Introducing the Debt Capacity module: a powerful new addition to Zanders’ Transfer Pricing Suite, enabling fast, accurate, and scalable debt capacity testing for multinational entities.

In the ongoing efforts to enhance tax transparency for multinational corporations, tax authorities have progressively increased scrutiny on intercompany financial transactions. While the interest rates on intra-group loans have long been a focus of regulatory attention, recent administrative guidelines have shifted the spotlight toward the level of indebtedness of borrowers. For instance, the German Federal Ministry of Finance recently issued new guidelines mandating a debt capacity test for intercompany financial transactions1.

Although many multinational entities already have compliant solutions in place to determine arm’s length interest rates, the same cannot be said for debt capacity tests. Historically, verifying the level of indebtedness for subsidiaries has relied on complex, manual analyses conducted in Excel spreadsheets. These methods, while tailored, often lack efficiency and scalability.

Today, we are thrilled to announce the launch of a new addition to our Transfer Pricing Suite: the Debt Capacity module. This innovative tool allows clients to build on their pricing analyses by quickly and accurately testing the debt capacity of borrower entities. Staying true to the essence of our Transfer Pricing Suite, the module is user-friendly yet delivers best-in-class support for tax compliance.

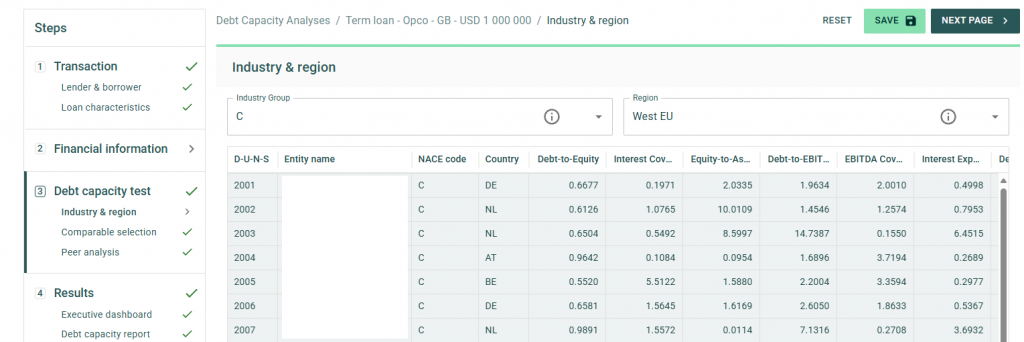

To streamline your in-house workflow, the standard package includes access to comparable data for a wide variety of borrowers. Within seconds, the application can automatically generate 40 comparable peers based on the borrower’s size, country, and industry through our connection with Dun & Bradstreet. Additionally, users can adjust and amend the list of comparable peers to ensure robust and tailored debt capacity tests for any scenario.

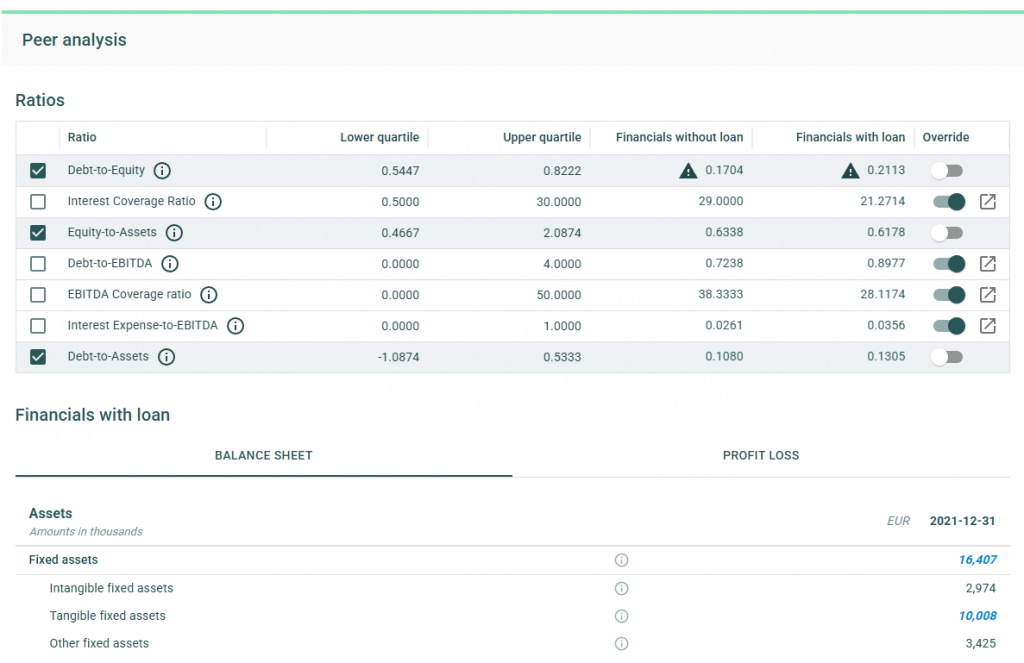

The debt capacity test leverages a flexible framework of financial ratios, which can be customized on a case-by-case basis. Our financial models dynamically adjust a borrower’s ratios to account for the impact of new loans on the balance sheet. With financial data for comparable entities readily available in the application, users receive feedback on debt capacity tests in under a minute.

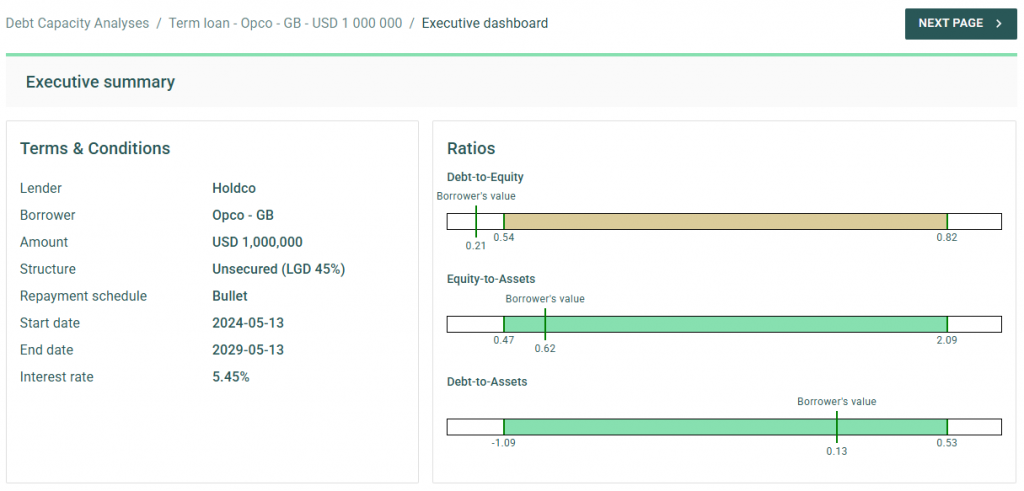

Upon completing the analysis, the application offers the option to generate a comprehensive report, available in Word or PDF formats. This detailed report outlines the methodology and underlying data used in the analysis, serving as an excellent complement to existing pricing reports and providing critical compliance support when it matters most.

After releasing the initial version of the Debt Capacity module to clients, we will work on continuing to improve our applications. For example, by further supporting the debt capacity test through the inclusion of a dedicated cash flow forecast and an increase in comparable companies. If you’re interested in learning more, we invite you to contact our Transfer Pricing team to schedule a demo or trial the new module within your Zanders Inside environment.

Zanders Transfer Pricing Solution

As tax authorities intensify their scrutiny, it is essential for companies to carefully adhere to the recommendations outlined above. Does this mean additional time and resources are required? Not necessarily.

Technology provides an opportunity to minimize compliance risks while freeing up valuable time and resources. The Zanders Transfer Pricing Suite is an innovative, cloud-based solution designed to automate the transfer pricing compliance of financial transactions.

With over seven years of experience and trusted by more than 80 multinational corporations, our platform is the market-leading solution for intra-group loans, guarantees, and cash pool transactions.

Our clients trust us because we provide:

- Transparent and high-quality embedded intercompany rating models.

- A pricing model based on an automated search for comparable transactions.

- Automatically generated, 40-page OECD-compliant Transfer Pricing reports.

- Debt capacity analyses to support the quantum of debt.

- Legal documentation aligned with the Transfer Pricing analysis.

- Benchmark rates, sovereign spreads, and bond data included in the subscription.

- Expert support from our Transfer Pricing specialists.

- Quick and easy onboarding—completed within a day!

Learn more, and discover the key compliance challenges for intra-group loan transfer pricing in 2025.

Citations

- See our blog on Transfer Pricing best practices 2025 for more information. ↩︎

Discover the key compliance challenges for intra-group loan transfer pricing in 2025.

Over the past year, the interest rates on intercompany financial transactions have come under closer examination by tax authorities. This intensified scrutiny stems from a mix of factors, including evolving regulations, more sophisticated audit procedures, the need from governments to boost revenue, and of course, high-interest-rate environment.

As a result, these transactions are now being assessed with greater depth and rigor than ever before. Historically, tax authorities focused on interest rate benchmarks as the primary point of analysis. However, their attention has now widened significantly to cover a range of interrelated considerations.

Below is a brief overview of the key trends and areas attracting the most scrutiny in today’s landscape, highlighting what multinationals should pay attention to in 2025:

Arm’s length T&Cs

In the past years, tax authorities are closely examining the terms and conditions of intra-group debt, scrutinizing the pricing of loans and the effects of increased leverage.

Accordingly, it is critical to ensure that the loan’s terms and conditions reflect the arm’s length standards and align with the actual economic substance of the transaction. This includes evaluating whether a hypothetical independent borrower, under similar conditions, could and would obtain a comparable loan.

In addition to establishing an arm’s length interest rate and the appropriate amount of debt (further explained below), it is also necessary to assess whether the other terms and conditions are at arm’s length. This involves considering the main features of the loan—such as currency, maturity, repayment schedule, and callability—and evaluating their impact on the risk profile of both the borrower and the lender, as well as on the arm’s length interest rate.

In this regard, tax authorities may challenge intra-group loans that do not include a maturity date, have an excessively long maturity (e.g., over 25 years), or lack a repayment schedule, since third-party loans would generally include these provisions.. They might also challenge situations where the actual conduct of the parties does not reflect the terms and conditions outlined in the loan agreement. For example, if the parties apply a different maturity or repayment schedule than the one initially agreed upon—without amending the legal documentation, which often happens in a dynamic intra-group financing environment—this could prompt further scrutiny from tax authorities.

As a result, it is important for multinational enterprises to carefully consider these terms and conditions before issuing a loan, as they will have a direct impact on the interest rate applied in the transaction. Drafting a comprehensive loan agreement that clearly outlines these terms, aligns with the conditions applied in practice, and is supported by a robust Transfer Pricing analysis is recommended to mitigate the risk of challenges by tax authorities.

Debt Capacity Analysis

One of the most important terms and conditions that must meet arm’s length standards is the so-called quantum of debt (i.e. nominal amount of the loan extended). Tax authorities are increasingly scrutinizing whether the amount of intra-group debt is economically justified and supported by a clear business purpose. They also evaluate whether the debt aligns with arm’s length principles and serves a legitimate economic function consistent with the borrower’s overall business strategy.

A debt capacity analysis is often conducted to determine whether the borrower has the financial capacity to repay the loan and whether an unrelated party would provide a similar amount of financing under comparable conditions.

While many jurisdictions have long required this type of analysis in practice, Germany has taken a step further by formalizing this requirement under its 2024 Growth Opportunities Act. This was further clarified on December 12, 2024, when the German Federal Ministry of Finance issued administrative principles providing specific guidance on financing relationships under the new Transfer Pricing provisions. According to these principles, the debt capacity test hinges on two key criteria:

(i) a credible expectation that the debtor can meet its obligations (e.g., interest payments and principal repayments),

and (ii) a commitment to provide financing for a defined period.

As a result, multinational enterprises are expected to robustly justify the level of debt assumed by their subsidiaries, particularly for entities operating in Germany.

Credit Rating Analyses

Tax authorities are increasing their focus on credit rating analyses. While simplified approaches, such as applying a uniform credit rating across all subsidiaries, were once more widely accepted, current practices favour a more detailed entity by entity evaluation. This involves first assigning a stand-alone credit rating to the individual borrower and then adjusting it to account for any implicit or explicit group support.

In this context, Swiss tax authorities published last year a Q&A addressing various Transfer Pricing topics. In the section on financial transactions, they emphasized a clear preference for the bottom-up approach described above. This aligns closely with the OECD Transfer Pricing Guidelines and is consistent with the prevailing practices in most jurisdictions.

In contrast, the administrative principles issued in Germany appear to take a different direction. According to the new rules, the arm’s-length nature of the interest rate for cross-border intercompany financing arrangements must generally be determined based on the group’s credit rating and external financing conditions. However, taxpayers are allowed to demonstrate that an alternative rating better aligns with the arm’s-length principle.

This new approach diverges not only from the OECD guidelines but also from previous case law established by the German Federal Tax Court. As a result, several questions arise regarding how these rules will be applied in practice by German tax authorities. For instance, it remains unclear whether this approach will constitute a strict obligation or whether flexibility will be granted. Additionally, concerns exist about the burden of proof placed on taxpayers when opting for the bottom-up approach recommended by the OECD Transfer Pricing Guidelines.

Cash Pool Synergy Distribution

Tax authorities are increasingly aligning with Chapter X of the OECD Guidelines when evaluating cash pooling arrangements, with particular attention to the distribution of synergies among pool participants.

According to the OECD Transfer Pricing Guidelines (Section C.2.3.2, paragraph 10.143), synergy benefits should generally be allocated to pool members by determining arm’s length interest rates that reflect each participant’s contributions and positions within the pool (e.g., debit or credit).

Historically, the focus of tax authorities was primarily on the pricing methodologies— ensuring that both deposit and withdrawal margins were set at arm’s length. However, there is now a growing emphasis on how synergy benefits are distributed among participants. This is especially significant in jurisdictions where participants make substantial contributions to the pool balance. According to the OECD guidelines, these participants should benefit from the synergies generated by the pool through more favourable financing terms.

To address these requirements and reduce the risk of disputes over cash pool structures, a three-step approach is recommended:

1- Price the credit and debit positions of the participants.

2- Calculate the synergy benefits generated within the structure.

3- Allocate these benefits between the Cash Pool Leader and participants by adjusting the price applied to the participants.

By following this approach, multinationals can ensure compliance with OECD guidelines and mitigate the likelihood of challenges from tax authorities.

Zanders Transfer Pricing Solution

As tax authorities intensify their scrutiny, it is essential for companies to carefully adhere to the recommendations outlined above.

Does this mean additional time and resources are required? Not necessarily.

Technology provides an opportunity to minimize compliance risks while freeing up valuable time and resources. The Zanders Transfer Pricing Suite is an innovative, cloud-based solution designed to automate the transfer pricing compliance of financial transactions.

With over seven years of experience and trusted by more than 80 multinational corporations, our platform is the market-leading solution for intra-group loans, guarantees, and cash pool transactions.

Our clients trust us because we provide:

- Transparent and high-quality embedded intercompany rating models.

- A pricing model based on an automated search for comparable transactions.

- Automatically generated, 40-page OECD-compliant Transfer Pricing reports.

- Debt capacity analyses to support the quantum of debt.

- Legal documentation aligned with the Transfer Pricing analysis.

- Benchmark rates, sovereign spreads, and bond data included in the subscription.

- Expert support from our Transfer Pricing specialists.

- Quick and easy onboarding—completed within a day!

Discover how neural networks are revolutionizing XVA calculations, delivering unprecedented speed, efficiency, and agility for the banking industry.

Introduction: Faster, smarter, and future-proof

In the fast-paced financial industry , speed and accuracy are paramount. Banks are tasked with the complex calculation of XVAs (‘X-Value Adjustments’) on a daily basis, which often involve computationally expensive Monte Carlo simulations. These calculations, while crucial, can become a bottleneck, slowing down decision-making processes and affecting efficiency. What if there is a faster and smarter way to handle these calculations? In this article, we explore a revolutionary approach that uses neural networks to drastically accelerate XVA calculations, promising significant speed-ups without sacrificing accuracy.

The traditional approach: Monte Carlo simulations and their limitations

Traditionally, banks have relied on Monte Carlo simulations to calculate XVAs. These simulations involve numerous complex scenarios, requiring substantial computational power and time. Imagine running simulations endlessly, with every tick of the clock translating to computing expenses. The problem? Time and resources. These calculations must be repeated daily, leading to significant delays and costs, potentially hindering your bank's responsiveness and decision-making agility.

Despite bringing precision, this traditional method poses challenges. Given that the rates offered by banks do not fluctuate dramatically within days, repeating these extensive simulations seems redundant. This redundancy leads us to seek a solution that can deliver both speed and efficiency, paving the way for innovation.

A new era: Leveraging Neural Networks for speed and efficiency

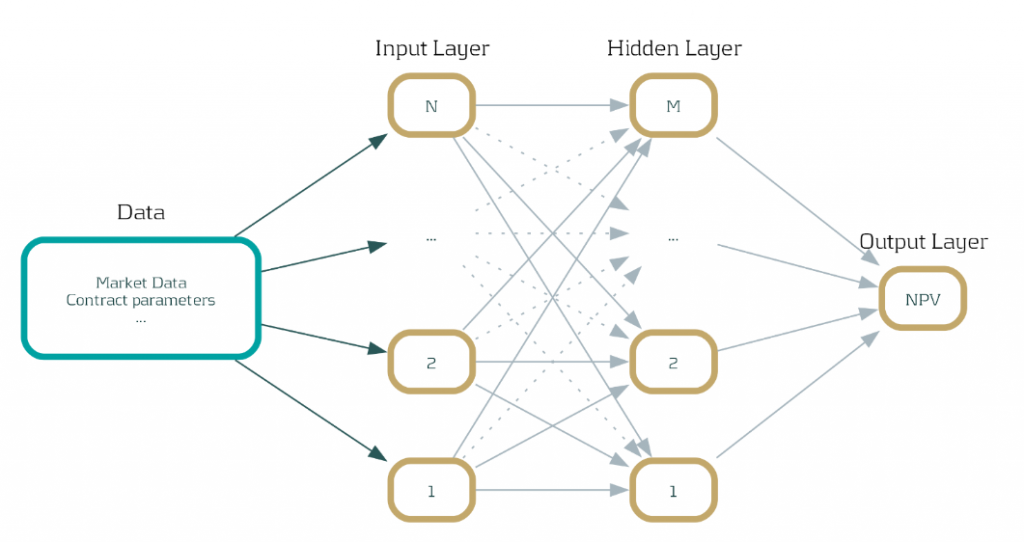

Enter neural networks—an innovative technology that promises a solution to the Monte Carlo conundrum. By training these networks on Monte Carlo simulations conducted early in the week, such as on a Monday, the model can predict outcomes for the rest of the days. This approach sidesteps the need to perform cumbersome computations daily.

Here’s how it works: The neural network learns from initial data, absorbing patterns and information that remain relatively constant through the week. This enables it to approximate net present value calculations with astonishing speed and accuracy. A practical example? Our integration of this technique into the Open-source Risk Engine resulted in a remarkable 600% increase in speed when assessing interest rate swap exposure in a stable market.

Benefits of our solution: Integration and acceleration

- Seamless Integration: Our solution can be seamlessly integrated with any existing systems, as long as they provide net present value outputs for some simulations.

- Scalability with GPUs: Neural network calculations can harness the parallel processing power of GPUs, exponentially increasing inference speed. Imagine every inference equating to calculations for numerous trades simultaneously.

- Feasibility and Reliability: With approximation of net present values being a commonly accepted practice in finance, this approach is both feasible and reliable for banks striving for rapid insights.

Zanders Recommends: A strategic approach to implementation

At Zanders, we believe in empowering banks with cutting-edge technology that aligns with their growth ambitions. Here is what we recommend:

1- Assessment Phase: Evaluate the current computational model and identify areas that can benefit from the implementation of neural networks.

2- Pilot Programs: Start with small-scale implementations to address specific bottlenecks and measure impact.

3- Utilize GPUs: Leverage the parallelization capabilities of GPUs not just for neural networks but also for Monte Carlo simulations themselves, if needed.

4- Continuous Improvement: Regularly update neural network models to ensure accuracy as market conditions evolve.

Our extensive experience with high-performance computing, particularly the use of GPUs for parallelization, positions us as a trusted partner for banks navigating this transformation journey.

Expertise spotlight: High-Performance Computing and AI solutions

In addition to revolutionizing XVA calculations, Zanders offers robust high-performance computing solutions that maximize the capabilities of GPUs across various applications, including Monte Carlo simulations. Our expertise also extends into AI technologies such as chatbots, where we implement and validate models, ensuring banks remain at the forefront of innovation.

Conclusion: Embrace the future of banking technology

As the financial world evolves, so must the technologies that drive it. By leveraging neural networks, banks can achieve unprecedented speed and efficiency in XVA calculations, providing them with the agility needed to navigate today's dynamic markets. Now is the time to embrace a solution that is not only faster but smarter. At Zanders, we're ready to guide you through this transformation. Get in touch with Steven van Haren to learn how we can elevate your XVA calculations and ensure your bank stays competitive in an ever-changing financial landscape.