Are you overwhelmed by the sheer volume of different Treasury Technology Systems on the market?

Do you have difficulties setting out your treasury technology requirements (both from a functional as well as IT perspective), or matching those to the latest capabilities of a modern Treasury Systems? Are you wishing for a technology selection process that is less cumbersome and time consuming? If you said ‘yes’ to any of these, then we might have the solution for you!

Introducing Zanders’ Treasury Technology Selection Service powered by Tech-Select, our proprietary cloud-based Treasury Technology Selection tool designed to give you an easier, quicker way to select a new treasury system that best supportis your specific needs, or to evaluate your current system against other alternatives. For over 30 years, Zanders has been helping organizations globally to select treasury management systems and other related treasury technology. As an independent and unbiased expert, we have built extensive experience into how best to assist our clients to select, implement and deploy the most appropriate solution for their technology needs – it is this insight that drove us to develop a system to modernize the commonly used RfP process.

Zanders Tech-Select is the driving force behind our Treasury Technology Selection Service and accelerates your treasury system selection project by addressing the traditional challenges faced by organizations when choosing treasury technology solutions and introduces several other benefits as follows:

- Provides a broad overview of the systems market, giving you access to a wider range of potential vendors that can provide systems supporting your needs, and the most up-to-date insights on their current capabilities and new product developments

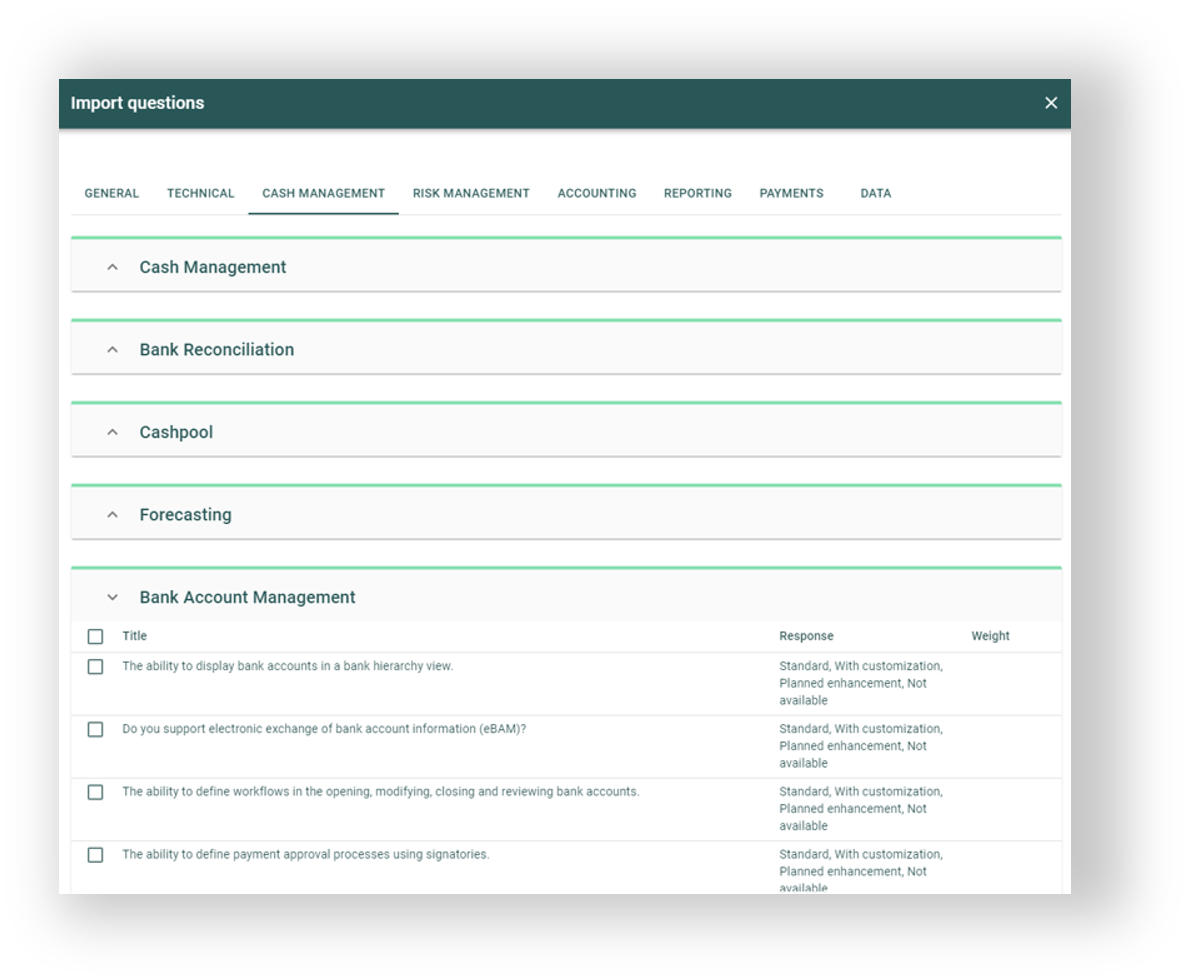

- Allows you to easily identify and define your functional needs, short-list suitable vendors, and automatically create and issue your RfP, by providing access to our comprehensive library of functional and technical requirements alongside our curated database of vendors, system functionality and capabilities

- Facilitates and accelerates multi-user assessment and evaluation of vendor responses, by utilizing workflows for scoring, the ability to assess user scoring differences, and the opportunity to determine final scores for each vendor

- Helps you to understand key differentiators between services and functionality on offer from each vendor, using our pre-defined results analytics and drilldowns

- Helps to streamline and accelerate the RfP process from end-to-end within a single cloud-based platform, removing the need for multiple emails, spreadsheets or complex scoring models, and

- Reduces the resource and time investment required to engage with multiple vendors, freeing you to focus on key analysis and value-add activities

Let’s take a deeper look at how Zanders Tech-Select achieves this:

- Once you’ve chosen from Zanders Tech-Select’s comprehensive library of functional and technical requirements, these are matched to our curated database of system functionality and capabilities in order to present you with a shortlist of systems and vendors that are suited to your specific needs. You can then select which of those vendors you would like to invite for your RfP process, utilise our templates to create cover letters and other attachments, and specify deadlines for acknowledgement, Q&As and final responses.

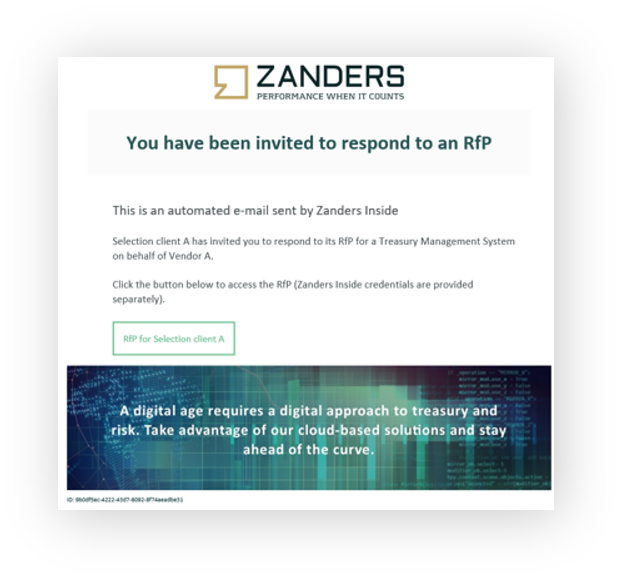

- When you are ready to launch your RfP, you simply click the ‘Issue’ button to automatically generate RfP invite emails quickly and easily to all chosen vendors. Once they receive the invite, vendors can use Zanders Tech-Select to access all document attachments, view your requirements, ask any questions, and respond to the RfP.

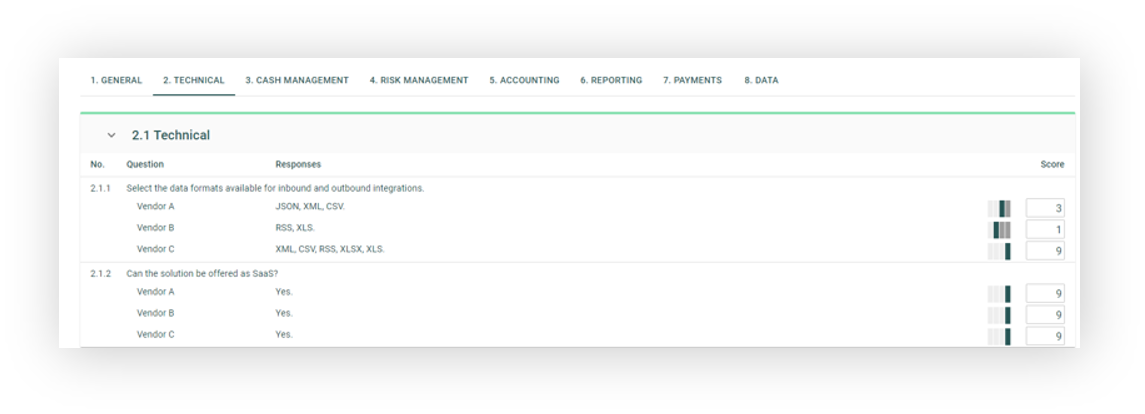

- Once vendors have completed submitting their RfP responses, multiple users from your treasury, finance, IT and procurement teams can use Zanders Tech-Select to independently compare each vendor’s responses to each requirement in a consolidated view, and can assign scores to each. When all users have completed their scoring, the system automatically consolidates their scores and provides you with the opportunity to review and moderate the final scores before moving forwards to analyze the results.

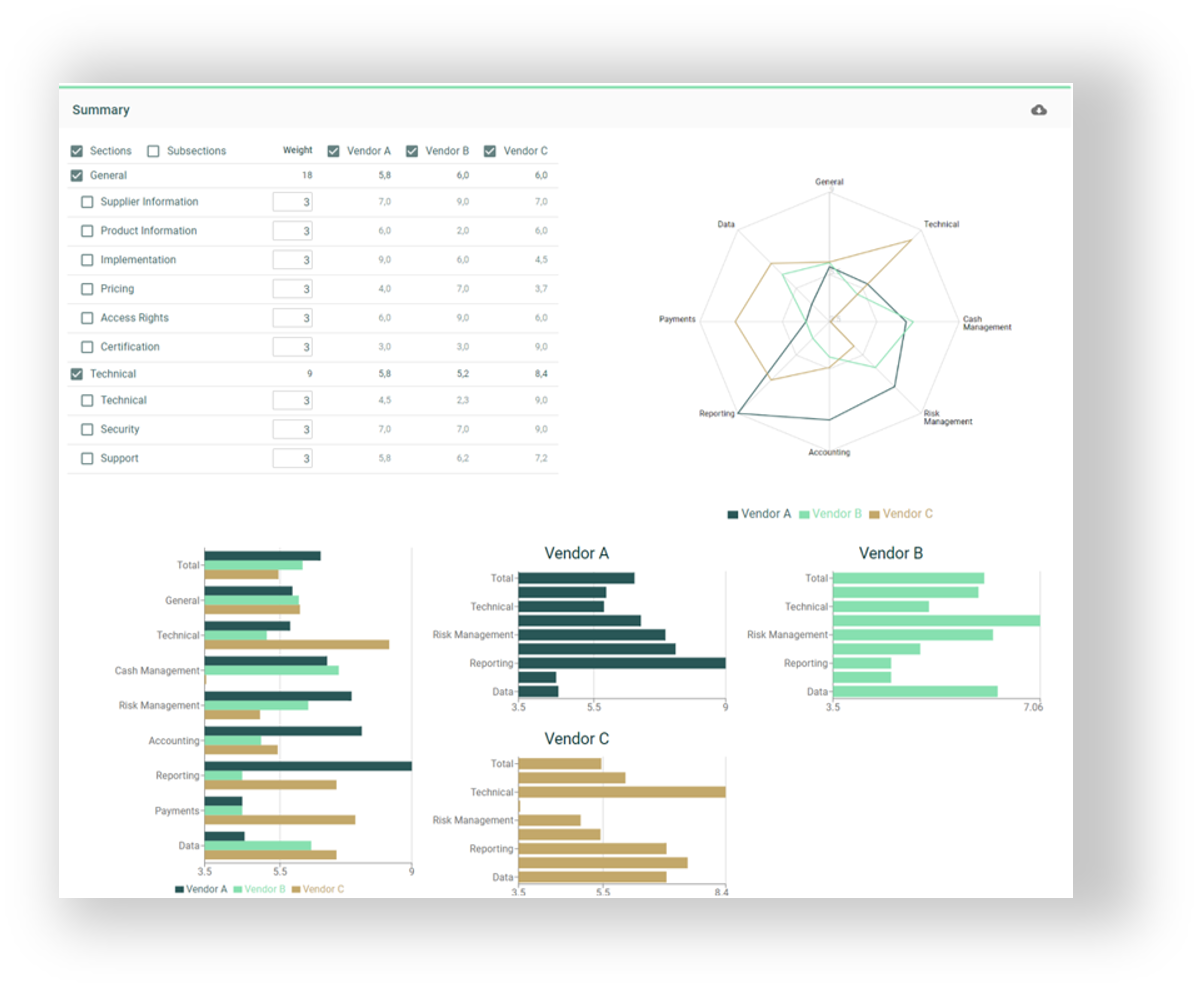

- At the final stage, Zanders Tech-Select’s interactive results analytics provide you with several ways to view and drill down into your results. Simply hover over data points to see more detailed information, check or uncheck to include or exclude vendors, sections and subsections, or most importantly click on specific scores to drilldown and quickly understand the reasons behind any scoring differences between vendors.

Based on experience from our clients, Zanders’ Treasury Technology Selection Service powered by Tech-Select drastically improves the current RfP processes many corporates are using today.

Zanders is unique in offering a system selection solution that includes an extensive library of the most common technology requirements alongside pre-populated and curated responses from over 90% of the leading treasury systems currently on the market. The structured, end-to-end process helps to streamline and automate your selection project and is applicable to a wide variety of use cases, enabling a consistent approach to vendor selection based on objective and rigorous evaluation.

Zanders Tech-Select uniquely provides the most efficient, thorough and cost-effective digital selection service within the treasury space, with Zanders experts to guide you throughout. If you would like to find out more about how Zanders can help to streamline your next technology or service selection process, get in touch now.

Article updated in May 2024

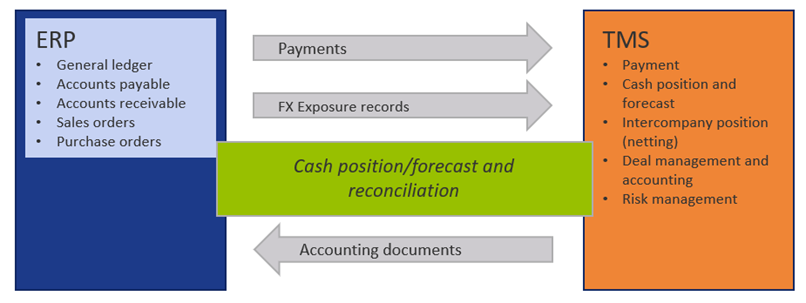

The recent decade has brought notable developments in both ERP and treasury management system (TMS) markets.

On one hand, the trend towards ERP system consolidation has progressed, most companies have centralized all their global entities and processes in a single environment with unique master data. At the same time, the trend towards cloud solutions has brought innovation and increased competition also to the TMS area. In this context, we are often asked: should the treasury function follow into the centralized ERP solution as well, or does a separate TMS instance have its justification?

Nowadays, all established TMS solutions are also available in the cloud or have disappeared from the market. The cloud technology brings disruption to the TMS market – high scalability of the cloud solutions has brought a number of new players to the global market – originally regional leaders seek to expand their footprint in other regions, some of them challenging the traditional market leaders. Established cloud TMS providers expand their functional covering in a very high pace and at relatively low marginal costs, which leads to increased competition in both functional capabilities and pricing.

In the segment of companies with more than USD 1 billion revenue, SAP occupies a special position among both ERP and TMS vendors (see numbers here) – it offers both a leading ERP system and a TMS with very broad functional coverage.

Benefit areas

In what areas can you find the benefits from integrating the TMS into ERP? We list them for you.

- Process integration

Treasury is usually involved closely in the following three cross-functional processes, with the following implications:

(a) Cash management

Short- and mid-term cash forecast reflects accounts payable and accounts receivable, but purchase and sales orders can also be used to enrich the report. Even when commercial accounts are cash-pooled to treasury accounts, expected movements on these accounts can be used to plan cash pool movements on treasury accounts.

(b) Payments

Various levels of integration can be found among the companies. While some leave execution of commercial payments locally, others implement payments factories to warehouse all types of payments centrally. Screening against payment frauds and sanction breach is facilitated with centralized payment flow. Centralized, well-maintained bank master used at payment origination helps to avoid the risk of declined payments.

(c) Exposure hedging

FX and commodity hedging activities are usually centralized with the treasury team.

In case FX or commodity exposure arises from individual purchase and sales orders or contracts, the treasury team needs tools to be directly involved in the exposure identification and hedge effectiveness controlling.

- System integration

Streamlined processes described above have implications for the required system integration. Depending on frequency and criticality of the data flows, different integration approaches can be considered.

All TMS on the market support file integration with the ERP systems in a reasonable way. They are also often very strong in supporting API integration with trading platforms and bank connectivity providers, but usually lag behind in API integration with the ERPs. Claims of available API integration need to be always critically reviewed on their maturity. API integration is preferred.

What are the benefits of API-based integration?

- It offers real-time process integration between the systems and empowers treasury to be tightly integrated in the cross-functional processes. It can be important when intraday cash positions are followed, payments are executed daily or exposure needs to be hedged continuously.

- It keeps the data flow responsibility with the users. Interfaces often fail because of master data are not aligned between the participating systems. If message cannot be delivered because of this reason, user receives the error message immediately and can initiate corrective actions. On the other hand, file-based interfaces are usually monitored by IT and errors resolution needs to be coordinated with multiple parties, requiring more effort and time.

Figure 1 Usual data flow between ERP and TMS

- Parallel maintenance of master data

Integration flows require harmonization decisions in the area of master data. Financial master data (G/L accounts, cost centers, cost elements) are involved as well as bank master data and payment beneficiaries (vendors). TMS systems rarely offer an interface to automatically synchronize the master data with the ERP system – dual manual maintenance is assumed. Using one of the systems as leading system for the respective master data (e.g. bank masters) is usually not an available option.

- Redundant capabilities

Both the ERP and TMS systems need to cover certain functionalities for different purpose. ERP to support payments and cash management in purchase-to-pay and order-to-cash, while TMS supports the same in treasury process. Both systems need to cover creation of payment formats, reconciliation of electronic bank statement, update of cash position for their area. These functionalities need to be maintained in parallel, or specific solution defined, to avoid the redundancy.

Conclusion

So, should the treasury function follow into the centralized ERP solution as well, or does a separate TMS instance have its justification? The answer to this question depends strongly on your business model and the degree of functional centralization. If functional centralization and streamlined business operations across your global entities is important in your business, you are probably already very advanced in ERP centralization as well. You can expect benefits from integrating the treasury function into such system setup.

On the other hand, if the above does not apply, you may benefit from the rich choice of various TMS solutions available at competitive prices to fit your specific needs.

Every business runs differently. We are happy to support you in your specific situation.

Rapid advancements in technology and globalization often require cutting- edge payment solutions for corporates with a diverse footprint, but be sure to bake in anti-fraud measures.

Payment fraud originating from within or outside an organization must be guarded against. Read on to learn how SAP Advanced Payment Management (APM) and Business Integrity Screening (BIS) can help.

Compliance requirements, audit needs and external factors like embargos, sanctions imposed by governments, and so on are additional imperatives for corporates and financial institutions (FIs) that want to secure their end-to-end payment lifecycle. Protection must be provided from the time of triggering a payment – or even before – until payment reaches the intended recipient.

In an increasingly digitized world with multiple cybersecurity threats, it is becoming even more important that the payment process is robust and ably supported by a strong technology infrastructure that provides security, speed, and efficiency.

Challenge for Corporates

The reality for many corporates is that they have multiple enterprise resource planning (ERP) systems – SAP or from other vendors – implemented over a period of time, or they have multiple systems due to merger and acquisition (M&A) activity in the past. Such corporates end up having lots of multi-banking relationships with different processes across the entire company, and different systems or banking portals for making payments. In an ideal world, moving to a single system with focused banking relationships, centralized treasury management and harmonized global processes is the end game that every company wants to achieve. But the process to get there is long.

SAP S/4 HANA

Companies using, or moving, to SAP as their primary ERP often aim for a single instance of the S/4 HANA landscape to get a single version of truth, but they may approach it in different ways. The journey most often is long and complex. But payment risk has to be mitigated sooner, rather than later.

Companies can adopt different strategies like ‘Central Finance’, ‘Treasury First’ or centralization of payments through a Payment Factory (PF) solution to enable certain quicker wins and security for the treasury and finance organization.

Advanced Payment Management Functionality

SAP introduced APM in 2019 to help payment centralization, visibility and oversight for those using its systems. APM alongside In-House Bank is its payment factory solution. SAP has continuously upgraded it since, with appropriate functionalities including anti-fraud measures available to users now.

APM allows for centralization of payments originating from any system – be it SAP or non-SAP – and facilitates:

- Data enrichment,

- Data validations,

- Conversions to bank specific file formats where needed,

- Batching, along with adding an approval mechanism by integrating with SAP’s Bank

- Communication Management option and by using a secured single channel of communication to all banks like SAP’s Multi-Bank Connectivity.

These measures enable treasury to have central and near-real time visibility of all payments going out, allowing corporate treasurers to put controls and checks in place through a robust payment approval mechanism.

Having a strong and auditable payment approval process governed by a unified system will enable reductions in payment fraud. However, payment approval alone is somewhat of a reactive mechanism and relies on a human touch that can sometimes become time consuming, labor-intensive and prone to errors, which can potentially miss some transactions when done on a large scale. A more advanced way of managing payment risk efficiently is through an exception-based procedure, where only absolutely required payments go through a human touch, with low-risk transactions filtered through an automated rules engine that allows for targeted attention on high-risk payments.

The need for Business Integrity Screening

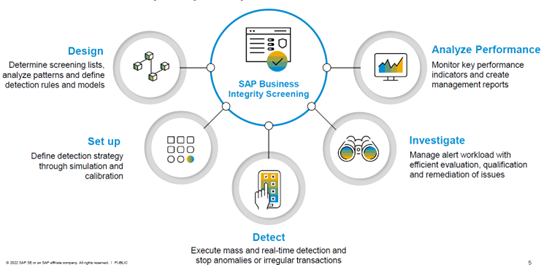

SAP Business Integrity Screening (BIS) is a solution that complements the payment engine of S/4 HANA, including the advanced payment management (APM) function. BIS is a SAP solution that can be enabled on S/4 HANA. At a high level, it is a rules-based engine designed to detect anomalies and third-party risk. It uses data to predict and prevent future occurrences of fraud risk.

By virtue of being on S/4 HANA, BIS handles large volumes of payments, processing through real-time simulations. SAP BIS also integrates with different process areas like master data management, invoice processing, payment execution (payment runs), and with APM for payments originating from other systems. This helps fraud prevention at a much earlier stage.

The below Figure 1 picture depicts a few of the features of BIS where a set of rules can be defined for different scenarios with certain SAP provided out-of-box rules – for example, identified risk factors might include:

- Supplier invoice and payment execution stages, like vendor invoices or banks accounts in high-risk countries,

- One-time vendors,

- Payments made too early,

- Changes to vendor banking details just before a payment cycle,

- Duplicate invoices,

- Manual payments, and so on.

Figure 1: SAP’s Business Integrity Screening (BIS) Key Features

Source: SAP.

BIS has a highly flexible detection and screening strategy for business partners where new rules can be added and it can make composite rule scenarios, resulting in an overall risk score being awarded. For example, a weighted score may be determined based on individual Rules like:

- Payment value banding.

- Consecutive payments to the same beneficiary.

- Beneficiary address in an ‘at risk’ country.

Using the power of S/4 HANA, every payment is processed through all the rules and strategies defined to detect anomalies as early as possible, with real-time alert mechanisms providing further security. Implementations can leverage out-of-the-box rules and create new rules based on internal knowledge to refine anti-fraud measures going forward. BIS also has powerful analytics through the SAP Analytics Cloud solution for evaluating the performance of each strategy and rule, enabling refinements to be made.

BIS & APM Integration

For customers operating a single system environment, BIS was previously integrated with Payment Run functionality. With a multi-ERP Payment Factory landscape, BIS now integrates directly with APM. This means payments across the enterprise can be routed through screening for exception-based handling.

BIS combined with APM has two possibilities (as of writing this article):

- online screening for individual items,

- or batch screening for larger volumes of payments.

Rules can be set based on the size of payments as well – for example, Low value payments can be set for batch screening, while high value transactions can be set for online screening.

In the current release BIS 1.5 (FPS00), there are pre-defined scenarios specifically for APM. These check recipient bank accounts – for example, in high-risk countries and so on – and business partner (payee) bona fides for sanction screening/embargo checks at the payment order/payment item level. Custom scenarios can be created, and further custom code enhancements built within SAP-provided enhancement points.

While screening online, APM payment orders are validated through BIS detection rules. Payments without any anomalies or risk scores below threshold are automatically approved and processed for further normal processing through APM outbound processing. Payments which are suspicious will be ‘parked’ in BIS for user intervention to either release the payment – remembering, it could be a false positive scenario – or for blocking.

Any blocked payment in BIS automatically moves the APM payment order to the Exception Handling queue within Advanced Payment Management for further processing – for example, taking corrective actions in source systems, validating internal processes, contacting the vendor, cancelling/reversing a payment, and so on.

End-to-End Payment Fraud Prevention

There are different solutions available to cater to the specific needs of corporates across the payment lifecycle. A key first step is to centralize payments where Advanced Payment Management can help. A key benefit of Payment Centralization in a corporate landscape is the opportunity to initiate centralized payment screening and fraud prevention using BIS.

The integration between BIS and the APM Payment Factory enables effective payment fraud and sanction screening detection across the whole payment landscape. Adding Bank Communication Management for further approval control on an exceptions-basis will ensure a robust and automated payment process mechanism, with a strong focus on automated payment fraud prevention.

Once the payment process is secured, the next step is having secure connectivity to banks. This is where solutions like the SAP Multi-Bank Connectivity option can help.

If you are interested in any of the topics mentioned, or Sanction Screening & Fraud Detection more generally, we at Zanders encourage you to reach out to us via the ‘Get In Touch’ button. You can read more about Bank Connectivity Solutions & Advanced Payment Management: APM in our earlier articles.

Setting up a complete stand-alone treasury function from scratch is one of the most comprehensive activities for any Treasurer.

Having to do this as part of a transaction where part of an existing business is being sold adds a major challenging element: time.

Time pressure together with the uncertainty of who will be the ultimate buyer (Financial Investor vs. Strategic Investor with an existing treasury function) requires many key decisions to be made under uncertainty. One of these key decisions is the one about the Treasury Management System (TMS) and the corresponding functionalities that have to be available on the closing day of the transaction. This decision has two components: costs and time to go-live.

Considerations

Technical developments in recent years have led to a situation where basic functionalities can be provided in-time by deploying a standard TMS at a cost not higher than any individual spreadsheet-based solution provided by consultants. Therefore, it has become a standard that an integrated TMS is a must-have for Day-1. It provides cash visibility and forecasting, captures both internal and external financial transactions and valuates them for period-end closing, therefore a TMS is the main Treasury Enabler.

With the time remaining until closing usually being quite short (often not more than 3-6 months) the question regarding the long-term strategic fit however has been one of minor relevance. This was and still is the case when the ERP-System is SAP-based. Until now, SAP treasury and risk management and cash and liquidity management components have not been part of the shortlist for transaction related TMS requirements. Three major (valid) arguments have been the reason for this:

- Cost,

- Complexity and therefore the longer duration time for an SAP implementation

- & Usability, especially by treasury staff that are not necessarily familiar with SAP logic.

But every major technical development requires us to question existing narratives and ask whether certain arguments are still valid.

Making the Right Strategic Choice

Usually, SAP has been dropped from the discussion when an implementation time constraint of between 3-6 months exists. The same applies if the future ERP landscape hasn’t been decided upon. This uncertainty often leads to the decision to opt against SAP. Let’s start with this element. A feasible solution to overcome this uncertainty is that of a Treasury Sidecar, i.e., implement a separate SAP instance with the SAP Treasury components. This allows connection to the existing (SAP) landscape, as well as providing the option of a future migration into a single S/4HANA environment and mapping treasury to the new General Ledger. This means that there should be no strategic or technical reason not to consider SAP.

We also looked at the latest SAP Treasury developments regarding the cloud-based SAP S/4HANA Treasury components from a time perspective. We specifically looked at the Private and Public Cloud Solutions from two angles: What is the minimum implementation time considering that SAP Best Practices are applied and secondly what are the consequences when looking at the integration into either an existing SAP ERP Central Component (SAP ECC) environment or a future S/4HANA platform? What our evaluation revealed is quite astonishing.

Public or Private Cloud?

When looking at the tight timeline argument against SAP we should examine the two main alternatives: the public cloud solution and the private cloud alternative. The private cloud can be considered similar to an on-premise installation, with the main difference being that the private cloud solution can be hosted by SAP or built within in your own data center. A private cloud could also use one of the Infrastructure-as-a-Service (IaaS) providers, such as AWS, Azure, GCP, or Alibaba Cloud.

These alternatives have the advantage of a fixed timeline (3-6 Months) for their implementation based on SAP’s Best Practices approach, together with SAP’s Activate. A requirements gathering is still the starting point to call out what is included in the first phase during its 3 months of implementation. This phase delivers a comfortable solution based on an 80/20 approach and covers what is usually required on Day-1.

Pros & Cons of the Cloud Options

A typical question is: what can’t we do if we opt for either the public or the private cloud? The answer is quite simple: The public cloud is a common environment with restrictions on building what is not already there – i.e. a gap identified is a real gap (and remains so). The private cloud is much like an on-premise solution with certain variations – like the SAP hosted option – where additional restrictions apply in terms of how far you can go about extending functionality.

Building a treasury side car and applying SAP Best Practice and the SAP Activate methodology, and following them closely, leads to similar implementation times for both public and private cloud (or on-premise) options, given that the same functionalities are to be implemented. This means, that implementation duration is not a major decision point. This leaves one key decision element: the question is, what type of flexibility & functional requirements – beyond what’s available in the public cloud solution – are required in the future?

The answer to this may lead to adopting an implementation approach very much like public cloud but in a private cloud (or on-premise) environment in order to get the flexibility needed to extend and expand for the future.

So yes, there is a new kid on the block, and it has to be taken seriously.

The SAP Activate approach and Best Practices for SAP S/4HANA can help organizations deliver a fast, simplified adoption of SAP treasury functionality within S/4HANA.

Greg Williams, senior manager at Zanders, tells us what this is, how it can accelerate implementations, and informs us about new developments in 2023.

In previous articles we covered a perspective on the different types of deployment options available for SAP S/4HANA – i.e. On-Premise, Public Cloud and Private Cloud. In this article we look to provide insight into how to leverage SAP’s Activate implementation methodology and Best Practice content to accelerate your adoption of SAP’s S/4HANA treasury capability.

Previously, SAP had what they used to call ‘rapid deployment solutions’ (RDS) and content to aid implementation. But the replacement SAP Activate approach is a far more complete way to build and deploy systems. It has also evolved and matured over the years, since the first release in 2015, so it is important to keep up-to-date. The offering is now supported by very rich and mature Best Practice content that includes detailed business process documentation and test scripts.

Implementation Methodology

SAP Activate is an agile methodology that leverages the various accelerators mentioned above. In reality, most implementations will not necessarily adopt the full methodology completely, only taking what is relevant to them. However many aspects of it should be leveraged in formulating some type of hybrid agile / waterfall methodology for a treasuries implementation project – based on all of the complex real-world factors that any given organization has to accommodate.

In this article we will provide some insight into the SAP Activate elements and methodology and then look at it from a treasury perspective, examining the treasury specific scope items included in SAP’s Best Practices run-through. We will drill down into the specific detail so that you get a feel for both the breadth and depth of what SAP has to offer.

This will be like a visual tour from the highest level, with lots of graphs to come, through to the lowest level of detail. The key thing to remember is that the Best Practices content and SAP Activate methodology is applicable to the full array of system functionality and herein lies the benefit in that all parts of the business embrace this same content and approach.

SAP Activate

First let’s have a brief look into SAP Activate. Starting with the elements that are included and then looking at the phases in the project lifecycle, which will give greater insight into the methodology. The elements are:

- the methodology,

- tools, which are very much supported by SAP’s Solution Manager,

- & then the content, including for example the Best Practices advice, which we will unpack a bit later.

The elements provide the project team with ready-to-use templates and accelerators, which can be used in the entire Activate journey with the help of step-by-step guidelines. We will cover what needs to be delivered in each phase and how to deploy the solution in Cloud/On-premise, according to the business needs.

Figure 1: SAP Activate elements.

Source: SAP

In SAP Activate, there are six phases. At the end of each phase, quality gates are present to make sure respective deliverables in each phase are completed, as per the standards.

This methodology is an agile framework and hence all these phases are run in an iterative manner in order to build a solution. The six phases are: Discover, Prepare, Explore, Realize, Deploy and Run.

Figure 2: SAP Activate phases.

Source: SAP.

SAP Best Practices Content

The SAP Best Practice content is currently accessed through the SAP Best Practices explorer. This application is planned to be discontinued by end of June 2023, whilst it will not be replaced SAP will provide an entirely different application that will also cover SAP Best Practices solutions. The first release of the new application is planned prior to the end of June 2023.

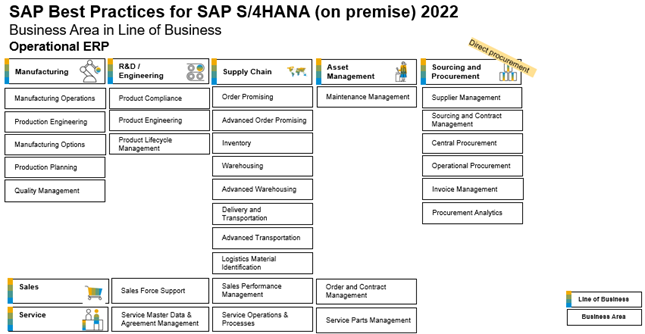

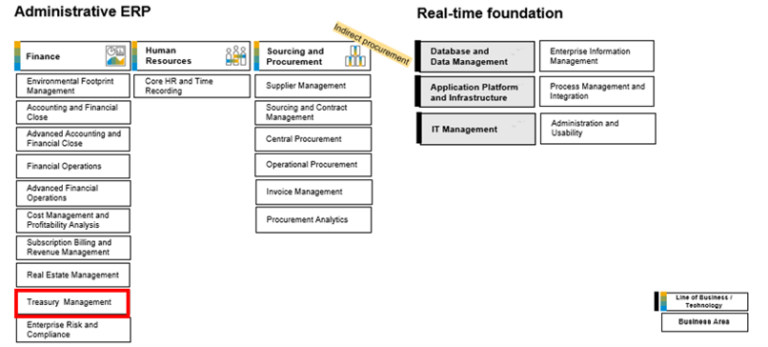

Turning to the SAP Best Practices advisory content next, there are two diagrams below that show all the lines of business and business areas included in Best Practices approach for SAP S/4HANA. These diagrams are logically split between what the vendor calls Operational ERP and Administrative ERP. Treasury Management forms part of the Finance subset under the Administrative ERP side.

Figure 3: SAP Best Practices – Operational & Administrative ERP.

Source: SAP.

Here you can view the diagram (Figure 4: Treasury Management’s position in SAP’s Best Practices implementation methodology. (Source: SAP)). that shows the full set of Treasury Management scope items included in the coverage. From here we will then select a specific scope item to demonstrate some of the detail that is included for every scope item.

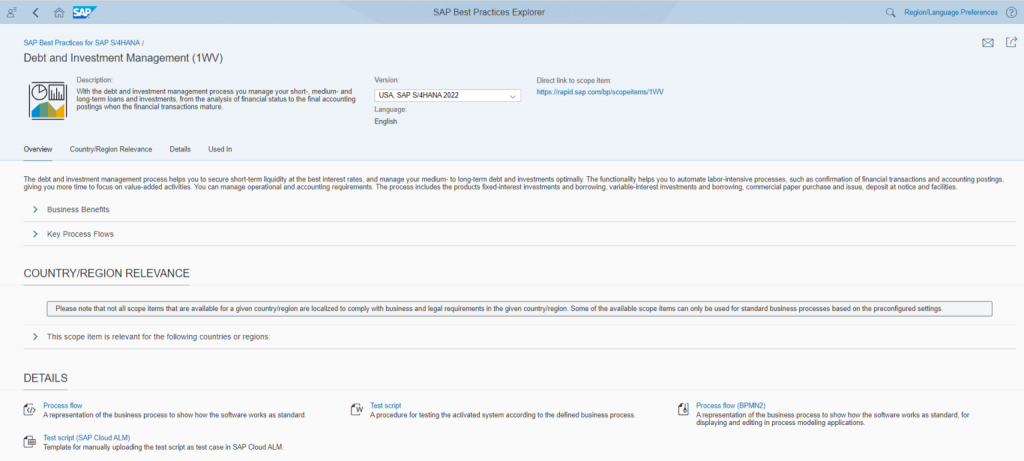

Treasury Management Scope Items, are important aspects of SAP’s Best Practices implementation methodology. We will now focus Debt and Investment Management, diving into the details. Scope Item 1WV (Debt and Investment Management) is shown on the Best Practice Explorer module below, Including Process Flows and Test Scripts.

Figure 5: An example of a scope item – for debt & investment management – in SAP’s Best Practices content.

Source: SAP.

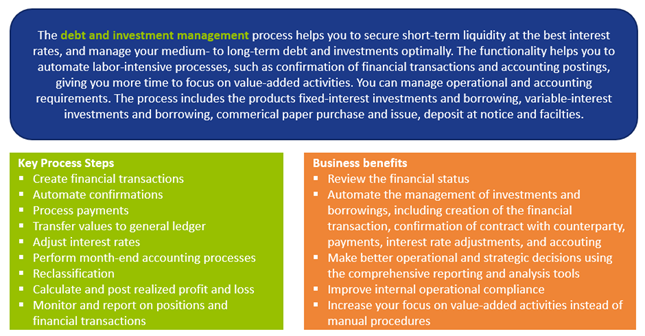

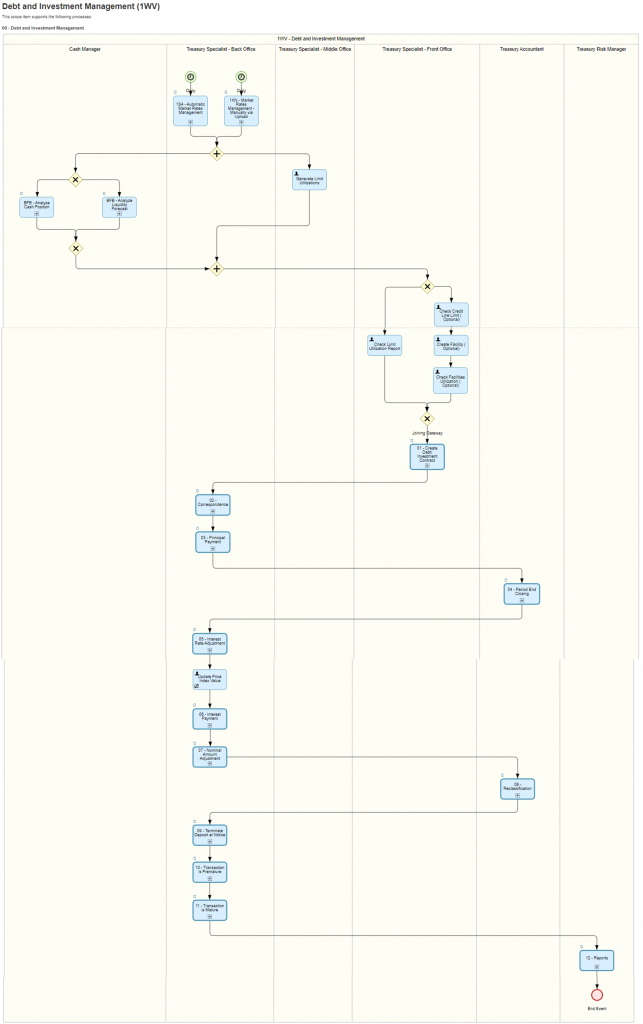

There are 13 Process flow diagrams for scope item 1WV – Debt and Investment – alone in SAP Best Practices. A view of the debt and investment management overview process flow diagram is provided in figure 7. The process steps in the Debt and Investment Overview include: (1) Create Debt and Investment Contract; (2) Correspondence; (3) Principal Payment; (4) Period End Closing; (5) Interest Rate Adjustment; (6) Interest Payment; (7) Nominal Amount Adjustment; (8) Reclassification; (9) Terminate Deposit at Notice; (10) Transaction is Premature; (11) Transaction is Mature; (12) Reports. Scope Item 1WV also has a 188-page word based test script document. Additionally, a test script template for Cloud Asset and Liability Management (ALM) risk purposes is also included in the same content.

A view of the debt and investment management overview process flow diagram is provided below:

Figure 6: Debt & investment management process flow.

Source: SAP.

Conclusions: Solution Builder

When you embark on the initial phases of your treasury implementation you can also use the SAP Solution Builder to deploy the Best Practice content into a working sandbox test system.

You need to select the scope items for inclusion in the solution build option. It will then build the system, including configuration and master data, such that you will be able to follow the test scripts, and run the business processes. This means you can quickly and easily explore the system according to the documented functionality very early on in your project.

A good approach is to keep a dedicated Best Practices sandbox client in your development environment where you can deploy and explore content at the start of your project, and also use it for future initiatives.

It is clear that you should be able to leverage significantly faster implementation times and to get value quickly, using as much of this vendor provided advisory content as possible. In addition, it is going to be crucial to have a consistent approach for all lines of business and business areas within the project. All areas need to embrace what is on offer in a universal manner, so that the benefit of a more unified approach to your transformation journey can be fully realized. As ever, good project management and perhaps consultancy advice if it is deemed necessary, can improve any implementation template so bear in mind some thought power will still be needed by the project management team.

At Zanders we are striving to embrace the new approach to SAP S/4HANA implementations discussed in this article, while still drawing on the depth of experience and knowledge we’ve built up from both a treasury business and technology perspective over the years on more traditional approaches we’ve used in the past. This can and should be seen as a healthy tension – comparing what has worked previously with what is possible now to find the best pathway forward. This synthesis allows for the benefits of both schools of thought to be leveraged when guiding our customers through their treasury transformation journeys on SAP.

It is without a grain of doubt that cash positioning is at the forefront of successful cash & liquidity management.

There are various sources from which treasurers obtain information that forms accurate cash position within the company’s ERP or Treasury Management System. The most important of these sources is the current available balance, most often obtained from bank statements which are reported by various banks through numerous protocols.

Depending on the system an enterprise is using, the cash position can be updated in two main ways; directly from the balance which has been reported on the bank statement by the bank, or through making appropriate accounting postings of bank statement items to relevant GL accounts. For a long time, in SAP only the latter was possible. The very least that needed to happen was the posting in so-called posting area 1, whereby the bank statements were posted to the Bank GL Balance Sheet account, with opposing entry posted to the Bank GL Clearing Account.

New feature in SAP: Cash positioning without posting

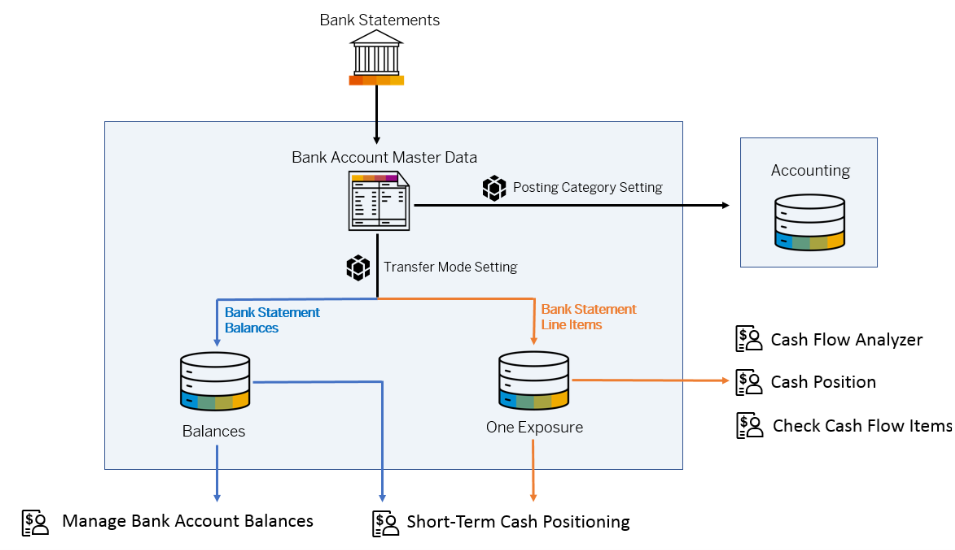

A new functionality has been introduced as of SAP S/4HANA 2111 (Cloud version) and SAP S/4HANA 2021 (On-Premises version) releases. With the new functionality it is no longer required to post the items from the bank statements to have the cash position updated within a selection of Fiori Applications. It is important to note that the feature only applies to the bank EOD (end of day) bank statements, with Intraday bank statements still relying on creating memo records to update cash position.

Depending on the settings maintained within the S/4 environment, one can then view the cash position in either of the 5 Fiori apps. It is possible to use only the balance that is reported by the bank on the bank statement to update the cash position, or use the individual bank statement line items, or both. The picture below shows the sources of information that can be used to update the cash position, as well as which Fiori apps can be used to view the cash position.

Figure 1: How bank statement data can be integrated and processed in cash management. Source

The functionality can prove especially useful in a scattered entity landscape, where multiple accounting systems are used, but only one central system should be used for cash positioning. With this new functionality, where bank statements do not need to be posted, and a minimal setup is sufficient on company code level (no GL accounts are even needed), the enterprise will be able to achieve a consolidated cash position overview in one SAP S/4 environment.

Updating the cash position

How important is it to base the cash position on reconciled accounting entries rather than what the bank has reported on the bank statement? One might argue that using cash position that was updated via the means of the latter process can carry a risk of an unaccounted transaction making its way onto a bank statement, and thus skewing the cash position. But how many times as a treasurer have you actually seen that the bank statement contained transactions that should not be there? What is more, within the current bank connectivity landscape, whereby bank statements are delivered in a secure manner via either SWIFT, H2H, EBICS, instead of a manual upload, the risk of bank statements being tampered with is very low, or even non-existent. So, there we have it, a new means of updating your cash position in SAP.

Supportive API

What is in store for the future for Cash & Liquidity Management within SAP S/4HANA? Do we even need the bank statements if the goal is only to update the cash position? With the increasing presence of APIs within the treasury world, SAP has been also making efforts to allow the cash position to be updated via means other than bank statements. With an API, one would be able to connect to the bank to obtain the information on the current available balance, either on a schedule, or whenever desired, with a click on a button. With the ever-increasing need for up-to-date immediate cash position information, this seems like a logical way forward.

Integrating treasury and supply chain processes via SAP Trade finance functionalities helps companies with strong international trade business exposure to improve transparency and increase efficiency in their order-to-cash, and also purchase-to-pay processes.

Initial functionalities to support trade finance were introduced in SAP Treasury Transaction manager relatively recently in 2016, within the ECC EhP 8 version. Covering the obtained and provided guarantees and letters of credit, they offer a seamless integration between the processes in treasury and the purchase-to-pay, order-to-cash area.

Trade finance covers financial products which help importers and exporters to reduce credit risk and support financing of the goods flow. Almost 90% of world trade relies on trade finance (source: WTO).

What is covered?

Most instruments used in trade finance are supported by the available functionality, namely:

- Guarantees

- Issued – (direct or indirect through correspondent bank) to support the purchase-to-pay process of the buyer.

- Received – to support the order-to-cash process of the seller.

- Commercial and Standby letter of credit (L/C)

Commercial L/C represents direct payment method, while Standby L/C is secondary payment method, used to pay the beneficiary only when the holder fails.- Issued – to pay (on behalf) of the buyer (purchase-to-pay process)

- Received – collect the payment by the seller (order-to-cash process)

How is the functionality integrated with supply chain functionalities?

Once activated, the trade finance financial products are fully integrated to the existing framework of the Treasury transaction manager: you can manage them using the existing transaction codes in front office, back office (settlement, payments, correspondence framework for MT message exchange), accounting, reporting and risk management functions. In case of received guarantees and L/C, the contracts can be included in the respective credit risk limits for the issuing bank. This excellent integration helps the treasury team integrate the trade finance flows to their existing operations with which they are already familiar.

Beyond that, issued L/Cs can be connected with an existing bank facility and (advance) loan contract, in order to be correctly included in its utilisation and to be integrated in the corresponding facility fee calculation. In case of L/C, when conditions to release the payment are fulfilled, a new financing deal can be created or an existing one assigned to the trade finance contract.

Beyond the treasury functionality, the solution offers two unique features to support the trade process:

- Support of Trade documentation management

Fields are available, for example, to note L/C document number, shipment period, places of receipt and delivery, ports of loading and discharge, incoterms. Further it can be defined, which documents are needed to be presented to release the payment, and their scans can be attached to the trade finance deals. Accounting documents can be generated based on flow types, when payment conditions are fulfilled (for off-balance sheet recognition). - Integration with Material management and Sales and distribution modules

One or multiple related sales order numbers (received L/C, guarantee) or purchase order numbers (issued L/C, guarantee) can be maintained in the trade finance contracts. Related FI Customer (applicant) or FI Vendor (beneficiary) can be maintained as business partner.

Integration with the sales module

In case of received trade finance instruments, a tight integration with the sales module is possible. The system is able to check the relevant data in the sales order against one or multiple assigned trade finance transaction for compliance. On the condition that the applicant in the letter of credit is identical to the payer in the sales order. The checks are triggered when:

(a) User saves a sales order after updating the assigned trade finance transactions;

(b) User saves the trade finance transaction after changing the risk-check relevant fields;

(c) User processes goods delivery (e.g. outbound delivery, picking, posting goods issue).

The checks make sure that the sales order amount does not exceed the total of trade finance transactions, considering the tolerance. The currency needs to be identical in both documents. The schedule lines of the goods issues must be within the trade finance document term period.

In case of commercial (standard) L/C, shipment period, partial shipment, places of delivery, ports, shipping methods can be checked. The result of the consistency check is displayed in a dedicated report and can be used as a guide for further action.

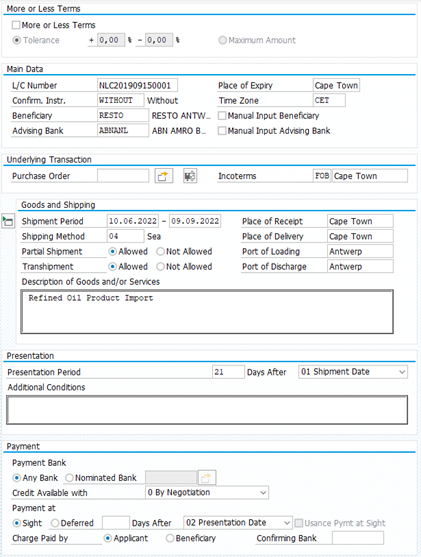

Figure 1: Example available fields for L/C in SAP Trade Finance

In some deployment scenarios, the SAP Treasury is not located in the same system instance as logistic functionalities. For purpose of system integration, APIs (BAPIs) are available for creation and update of trade finance transactions from external systems.

Conclusion

In many companies, trade finance is often an area still managed in separate solutions or in Excel. The SAP S/4HANA Trade finance management helps you to cover the whole lifecycle of trade finance instruments in your SAP Treasury management system and can integrate well with your supply chain functionalities, especially with the sales management.

What does Taulia offer to clients using SAP?

Efficiently managing working capital becomes more and more important for corporates in the current challenging economic conditions and disruptions in the supply chain. As a result, the market has seen an increased demand for early payments of receivables from corporates. Managing working capital is essential in maintaining the health or even the survival of the business, especially in difficult economic times. Furthermore, efficient working capital management could benefit the growth of the company.

Working capital management includes the act of improving the cash conversion cycle. The cash conversion cycle expresses the length in days that it takes to convert cash outflow from purchasing supplies into cash inflow from sales. The cash conversion cycle (CCC) is defined as Days Sales (Receivable) Outstanding + Days Inventory Outstanding – Days Payables Outstanding (CCC = DSO + DIO – DPO). Decreasing DSO and DIO and increasing DPO lowers the cash conversion cycle, accelerates cash flow and improves a company’s liquidity position.

What is Supply Chain Finance?

The most popular method to manage working capital efficiently is using Supply Chain Finance (SCF). We distinguish the following SCF solutions:

- Static discounting: Option for the buyer (using the buyer’s own funds) to get a discount on the invoice if it is paid early. If the option is used, the supplier receives its money earlier than the due date. The discount for the supplier is determined upfront and fixed for a specific number of days.

- Dynamic Discounting: Similar to static discounting using the buyer’s own funds. The difference is that the discount rate is not fixed for a specific number of days. The buyer decides when it wants to pay the invoice. The earlier the invoice is paid, the higher the discount will be.

- Factoring: The supplier is selling its account receivables to a third party. The funding party pays the invoices early (i.e. well before the due date) to the supplier, benefiting the supplier. The interest paid on this solution is based on the credit rating of the supplier.

- Reverse Factoring: The buyer offers the supplier the opportunity to sell its receivables on its SCF platform, so the supplier will receive its money earlier than the due date (from the SCF party). This benefits both the supplier and the buyer, as the buyer will try to extend payment terms with the supplier and therefore pay later than the original due date.

An SCF program is financed by a third-party funder, which is usually a bank or an investing company. Additionally, SCF is often facilitated by technology to facilitate the selling of the supplier’s receivable in an automated fashion.

Reverse factoring

An example of reverse factoring is an automobile manufacturer that is buying various automobile parts from various suppliers. The automobile manufacturer will use a reverse factoring solution to pay the part suppliers earlier and extend the payment terms with these suppliers. Reverse factoring works best when the buyer has a better credit rating than the seller, as the costs of receiving the payment in advance is based on the credit rating of the buyer (which is higher than the credit rating of the seller), the seller receives funding at a more favorable rate than it would receive in the external capital market. This advantage gives the buyer the opportunity to negotiate better payment terms with the seller (higher DPO), while the seller could receive payments of the sale transaction in advance (lower DSO), decreasing the cash conversion cycle of both parties. Effectively, reverse factoring encourages collaboration between the buyer and the seller and potentially leads to a true win-win between buyers and suppliers. The buyer succeeds in its desire to delay payments, while the seller will be satisfied with advanced payments. However, the win for the supplier depends on how the costs of the program are split between the corporate (buyer) and its supplier. Usually, the costs are borne solely by the supplier. Therefore, the program is only desirable for a supplier if the program costs (interest to pay on the SCF funding based on the buyer’s credit rating and the program fee) is lower than the opportunity costs of the supplier. The opportunity costs are defined as the costs of lending funds against an interest rate which is based on its own credit rating.

Benefits and Risks

The benefits of SCF are the following:

- Suppliers can control their incoming cash flows with prepayment of invoices;

- Quick access to funding for the supplier in case of a liquidity crisis;

- Buyer-seller relationship is strengthened due to the collaboration in an SCF program;

- Reduced need of traditional (trade) finance;

- With reverse factoring, the buyer can negotiate extended payment terms with the supplier, providing the prepayment option to the supplier;

- With reverse factoring, suppliers have access to funding with lower interest rates as the pricing of the financing is based on the buyer’s credit rating.

Supply Chain Finance also has risks:

- Reporting ambiguity: Although corporates are obliged under IFRS to disclose additional information about their SCF arrangements (such as Terms and Conditions and carrying amounts of liabilities that are part of the SCF program), reverse factoring can mask true overall debt levels for the supplier when significant amounts of factoring does not have to be classified as debt but as trade payables. Accounting principles IFRS and US GAAP are regularly updated to reflect the latest guidelines around the classification of SCF programs as either trade payables or debt.

- Dependency on SCF: If the SCF program is of a substantial size, a withdrawal of the SCF facility can have dramatic consequences for liquidity and create terminal collateral damage through the supplier network. The US securities regulators warn that reverse factoring is not cycle-tested, which means that it is unclear what might happen in an economic downturn. However, a multi-funder structure makes it easy to replace or add funders in case of a facility withdrawal without disruption to suppliers.

What is Taulia?

Zanders sees a lot of movement in the SCF market. One interesting development is the acquisition of Taulia by SAP. Taulia is a leading supply chain software provider founded in 2009 with over 2 million business users. The rationale behind this acquisition is to expand SAP’s business network further and strengthen the SAP solutions in the financial area. The takeover of Taulia is understandable as more than 80% of the customer base of Taulia runs SAP as their ERP system. Taulia will both be tightly integrated into the SAP software as well as continue to be available as a standalone solution. It will operate as an independent company with its own brand within the SAP Group. Unique in the software business is that Taulia earns a percentage fee of each prepaid invoice that flows through the platform, instead of a fixed fee per transaction or a monthly fee, which is what we usually observe in the market of software vendors. When an invoice is selected for prepayment, the vendor receives a lower amount than the amount of the original invoice. The difference between these amounts is partly compensation for the investor and partly income for Taulia. Taulia offers solutions for all SCF options mentioned earlier: static discounting, dynamic discounting, factoring, and reverse factoring. It is a multi-funder platform on which any and as many banks as desired can be engaged, including the relationship banks of a corporate.

Supply Chain Finance Example

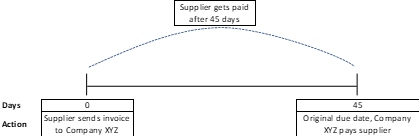

Original situation

In this example, the supplier and Company XYZ have a payment term of 45 days in place. This is the ‘original situation’:

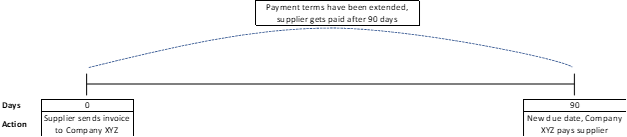

Payment term extension (optional)

Company XYZ starts negotiations with the supplier to extend the payment terms. They agree on a new payment term of 90 days. This step is optional.

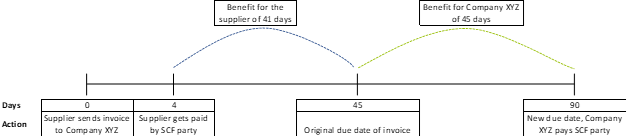

Supplier joins SCF program

The supplier joins the SCF program. Due to the SCF program, the supplier benefits from early payment. The interest that the supplier needs to pay is based on the (strong) credit rating of Company XYZ. In other words, the supplier can finance at lower interest rates.

Features of a Supply Chain Finance program

The features of a best practice SCF program such as Taulia are the following:

- A self-service portal with the branding of your company is provided to your suppliers. Suppliers can be onboarded on this portal, where they select invoices that they would like to receive in advance. When selecting an invoice, the supplier will be quoted with the prepayment costs immediately.

- Automated and near real-time integration with your ERP system, ensuring manual adjustments are redundant and data integrity is maintained. Integration is possible via multiple connectivity solutions or middleware applications. The integration of Taulia with SAP ERP is fully automated. Taulia has its own name space within SAP, although there are no changes in the core SAP code. In this name space, it is amongst others possible to run reconciliation reports. For more information about integration of a SCF platform to SAP, please read this article that we published earlier this year.

- Automatic netting of credit notes against future early payments or block early payments when a credit note is outstanding.

- Leverage real-time private and public data with machine learning in a dashboard to track performance and to make informed decision on your SCF program. This could include scenario analysis of different SCF rates and the effect on adoption rate of your suppliers. Additionally, the dashboard provides benchmarking of payment terms to industry standards.

- Automated solution to automatically accept early payments for suppliers (called ‘CashFlow’ in the Taulia solution). This solution will accept the early payment automatically if the discount is better or equivalent to a pre-set rate curve.

Accounts Receivable solution

Next to the reversed factoring solution, Taulia offers a solution for accounts receivable (AR) financing, also known as factoring. This solution works slightly differently than the reversed factoring solution as your customers do not need to be onboarded on the platform. AR invoices can be sold to a third-party funder, who pays the face value of the invoice less the proposed discount. The actual AR invoice payment from the buyer at maturity date will be collected in a collection account and send back to the investor.

To conclude

The ultimate goal of an SCF program is to unlock working capital for your company. With the choice for an appropriate SCF solution, and a successful implementation including integration to your ERP, the benefits of an SCF program can be achieved. Taulia could be the appropriate solution for you.

If you would like to know more about Supply Chain Finance and/or SAP Taulia, contact Mart Menger at +31 88 991 02 00.

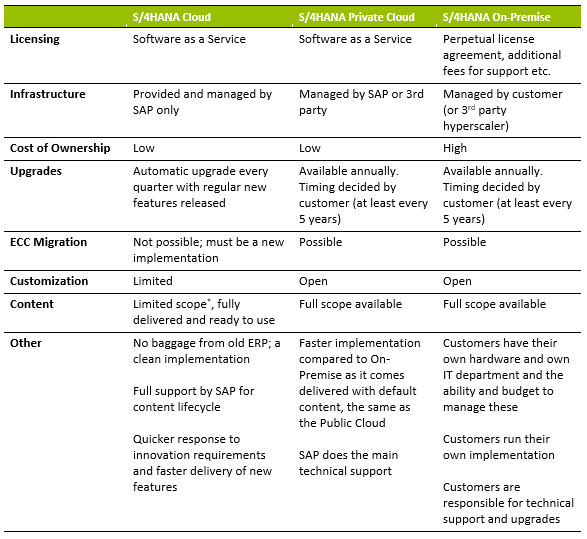

With SAP recently focusing heavily on developing its S/4HANA Cloud solutions, now is an opportune time for corporate executives to investigate the deployment options and weigh up the investment versus the benefit of each.

Changing IT infrastructure and systems is costly, and executives need the right knowledge to make informed decisions to best meet their current and future demands at the optimal price point. What are the best options?

We will start by looking at the features of the various options before taking a deeper dive into what the differences are specifically for Treasury Management on SAP S/4HANA and how that might influence decisions.

The main features are summarized in the table below:

*Scope covered should be sufficient for small to medium corporate treasuries, depending on complexity

Treasury Management on S/4HANA

In terms of selecting the right platform for treasury management on S/4HANA, there are many considerations, and the needs of each organization will differ. SAP has been working to ensure that the Public Cloud for Treasury Management has wider instrument coverage for corporate customers.

A development that could notably sway more corporates to consider the cloud-based options, is the inclusion of the new in-house banking component in the best practice offering from August 2022. In this module, which is embedded into Advanced Payment Management, SAP offers a completely rewritten solution, with advantages even over the traditional In-House Cash (IHC) module. IHC was previously not available to Public Cloud customers and this gap in the offering has no-doubt been a factor in customers deciding not to select the Public Cloud edition. These larger companies often need the payment functionalities available within IHC (such as payments on Behalf of, routing and internal transfers) and the lack of them is limiting. The addition of the in-house banking component makes for a more complete in-house bank functionality when paired with Advanced Payment Management (which is a prerequisite) and Treasury and Risk Management. This new in-house banking solution will also be made available to On-Premise customers during 2022 and with improved features and functionality, should be considered during upgrade decisions.

In Cash Management, S/4HANA Cloud comes standard with Basic Cash Management (Basic Bank Account Management and Basic Cash Operations). Advanced Cash Management, which delivers essentially the same as the On-Premise edition, barring one or two smaller features, is available, although an additional license is required. Liquidity Planning is only available if a customer has an SAP Analytics Cloud license.

SAP Treasury & Risk Management (TRM) is where the most differences currently exist between the Public Cloud and the Private Cloud or On-Premise editions. The Public Cloud has less instruments that are supported, although SAP is continually adding to the list.

Looking at the other most notable differences per area in TRM, the impact of the following in respect of the Public Cloud version should be discussed further with the customer:

- Hedge management – Reference-based hedging is currently not supported.

- Risk analyzers – Portfolio Analyzer is not offered, and SAP has no plans to include it. This is not generally required by corporate treasuries, so should not be an issue if the Public Cloud is selected.

- Securities – the offering is limited, although SAP is working to bridge the gaps. Asset-backed and mortgage-backed securities will be available in the August 2022 release.

- Derivatives – only interest rate swaps and cross currency swaps are possible, with no option to configure your own instruments.

- Position management – limited due to the reduced scope of instruments available in the cloud.

- Treasury analytics – FX reporting in SAP Analytics Cloud is limited but is being improved and customers can expect FX Hedging Area reports to be available by early 2023.

Making the Choice

Based on the above, the Public Cloud option makes sense for new businesses or smaller organizations that do not have the budget or resources to implement and support a customized solution. It would also suit organizations that need their systems to be responsive to market changes. Content is delivered as-is from SAP with minimal customization options, however, the cost of ownership is lower. It should also be noted that currently the Public Cloud edition of S/4HANA has been configured with local requirements for 43 countries. No more countries will be added; however, SAP is working on a tool which will enable customers to copy an existing country and create the settings for an additional country. This feature should be released in 2023.

In terms of treasury management, the Public Cloud would suit organizations with a vanilla treasury function and those that are looking to do a completely new implementation with no need to migrate from an existing system. This option does, however, require what SAP calls a “cloud mindset”, where customers cannot expect the system to fit into their existing processes but instead should look at how their organizational requirements can be met by SAP’s standard offerings.

The On-Premise solution would better suit larger organizations with well-established IT infrastructure and resources, as well as businesses using a broad spectrum of financial instruments that require customization. The On-Premise solution gives the customer full control and maximum freedom in terms of content, configuration, and timings of upgrades although there is a higher cost of ownership.

An attractive choice in the treasury space particularly is the hybrid one, i.e., the Private Cloud. Here customers would outsource their infrastructure management to SAP or another third party, whilst still ensuring they have the flexibility of options around treasury management scope.

With the Private Cloud and On-Premise, customers can still make use of Best Practice content as an accelerator. This content is available online for download and contains the likes of Process Flow diagrams and Test Scripts, helping customers to save time in an implementation. The Cloud’s Starter system is also provided as a way to see content before needing to configure it, thereby allowing the customer to test functionality upfront.

Zanders has in-depth knowledge and experience of Treasury Management on SAP S/4HANA and can help customers to analyze their requirements and ensure they make the best selection between Public Cloud, Private Cloud and On-Premise, or even a combination of the options.

The corporate landscape is being redefined by a plethora of factors, from new business models and changing regulations to increased competition from digital natives and the acceleration of the consumer digital-first mindset.

The new landscape is all about a digital real-time experience which is creating the need for change in order to stay relevant and ideally thrive. If we reflect on the various messages from the numerous industry surveys, it’s becoming crystal clear that a digital transformation is now an imperative.

We are seeing an increasing trend that recognizes technological progress will fundamentally change an organization and this pressure to move faster is now becoming unrelenting. However, to some corporates, there is still a lack of clarity on what a digital transformation actually means. In this article we aim to demystify both the terminology and relevance to corporate treasury as well as considering the latest trends including what’s on the horizon.

What is digital transformation?

There is no one-size-fits-all view of a digital transformation because each corporate is different and therefore each digital transformation will look slightly different. However, a simple definition is the adoption of the new and emerging technologies into the business which deliver operational and financial efficiencies, elevate the overall customer experience and increase shareholder value.

Whilst these benefits are attractive, to achieve them it’s important to recognize that a digital transformation is not a destination – it’s a journey that extends beyond the pure adoption of technology. Whilst technology is the enabler, in order to achieve the full benefits of this digital transformation journey, a more holistic view is required.

Figure 1 provides a more holistic view of a digital transformation, which embraces the importance of cultural change like the adoption of the ‘fail fast’ philosophy that is based on extensive testing and incremental development to determine whether an idea has value.

In terms of the drivers, we see four core pillars providing the motivation:

- Elevate the customer experience

- Operational agility and resilience

- Data driven real time vision

- Workforce enablement

Figure 1: Digital Transformation View

What is the relevance to corporate treasury?

Considering the digital transformation journey, it’s important to understand the relevance of the technologies available.

Whilst figure 2 highlights the foundational technologies, it’s important to note that these technologies are all at a different stage of evolution and maturity. However, they all offer the opportunity to re-define what is possible, helping to digitize and accelerate existing processes and elevate overall treasury performance.

Figure 2: Core Digital Transformation Technologies

To help polarize the potential application and value of these technologies, we need to look through two lenses.

Firstly, what are some of today’s mainstream challenges that currently impact the performance of the treasury function, and secondly, how these technologies provide the opportunity to both optimize and elevate the treasury function.

The challenges and opportunities to optimize

Considering some of the major challenges that still exist within corporate treasury, the new and emerging technologies will provide the foundation for the digital transformation within corporate treasury as they will deliver the core capabilities to elevate overall performance. Figure 3 below provides some insights into why these technologies are more than just ‘buzzwords’, providing a clear opportunity to elevate current performance.

Figure 3: Common challenges within corporate treasury

Cognitive cash flow forecasting systems can learn and adapt from the source data, enabling automatic and continuous improvements in the accuracy and timeliness of the forecasts. Additionally, scenario analysis accelerates the informed decision-making process. Focusing on currency risk, the cognitive technology is on a continuous learning loop and therefore continues to update its decision-making process which helps improve future predictions.

Moving onto working capital, these new cognitive technologies combined with advanced optical character recognition/intelligent character recognition can automate and accelerate key processes within both the accounts payables (A/P) and account receivables (A/R) functions to contribute to overall working capital management. On the A/R side, these technologies can read PDF and email remittance information as well as screen scrape data from customer portals. This data helps automate and accelerate the cash application process with levels exceeding 95% straight through reconciliation now being achieved. Applying cash one day earlier has a direct positive impact on days sales outstanding (DSO) and working capital. On the A/P side, the technology enables greater compliance, visibility and control providing the opportunity for ‘autonomous A/P’. With invoice approval times now down to just 10.4 business hours*, it provides a clear opportunity to maximize early payment discounts (EPDs).

Whilst artificial intelligence/machine learning technologies will play a significant role within the corporate treasury digital transformation, the increased focus on real-time treasury also points to the power of financial application program interfaces (APIs). API technology will play an integral part of an overall blended solution architecture. Whilst API technology is not new, the relevance to finance really started with Europe’s PSD2 (Payment Services Directive 2) Open Banking initiative, with API technology underpinning this. There are already several use cases for both Treasury and the SSC (shared service center) to help both digitize and importantly accelerate existing processes where friction currently exists. This includes real time balances, credit notifications and payments.

The latest trends

Whilst a number of these new and emerging technologies are expected to have a profound impact on corporate treasury, when we consider the broader enterprise-wide adoption of these technologies, we are generally seeing corporate treasury below these levels. However, in terms of general market trends we see the following:

- Artificial intelligence/machine learning is being recognized as a key enabler of strategic priorities, with the potential to deliver both predictive and prescriptive analytics. This technology will be a real game-changer for corporate treasury not only addressing a number of existing and longstanding pain-points but also redefining what is possible.

- Whilst robotic process automation (RPA) is becoming mainstream in other business areas, this technology is generally viewed as less relevant to corporate treasury due to more complex and skilled activities. That said, Treasury does have a number of typically manually intensive activities, like manual cash pooling, financial closings and data consolidations. So, broader adoption could be down to relative priorities.

- Adoption of API technology now appears to be building momentum, given the increased focus around real time treasury. This technology will provide the opportunity to automate and accelerate processes, but a lack of industry standardization across financial messaging, combined with the relatively slow adoption and limited API banking service proposition across the global banking community, will continue to provide a drag on adoption levels.

What is on the horizon?

Over the past decade, we have seen a tsunami of new technologies that will play an integral part in the digital transformation journey within corporate treasury. Given that, it has taken approximately ten years for cloud technology to become mainstream from the initial ‘what is cloud?’ to the current thinking ‘why not cloud?’ We are currently seeing the early adoption of some of these foundational transformational technologies, with more corporates embarking on a digital first strategy. This is effectively re-defining the partnership between man and machine, and treasury now has the opportunity to transform its technology, approach and people which will push the boundaries on what is possible to create a more integrated, informed and importantly real-time strategic function.

However, whilst these technologies will be supporting critical tasks, assisting with real-time decision-making process and reducing risk, to truly harness the power of technology a data strategy will also be foundational. Data is the fuel that powers AI, however most organizations remain heavily siloed, from a system, data, and process perspective. Probably the biggest challenge to delivering on the AI promise is access to the right data and format at the right time.

So, over the next 5-10 years, we expect the solutions underpinned by these new foundational technologies to evolve, leveraging better quality structured data to deliver real time data visualization which embraces both predictive and prescriptive analytics. What is very clear is that this ecosystem of modern technologies will effectively redefine what is possible within corporate treasury.

*) Coupa 2021 Business Spend Management Benchmark Report