Six years ago, LeasePlan decided to set up its own savings bank. In order to be able to follow an investment strategy that reflects the needs of a savings bank, it is important to have a good idea of customer saving behavior. LeasePlan Bank therefore decided to investigate the interest and liquidity typical terms of its savings.

In 1963, LeasePlan Nederland started equipment leasing and providing services to the business market with the ‘Maatschappij tot Verhuur en Financiering van Bedrijfsmiddelen’. Not much later, the company was focusing entirely on leasing vehicles. The operational form of leasing, where all services are provided – including maintenance and insurance as well as financial leasing – was still new at the time. It turned out to be very successful and LeasePlan began its own activities in Belgium and Germany in 1972. Since 1983, LeasePlan also has a branch in the United States. According to the 2015 annual report, LeasePlan now has more than 1.55 million vehicles and employs 7,200 people. The company’s revenue is EUR 6,475 billion and it is active in 32 countries. “We are steadily building on international expansion,” says Rob Keulemans, director of LeasePlan Bank. “We are now working on the start-up of a branch in Malaysia. And our strategy is to continue to grow in Asia.” The profit is growing with the expansion: in 2015, LeasePlan reported a net profit of EUR 442 million, an increase of EUR 70 million (+19 %) compared to 2014.

Banking license

LeasePlan’s history is closely linked with banks and, for part of its existence, the company was part of ABN Amro. “In the history of the company we have basically always been a bank,” says Keulemans. “In the period that LeasePlan was part of ABN Amro, LeasePlan applied for an independent banking license. We got this license in 1993. Until 2009, we funded ourselves on the capital market, with bank lines and securitizations.” That all changed with the crisis, however. “That made it clear that the dependence on wholesale funding was too big. Therefore, a funding-diversification strategy was developed in which the retail bank was a new component. We already had the full banking license, meaning we could attract savings,” says Keulemans.

After thorough research into the savings market and consultation with DNB, in 2009, LeasePlan started incorporating the savings bank: LeasePlan Bank. Keulemans explains: “In a year’s time, we were able to set up all systems and the organization. In February 2010, we opened and our product was distinctive for that time; our interest was linked to the one-month Euribor plus a fixed surcharge. At the time, there was the obvious suspicion as to how banks set their interest. Our transparent interpretation of the savings product proved successful; we got a lot of savings.” LeasePlan Bank is a lean and mean savings bank, with only two products: flexible savings and term deposits. “We only have 17 full-time employees on the payroll, and thus outsource a lot. That works very efficiently,” says Keulemans. “Like some other Dutch banks, we are also active in Germany. With the advent of SEPA, among other things, we did not have to open a branch there. Our German operations are done cross-border from Almere. We now have about 200,000 customers in the Netherlands and Germany. We manage around EUR 5 billion in savings and, thanks to our transparent model, we have a very loyal customer base.”

Longer than overnight

At first, the flexible savings were lent on an overnight basis to the central treasury organization, which is responsible within LeasePlan for the intercompany funding of the countries. “That approach went well for a while,” says Keulemans. “In the meantime, however, we gained a better understanding of customer behavior. The special feature of flexible savings is that you do not know in advance what the duration will be. It was evident that it was longer than overnight, but without historical data, you cannot prove that.”

To get a better idea of customer behavior and thus manage the risks, the bank decided to investigate the interest and liquidity typical terms of the flexible savings. “The liquidity typical part is the most tangible,” says Michelle Ebens, associate strategic finance at LeasePlan. “Because the question is: if a customer has a deposit, how long is it for? The next step was: how can we make a loan portfolio that also mimics the interest typical behavior? If we create eight loans per month, with various maturities, each month an amount is released – and you can then reinvest it every month. It is the intention that the proceeds from this so-called replicating portfolio continue to cover the cost of savings.”

Investment methodology

LeasePlan Bank attempted to translate customer behavior into the loan portfolio, which replicates the behavior of the savings. For this replication, there are two commonly used investment methods: the marginal investment and the portfolio investment strategy. The difference between these is that the marginal investment strategy invests the volume with a fixed allocation in fixed maturities. “And we have opted for the marginal strategy,” explains Ebens. Her role in the project was to gain an understanding of the interest and liquidity typical period of savings. And then analyze how this knowledge could be best implemented in practice: what are the advantages/disadvantages of all the possibilities, what are the risks, how does treasury deal with it? They received help from Zanders consultant Wouter Dikkers. “It’s a tricky matter, but since we are not bound by all kinds of restrictions, we could set up the investment methodology exactly as we had devised it,” he says.

Valuable insight

The interest is no longer linked to the one-month Euribor plus a fixed surcharge – the bank now tells its customers each month what the interest is. “This is now also based on what follows from our model,” said Ebens. “The tricky thing about the project was changing something that had been done in a certain way for five years. We knew that it could be better, but to know how we had to or could change, that takes time.” Keulemans nods in agreement: “Previously, we lent everything briefly to our central treasury organization. But that means that you increase other risks, such as interest rate risks. The approach of this model has put us on the right track. The insight that it provides is very valuable. We now create loans that mimic customer behavior, with which savings are invested longer and the cost is lower. And that is good for the company.”

What has Zanders done for LeasePlan?

- Research on the interest and liquidity typical terms for both variable savings and term deposits;

- Making the transition to an investment strategy, whereby these insights are included in the balance sheet management in the right way;

- Proposal for customized interest and liquidity risk reports to improve the understanding of the risks.

Many banks use a framework of replicating investment portfolios to measure and manage the interest rate risk of variable savings deposits. There are two commonly used methodologies, known as the marginal investment strategy and the portfolio investment strategy. While these have the same objective, the effects for margin and interest maturity may vary. We review these strategies on the basis of a quantitative and a qualitative analysis.

A replicating investment portfolio is a collection of fixed-income investments based on an investment strategy that aims to reflect the typical interest rate maturity of the savings deposits (also referred to as ‘non-maturing deposits’). The investment strategy is formulated so that the margin between the portfolio return and the savings interest rate is as stable as possible, given various scenarios.

A replicating framework enables a bank to base its interest rate risk measurement and management on investments with a fixed maturity and price – while the deposits have no contractual maturity or price. In addition, a bank can use the framework to transfer the interest rate risk from the business lines to the central treasury, by turning the investments into contractual obligations. There are two commonly used methodologies for constructing the replicating portfolios: the marginal investment strategy and the portfolio investment strategy. These strategies have the same objective, but have different effects on margin and interest-rate term, given certain scenarios.

Strategies defined

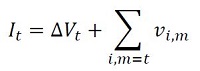

An investment strategy determines the monthly allocation of the investable volume across various maturities. The investable volume in month t ( It ) consists of two parts:

The first part is equal to the decrease or increase in the volume of savings deposits compared to the previous month. The second part is equal to the total principal of all investments in the investment portfolio maturing in the current month (end date m = t ), Σi,m=t vi,m.

By investing or re-investing the volume of these two parts, the total principal of the investment portfolio will equal the savings volume outstanding at that moment. When an investment is generated, it receives the market interest rate relating to the maturity at that time. The portfolio investment return is determined as the principal weighted average interest rate.

The difference between a marginal investment strategy and a portfolio investment strategy is that in a marginal investment strategy, the volume is invested with a fixed allocation across fixed maturities. In a portfolio strategy, these parameters are flexible, however investments are generated in such a way that the resulting portfolio each month has the same (target) proportional maturity profile. The maturity profile provides the total monthly principal of the currently outstanding investments that will mature in the future.

In the savings modeling framework, the interest rate risk profile of the savings portfolio is estimated and defined as a (proportional) maturity profile. For the portfolio investment strategy, the target maturity profile is set equal to this estimated profile. For the marginal investment strategy, the ‘investment rule’ is derived from the estimated profile using a formula. Under long lasting constant or stable volume of savings deposits, the investment portfolio given the investment rule converges to the estimated profile.

Strategies illustrated

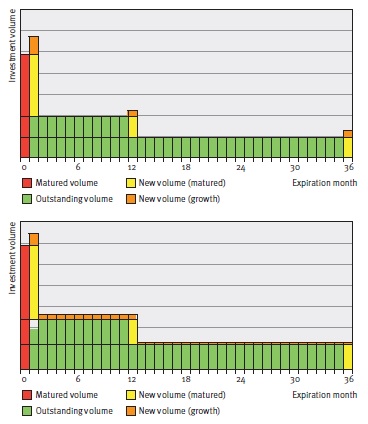

In Figure 1, the difference between the two strategies is graphically illustrated in an example. The example provides the development of replicating portfolios of the two strategies in two consecutive months upon increasing savings volume. The replicating portfolios initially consist of the same investments with original maturities of one month, 12 months and 36 months. To this end, the same investments and corresponding principals mature. The total maturing principal will be reinvested and the increase in savings volume will be invested.

Figure 1: Maturity profiles for the marginal (figure on top) and portfolie (figure below) investment strategies given increasing volume.

Note that if the savings volume would have remained constant, both strategies would have generated the same investments. However, with changing savings volume, the strategies will generate different investments and a different number of investments (3 under the marginal strategy, and 36 under the portfolio strategy).

The interest rate typical maturities and investment returns will therefore differ, even if market interest rates do not change. For the quantitative properties of the strategies, the decision will therefore focus mainly on margin stability and the interest rate typical maturity given changes in volume (and potential simultaneous movements in market interest rates).

Scenario analysis

The quantitative properties of the investment strategies are explained by means of a scenario analysis. The analysis compares the development of the duration, margin and margin stability of both strategies under various savings volume and market interest rate scenarios.

Client interest rate

As part of the simulation of a margin, a client interest rate is modeled. The model consists of a set of sensitivities to market interest rates (M1,t) and moving averages of market interest rates (MA12,t). The sensitivities to the variables show the degree to which the bank has to reflect market movements in its client interest rate, given the profile of its savings clients.

The model chosen for the interest rate for the point in time t (CRt) is as follows:

Up to a certain degree, the model is representative of the savings interest rates offered by (retail) banks.

Investment strategies

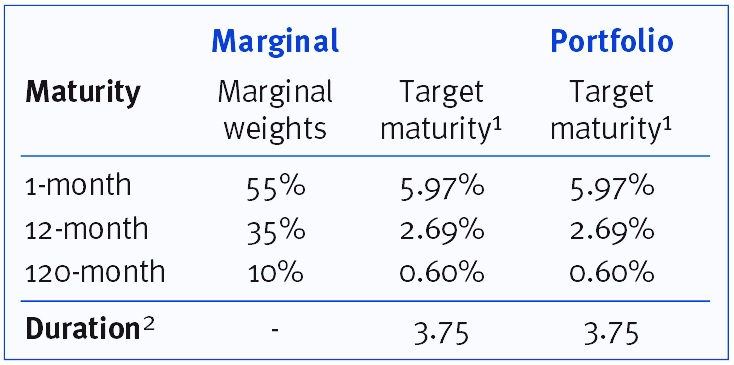

The investment rules are formulated so that the target maturity profiles of the two strategies are identical. This maturity profile is then determined so that the same sensitivities to the variables apply as for the client rate model. An overview of the investment strategies is given in Table 1.

The replication process is simulated for 200 successive months in each scenario. The starting point for the investment portfolio under both strategies is the target maturity profile, whereby all investments are priced using a constant historical (normal) yield curve. In each scenario, upward and downward shocks lasting 12 months are applied to the savings volume and the yield curve after 24 months.

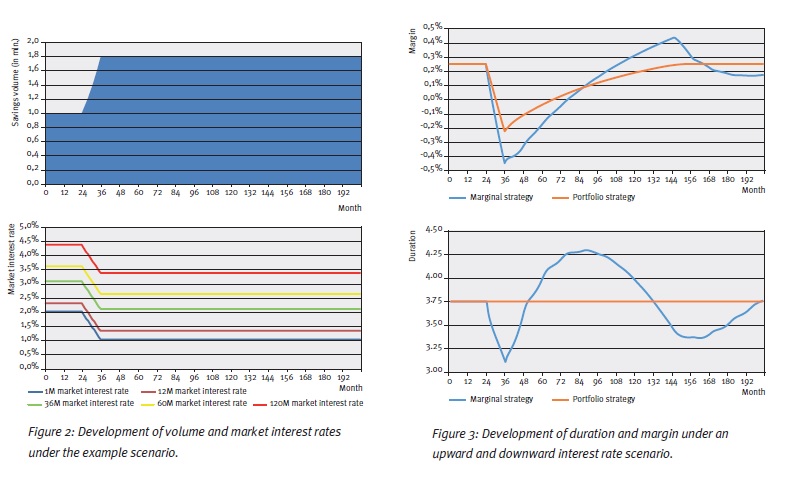

Example scenario

The results of an example scenario are presented in order to show the dynamics of both investment strategies. This example scenario is shown in Figure 2. The results in terms of duration and margin are shown in Figure 3.

As one would expect, the duration for the portfolio investment strategy remains the same over the entire simulation. For the marginal investment strategy, we see a sharp decline in the duration during the ‘shock period’ for volume, after which a double wave motion develops on the duration. In short, this is caused by the initial (marginal) allocation during the ‘stress’ and subsequent cycles of reinvesting it.

With an upward volume shock, the margin for the portfolio strategy declines because the increase in savings volume is invested at downward shocked market interest rates. After the shock period, the declining investment return and client rate converge. For the marginal strategy this effect also applies and in addition the duration effects feed into the margin development.

Scenario spectrum

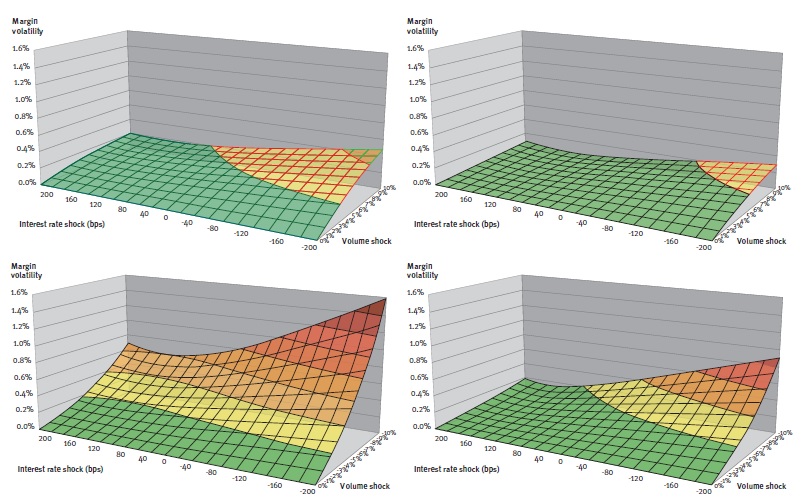

In the scenario analysis the standard deviation of the margin series, also known as the margin volatility, serves as a proxy for margin stability. The results in terms of margin stability for the full range of market interest rate and volume scenarios are summarized in Figure 4.

Figure 4: Margin volatility of marginal (left-hand figure) and portfolio strategy (right-hand figure) for upward (above) and downward (below) volume shocks.

From the figures, it can be seen that the margin of the marginal investment strategy has greater sensitivity to volume and interest rate shocks. Under these scenarios the margin volatility is on average 2.3 times higher, with the factor ranging between 1.5 and 4.5. In general, for both strategies, the margin volatility is greatest under negative interest-rate shocks combined with upward or downward volume shocks.

Replication in practice

The scenario analysis shows that the portfolio strategy has a number of advantages over the marginal strategy. First of all, the maturity profile remains constant at all times and equal to the modeled maturity of the savings deposits. Under the marginal strategy, the interest rate typical maturity can vary from it over long periods, even when there are no changes in market interest environment or behavior in the savings portfolio.

Secondly, the development of the margin is more stable under volume and interest rate shocks. The margin volatility under the marginal investment strategy is actually at least one and a half times higher under the chosen scenarios.

An intuitive process

These benefits might, however, come at the expense of a number of qualitative aspects that may form an important consideration when it comes to implementation. Firstly, the advantage of a constant interest-rate profile for the portfolio strategy, comes at the expense of intuitive combinations of investments. This may be important if these investments form contractual obligations for the transfer of the interest rate risk.

The strategy, namely, requires generating a large number of investments that can even have negative principals in case of a (small) decline of savings volume. Secondly, the shocks in the duration in a marginal strategy might actually be desirable and in line with savings portfolio developments. For example, if due to market or idiosyncratic circumstances there is high inflow of deposit volume, this additional volume may be relatively more interest rate sensitive justifying a shorter duration.

Nevertheless, the example scenario shows that after such a temporary decline a temporary increase will follow for which this justification no longer applies.

The choice

A combination of the two strategies may also be chosen as a compromise solution. This involves the use of a marginal strategy whereby interventions trigger a portfolio strategy at certain times. An intervention policy could be established by means of limits or triggers in the risk governance. Limits can be set for (unjustifiable) deviations from the target duration, whereas interventions can be triggered by material developments in the market or the savings portfolio.

In its choice for the strategy, the bank is well-advised to identify the quantitative and qualitative effects of the strategies. Ultimately, the choice has to be in line with the character of the bank, its savings portfolio and the resulting objective of the process.

- The profile shown is a summary of the whole maturity profile. In the whole profile, 5.97% of the replicating volume matures in the first month, 2.69% per month in the second to the 12th month, etc.

- Note that this is a proxy for the duration based on the weighted average maturity of the target maturity profile.

An extended version of this article is published in our Savings Special. Would you like to read it? Please send an e-mail to [email protected].

More articles about ‘The modeling of savings’:

{kind=link}