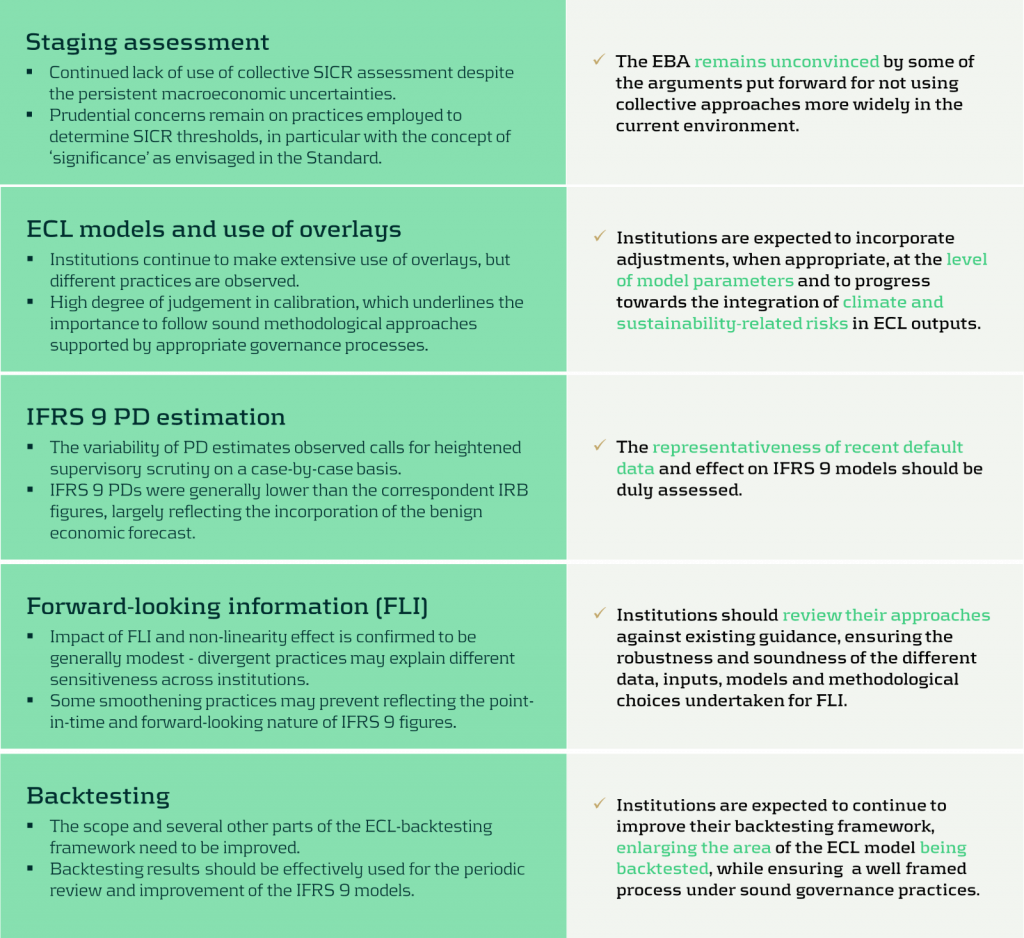

The EBA published a monitoring report in November 2023 on the current status of the IFRS 9 model landscape (IFRS 9 Monitoring report, EBA (November 2023)). In this report the EBA highlights several takeaways, which are shown in Figure 2. One of these takeaways is the manner in which SICR is modelled at the moment. The EBA is not convinced that non-collective approaches are more suitable than collective approaches. In the results of the survey however, it was shown that most respondents did not indicate SICR as one of the main challenges in their IFRS 9 landscape. This raises the question whether banks in the Netherlands are aware of the EBA’s remark on the current SICR approaches, or whether Dutch banks are outliers when it comes to the SICR modeling approaches.

Furthermore, the report indicates that out-of-model adjustments should be applied on the model parameter level and not on the outcome level. During the roundtable it was discussed that several participants recognize this desire from the regulator, but that they still apply it on the outcome level because the available data only allows for this level. This discrepancy could lead to further scrutiny from the regulator in the near future.

Figure 2: Key takeaways from the IFRS 9 monitoring report (EBA, 2023).

Annual report study

In the Dutch banking market, a variety of modeling practices is observed when it comes to IFRS 9 models for calculating credit loss provisions. Besides gaining insights into these IFRS 9 modeling practices via a survey, annual reports are analyzed to identify potential differences (or similarities) from information that is publicly available.

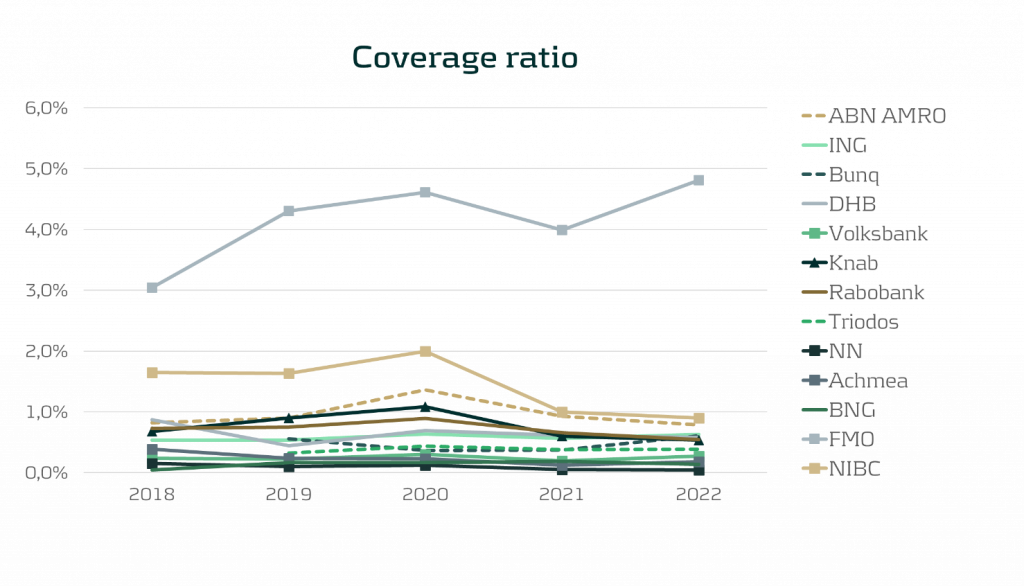

One of the observations from comparing annual reports is that no common level is observed for the Provisioning Coverage Ratio (PCR), i.e. the percentage of funds set aside for covering losses due to bad debts. Characteristics such as portfolio type/composition and loan maturity likely explain these differences. In 2020, almost all banks show an increase in the PCR due to increased allowances in response to the Covid-19 pandemic. Note that this was not necessarily caused by models picking up changing macroeconomic dynamics, but because of model overlays. PCR levels stabilized again in 2021 and 2022.

Figure 3: Coverage ratio over the years 2018 till 2022 . All results were gathered from public annual reports.

Although not all banks report macroeconomic scenario weights in their annual reports, it is worth noting that large differences exist in the scenario weights of banks that do report these figures. Especially weights assigned to the up and down scenarios vary significantly. In 2022, the weight percentage for the base scenario is generally between 40% and 60% (one bank uses a weight of 30%), whereas the weight percentage for the down scenario ranges from 20% to 60%. For the up scenario, percentage weights differ from 2% to 30%. It must be noted that the scenario weights cannot be judged without considering the actual scenario definitions/severity. Nonetheless, the wide variety in scenario weight percentages as well as large differences in the development of these scenario weights over time raises questions on the accuracy of macroeconomic predictions. In addition, it also complicates the comparability of IFRS 9 figures amongst banks.

What can Zanders offer?

We combine deep credit risk modeling expertise with relevant experience in regulation and programming:

- A Risk Advisory Team consisting of 75+ consultants with quantitative backgrounds (e.g. Econometrics and Physics);

- Strong knowledge of IFRS 9 models and developments in the IFRS 9 landscape;

- Extensive experience with calibration, implementation and validation of IFRS 9 models;

- We offer ready-to-use Expected Credit Loss models, Credit Risk Academy modules and expert sessions that can be tailored to the needs of your organization.

Interested to learn more? Contact Kasper Wijshoff or Michiel Harmsen for questions on IFRS 9.

EBA publishes recommendations how to include E&S risks in the prudential framework for banks and insurers.

In October 2023, the European Banking Authority (EBA) published a report[1] with recommendations for enhancements to the Pillar 1 prudential framework to reflect environmental and social (E&S) risks, distinguishing between actions to be taken in the short term and in the medium to long term. The short-term actions are to be taken into account over the next three years as part of the implementation of the revised Capital Requirements Regulation and Capital Requirements Directive (CRR3/CRD6).

The EBA report follows a discussion paper on the same topic from May 2022[2], on which it solicited input from the financial industry. In this note, we provide an overview of the recommended actions by the EBA that relate to the prudential framework for banks. The EBA report also contains recommended actions for the prudential framework applying to investment firms, but these are not addressed here.

If the EBA’s recommendations are implemented in the prudential framework, in our view the most immediate implications for banks would be:

- When using external ratings to determine own fund requirements for credit risk under the standardized approach (SA) of Pillar 1, ensure that E&S risks are explicitly considered when evaluating the appropriateness of the external ratings as part of the due diligence requirements.

- When calculating own fund requirements for credit risk under the internal-ratings-based (IRB) approach, embed E&S risks in the rating assignment, risk quantification (for example through a margin of conservatism or the downturn component) and/or expert judgment and overrides.

- To assess E&S risks at a borrower level, establish a process to obtain and update material E&S-related information on the borrowers’ financial condition and credit facility characteristics, as part of due diligence during onboarding and ongoing monitoring of the borrowers’ risk profile.

- For IRB banks, embed E&S risks in the credit risk stress testing programs.

- Ensure that E&S risks are considered in the valuation of collateral, specifically for financial and real estate collateral.

- For market risk, embed environmental risks in trading book risk appetite, internal trading limits and the new product approval process. Furthermore, for banks aiming to use the internal model approach (IMA) of the Fundamental Review of the Trading Book (FRTB) regulation, environmental risks need to be considered in their stress testing program.

- For operational risk, identify whether E&S risks constitute triggers of operational risk losses.

We note that many of these implications align with the ECB’s expectations in the ECB Guide on climate-related and environmental risks[3].

Background

The EBA report considers both environmental and social risks, which the EBA characterizes as follows:

- As drivers of environmental risks, EBA distinguishes physical and transition (climate) risks. It does not explicitly refer in the report to other environmental risks, such as a loss of biodiversity or pollution, but in an earlier report the EBA considered these as part of chronic physical risks[4].

- EBA considers social factors to be related to the rights, well-being and interests of people and communities, including factors such as decent work, adequate living standards, inclusive and sustainable communities and societies, and human rights. As drivers of social risks, EBA distinguishes environmental factors (as materialization of physical and transition risks may change living standards and the labor market and increase social tensions, for example) as well as changes in policies and market sentiment. These may in part be driven by actions taken to meet the United Nation’s sustainable development goals (SDGs) in 2030.

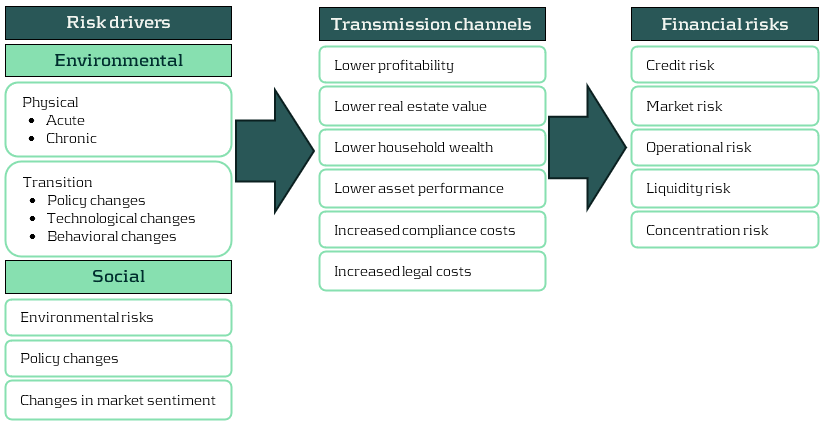

In line with the ECB Guide on climate-related and environmental risks[5], the EBA does not view E&S risks as stand-alone risks, but as drivers of traditional banking risks. This is depicted in Figure 1. The report considers the impact on credit, market, operational, liquidity and concentration risks and reviews to what extent E&S risks can be reflected in capital buffers and the macro-prudential framework. It does not explicitly consider the securitization framework, although this will be implicitly affected by impacts on credit risk. The EBA does not see an impact of E&S risks on the (risk-insensitive) leverage ratio, and therefore does not consider it in the report.

Figure 1: Examples of transmission channels for environmental and social risks (source: EBA).

The EBA notes that the Pillar 1 framework has been designed to capture the possible financial impact of cyclical economic fluctuations, but not to capture the manifestation of long-term environmental risks. It is therefore important to keep the main principles that form the basis of the prudential framework in mind when contemplating adjustments to reflect E&S risks in the prudential framework. The main principles as highlighted by the EBA are summarized below.

Main principles of the prudential framework and the relation to the horizon for E&S risks

With repect to the framework in general:

- Own fund requirements are intended to cover potential unexpected losses. In contrast, expected losses are directly deducted from own funds, and are generally captured in the accounting rules through provisions, impairments, write-downs and appropriate valuation of assets.

- The purpose of own fund requirements is to ensure resilience of an institution to unexpected adverse circumstances, before appropriate mitigating actions and strategy adjustments can be implemented. Therefore, environmental factors that can affect institutions in the short to medium term are expected to be reflected in the prudential framework. However, for those with an impact in the longer term, institutions are expected to take appropriate mitigating actions in their strategy.

- The high confidence level used in the Pillar 1 framework to protect institutions from risks over the short to medium horizon may no longer be achievable and appropriate if longer horizons would be considered.

- To the extent that institutions are exposed to E&S risks in relation to their specific strategy and business model, coverage of these risks in the Pillar 2 own-fund requirements instead of Pillar 1 could be appropriate. In addition, reflection of these risks in the Pillar 2 guidance for stress testing may be considered.

With respect to the internal-ratings-based (IRB) approach for credit risk:

- The Probability of Default (PD) represents a one-year default probability, which is required to be calibrated based on long-run average (‘through-the-cycle’) default rates. As such, longer-term risk characteristics of the obligor may be taken into account.

- The Credit Conversion Factor (CCF) as an estimate of potential additional drawdowns before default naturally relates to the one-year time horizon for the PD, but is expected to reflect the situation of an economic downturn.

- The time horizon for the Loss Given Default (LGD) extends to the full maturity of the exposure and/or the collection process and its calibration is also expected to reflect the situation of an economic downturn.

In the following sections we summarize the EBA recommendations by risk type.

Credit risk

The recommendations of the EBA largely put the burden on financial institutions to take E&S risks into account in the inputs for the existing Pillar 1 framework and/or to apply conservatism or overrides to the outputs. It does not recommend to include explicit E&S risk-related elements in the determination of risk weights for rated and unrated exposures in the SA or in the risk-weight formulas of the IRB. The main reasons for not doing so are that it is not clear what common and objective E&S-related factors should be used as input, what the proper functional form would be, a lack of evidence on which the size of an adjustment could be based so that it results in proper risk differentiation, and the risk of double counting with the reflection of E&S risks in the inputs to the existing own funds calculations under Pillar 1 (external ratings in the SA and PD, LGD and CCF in the case of IRB). However, the EBA will continue to evaluate this possibility in the medium to long term. The EBA also does not recommend introducing an environment-related adjustment factor to the risk weights resulting from the existing Pillar 1 framework[6].

Recommended actions for credit risk

| Short term |

- SA) The EBA encourages rating agencies to integrate environmental and social factors as drivers in the external credit risk assessments and to provide enhanced disclosures and transparency about the rating methodologies.

- (SA) Financial institutions to explicitly consider environmental factors in the due diligence that they are required to perform when using external credit risk assessments.

- (IRB) Financial institutions to reflect E&S risks in the rating assignment, risk quantification (for example through a margin of conservatism or the downturn component) and/or expert judgment and overrides, without affecting the overall performance of the rating system. In this context:

- Quantification of risks must be based on sufficient and reliable observations;

- Overrides should be for specific, individual cases where the institution believes there is material exposure to E&S risks but it has insufficient information to quantify it. Such overrides need to be regularly assessed and challenged;

- If an institution derives PDs for internal rating grades by a mapping to a scale from a credit rating institution, it needs to consider whether the default rates associated with the external scale reflect material E&S risks.

- To assess E&S risks at a borrower level, institutions need to have a process to obtain and update material E&S-related information on the borrowers’ financial condition and on credit facility characteristics, as part of the due diligence during onboarding and ongoing monitoring of borrowers’ risk profile.

- (IRB) Financial institutions to consider E&S risks in their stress testing programs.

- (SA, IRB) Financial institutions to ensure prudent valuation of immovable property collateral, considering climate-related physical and transition risks as well as other environmental risks. The prudent valuation should be considered at origination, re-valuation and during monitoring.

| Medium to long term |

- (SA) Financial institutions to monitor that environmental factors are reflected in financial collateral valuations through market values under Pillar 1 and valuation methodologies under Pillar 2.

- (SA) The EBA to consider whether benefits from the Infrastructure Supporting Factor (ISF) should only be applied to high-quality specialized lending corporate exposures that meet strong environmental standards.

- (SA) The EBA to consider adjusting risk weights, both in general and specifically for those assigned to real estate exposures.

- (IRB) As E&S risks materialize in defaults and loss rates over time, institutions need to redevelop or recalibrate their PD and LGD estimates.

(SA = standardized approach; IRB = Internal-rating-based approach)

Market risk

Within market risk, the EBA sees the main interaction of E&S risks with the equity, credit spread and commodity markets, in which E&S risks may cause additional volatility. In line with the existing regulatory guidance, the EBA expects E&S risks not to be treated as separate risk factors but as drivers of existing risk factors, with the exception of products for which cash flows depend specifically on ESG factors (‘ESG-linked products’).

The EBA does not recommend changes at this point to the standardized approach (SA) and the internal model approach (IMA) under the FRTB regulation, which will come into effect in the EU in 2025. The primary reason is the lack of sufficient evidence on the impact of E&S risks to enable a data driven approach, which forms the basis of the FRTB.

When calculating the expected shortfall (ES) measure under the IMA based on last 12 months' market data, the materialization of E&S risks will automatically be reflected in the market data that is used. When using market data from a stress period, either to calculate ES in the IMA or to calibrate risk factor shocks for the sensitivity-based measure (SbM) at a risk class level in the SA, the reflection of E&S risks will depend on the choice of stress period. To include E&S risks fully in the IMA but avoid overlap with the (partial) presence of E&S risks in historical data, the EBA views the consideration of E&S risks in a separate ‘risk not in the model engine’ (RNIME) add-on as most promising option for the medium to long term, leveraging the framework described in the ECB Guide to internal models[7].

Recommended actions for market risk

| Short term |

- (SA, IMA) Financial institutions to consider environmental risks in relation to their trading book risk appetite, internal trading limits and new product approval.

- (IMA) Financial institutions to consider environmental risk as part of their stress testing program that is required to get internal model approval.

| Medium to long term |

- (SA, IMA) Competent authorities to consider how to treat ESG-linked products for the residual risk add-on in the SA and in the IMA.(SA) The EBA to consider including a dimension for ESG risks in the existing equity and credit spread risk classes, or including a separate environmental risk class.

- (IMA) Financial institutions to consider ESG risks when monitoring risks that are not included in the model, for which the ECB’s RNIME framework could be used as a basis.

(SA = standardized approach; IRB = Internal-rating-based approach)

Operational risk

The EBA notes that various types of operational risks can increase as a result of E&S risks, including damage to physical assets, disruption of business processes and litigation. However, the new standardized approach (SA) for operational risk in the Basel III framework, which will come into effect in the EU in 2025, does not have a forward-looking component – it only considers historical loss experience (besides business indicators). Historical losses are unlikely to fully reflect the potential future impact of E&S risks, but there is as of yet insufficient evidence and data to quantify and consider this in an amendment of the SA.

Recommended actions for operational risk

| Short term |

- Financial institutions to identify whether E&S risks constitute triggers of operational risk losses.

| Medium to long term |

- Following evidence of E&S risk factors to trigger operational risk losses, the EBA to consider whether revisions to the BCBS SA methodology are warranted.

Liquidity risk

The EBA report describes three ways in which E&S risks may affect the liquidity coverage ratio (LCR) calculation. First, liquid assets that are specifically exposed to E&S risks may become less liquid and/or decrease in value. As a consequence, they may no longer satisfy the eligibility criteria for liquid assets. If they still do, then the decrease in market value would reflect the lower liquidity and reduce the LCR. Second, contingent liabilities arising from environmentally harmful investments would need to be included as outflows in the LCR calculation, thereby lowering the LCR. Third, a decrease in credit quality of receivables that are particularly exposed to E&S risks will decrease the inflows that can be taken into account in the LCR calculation. The EBA concludes that the existing LCR framework can capture the impact of E&S risks on the definition of liquid assets, outflows and inflows, so that no amendments are needed.

Regarding the existing framework for the net stable funding ratio (NSFR), the EBA notes that a reduction in the creditworthiness and/or liquidity of loans and securities exposed to E&S risks would lead to a higher requirement for stable funding and thereby negatively impact the NSFR. In this way, the existing NSFR framework can capture the impact of E&S risks on the definition of stable assets.

In summary, the EBA does not propose changes to the LCR and NSFR frameworks in relation to E&S risks. In case of excessive exposure to E&S risks for individual institutions, it notes that supervisors can set specific liquidity or funding requirements as part of the Pillar 2 framework for LCR and NSFR.

Concentration risk

The SA and IRB of the Pillar 1 framework for credit risk assume that a bank’s loan portfolio has full diversification of name-specific (idiosyncratic) risk and is well diversified across sectors and geographies. Because of these assumptions, the framework is not able to capture concentration risks, including those arising from E&S risks. In the current framework, single-name concentration risk is separately captured in Pillar 1 using the large exposure regime. Sector and geographic concentrations are considered in the SREP process under Pillar 2.

Recommended actions for concentration risk

| Short term |

- The EBA to develop a definition of environment-related concentration risk as well as exposure-based metrics for its quantification (e.g., ratio of exposures sensitive to a given environmental risk driver in a specific geographical area or in a specific industry sector over total exposures, total capital or RWA). These metrics will be part of supervisory reporting and, when relevant, external disclosure. In addition, they should be considered as part of Pillar 2 under SREP and/or supplement Pillar 3 disclosures on ESG risks.The EBA does not recommend to change the existing large exposure regime.

| Medium to long term |

- Based on the experience obtained with initial environment-related concentration risk metrics and quantification, the EBA may consider enhanced metrics and the appropriateness to introduce it in the Pillar 1 framework.

- This would entail the design and calibration of possible limits and thresholds, add-ons or buffers, as well as the specification of possible consequences if there are breaches.

Capital buffers and macroprudential framework

An alternative to amending the calculation of capital requirements to capture E&S risks in the prudential framework would be to increase the minimum required level of capital and/or to implement ‘borrower-based measures’ (BMM). Such BMMs aim to prevent a build-up of risk concentrations, for example by setting upper bounds on loan-to-value or loan-to-income for mortgage lending. Of the various possibilities, the EBA deems the use of a systemic risk capital buffer as the most suitable, although a double counting with the inclusion of E&S risks in the calculation of capital requirements under Pillar 1 and 2 needs to be avoided.

Recommended actions for capital buffers and macroprudential framework

| Short term |

- The EBA to asses changes to the guidelines on the appropriate subsets of sectoral exposures to which a systematic risk buffer may be applied.

| Medium to long term |

- The EBA to coordinate with other ongoing initiatives and assess the most appropriate adjustments.

Conclusion

The EBA considers E&S risks as a new source of systemic risk, which may not be adequately captured in the existing prudential framework. At the same time, the EBA recognizes the challenges in assessing the impact of these risks on regulatory metrics. The challenges range from a lack of granular and comparable data, varying definitions of what is environmentally and socially sustainable, historic data not being representative of what can be expected in the future, to the high uncertainty about the probability of future materialization of E&S risks. Moreover, the time horizon considered in the existing Pillar 1 framework is much shorter than the long horizon over which environmental risks are likely to fully materialize, with an exception of short-term acute physical and transition risks.

Against this background, the EBA does not recommend concrete quantitative adjustments to the existing Pillar 1 framework at this point. Nonetheless, it does expect financial institutions to take E&S risks into account in the inputs to the existing Pillar 1 framework or to apply overrides based on expert judgment. The EBA further proposes actions that should provide more clarity over time about the drivers and materiality of E&S risks. In due time, this can provide the basis for quantitative amendments to the Pillar 1 framework.

If you are interested to discuss this topic in more detail or would like support to embed E&S risks in your organization, please contact Pieter Klaassen at [email protected] or +41 78 652 5505.

[1]EBA (2023), Report on the role of environmental and social risks in the prudential framework (link), October.

[2] EBA (2022), Discussion paper on the role of environmental risks in the prudential framework (link), May. For a summary, see the article (link) on the Zanders website.

[3] ECB (2020), Guide on climate-related and environmental risks (link), November.

[4] See section 2.3.2 in EBA (2021), Report on management and supervision of ESG risks for credit institutions and investment firms (link), June.

[5] ECB (2020), Guide on climate-related and environmental risks (link), November.

[6] In the current EU Pillar 1 framework, adjustments are included that result in lower risk weights for small- and medium-sized enterprises (SME) and infrastructure lending. As the EBA notes, these adjustments are not risk-based but have been included in the EU to support lending to SMEs and for infrastructure projects.