At Zanders, we are proud to announce the promotion of Tobias Westermaier as our newest partner.

At Zanders, we are proud to announce the promotion of Tobias Westermaier as our newest partner. With a rich background in Corporate Finance and Treasury, he brings a wealth of experience and a clear vision to support the growth of our Treasury Advisory Group in the DACH region. We caught up with him to learn more about his career journey, aspirations, and insights into the future of our industry.

A Career Built on Global Expertise

“I’ve spent my whole career in Corporate Finance and Treasury roles, working within corporates, banks, and consulting,” Tobias shares. “I joined Zanders Switzerland in 2014 after returning from Asia and was fortunate to work on a variety of projects both in Switzerland and internationally. In 2021, I rejoined Zanders, after gaining further experience in Corporates and Investment Banking in Zurich, to lead the Swiss Treasury Advisory team and help expand Zanders’ footprint in Switzerland and the broader DACH region.”

This journey, marked by diverse experiences and consistent growth, has prepared Tobias for his new role as a partner at Zanders.

Excitement for the New Role

When asked about what excites him most about becoming a partner, Tobias highlights two key areas: growth and collaboration. “I am very much looking forward to actively shaping the Zanders growth story. In particular, I am excited to build and lead our Treasury Advisory Group in the DACH region. Working towards ambitious goals with my outstanding colleagues gives me the most energy. Empowering the team to unlock their full potential will be key to delivering great results for our clients.”

What Makes Zanders Unique

For Tobias, Zanders stands out as a company that truly lives its values of Freedom, Fun, and Collaboration. “The entrepreneurial spirit at Zanders allows everyone to contribute, evolve, and implement ideas. We see opportunities, not obstacles. Cross-departmental and regional collaboration is part of our DNA - we operate as One Zanders. And while we’re passionate about delivering high-quality results for our clients, we never forget to have fun as a group!”

Mentors and Influences

Reflecting on his career, Tobias emphasizes the importance of having trusted mentors and colleagues. “Fortunately, from most of my career steps, colleagues or mentors have remained part of my journey. Having trustful relationships with people who can provide unbiased opinions, new perspectives, or hold up a mirror is invaluable. I encourage everyone to seek such external reflections.”

Industry Trends and Developments

Looking ahead, Tobias is particularly excited about the transformative potential of Artificial Intelligence (AI). “AI is on top of my mind. It will fundamentally change how we work, especially in the consulting industry, and open new opportunities for us and our clients’ business cases.”

Vision for Zanders’ Future

With a steep growth trajectory, Zanders is poised to become the financial performance partner of choice globally. Tobias sees his role as instrumental in achieving this vision. “My contribution focuses on two key areas: (i) growing our presence in the DACH region, and (ii) expanding our service offering for the Office of the CFO. With our expertise, project track record, and global presence, Zanders is well-positioned to achieve its ambitious goals.”

Celebrating the Future

We are very excited to have Tobias join the partner team and contribute to Zanders’ mission of delivering exceptional value to our clients. His leadership, vision, and expertise will undoubtedly propel us forward as we continue to grow and innovate. Congratulations, on this well-deserved promotion!

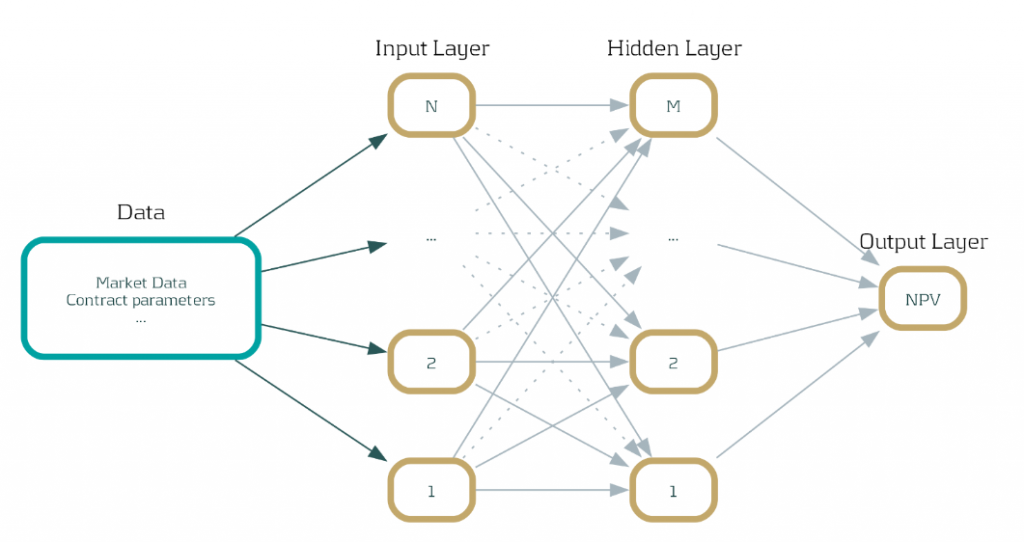

Discover how neural networks are revolutionizing XVA calculations, delivering unprecedented speed, efficiency, and agility for the banking industry.

Introduction: Faster, smarter, and future-proof

In the fast-paced financial industry , speed and accuracy are paramount. Banks are tasked with the complex calculation of XVAs (‘X-Value Adjustments’) on a daily basis, which often involve computationally expensive Monte Carlo simulations. These calculations, while crucial, can become a bottleneck, slowing down decision-making processes and affecting efficiency. What if there is a faster and smarter way to handle these calculations? In this article, we explore a revolutionary approach that uses neural networks to drastically accelerate XVA calculations, promising significant speed-ups without sacrificing accuracy.

The traditional approach: Monte Carlo simulations and their limitations

Traditionally, banks have relied on Monte Carlo simulations to calculate XVAs. These simulations involve numerous complex scenarios, requiring substantial computational power and time. Imagine running simulations endlessly, with every tick of the clock translating to computing expenses. The problem? Time and resources. These calculations must be repeated daily, leading to significant delays and costs, potentially hindering your bank's responsiveness and decision-making agility.

Despite bringing precision, this traditional method poses challenges. Given that the rates offered by banks do not fluctuate dramatically within days, repeating these extensive simulations seems redundant. This redundancy leads us to seek a solution that can deliver both speed and efficiency, paving the way for innovation.

A new era: Leveraging Neural Networks for speed and efficiency

Enter neural networks—an innovative technology that promises a solution to the Monte Carlo conundrum. By training these networks on Monte Carlo simulations conducted early in the week, such as on a Monday, the model can predict outcomes for the rest of the days. This approach sidesteps the need to perform cumbersome computations daily.

Here’s how it works: The neural network learns from initial data, absorbing patterns and information that remain relatively constant through the week. This enables it to approximate net present value calculations with astonishing speed and accuracy. A practical example? Our integration of this technique into the Open-source Risk Engine resulted in a remarkable 600% increase in speed when assessing interest rate swap exposure in a stable market.

Benefits of our solution: Integration and acceleration

- Seamless Integration: Our solution can be seamlessly integrated with any existing systems, as long as they provide net present value outputs for some simulations.

- Scalability with GPUs: Neural network calculations can harness the parallel processing power of GPUs, exponentially increasing inference speed. Imagine every inference equating to calculations for numerous trades simultaneously.

- Feasibility and Reliability: With approximation of net present values being a commonly accepted practice in finance, this approach is both feasible and reliable for banks striving for rapid insights.

Zanders Recommends: A strategic approach to implementation

At Zanders, we believe in empowering banks with cutting-edge technology that aligns with their growth ambitions. Here is what we recommend:

1- Assessment Phase: Evaluate the current computational model and identify areas that can benefit from the implementation of neural networks.

2- Pilot Programs: Start with small-scale implementations to address specific bottlenecks and measure impact.

3- Utilize GPUs: Leverage the parallelization capabilities of GPUs not just for neural networks but also for Monte Carlo simulations themselves, if needed.

4- Continuous Improvement: Regularly update neural network models to ensure accuracy as market conditions evolve.

Our extensive experience with high-performance computing, particularly the use of GPUs for parallelization, positions us as a trusted partner for banks navigating this transformation journey.

Expertise spotlight: High-Performance Computing and AI solutions

In addition to revolutionizing XVA calculations, Zanders offers robust high-performance computing solutions that maximize the capabilities of GPUs across various applications, including Monte Carlo simulations. Our expertise also extends into AI technologies such as chatbots, where we implement and validate models, ensuring banks remain at the forefront of innovation.

Conclusion: Embrace the future of banking technology

As the financial world evolves, so must the technologies that drive it. By leveraging neural networks, banks can achieve unprecedented speed and efficiency in XVA calculations, providing them with the agility needed to navigate today's dynamic markets. Now is the time to embrace a solution that is not only faster but smarter. At Zanders, we're ready to guide you through this transformation. Get in touch with Steven van Haren to learn how we can elevate your XVA calculations and ensure your bank stays competitive in an ever-changing financial landscape.

Explore the overlooked role of FX risk management in enhancing portfolio company value.

In the high-stakes world of Private Equity (PE), where exceptional returns are non-negotiable, value creation strategies have evolved far beyond financial engineering. Today, operational improvements, including in treasury and financial risk management, are required to yield high-quality returns. Among these, FX risk management often flies under the radar but holds significant untapped potential to protect and drive value for portfolio companies (PCs). In this article, we explore the importance of identifying and managing FX risks and suggest various quick wins to unlock value for portfolio companies.

The Untapped Potential of FX Risk Management in Value Creation

PCs operating across multiple countries frequently lack a cohesive treasury and financial risk management approach. For example, bolt-on acquisitions often lead to fragmented teams, processes, systems and banking structures, while exposure to an increasing number of currencies creates financial risk that often remains invisible to central teams. This complexity is exacerbated by ad hoc and localized FX hedging practices, where PCs may not have access to competitive FX rates from their banking partners or access to a multi-bank FX dealing platform.

For PE firms, FX risk often represents a hidden drain on EBITDA and cash flow. FX mismanagement can erode margins and impact portfolio company value. Hence the importance of uncovering financial and operational inefficiencies and building streamlined processes to manage FX exposures effectively. Proper FX risk management, which goes beyond hedging by means of financial instruments, not only mitigates financial risk but directly contributes to value creation by reducing cash flow volatility, reducing costs, increasing control, and increasing transparency.

In this simplified example, a private equity-owned manufacturing firm, focused on expansion into emerging markets, was losing millions annually due to unmanaged foreign exchange (FX) exposures. The culprit? Decentralized treasury processes, idle bank balances in multiple currencies, and hidden FX risks within operational flows. The firm can address and manage these inefficiencies by using FX forward contracts to lock in exchange rates for future transactions and employing centralized treasury technology to monitor and control FX exposures across all operations. By addressing the inefficiencies, the firm reduced financial losses, stabilized its margins, and reinvested savings from FX gains into growth initiatives.

Quick Wins in FX Risk Management

In your search of value creation, we suggest two potential quick wins to unlock PC value.

Enhance Exposure Visibility

Check whether your PCs operate with a clear understanding of their FX exposure landscape. Conducting a quick scan early in the investment lifecycle should identify, amongst others:

- Where exposures are originated (e.g., revenues, costs, intercompany transactions) and if there are natural hedging possibilities.

- Idle cash balances or loans in nonfunctional currencies, which create FX volatility.

- The potential impact of these exposures on financial results through FX risk quantification.

Private equity sponsors can facilitate the creation of a centralized treasury function that i) establishes a policy and process for FX risk management, ii) implements an FX dealing platform for efficient and competitive FX trading with banks, iii) monitors balances to reduce cash balances in non-functional currencies, and iv) implements netting arrangements to streamline intercompany payments and minimize cross-border transactions.

Hidden FX Risk Discovery

Business practices, such as allowing customers to pay in multiple currencies or a pricing agreement based on currency conversions, often lead to hidden FX risks and are a common pain point which is overlooked. For instance, a PC may receive customer payments in USD but agree to link the actual payable amount to the EUR/USD exchange rate, creating an implicit EUR exposure that impacts margins and cash flow.

To address hidden FX risks, a private equity sponsor can help portfolio companies achieve a quick win by conducting a thorough analysis of their pricing models and operational agreements to identify implicit currency exposures, then implementing (soft) hedging techniques, such as adjusting pricing strategies to match revenue and cost currencies, renegotiating contracts with suppliers and customers to align payment terms, and utilizing natural hedging opportunities like balancing currency inflows and outflows, thereby minimizing net exposure before deciding to resort to financial instruments.

In summary, as illustrated by the above quick wins, streamlining treasury processes can yield:

- Hard dollar savings: Reduced FX costs by accessing competitive spreads.

- Soft dollar savings: Enhanced decision-making through better visibility on exposures and reduced operational complexity.

Consider this: A PE-owned retail chain expanded into international markets and faced profit erosion due to unmanaged FX risks and fragmented treasury processes. The sponsor conducted a quick scan to map exposures, uncovering mismatched revenue and expense currencies, a scattered landscape of bank accounts with idle balances, and operational inefficiencies. Hidden FX risks, such as supplier pricing tied to EUR/USD rates and uncoordinated customer payment options in multiple currencies, were also identified. Leveraging these insights, the sponsor centralized FX management by consolidating bank accounts, aligning supplier contracts with revenue streams to create natural hedges, and introducing competitive trading for FX transactions. They also established internal multilateral netting to streamline intercompany settlements, reducing FX costs by 20%.

Measurable Results

Integrating exposure identification and quantification, hidden risk discovery, and treasury process optimization into a single strategy enables PE firms to achieve more stable margins, cost savings, improved cash flow predictability and liberates capital for reinvestment. Furthermore, a proactive approach to FX risk management provides improved transparency for decision-making and LP reporting and strengthens financial resilience against market volatility. By embedding these robust treasury and financial risk management practices, PE sponsors can unlock hidden potential, ensuring their portfolio companies are not only protected but also positioned for sustainable growth and profitable exits.

Conclusion

In the dynamic world of private equity, optimizing FX risk management for internationally operating PCs is a crucial strategy for safeguarding and enhancing portfolio value. Reflect on your current FX risk strategies and identify potential areas for improvement. Are there invisible exposures or inefficiencies limiting your portfolio’s growth? Take the initiative today - evaluate your FX risk management practices and make the necessary refinements to unlock substantial value for your portfolio companies. Embrace the opportunity to drive significant improvements in their financial resilience and overall performance.

If you're interested in delving deeper into the benefits of strategic treasury management for private equity firms, please contact Job Wolters.

Spreading festive cheer and fostering community connections through a heartfelt Christmas high tea for local residents in Amsterdam.

For many, December is the most magical time of the year. It is a season filled with the warmth of family members, the joy of hanging out with friends, and the coziness of gathering around the Christmas tree with Christmas music in the background. It can be said that December is a month of celebration, reflection and gratitude. Yet, amidst the laughter and the shared moments, it's important to remember that for some, this season can also spark feelings of loneliness and hardship.

The true beauty of the holiday season is the part where we give back. We take a moment to extend our kindness and take the opportunity to give back to our communities, to reach out to those who may be struggling, and to make the season a little brighter for everyone. With this in mind, we at Zanders, organized a great initiative called “Zanders Gives Back” that is in line with the spirit of December: a period of solidarity, giving and time together.

With 19 enthusiastic volunteers, we brought festive cheer to a local community house in Amsterdam Oost, a safe neighborhood meeting space where young and old gather to connect with fellow residents, enjoy a nice cup of coffee, receive support, and stay active. Our team organized a Christmas high tea lunch for 50 local residents, who are all part of the wider community. Divided into groups, each with a specific task and clear instructions to ensure that the food was ready on time. We worked together to prepare a nice high tea including delicate sandwiches, colorful fruit sticks, devilled eggs and mozzarella sticks. Meanwhile, others folded napkins and created thoughtful place cards with a nice holiday message to the tables.

After finishing the food preparations, we started decorating the room, stringing garlands along the walls to create a festive atmosphere, and we made sure to have plenty of tea and coffee ready to serve. Just before the guests arrived, we prepared the freshly baked croissants and bagels on the tables, all ready to go for a nice Christmas high tea.

Serving coffee and tea became an opportunity to connect further, listening to local residents, each with their own personal story. It wasn’t just about the food or the decorations. It was about celebrating Christmas together, bridging gaps, and making everyone feel part of something special. Throughout the lunch, laughter was shared, kind words were said, and joy was simply present.

As the afternoon came to an end, we reflected on the impact of this simple yet meaningful gesture. The high tea lunch reminded us of the importance of kindness, the value of community, and the power of working together toward a shared goal. Not only did this experience allow us to give back, but it also strengthened our bond as colleagues, making it a truly memorable day.

At Zanders, we believe that giving back to the community is not just a responsibility but it’s an integral part of who we are. Initiatives like "Zanders Gives Back" allow us to live out our values, making a meaningful impact on the community while fostering a sense of purpose and connection among our team.

Such initiatives are important because they provide us with the opportunity to step outside of our daily work, come together as a team, and contribute to something bigger than ourselves. By engaging with the community, we not only spread joy and support those who may feel lonely or in need, but we also strengthen the bond between our employees, creating shared memories and deepening relationships in a way that goes beyond the workplace. Volunteering activities like this remind us of the power of kindness and connection. They exemplify our commitment to being a company that cares, not only about what we do but about the world we’re helping to shape and make a positive difference.

The PRA’s near-final Rulebook PS9/24 introduces critical updates to credit risk regulations, balancing Basel 3.1 alignment with industry competitiveness, and Zanders offers expert support to navigate these changes efficiently.

The near-final PRA Rulebook PS9/24 published on 12 September 2024 includes substantial changes in credit risk regulation compared to the Consultation Paper CP16/22. While these amendments enhance clarity of Basel 3.1 implementation, institutions should conduct in-depth impact analysis to efficiently manage capital requirement.

PRA has published draft proposal CP16/22 aligning closely with Basel 3.1 reforms. In response to industry feedback, the PRA has made material adjustments in PS9/24, which are aimed at better balancing alignment with international standards and maintaining the competitiveness of UK regulated institutions.

Key takeaways

1- Scope for a ‘Backstop’ revaluation every 5-years for valuation of real estate exposures

2- SME and Infrastructure support factor is maintained, yet firm-specific adjustments will be introduced in pillar 2A.

3- Despite industry concern on international competitiveness, the risk-sensitive approach for unrated corporate exposure is maintained.

The implementation timeline is extended to 1 January 2026 with a 4-year transitional period, which is a one-year delay from the proposed implementation date of 1 January 2025 from CP16/22.

Real Estate Exposures

According to the final regulations, the risk weights associated with regulatory real estate exposure will be calculated based on the type of property, the loan-to-value (LTV) ratio, and whether the repayments rely significantly on the cash flows produced by the property. In place of the potentially complex analysis proposed in CP16/22, the rules for determining whether a real estate exposure is materially dependent on cash flows have been significantly simplified and there is now a straightforward requirement for the classification of real estate exposures.

One major change in the proposals relates to loans that are secured by commercial properties. The PRA has dropped the 100% risk weight floor for exposures backed by commercial real estate (CRE), provided that the repayment is not 'materially dependent on cash flows from the property' and that the exposure fits the 'regulatory real estate (RRE)' definition. Consequently, under the new rules, firms may, in some instances, benefit from low risk weights for commercial real estate, depending on the loan's loan-to-value (LTV) ratio and the type of counterparty involved.

Additionally, the final rules regarding the revaluation of real estate have become more risk-sensitive. Although firms are still required to use the original valuation to calculate LTV, there is now a provision allowing for a ‘Backstop’ revaluation after five years. Going forward, the PRA has eliminated the need for firms to adjust valuations to reflect the 'prudent value' sustainable throughout the loan's duration. The requirements for downward revaluation have been simplified, mandating firms to reevaluate properties when they estimate a market value decline of over 10%. Furthermore, the PRA has specified that valuations can be conducted using a robust statistical model, such as an automated valuation model (AVM).

SME support factor

The PRA has maintained the draft proposal to remove the SME support factor under SA and IRB (Pillar 1), but has applied a firm-specific structural adjustment to Pillar 2A (the ‘SME lending adjustment’). The ‘SME lending adjustment’ aims to absorb the impact of removing the SME support factor in overall capital requirement.

The PRA plans to communicate the adjusted Pillar 2 requirements to firms, ahead of the implementation date of the Basel 3.1 standards on 1 January 2026 (‘day 1’), so that firm-specific requirements will be updated at the same time as the Basel 3.1 standards are implemented.

Infrastructure support factor

The PRA has maintained the draft proposal to remove infrastructure support factor under SA and IRB approach, but has made two material changes which will diminish the impact on overall capital requirement.

i. apply a firm-specific structural adjustment to Pillar 2A (the ‘SME lending adjustment’), which will minimize disruption in overall capital requirement.

ii. introduce a new substantially stronger category in the slotting approach for IRB. PRA proposed lower risk-weight on the ‘substantially stronger’ IPRE exposures in CP16/22. The new definition of ‘substantially stronger’ is expected to include broader scope of IPRE exposures, thus lowering overall capital requirement.

Unrated corporate exposures

The PRA has maintained the draft proposal of introducing a two-way method on unrated corporate exposures: risk-sensitive and risk-neutral approach. Since the new approach does not apply in other jurisdictions, additional operational challenge is expected. Also, the 135% risk-weight on Non-IG(non-Investment Grade) unrated corporate exposure is higher than 100% in other jurisdictions, implying higher lending cost for UK regulated banks compared to its internationally regulated peers.

i. risk-sensitive approach : The PRA has proposed a risk-sensitive approach additional to the Basel III reforms. Exposures assessed by firms as IG would be risk-weighted at 65%, while exposures assessed by firms as Non-IG would be risk-weighted at 135%. This is a more risk-sensitive approach which aims to maintain an aggregate level of RWAs broadly consistent with the Basel III reforms.

ii. risk-neutral approach: 100% risk weight is applied where the risk-sensitive approach is too costly or complex.

In conclusion, the PRA's near-final Rulebook (PS9/24) reflects significant revisions to credit risk regulation that enhance clarity and alignment with Basel 3.1, while addressing industry feedback. The introduction of a five-year 'backstop' revaluation for real estate exposures, firm-specific adjustments for SMEs and infrastructure support factors, and the maintenance of a risk-sensitive approach for unrated corporate exposures underscore the PRA's commitment to balancing regulatory requirements with maintaining the competitiveness of UK institutions.

The extended implementation timeline to 1 January 2026, along with the transitional period, allows firms adequate time for adjustment. Overall, these changes aim to foster a more robust and competitive banking environment, while also navigating the complexities introduced by differing international standards.

How can Zanders help?

We have extensive experience of implementation and validation of Pillar 1 & 2 models which allows us to effectively support our Clients managing the change process to full compliance with the latest regulations.

From our experience, as the following are key areas on which our services can add most value:

1- Carry out thorough self-assessment against new requirements including an impact analyses of new regulations on their capital requirements.

2- Support model development activities to align models to new rules; we could be done either on an advisory basis or via direct supply of additional resources

3- Support amendments to Pillar 2 models (which will have to reflect changes to Pillar 1 models)

4- Support Internal Validation activities across Pillar 1 & 2

5- Carry out quality assurance on final models & documentation before final submission to the PRA

6- Support adoption of solutions for prudential valuation of (real estate) collateral while integrating climate risk information.

Please reach out to Paolo Vareschi or Suneet Dutta Roy to find out more about how we could support you on your journey to Basel 3.1 compliance.

References

[1] Bank of England (2024), PS9/24 – Implementation of the Basel 3.1 standards near-final part 2 URL PS9/24

[2] Bank of England (2022), CP16/22 – Implementation of the Basel 3.1 standards

URL CP16/22

This blog explores how financial institutions can enhance their risk data aggregation and reporting by aligning with BCBS 239’s RDARR principles and the ECB’s supervisory expectations.

The ECB Banking Supervision has identified deficiencies in effective risk data aggregation and risk reporting (RDARR) as a key vulnerability in its planning of supervisory priorities for the 2023-25 cycle and has developed a comprehensive, targeted supervisory strategy for the upcoming years.

Banks are expected to step up their efforts and improve their capabilities in Risk Data Aggregation and Risk Reporting as Risk Data Architectures and supporting IT infrastructures are insufficient for most of the Financial Institutions. Hence, RDARR principles are expected to become more and more important during Internal Model Investigations and OnSite Inspections by the ECB.

In May 2024, the ECB published the Guide on effective risk data aggregation and risk reporting to ensure effective processes are in place to identify, manage, monitor and report the risks the institutions are or might be exposed to. With it, the ECB details its minimum supervisory expectations for a set of priority topics that have been identified as necessary preconditions for effective RDARR.

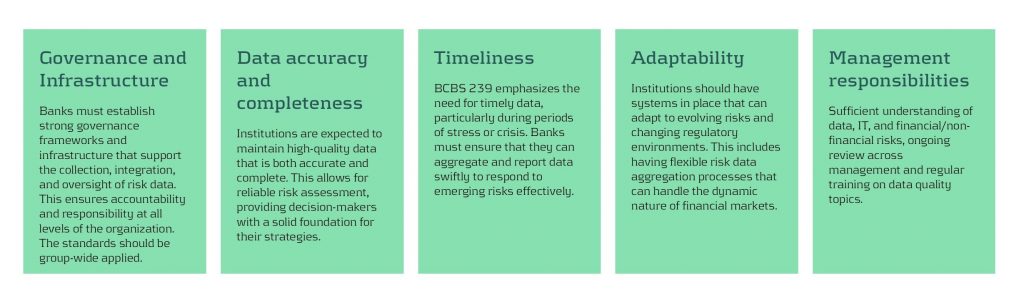

The ECB identifies seven priority areas, considered important prerequisites for robust governance arrangements and effective processes for identifying, monitoring and reporting tasks. The scope of application of these principles is reporting, Key Internal Models and other important models (e.g., IFRS9):

Relevance of BCBS 239

RDARR represents the implementation of the principles outlined in BCBS 239, which was published by the Basel Committee on Banking Supervision (BCBS) in 2013. BCBS 239 is essential to maintain regulatory compliance, mitigate risks, and drive data-driven decision-making. Non-compliance can result in significant financial penalties, reputational damage, and increased scrutiny from regulatory bodies. Therefore, BCBS 239 is a crucial framework that enhances financial stability by setting robust standards for risk data aggregation and reporting. Its principles encourage institutions to embrace data-driven practices, ensuring resilience, transparency, and efficiency. While challenges such as legacy infrastructure, data quality, and evolving risks persist, banks can overcome these hurdles through strategic investment in governance, technology, and data-driven culture to build end-to-end data transparency.

Zanders’ view on supervisory planning

We believe the following 5 topics of the RDARR principles are of major importance for financial institutions:

Establishing an effective program to review and address these topics, considering the nature, size, scale and complexity of each financial institution, will facilitate alignment with the ECB’s expectations.

Zanders experience on RDARR implementation

Data extends beyond being merely a technical database; it is a fundamental component of an organization’s strategic framework. Data-driven organizations are not defined solely by their technological solutions, but by the data culture across the entire organization. At Zanders, we have assisted clients in developing data strategies aligned with RDARR principles and supported the implementation of future-proof data utilization, including the integration of advanced tools such as AI.

One critical observation is that organizations must urgently address key questions regarding their data: What governance structures are currently in place? Are roles and responsibilities within this governance framework clearly defined? Is the governance being effectively implemented as planned? What training, guidance, and support do employees require? Are data definitions and requirements consistently aligned across all stakeholders? When undertaking such an extensive program, institutions must carefully consider whether a top-down or bottom-up approach will be most effective. In the case of RDARR, success necessitates a comprehensive, dual-directional approach that fosters change across all levels.

If you are unsure about your compliance with BCBS 239 and RDARR requirements, contact us today to ensure alignment with best practices.

A recent webinar outlined strategies for optimizing corporate treasury FX programs, addressing recent risk events, potential 2025 challenges, and the importance of strong risk management policies.

Recently, Zanders' own Sander de Vries (Director and Head of Zanders’ Financial Risk Management Advisory Practice) and Nick Gage (Senior VP: FX Solutions at Kyriba) hosted a webinar. During the event, they outlined strategies for optimizing corporate treasury FX programs. The duo analysed risk-increasing events from recent years, identified potential challenges that 2025 may pose, and discussed how to address these issues with a strong risk management policy.

Analyzing 2024 Events

The webinar began with a review of 2024's key financial events, particularly the Nikkei shock. During this period, the Japanese Yen experienced significant appreciation against the USD, driven by concerns over U.S. economic projections and overvalued tech stocks. This sharp rally in the JPY led to a wave of unwinding carry trades, forcing investors to sell assets, including stocks, to cover their positions. Additionally, western central banks continued their gradual reduction of interest rates throughout 2024, further influencing market dynamics. The webinar explored the correlation between these economic shocks and anticipated events, particularly their impact on EUR/USD rate fluctuations. By examining how past events shaped market volatility, risk managers can better prepare for potential future disruptions.

Coincidentally, the webinar was held on November 5, 2024, the same day as the U.S. presidential election—a key topic of discussion among the hosts. The election outcome was expected to have a significant impact on markets, increasing both volatility and complexity for corporate risk managers. Shortly after the session, another Trump victory was announced, leading to a strengthening of the USD against the EUR, even as the Federal Reserve reduced interest rates further in the following days. In addition to the election, rising geopolitical tensions and ongoing reductions in base interest rates were highlighted as potential catalysts for heightened market volatility.

Challenges and Opportunities in 2025

By reflecting on past challenges and looking ahead, risk managers can optimize their policies to better mitigate market shocks while protecting P&L statements and balance sheets. Effective risk management begins with accurately identifying and measuring exposures. Without this foundation, FX risk management efforts often fail—commonly referred to as “Garbage In, Garbage Out.” A complete, measurable picture of exposures enables risk managers to select optimal responses and allocate resources efficiently.

During the webinar, a poll revealed that gathering accurate exposure data is the biggest challenge in FX risk management. Common issues include fragmented system landscapes, incomplete data, and delays in data registration. Tools designed for FX risk planning and exposure analysis can address these gaps by verifying data accuracy and ensuring completeness.

A sound financial risk management strategy considers three core drivers:

1- External Factors: These include the ability to pass FX or commodity rate changes to customers and suppliers, as well as regulatory constraints faced by corporate treasuries.

2- Business Characteristics: Shareholder expectations, business margins (high or low), financial leverage, and debt covenants shape this driver.

3- Risk Management Parameters: These encompass a company’s risk-bearing capacity (how much risk it can absorb) and its risk appetite (how much risk it is willing to take).

By incorporating these drivers into their approach, risk managers can design more effective and strategic responses, ensuring resilience in the face of uncertainty.

Understanding these core risk drivers can enable risk managers to derive a more optimal response to their risk profile. To design an optimal hedging strategy, treasurers need to consider various risk responses, which include:

- Risk Acceptance

- Risk Transfer

- Minimization of Risk

- Avoidance of Risk

- Hedging of Risk

Treasury should serve as an advisory function, ensuring other departments contribute to mitigating risks across the organization. While creating an initial risk management policy is critical, continuous review is equally important to ensure the strategy delivers the desired results. To validate the effectiveness of a financial risk management (FRM) strategy, treasurers must regularly measure risks using tools like sensitivity analysis, scenario analysis, and at-risk analysis.

- Sensitivity analysis and scenario analysis evaluate how market shifts could impact the portfolio, though they do not account for the probability of these shifts.

- At-risk analysis combines the impact of changes with their likelihood, providing a more holistic view of risk. However, these models often rely on historical correlations and volatility data. During periods of sharp market movement, volatility assumptions may be overstated, which can undermine the reliability of results.

We recommend a combined approach: use at-risk analysis to understand typical market conditions and scenario analysis to model the impact of worst-case scenarios on financial metrics.

To further enhance hedging strategies, some corporates are turning to advanced methods such as dynamic portfolio Value-at-Risk (VaR). This sophisticated approach improves risk simulation analysis by integrating constraints that maximize VaR reductions while minimizing hedging costs. It generates an efficient frontier of recommended hedges, offering the greatest risk reduction for a given cost.

Dynamic portfolio VaR requires substantial computing power to process a large number of scenarios, allowing for optimized hedging strategies that balance cost and risk reduction. With continuous backtesting, this method provides a robust framework for managing risks in volatile and complex environments, making it a valuable tool for proactive treasury teams.

Conclusion: Preparing for 2025

2024 was a year that brought many challenges for risk managers. The market uncertainty resulting from many larger economic shocks, such as the U.S. Election and multiple geopolitical tensions made an efficient risk management policy more important than ever. Understanding your organization's risk appetite and bearing capacity enables the selection of the optimal risk response. Additionally, the use of methods such as dynamic portfolio VaR can promote your risk management practices to the next level. 2025 looks to create many challenges, where treasurers should stay vigilant and create robust risk management strategies to absorb any adverse shocks. How will you enhance your FX risk management approach in 2025?

You can view the recording of the webinar here. Contact us if you have any questions.

Mastering payment orchestration isn’t just a tech upgrade—it’s a strategic game-changer that can unlock savings, boost liquidity, and fuel global competitiveness in today’s complex, multi-channel marketplace.

The Right Payment Orchestration Strategy: A Critical Factor for Success

The digitalization and globalization of payment infrastructures have significantly impacted businesses in recent years. Financial departments of multinationals operating in a multi-channel environment are now required to manage a diverse range of payment methods, currencies, and interacting platforms, increasing complexity. This results in higher costs for companies, especially those with higher transaction volumes in B2C, diverse market operations, and global presence. These organizations are further required to integrate disparate payment solutions, including mobile payments, e-wallets, and physical channels. The global reach of these systems adds challenges in overseeing cross-border transactions, managing a broad and diverse group of payment service providers.

Moreover, the regulatory environment in the payments sector is constantly evolving. New regulations such as PSD2 in Europe, stricter data protection guidelines like GDPR, and international standards like ISO 20022 are influencing how payments are processed. Organizations must continually adapt to these regulatory changes to ensure compliance while maintaining efficiency and security in their payment processes. These changes can significantly impact systems, processes, internal cost structures, and often require strategic realignment.

Under this scenario, can companies afford to leave millions in savings on the table?

Previously considered merely as an operational task, payment transactions offer a way to unlock untapped value while navigating the complexities of global payments and hence has gained strategic importance. Efficient payment management will enhance a company's liquidity, minimize risks, and reduce costs. By leveraging a modern payment orchestration, companies can centrally control their payment flows, gain real-time transparency over their financial positions, and make better decisions in cash and liquidity management. This not only significantly contributes to a company's competitiveness and financial stability but also has the potential to become a critical success factor for the organization and to directly influence liquidity — a central focus of any treasury function.

In other words, a well-designed payment orchestration strategy is far more than a technical enhancement. It is actually a vital component of a modern, efficient business strategy for corporations operating in B2C environments and those adapting to evolving business models in B2B markets.

Understanding the Use of Payment Orchestration

As customer demand for specific payment channels has grown, companies have increasingly relied on single payment service providers, especially for incoming payments, in order to offer global solutions. However, this dependence amplifies organizational risks, as any failure or disruption within the provider's system can severely impact operations and costs. The challenges and resource demands of switching providers, coupled with reliance on bespoke solutions, further entrench this dependency, leaving companies vulnerable to operational disruptions and potentially escalating indirect transaction costs over time.

Under this context, payment orchestration can mitigate these adverse effects by integrating multiple providers and using advanced technologies, like redundancy and dynamic routing, that improve success rates and minimize transaction costs, ensuring maximum efficiency for global operations.

An efficient payment orchestration strategy requires careful consideration of factors such as the organizational anchoring of the topic (with treasury in the lead), the business model’s geographic presence, customer-specific needs, and the impact of payment methods on revenue and customer acceptance. Optimizing cost structures across providers and channels demands a deep understanding of business models and their fee structures. Under this topic, the Payment Orchestration Expert Thomas Tittelbach, CPO DINAPE Solutions GmbH, quotes the following: “Corporates often struggle with the complexity of payment processing, non-transparent pricing, and provider lock-ins. With the growing success of payment orchestration offerings, Corporates get back in the driver seat for their business.”

Technical Optimization: Breaking It Down

The payment environment is undergoing significant changes, particularly in digital payment methods. Concurrently, there is a shift in demand across various channels, prompting providers to offer innovative solutions. Leading providers like Stripe, Adyen, and Computop rely on advanced platform technologies to ensure optimal payment execution. These providers simplify payment processing by consolidating multiple payment channels—such as Payment Service Providers (PSPs), gateways, and wallets—onto a single platform. This integration aims to reduce costs through intelligent strategies that consistently deliver the best solutions for the organization. To understand this better, it is crucial to examine how payment orchestration impacts cost factors:

- Service and Technological Capabilities: Features offered by providers to help reduce transaction costs.

- Fees Charged by Providers: The costs associated with the services they deliver.

- Post-Processing Services: Solutions that unify and automate data transfer to ERP and treasury systems.

Regarding service and technological capabilities, providers often align their marketing with buzzwords like “dynamic routing,” “multi-acquirer strategy,” and “interchange optimization.” Let us break these down further:

- Dynamic Routing: Dynamic routing allows payment orchestration platforms to optimize transactions by selecting the most cost-effective provider, reducing interchange and scheme fees, improving success rates, and minimizing currency conversion costs. This results in significant cost savings and increased operational efficiency for the organization.

For instance, routing a European customer's payment to a local acquirer instead of a global provider could generate savings of almost 1.5% per transaction by avoiding unnecessary cross-border fees.

- Multi-Acquirer Strategy: By integrating multiple acquirers, platforms leverage local providers for local transactions, create competition to lower fees, and ensure redundancy by rerouting payments if one provider fails.

- Authorization Optimization: Advanced platforms use machine learning to determine the optimal time for submission, select transaction currencies that issuers are most likely to approve, and account for issuer preferences in different regions.

- Interchange Optimization: By routing transactions through acquirers with the lowest interchange fees, particularly in international contexts where these fees can range from 1–2% or higher, companies can minimize costs.

The Business Case: Numbers That Speak for Themselves

Asessing the effectiveness of technological capabilities can be complex, but comparing provider fees is much more straightforward. Transaction size and volume significantly influence overall costs, with volume-based discounts often playing a decisive role. Companies processing over one million transactions annually can negotiate processing fee reductions of up to 0.2%, resulting in substantial savings. Additionally, processing costs can be reduced by up to 0.5% through the addition of new payment methods via payment orchestration.

This case highlights the stark cost differences among providers, analyzing credit cards (EU and international), wallets, and direct debit payments. Providers such as Adyen, Stripe, Payone, Mollie, Checkout.com, Worldline, and Computop were included in the comparison, with a focus on European-based companies operating internationally.

While direct debit offers limited opportunities for price differentiation, credit cards and wallets reveal significant variations. For EU credit cards, fees can differ by a factor of 2.3 annually among providers. Wallet fees, while less variable, still show discrepancies of up to 20%. Consequently, companies could pay over 1 million EUR more in credit card fees alone when choosing a more expensive provider.

Not all fees are transparently structured, and acronyms are frequently used to describe cost components. However, the fees for each payment method can be categorized into the following structure:

| Fee Component | Description |

| Processing Fee | Fixed amount per transaction. |

| Interchange Fee | Often regulated (e.g., 0.2% for debit cards in the EU, app. 2% for credit cards in the US). |

| Scheme Fee | Varies by card network (e.g., Visa or Mastercard). |

| Acquirer Margin | Percentage of the transaction value. |

Our analysis closely examined the official fee structures of the providers listed, and calculated costs based on specific parameters outlined in Figure 1. The scenario focuses heavily on EU credit cards and wallets, while chargeback costs, currency conversion fees, and other cost components were excluded for simplicity. Figure 2 provides an overview of the average costs across all providers. A key finding is that payment processing costs, particularly for credit cards and wallets, can accumulate significantly if the details are overlooked. For wallets specifically, fee structures show considerable variation between providers.

These differences are significant. In total, the gap between the most cost-effective and most expensive provider in our hypothetical analysis reached nearly EUR 5 million annually— a figure that one cannot neglect and would justify a closer look at payment orchestration.

Payment Orchestration as the untapped Opportunity

The business case underscores the significant cost differences between providers and the key factors affecting payment efficiency, showing that payment orchestration can play a significant role in the organization’s success in managing cost and liquidity — a central focus of any treasury function. As a result, a well-executed payment orchestration strategy is not only an operational improvement but also a strategic element for a company’s overall success. Consequently, selecting the right provider goes beyond operational considerations and demands strategic evaluation of company goals, payment flows, and international presence.

By integrating payment orchestration into their cost and efficiency strategies, multinationals can achieve measurable financial and organizational benefits. With Zanders’ expertise, companies can align payment orchestration capabilities into their payment transactions’ framework to enhance operational transparency, optimize transaction approvals, achieve cost savings, and improve liquidity management. This can lead to increased profitability, enhanced liquidity, and improved compliance across different jurisdictions. Neglecting this potential means leaving substantial untapped value on the table—value that could otherwise drive growth and innovation.

If you would like to learn more about digital payment strategies in corporate treasury, please reach out to Sven Warnke or Gustavo Alves Caetano.

With this article we delve into the key mechanics of creating a successful Treasury function for a carved-out business, starting with its strategic foundation – a tailored, well-defined Target Operating Model (TOM).

In our previous article 'Navigating the Financial Complexity of Carve-Outs: The Treasury Transformation Challenge and Zanders’ Expert Solution' we outlined that in a carve-out, the TOM for the new Treasury function must be tailored to the unique characteristics of the newly formed entity. This includes considerations such as operational scale, geographical footprint and risk profile, aligned with investor preferences. To achieve this, the TOM will outline how the Treasury function will operate, including its governance structure, team size and composition, service delivery model, and its evolving role within the future organization.

Hence, a clear and prioritized TOM provides a roadmap for Treasury, ensuring the function is ready for its new challenges and addressing the carved-out entity’s needs. Furthermore, it ensures that Treasury’s role as a value-adding partner is fully realized, helping to drive long-term success.

So, where do you start with right-sizing the new Treasury organization? Below, we outline the key strategic and transactional topics to consider.

Shaping the Future of Treasury: Priorities and Strategic Objectives

The TOM of a Treasury function serves three essential purposes:

- (1) Ensuring the minimum viable design is in place for seamless operations from day one.

- (2) Defining how the Treasury function will actively drive value and align with the business’s strategic goals.

- (3) Creating a roadmap for growth: Laying the groundwork for Treasury’s future scalability and maturity as the business evolves.

From the outset, defining the TOM presents a key opportunity for Treasury to evolve from a purely operational support function to a strategic advisor. This transformation allows Treasury to play a pivotal role in decision-making, particularly in areas like working capital optimization, capital allocation, and future M&A activities. Moreover, it ensures that Treasury’s objectives are closely aligned with the broader goals of the organization, including growth, operational efficiency, and risk mitigation.

To achieve these objectives, a well-defined governance structure is essential. Governance provides the authority, alignment, and oversight necessary for effective risk management, cash flow optimization, and other core activities – transforming strategic aspirations into tangible results.

Governance Structure: Striking the Right Balance

Fundamentally a goal of the Treasury function is how it supports the broader business in achieving financial stability, operational efficiency and strategic objectives. Achieving this requires a governance structure that balances centralized control with local autonomy, tailored to the organization’s global footprint. The TOM serves as a unifying framework, aligning processes not only across Treasury but also with other functions to ensure consistency and collaboration.

This can be done by deciding where Treasury activities will be performed and applying either a centralized model (managed at a headquarters level) or decentralized model (with regional or local autonomy under a defined framework). With the need to keep agility in mind it’s a balancing act to ensure a lean but skilled Treasury team is in place to handle immediate requirements, with contingency plans for scaling as the business grows. Therefore, in most carve-outs a hybrid model is preferred initially, allowing for centralized oversight of critical activities (e.g., funding and risk management) while empowering local teams to handle region-specific cash and banking needs.

To complement this structure, clearly defining roles and responsibilities is crucial. Treasury teams must have well-delineated duties across areas like cash management, risk management, funding, financial reporting, and technology operations, ensuring effective decision-making and accountability. Equally important is the design of Treasury processes. As a central pillar of the organizational landscape, Treasury processes should prioritize standardization across regions to streamline operations and mitigate risks. Further, as a logical consequence of defined roles and responsibilities as well as of well-designed Treasury processes, the new TOM as offers an opportunity to clearly define and implement process and data interfaces between Treasury and other corporate functions, such as accounting and procurement, fostering seamless collaboration and enhancing overall efficiency.

Unveiling the Future: Day 1 Readiness and the Launch of a Bold Treasury Operating Model

As the governance structure is established, the next critical milestone in the carve-out process is ensuring readiness for Day 1 - when the responsibility officially shifts from the parent company to the newly independent entity. A well-designed TOM provides not only the governance framework but also the operational infrastructure needed for a seamless transition. This includes setting up the foundational capabilities that will allow the Treasury to operate without disruption, from basic cash visibility and banking relationships to staffing and technology setups.

- (1) Cash Visibility and Control with basic structures in place to ensure real-time visibility into cash positions across bank accounts, usually brought about by establishing processes for daily cash reconciliations, payment approvals and funding allocations.

- (2) Banking Relationships with the core banking partners onboarded and the account structures in place to manage inflows, outflows, and currency requirements. This may also include transferring the existing banking arrangements from the parent company or establishing new core banks.

- (3) Technology Setup comprising of a basic Treasury Management System (TMS) or interim solution in place to support key processes.

- (4) An appropriate level of Staffing and Expertise with a lean but skilled Treasury team in place to handle immediate requirements, with contingency plans for scaling as the business grows.

Underpinning these areas is the formalisation of a Treasury Policy and Procedures including essentials such as policies for cash management, payment processing and risk management to ensure compliance and mitigation of operational risks.

A Roadmap for achieving Treasury Maturity

While the minimum viable design outlines Day 1 functionality, the TOM also provides a clear pathway for scaling and maturing the Treasury function as the business evolves. Viewing the TOM as a strategic concept enables the business to set a target trajectory from the outset and identify and prioritise areas for long-term maturity. The design of a well-balanced – i.e. of appropriate complexity but with scope to grow – function at this stage is a critical tactical decision, something that Zanders does by taking into account development trends using our proprietary Treasury Risk Maturity Model.

Following the carve-out activity and as the new entity stabilises there will naturally be a move towards greater centralization and standardization of core Treasury functions, whose deployment can be improved by addressing them in the TOM. In turn, a centralization will result in the streamlining of processes such as cash pooling, intercompany funding, and hedging activities to improve efficiency and reduce costs.

To support these optimization processes after the transaction, designing the TOM to be agile enables the Treasury to scale operations both seamlessly in response to business growth or market changes but also to standardise by introducing consistent policies and processes. For example these could include those for cash management, risk mitigation, and compliance across all regions to enhance control and visibility across the function.

Ultimately the implementation of a well-defined TOM from the outset will be beneficial on both a functional and wider level. Taking Treasury as an intrinsic need of the business and therefore as a strategic function (as opposed to siloed and complimentary) empowers the broader finance department’s contributions to the strategic moves of the company overall.

Strategic evolution to Treasury excellence

Building a Treasury function for a carved-out entity is a complex yet rewarding process that requires strategic planning across all Treasury and finance areas. A clear TOM not only ensures operational readiness from Day 1 but also provides a robust framework for Treasury’s evolution. By defining how the Treasury function will serve the business, establishing a minimum design for immediate needs, and outlining a roadmap for maturity, the TOM ensures alignment with the carved-out entity’s goals. Over time, this approach positions Treasury as a strategic enabler, driving financial stability, operational efficiency, and long-term growth.

Zanders’ experts for Treasury M&A can help you in assessing and designing fit-for-purpose TOM models and considering the relevant aspects of their implementation, thereby realizing the specific benefits identified in the design phase. We bring extensive experience in M&A transactions and will effectively navigate you through the process of establishing a new Treasury function. Reach out to discuss your case with us.

In the next edition of this series, we look at implementing effective Cash and Liquidity Management practices within the newly carved-out entity, key areas of focus and the risks involved.

If you would like to learn more about how to build a Treasury function for a Carved-Out Business - please reach out to our Director Stephan Plein.

This article delves into a three-step approach to portfolio optimization by harnessing the power of advanced data analytics and state-of-the-art quantitative models and tools.

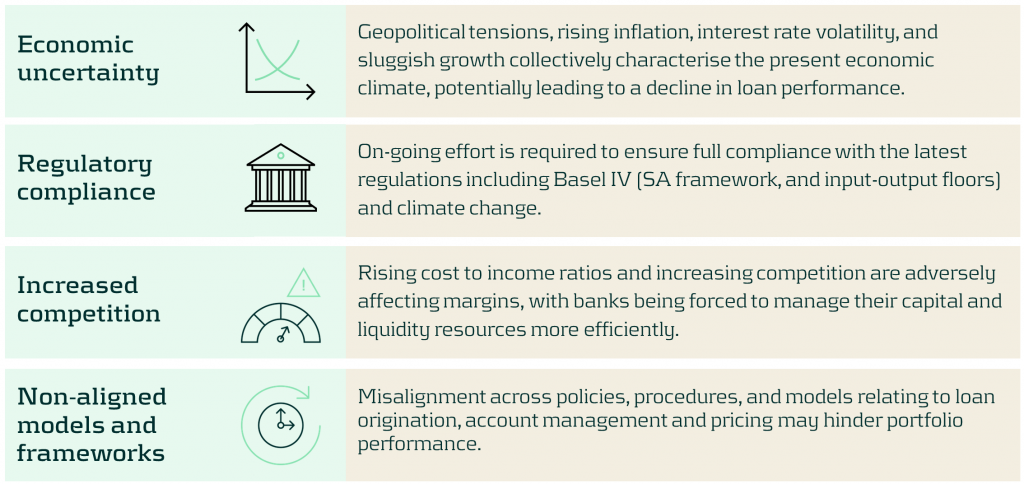

In today's dynamic economic landscape, optimizing portfolio composition to fortify against challenges such as inflation, slower growth, and geopolitical tensions is ever more paramount. These factors can significantly influence consumer behavior and impact loan performance. Navigating this uncertain environment demands banks adeptly strike a delicate balance between managing credit risk and profitability.

Why does managing your risk reward matter?

Quantitative techniques are an essential tool to effectively optimize your portfolio’s risk reward profile, as this aspect is often based on inefficient approaches.

Existing models and procedures across the credit lifecycle, especially those relating to loan origination and account management, may not be optimized to accommodate current macro-economic challenges.

Figure 1: Credit lifecycle.

Current challenges facing banks

Some of the key challenges banks face when balancing credit risk and profitability include:

Our approach to optimizing your risk reward profile

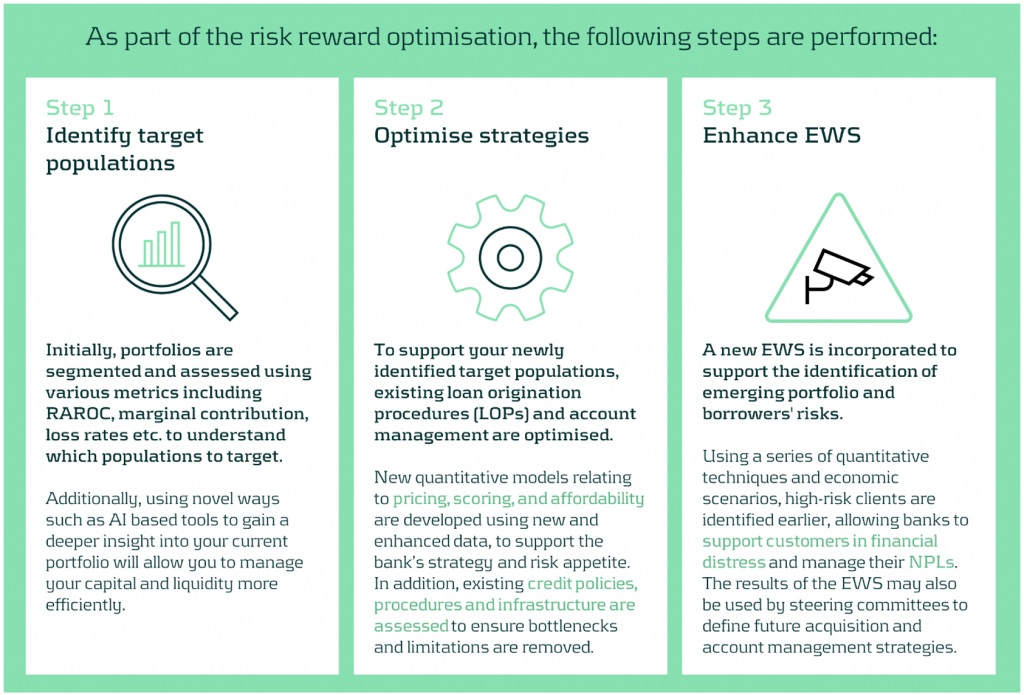

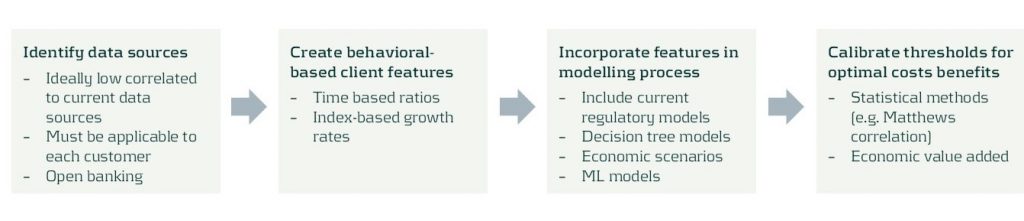

Our optimization approach consists of a holistic three step diagnosis of your current practices, to support your strategy and encourage alignment across business units and processes.

The initial step of the process involves understanding your current portfolio(s) by using a variety of segmentation methodologies and metrics. The second step implements the necessary changes once your primary target populations have been identified. This may include reassessing your models and strategies across the loan origination and account management processes. Finally, a new state-of-the-art Early Warning System (EWS) can be deployed to identify emerging risks and take pro-active action where necessary.

A closer look at redefining your target populations

With the proliferation of advanced data analytics, banks are now better positioned to identify profitable, low-risk segments. Machine Learning (ML) methodologies such as k-means clustering, neural networks, and Natural Language Processing (NLP) enable effective customer grouping, behavior forecasting, and market sentiment analysis.

Risk-based pricing remains critical for acquisition strategies, assessing segment sensitivity to different pricing strategies, to maximize revenue and reduce credit losses.

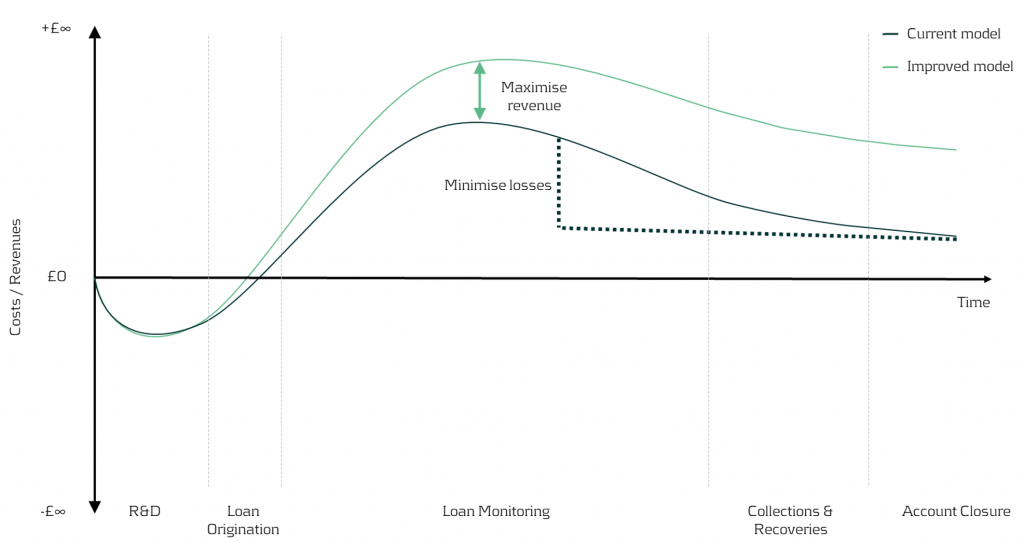

Figure 2: In the illustration above, we can visually see the impact on earnings throughout the credit lifecycle driven by redefining the target populations and application of different pricing strategies.

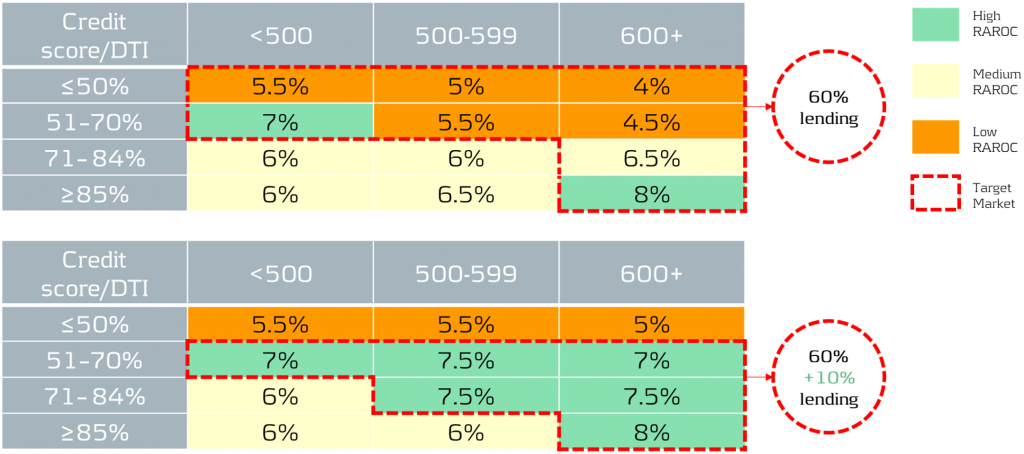

In our simplified example, based on the RAROC metric applied to an unsecured loans portfolio, we take a 2-step approach:

1- Identify target populations by comparing RAROC across different combinations of credit scores and debt-to-income (DTI) ratios. This helps identify the most capital efficient segments to target.

2- Assess the sensitivity of RAROC to different pricing strategies to find the optimal price points to maximize profit over a select period - in this scenario we use a 5-year time horizon.

Figure 3: The top table showcases the current portfolio mix and performance, while the bottom table illustrates the effects of adjusting the pricing and acquisition strategy. By redefining the target populations and changing the pricing strategy, it is possible to reallocate capital to the most profitable segments whilst maintaining within credit risk appetite. For example, 60% of current lending is towards a mix of low to high RAROC segments, but under the new proposed strategy, 70% of total capital is allocated to the highest RAROC segments.

Uncovering risks and seizing opportunities

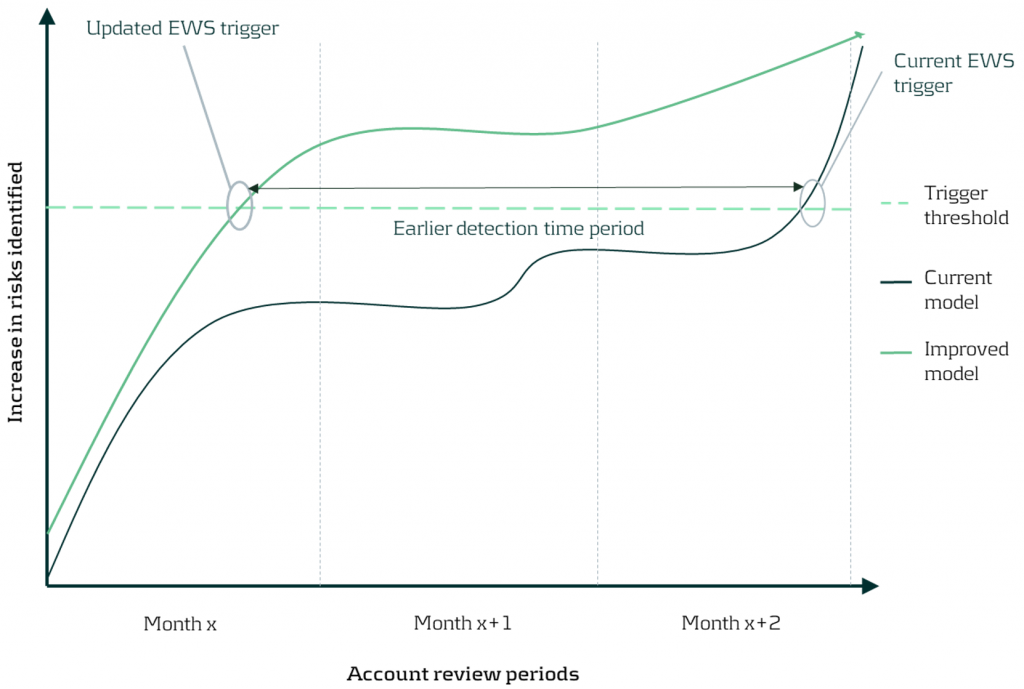

The current state of Early Warning Systems

Many organizations rely on regulatory models and standard risk triggers (e.g., no. of customers 30 day past due, NPL ratio etc.) to set their EWS thresholds. Whilst this may be a good starting point, traditional models and tools often miss timely deteriorations and valuable opportunities, as they typically use limited and/or outdated data features.

Target state of Early Warning Systems

Leveraging timely and relevant data, combined with next-generation AI and machine learning techniques, enables early identification of customer deterioration, resulting in prompt intervention and significantly lower impairment costs and NPL ratios.

Furthermore, an effective EWS framework empowers your organization to spot new growth areas, capitalize on cross-selling opportunities, and enhance existing strategies, driving significant benefits to your P&L.

Figure 4: By updating the early warning triggers using new timely data and advanced techniques, detection of customer deterioration can be greatly improved enabling firms to proactively support clients and enhance the firm’s financial position.

Discover the benefits of optimizing your portfolios

Discover the benefits in optimizing your portfolios’ risk-reward profile using our comprehensive approach as we turn today’s challenges into tomorrow’s advantages. Such benefits include:

Conclusion

In today's rapidly evolving market, the need for sophisticated credit risk portfolio management is ever more critical. With our comprehensive approach, banks are empowered to not merely weather economic uncertainties, but to thrive within them by striking the optimal risk-reward balance. Through leveraging advanced data analytics and deploying quantitative tools and models, we help institutions strategically position themselves for sustainable growth, and comply with increasing regulatory demands especially with the advent of Basel IV. Contact us to turn today’s challenges into tomorrow’s opportunities.

For more information on this topic, contact Martijn de Groot (Partner) or Paolo Vareschi (Director).