What does Taulia offer to clients using SAP?

Efficiently managing working capital becomes more and more important for corporates in the current challenging economic conditions and disruptions in the supply chain. As a result, the market has seen an increased demand for early payments of receivables from corporates. Managing working capital is essential in maintaining the health or even the survival of the business, especially in difficult economic times. Furthermore, efficient working capital management could benefit the growth of the company.

Working capital management includes the act of improving the cash conversion cycle. The cash conversion cycle expresses the length in days that it takes to convert cash outflow from purchasing supplies into cash inflow from sales. The cash conversion cycle (CCC) is defined as Days Sales (Receivable) Outstanding + Days Inventory Outstanding – Days Payables Outstanding (CCC = DSO + DIO – DPO). Decreasing DSO and DIO and increasing DPO lowers the cash conversion cycle, accelerates cash flow and improves a company’s liquidity position.

What is Supply Chain Finance?

The most popular method to manage working capital efficiently is using Supply Chain Finance (SCF). We distinguish the following SCF solutions:

- Static discounting: Option for the buyer (using the buyer’s own funds) to get a discount on the invoice if it is paid early. If the option is used, the supplier receives its money earlier than the due date. The discount for the supplier is determined upfront and fixed for a specific number of days.

- Dynamic Discounting: Similar to static discounting using the buyer’s own funds. The difference is that the discount rate is not fixed for a specific number of days. The buyer decides when it wants to pay the invoice. The earlier the invoice is paid, the higher the discount will be.

- Factoring: The supplier is selling its account receivables to a third party. The funding party pays the invoices early (i.e. well before the due date) to the supplier, benefiting the supplier. The interest paid on this solution is based on the credit rating of the supplier.

- Reverse Factoring: The buyer offers the supplier the opportunity to sell its receivables on its SCF platform, so the supplier will receive its money earlier than the due date (from the SCF party). This benefits both the supplier and the buyer, as the buyer will try to extend payment terms with the supplier and therefore pay later than the original due date.

An SCF program is financed by a third-party funder, which is usually a bank or an investing company. Additionally, SCF is often facilitated by technology to facilitate the selling of the supplier’s receivable in an automated fashion.

Reverse factoring

An example of reverse factoring is an automobile manufacturer that is buying various automobile parts from various suppliers. The automobile manufacturer will use a reverse factoring solution to pay the part suppliers earlier and extend the payment terms with these suppliers. Reverse factoring works best when the buyer has a better credit rating than the seller, as the costs of receiving the payment in advance is based on the credit rating of the buyer (which is higher than the credit rating of the seller), the seller receives funding at a more favorable rate than it would receive in the external capital market. This advantage gives the buyer the opportunity to negotiate better payment terms with the seller (higher DPO), while the seller could receive payments of the sale transaction in advance (lower DSO), decreasing the cash conversion cycle of both parties. Effectively, reverse factoring encourages collaboration between the buyer and the seller and potentially leads to a true win-win between buyers and suppliers. The buyer succeeds in its desire to delay payments, while the seller will be satisfied with advanced payments. However, the win for the supplier depends on how the costs of the program are split between the corporate (buyer) and its supplier. Usually, the costs are borne solely by the supplier. Therefore, the program is only desirable for a supplier if the program costs (interest to pay on the SCF funding based on the buyer’s credit rating and the program fee) is lower than the opportunity costs of the supplier. The opportunity costs are defined as the costs of lending funds against an interest rate which is based on its own credit rating.

Benefits and Risks

The benefits of SCF are the following:

- Suppliers can control their incoming cash flows with prepayment of invoices;

- Quick access to funding for the supplier in case of a liquidity crisis;

- Buyer-seller relationship is strengthened due to the collaboration in an SCF program;

- Reduced need of traditional (trade) finance;

- With reverse factoring, the buyer can negotiate extended payment terms with the supplier, providing the prepayment option to the supplier;

- With reverse factoring, suppliers have access to funding with lower interest rates as the pricing of the financing is based on the buyer’s credit rating.

Supply Chain Finance also has risks:

- Reporting ambiguity: Although corporates are obliged under IFRS to disclose additional information about their SCF arrangements (such as Terms and Conditions and carrying amounts of liabilities that are part of the SCF program), reverse factoring can mask true overall debt levels for the supplier when significant amounts of factoring does not have to be classified as debt but as trade payables. Accounting principles IFRS and US GAAP are regularly updated to reflect the latest guidelines around the classification of SCF programs as either trade payables or debt.

- Dependency on SCF: If the SCF program is of a substantial size, a withdrawal of the SCF facility can have dramatic consequences for liquidity and create terminal collateral damage through the supplier network. The US securities regulators warn that reverse factoring is not cycle-tested, which means that it is unclear what might happen in an economic downturn. However, a multi-funder structure makes it easy to replace or add funders in case of a facility withdrawal without disruption to suppliers.

What is Taulia?

Zanders sees a lot of movement in the SCF market. One interesting development is the acquisition of Taulia by SAP. Taulia is a leading supply chain software provider founded in 2009 with over 2 million business users. The rationale behind this acquisition is to expand SAP’s business network further and strengthen the SAP solutions in the financial area. The takeover of Taulia is understandable as more than 80% of the customer base of Taulia runs SAP as their ERP system. Taulia will both be tightly integrated into the SAP software as well as continue to be available as a standalone solution. It will operate as an independent company with its own brand within the SAP Group. Unique in the software business is that Taulia earns a percentage fee of each prepaid invoice that flows through the platform, instead of a fixed fee per transaction or a monthly fee, which is what we usually observe in the market of software vendors. When an invoice is selected for prepayment, the vendor receives a lower amount than the amount of the original invoice. The difference between these amounts is partly compensation for the investor and partly income for Taulia. Taulia offers solutions for all SCF options mentioned earlier: static discounting, dynamic discounting, factoring, and reverse factoring. It is a multi-funder platform on which any and as many banks as desired can be engaged, including the relationship banks of a corporate.

Supply Chain Finance Example

Original situation

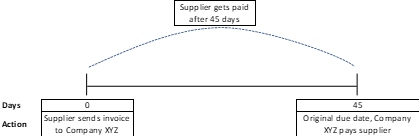

In this example, the supplier and Company XYZ have a payment term of 45 days in place. This is the ‘original situation’:

Payment term extension (optional)

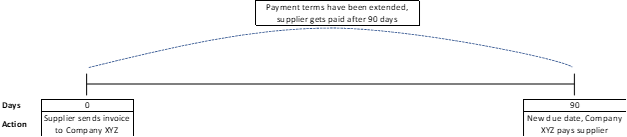

Company XYZ starts negotiations with the supplier to extend the payment terms. They agree on a new payment term of 90 days. This step is optional.

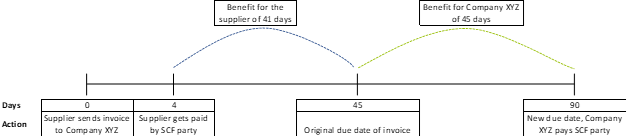

Supplier joins SCF program

The supplier joins the SCF program. Due to the SCF program, the supplier benefits from early payment. The interest that the supplier needs to pay is based on the (strong) credit rating of Company XYZ. In other words, the supplier can finance at lower interest rates.

Features of a Supply Chain Finance program

The features of a best practice SCF program such as Taulia are the following:

- A self-service portal with the branding of your company is provided to your suppliers. Suppliers can be onboarded on this portal, where they select invoices that they would like to receive in advance. When selecting an invoice, the supplier will be quoted with the prepayment costs immediately.

- Automated and near real-time integration with your ERP system, ensuring manual adjustments are redundant and data integrity is maintained. Integration is possible via multiple connectivity solutions or middleware applications. The integration of Taulia with SAP ERP is fully automated. Taulia has its own name space within SAP, although there are no changes in the core SAP code. In this name space, it is amongst others possible to run reconciliation reports. For more information about integration of a SCF platform to SAP, please read this article that we published earlier this year.

- Automatic netting of credit notes against future early payments or block early payments when a credit note is outstanding.

- Leverage real-time private and public data with machine learning in a dashboard to track performance and to make informed decision on your SCF program. This could include scenario analysis of different SCF rates and the effect on adoption rate of your suppliers. Additionally, the dashboard provides benchmarking of payment terms to industry standards.

- Automated solution to automatically accept early payments for suppliers (called ‘CashFlow’ in the Taulia solution). This solution will accept the early payment automatically if the discount is better or equivalent to a pre-set rate curve.

Accounts Receivable solution

Next to the reversed factoring solution, Taulia offers a solution for accounts receivable (AR) financing, also known as factoring. This solution works slightly differently than the reversed factoring solution as your customers do not need to be onboarded on the platform. AR invoices can be sold to a third-party funder, who pays the face value of the invoice less the proposed discount. The actual AR invoice payment from the buyer at maturity date will be collected in a collection account and send back to the investor.

To conclude

The ultimate goal of an SCF program is to unlock working capital for your company. With the choice for an appropriate SCF solution, and a successful implementation including integration to your ERP, the benefits of an SCF program can be achieved. Taulia could be the appropriate solution for you.

If you would like to know more about Supply Chain Finance and/or SAP Taulia, contact Mart Menger at +31 88 991 02 00.

Learning to manage sustainability risks has been one of the key challenges for financial organizations.

This topic is gaining momentum because of the European Commission’s Sustainable Finance Action Plan and associated regulatory changes.

One of the new requirements is that asset managers must incorporate sustainability risks in their risk management and reporting as of August 2022. This means that these risks must be measured, assessed and mitigated. However, this is not an easy task due to a lack of uniformity in risk management approaches and lagging data quality.

This prompted AF Advisors and Zanders to organize a round-table session on the subject. The large session turnout showed the importance of managing sustainability risks for the asset management sector. Parties that manage a total of no less than EUR 2.5 trillion in assets joined the session, including a broad selection of the largest asset managers active in the Netherlands. This attendance led to good, in-depth discussions. The discussion was preceded and inspired by a presentation from one of the expertized asset managers in the field of sustainability on how they mitigate, assess and monitor sustainability risks. Two hours of lively discussion is difficult to summarize but we would like to share a few interesting takeaways. Note that these takeaways do not necessarily represent the views of all the participants, though are merely an overview of the topics that were discussed.

Key takeaways

Financial risk management departments increasingly in the lead

While a few years ago, sustainability risks and the management of these risks were still the task of responsible investing teams in many organizations, this task is increasingly being taken up by financial risk managing departments as these are increasingly capable to quantify sustainability risks. This shift leads to new techniques and new requirements for data. Where previously exclusions were an important method for many parties, an integrated portfolio approach is emerging.

Lack of uniformity in the assessment of sustainability risks

The two main problems in managing sustainability risks are a lack of uniformity in approaches and a limited data quality or availability. Limited data quality is a well-known topic, especially for alternative asset classes. Specialized data vendors will be required to address these issues.

Important to realize, however, is that sustainability risk is such a broad and young concept that it is open to many interpretations. This means that the way in which sustainability risks are assessed can still differ considerably between parties. The benefit is that the different approaches help to speed up the evolvement of this new area. In the longer term it is expected that the assessments converge to a best market practice. Until then, there will be little standardization and different use of terminology. This is especially problematic in a multi-client environment with varying clients’ needs. Enforced communication by the regulator can therefore lead to outcomes that are hard to compare and interpret for clients. Listing definitions used and an explanation of the methodologies used is vital in communication on sustainability risks to clients.

ESG risk ratings are most popular concept despite drawbacks

The most frequently mentioned way in which sustainability risks are monitored is by means of environmental, social and governance (ESG) risk ratings. For example, by comparing a portfolio’s ESG scores with the scores of a corresponding benchmark and by limiting deviations. By using these ratings, environmental, social and governance factors are included. The major drawback of this approach is that it is partly backward-looking. Participants agreed, due to the long horizon over which most risks materialize, traditional (backward-looking) risk models may not be the most suited.

Most forward-looking data is available for climate risks. In addition to the use of ESG scores, a climate risk methodology is therefore desirable.

Not only European legislation matters

Next to European regulation, it is also important to consider emerging global initiatives and other regulation and reporting frameworks. US regulations such as US SDR can impact organizations and the approaches to sustainability risks to some extent. Global initiatives such as TCFD and TNFD are likely to influence and affect organizations’ risk management processes as well. Potential overlap must be analyzed so that an asset managers can face the challenges efficiently.

Internal organization

Sustainability risks can be defined and monitored at various levels of an organization. Portfolio managers should take them into account in the selection of investments. Second line monitoring and independent assessments must be in place. It is important to realize that this is not a topic that only affects the investment and risk management teams. The legislation explicitly places responsibility for managing sustainability risks on the board level and requires internal reporting, controls and sufficient internal knowledge of the topic.

Conclusion

Sustainability risk management is an important topic that asset managers will need to be working on in the coming years. It is expected that this field will evolve over time, it was even referred to as a ‘journey’. The deadline of MiFID, AIFMD and UCITS in August 2022 – date on which amendments of these regulations to incorporate sustainability risks come into effect – is an important first regulatory milestone but will certainly not be the last. With the organization of the round table, we hope to have assisted parties in getting a better understanding of the topic and to have contributed to their journey.

Financial institutions (FIs) play an important role in the transition towards a more sustainable economy in which Environmental, Social and Governance (ESG) factors are properly addressed.

But to seize the opportunities ESG must become an integrated part of a bank’s strategy, risk management and disclosure regimes. High-quality data is instrumental to identify and measure ESG risks, but it can be lacking. FIs need to improve their internal data and use of external private and public vendors like Moody’s or the IMF, while developing a framework that plugs any data gaps.

The lack of appropriate ESG data is considered one of the main challenges for many FIs, but proxies, such as using a building’s energy rating to work out its carbon emissions, can be used.

FIs need climate change-related data that isn’t always available if you don’t know where to look. This article will give you an overview of the most relevant data vendors and provide suggestions on how to treat missing data gaps in order to get a comprehensive ESG framework for the green future where carbon measurement, assessment, reporting and trading will be vital

The data challenge

In May 2021, the Network for Greening the Financial System (NGFS) published a ‘Progress report on bridging data gaps’. In this report, the NGFS writes that meeting climate-related data needs is a challenge that can be described along the following three dimensions:

- data availability,

- reliability,

- & comparability.

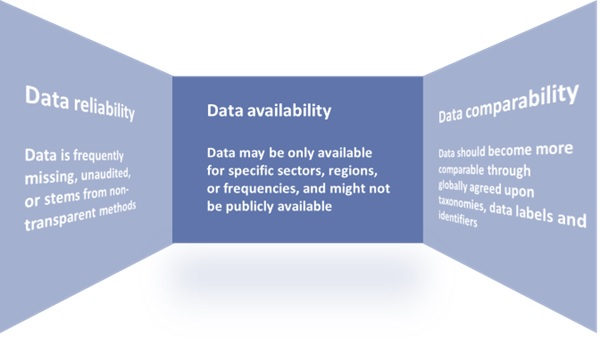

A further breakdown of the challenges related to these dimensions can be found in Figure 1.

Figure 1: The dimensions of the climate-related data challenge.

Source: Graphic adapted by Zanders from a NGFS report entitled: ‘Progress report on bridging data gaps’ (2021).

Key financial metrics

The NGFS writes that a mix of policy interventions is necessary to ensure climate-related data is based on three building blocks:

- Common and consistent global disclosure standards.

- A minimally accepted global taxonomy.

- Consistent metrics, labels, and methodological standards.

EU Taxonomy, CSRD & EBA’s 3 ESG risk disclosure standards

Several initiatives have started to ignite these needed policy interventions. For example, the EU Taxonomy, introduced by the European Commission (EC), is a classification system for environmentally sustainable activities. In addition, the recently approved Corporate Sustainability Reporting Directive (CSRD) provides ESG reporting rules for large listed and non-listed companies in the EU, including several FIs. The aim of the CSRD is to prevent greenwashing and to provide the basis for global sustainability reporting standards. Another example of a disclosure standard is the binding standards on Pillar 3 disclosures on ESG risks developed by the European Banking Authority (EBA).

Even though policy, law and regulation makers have a big part to play in the data challenge, there are also steps that individual institutions could and should take to improve their own ESG data gaps. Regulatory bodies such as the EBA and the European Central Bank (ECB) have shared their expectations and recommendations on the management of ESG data with FIs.

To illustrate, the EBA recommends FIs “[identify] the gaps they are facing in terms of data and methodologies and take remedial action” and the ECB expects institutions to “assess their data needs in order to inform their strategy-setting and risk management, to identify the gaps compared with current data and to devise a plan to overcome these gaps and tackle any insufficiencies”

Collecting data

Collecting ESG data is a challenging exercise. A distinction can be made between collecting data for large market cap companies, and small cap companies and retail clients. Although large cap companies tend to be more transparent, the data often is dispersed over multiple reports – for example, corporate sustainability reports, annual reports, emissions disclosures, company websites, and so on.

For small cap companies and retail clients, the data is more difficult to acquire. Data that is not publicly available could be gathered bilaterally from clients. For example, one European bank has developed an annual client questionnaire to collect data from its clients.

Gathering data from various reports or bilaterally from clients might not always be the best option, however, because it is time consuming or because the data is not available, reliable, or comparable. Two alternatives are:

- Use tools to collect the data. For example, using open-source tooling from the Two Degrees Investing Initiative (2DII) to calculate Paris Agreement Capital Transition Assessment (PACTA) portfolio alignment.

- Collect data from other external data sources, such as S&P Global.

This could be forward-looking external data on macro-economic expectations, international climate scenarios, financial market data or sectoral climate developments. Below we discuss some sources for external ESG and climate change-related data.

External data

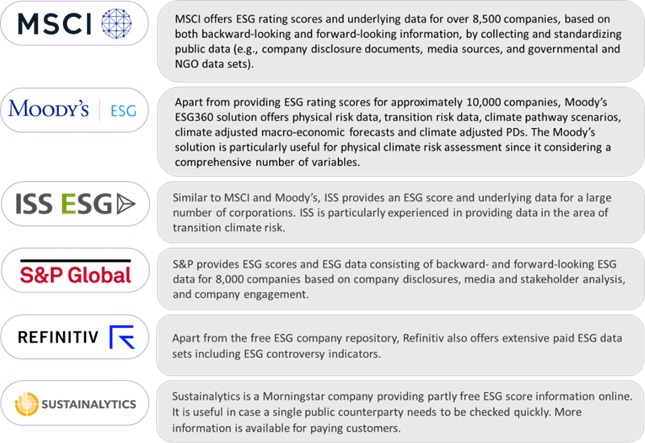

Some of Zanders’ clients resort to vendor solutions for acquiring their ESG data. The most commonly observed solutions, in random order, are:

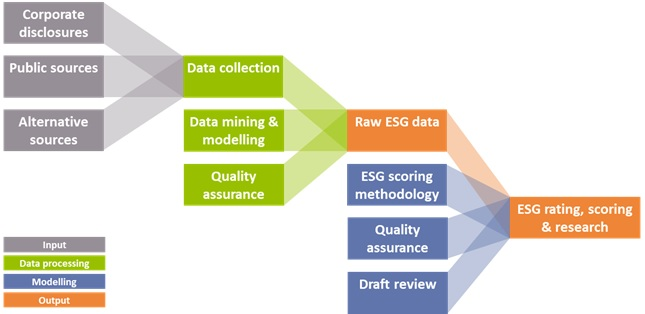

All the solutions above provide an aid to determine if climate related performance data is lacking, or can assist in reporting comparable and reliable data. They all apply a similar process of collecting the data and determining ESG scores, which is illustrated in Figure 2.

Figure 2: Data collection process for ESG data solutions (Source: Zanders).

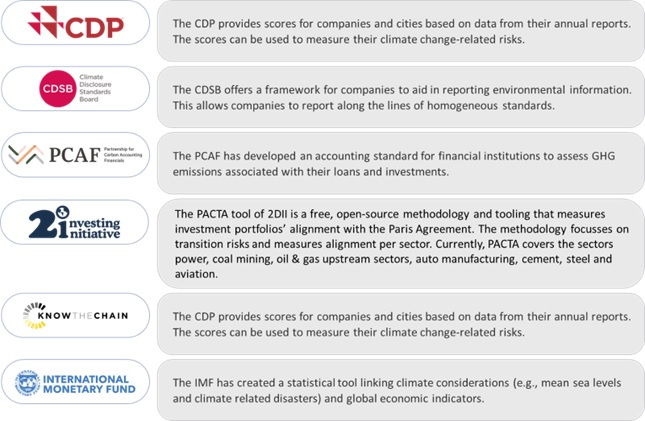

Additionally, public and non-commercial data and solution providers are available, such as:

Missing data

Given the data challenges, it is nearly impossible to create a complete data set. Until that is possible, there are several (temporary) methods to deal with missing data:

- Find a comparable loan, asset, or company for which the required data is available.

- Distribute sector data based on market share of individual companies. For example, assign 10% of the estimated emission of sector X to company Y based on its market share of 10%.

- Find a proxy, comparable or second-best metric. For example, by taking the energy label as a proxy for CO2 emission related to properties, or by excluding scope 3 emissions and focusing on scope 1 and 2 emissions.

- Change the granularity level. For example, by gathering data on sector level rather than on individual positions.

- Fill in the gaps with statistical or machine learning techniques.

Conclusion

The increased attention to integrating ESG risks into existing risk frameworks has led to a need for FIs to collect and disclose meaningful data on ESG factors. However, there is still a lack of data availability, reliability, and comparability.

Several regulatory and political efforts are ongoing to tackle this data challenge, such as the EU taxonomy. More policy interventions, however, are required. Examples are additional mandatory disclosure requirements, an audit and validation framework for ESG data, and social and governance taxonomies that classify economic activities that contribute to social and governance goals.

In the meantime, FIs have to find ways to produce meaningful insights and comply with regulatory requirements related to ESG risks. Zanders has experienced that there is no one-size-fits-all solution for defining, selecting, implementing, and disclosing relevant data and metrics. It is dependent on the composition of the asset and loan portfolio, the use of the data, and the data that is (already) available. Regardless of how the lack of data is solved, it is important that FIs are transparent about their choices and methodologies, and that the related metrics and scorings are explainable and intuitive.

Sources:

https://www.ngfs.net/sites/default/files/medias/documents/progress_report_on_bridging_data_gaps.pdf

https://ec.europa.eu/info/business-economy-euro/banking-and-finance/sustainable-finance/eu-taxonomy-sustainable-activities_en

https://www.europarl.europa.eu/news/en/press-room/20220620IPR33413/new-social-and-environmental-reporting-rules-for-large-companies

https://zandersgroup.com/en/insights/blog/ebas-binding-standards-on-pillar-3-disclosures-on-esg-risks

https://www.eba.europa.eu/sites/default/documents/files/document_library/Publications/Reports/2021/1015656/EBA%20Report%20on%20ESG%20risks%20management%20and%20supervision.pdf

https://www.bankingsupervision.europa.eu/ecb/pub/pdf/ssm.202011finalguideonclimate-relatedandenvironmentalrisks~58213f6564.en.pdf

https://2degrees-investing.org/resource/pacta/

On Friday 8 July, the European Central Bank (ECB) published the results of the climate risk stress test that was performed in the first half of this year.

In total 104 banks participated in the stress test that was intended as a learning exercise, for the ECB and the participating banks alike. In this article we provide a brief overview of the main results.

The ECB’s goal with the climate risk stress test was to assess the progress banks have made in developing climate risk stress-testing frameworks and the corresponding projections, as well as understanding the exposures of banks with respect to both transition and physical climate change risks. The stress test therefore consisted of three modules: 1) a qualitative questionnaire to assess the bank’s climate risk stress testing capabilities, 2) two climate risk metrics showing the sensitivity of the banks’ income to transition risk and their exposure to carbon emission-intensive industries, and 3) constrained bottom-up stress test projections for four scenarios specified by the ECB1. The third module only had to be completed by 41 directly supervised banks to limit the burden for some of the smaller banks included in the climate risk stress test.

An understatement of the true risk

The constrained bottom-up stress test projections show that the combined market and credit risk losses for the 41 banks in the sample amount to approximately EUR 70 billion in the short-term disorderly transition scenario. The ECB emphasizes that this probably is an understatement of the true risk, because it does not consider the scenarios underlying the stress test to be ‘adverse’. Second round economic effects from climate risk changes have, for example, not been factored in. Furthermore, only a third of the total exposures of the 41 banks were in scope and, on top of that, the ECB considers the banks’ modeling capabilities to be ‘rudimentary’ in this stage: they report that around 60% of the banks do not yet have a well-integrated climate risk stress testing framework in place, and they expect that it will take several years before banks achieve this. Even though banks are not meeting the ECB’s expectations yet, the ECB does conclude that banks have made considerable progress with respect to their climate stress testing capabilities.

Be aware of clients’ transition plans

A further analysis of the results shows that the share of interest income related to the 22 most carbon-intensive industries amounts to more than 60% of the total non-financial corporate interest income (on average for the banks in the sample). Interestingly, this is higher than the share of these sectors (around 54%) in the EU economy in terms of gross added value. The ECB argues that banks should be very much aware of the transition plans of their clients to manage potential future transition risks in their portfolio. The exposure to physical risks is much more varied across the sample of banks. It primarily depends on the geographical location of their lending portfolios’ assets.

The ECB points out that only a few banks account for climate risk in their credit risk models. In many cases, the credit risk parameters are fairly insensitive to the climate change scenarios used in the stress test. They also report that only one in five banks factor climate risk into their loan origination processes. A final point of attention is data availability. In many cases, proxies instead of actual counterparty data have been used to measure (for example) greenhouse gas emissions, especially for Scope 3. Consequently, the ECB is also promoting a higher level of customer engagement to improve in this area.

Many deficiencies, data gaps and inconsistencies

The outcome of the climate risk stress test will not have direct implications for a bank’s capital requirements, but it will be considered from a qualitative point of view as part of the Supervisory Review and Evaluation Process (SREP). This will be complemented by the results from the ongoing thematic review that is focused on the way banks consider climate-related and environmental risks into their risk management frameworks. The combination will indicate to the ECB how well a bank is meeting the expectations laid down in the ‘Guide on climate-related and environmental risks’ that was published by the ECB in November 2020.

The ECB notes that the exercise revealed many deficiencies, data gaps and inconsistencies across institutions and expects banks to make substantial further progress in the coming years. Furthermore, the ECB concludes that banks need to increase customer engagement to obtain relevant company-level information on greenhouse gas emissions, as well as to invest further in the methodological assumptions that are used to arrive at proxies.

If you are looking for support with the integration of Environmental, Social, and Governance risk factors into your existing risk frameworks, please reach out to us.

Notes

1) See our earlier article on the ECB’s climate stress test methodology for more details.

On Thursday 9 June, we hosted a roundtable in our head office in Utrecht titled ’Integrating ESG risks into a bank’s credit risk framework’. The roundtable was attended by credit and climate risk managers, as well as model validators, working for Dutch banks of different sizes. In this article we briefly describe Zanders’ view on this topic and share the key insights of the roundtable.

The last three to four years have seen a rapid increase in the number of publications and guidance from regulators and industry bodies. Environmental risk is currently receiving the most attention, triggered by the alarming reports from the Intergovernmental Panel on Climate Change (IPCC). These reports show that it is a formidable, global challenge to shift to a sustainable economy in order to reduce environmental impact.

Zanders’ view

Zanders believes that banks have an important role to play in this transition. Banks can provide financing to corporates and households to help them mitigate or adapt to climate change, and they can support the development of new products such as sustainability-linked derivatives. At the same time, banks need to integrate ESG risk factors into their existing risk processes to prepare for the new risks that may arise in the future. Banks and regulators so far have mostly focused on credit risk.

We believe that the nature and materiality of ESG risks for the bank and its counterparties should be fully understood, before making appropriate adjustments to risk models such as rating, pricing, and capital models. This assessment allows ESG risks to be appropriately integrated into the credit risk framework. To perform this assessment, banks may consider the following four steps:

- Step 1: Identification. A bank can identify the possible transmission channels via which ESG risk factors can impact the credit risk profile of the bank. This can be through direct exposures, or indirectly via the credit risk profile of the bank’s counterparties. This can for example be done on portfolio or sector level.

- Step 2: Materiality. The materiality of the identified ESG risk factors can be assessed by assigning them scores on impact and likelihood. This process can be supported by identifying (quantitative) internal and external sources from the Network for Greening the Financial System (NGFS), governmental bodies, or ESG data providers.

- Step 3: Metrics. For the material ESG risk factors, relevant and feasible metrics may be identified. By setting limits in line with the Risk Appetite Statement (RAS) of the bank, or in line with external benchmarks (e.g., a climate science-based emission path that follows the Paris Agreement), the exposure can be managed.

- Step 4: Verification. Because of the many qualitative aspects of the aforementioned steps, it is important to verify the outcomes of the assessment with portfolio and credit risk experts.

Key insights

Prior to the roundtable, Zanders performed a survey to understand the progress that Dutch banks are marking with the integration of ESG risks into their credit risk framework, and the challenges they are facing.

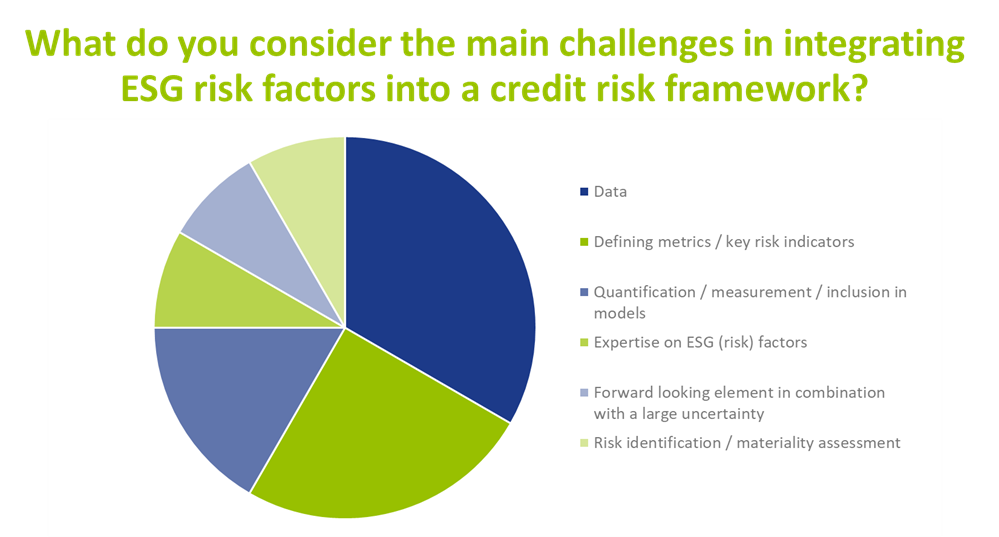

Currently, when it comes to incorporating ESG risks in the credit risk framework, banks are mainly focusing their attention on risk identification, the materiality assessment, risk metric definition and disclosures. The survey also reveals that the level of maturity with respect to ESG risk mitigation and risk limits differs significantly per bank. Nevertheless, the participating banks agreed that within one to three years, ESG risk factors are expected to be integrated in the key credit risk management processes, such as risk appetite setting, loan origination, pricing, and credit risk modeling. Data availability, defining metrics and the quantification of ESG risks were identified by banks as key challenges when integrating ESG in credit risk processes, as illustrated in the graph below.

In addition to the challenges mentioned above, discussion between participating banks revealed the following insights:

- Insight 1: Focus of ESG initiatives is on environmental factors. Most banks have started integrating environmental factors into their credit risk management processes. In contrast, efforts for integrating social and governance factors are far less advanced. Participants in the roundtable agreed that progress still has to be made in the area of data, definitions, and guidelines, before social and governance factors can be incorporated in a way that is similar to the approach for environmental factors.

- Insight 2: ESG adjustments to risk models may lead to double counting. The financial market still needs to gain more understanding to what extent ESG risk factor will manifest itself via existing risk drivers. For example, ESG factors such as energy label or flood risk may already be reflected in market prices for residential real estate. In that case, these ESG factors will automatically manifest itself via the existing LGD models and separate model adjustments for ESG may lead to double counting of ESG impact. Research so far shows mixed signals on this. For example, an analysis of housing prices by researchers from Tilburg University in 2021 has shown that there is indeed a price difference between similar houses with different energy labels. On the other hand, no unambiguous pricing differentiation was found as part of a historical house price analysis by economists from ABN AMRO in 2022 between similar houses with different flood risks. Participating banks agreed that further research and guidance from banks and the regulators is necessary on this topic.

- Insight 3: ESG factors may be incorporated in pricing. An outcome of incorporating ESG in a credit risk framework could be that price differentiation is introduced between loans that face high versus low climate risk. For example, consideration could be given to charging higher rates to corporates in polluting sectors or ones without an adequate plan to deal with the effects of climate change. Or to charge higher rates for residential mortgages with a low energy label or for the ones that are located in a flood-prone area. Participating banks agreed that in theory, price differentiation makes sense and most of them are investigating this option as a risk mitigating strategy. Nevertheless, some participants noted that, even if they would be able to perfectly quantify these risks in terms of price add-ons, they were not sure if and how (e.g., for which risk drivers and which portfolios) they would implement this. Other mitigating measures are also available, such as providing construction deposits to clients for making their homes more sustainable.

Conclusion

Most participating banks have made efforts to include ESG risk factors in their credit risk management processes. Nevertheless, many efforts are still required to comply with all regulatory expectations regarding this topic. Not only efforts by the banks themselves but also from researchers, regulators, and the financial market in general.

Zanders has already supported several banks and asset managers with the challenges related to integrating ESG risks into the risk organization. If you are interested in discussing how we can help your organization, please reach out to Sjoerd Blijlevens or Marije Wiersma.

We are very delighted that our client Sony Group Corporation has been awarded winner of an Adam Smith Award in the category of ‘Best Treasury Transformation project’.

The winners’ announcements of the 2022 Adam Smith Awards took place on 12 May in London. On that date Hiroyuki Ishiguro, Gurmeet Jhita and Terry Vouvoudakis, on behalf of their teams, were announced as the winners of this prestigious award.

On 14 June, during the Awards dinner, the award was physically presented to Hiroyuki Ishiguro and Gurmeet Jhita, who were leading Sony’s global treasury transformation project, which started in 2018. Judith van Paassen received the award on behalf of Zanders. Zanders was one of the eight partners named during the announcement, together with SAP, MUFG, SMBC, J.P. Morgan, Citi, HSBC and 360T.

The Adam Smith Awards are now in their 15th year and are recognized across the world as the ultimate benchmark of corporate achievement and exceptional solutions in treasury. The standard of submissions this year was of the very highest level, with 230 nominations spanning 34 countries. A list of all Adam Smith award winners can be found here on the Treasury Today website.

Over the course of the 2022 Adam Smith Awards season, Treasury Today will host a dedicated podcast series, case study series and social media celebration of this year’s winning projects.

Foto: Adam Smith Award winners for Best Treasury Transformation Project. From left to right: Vitantonio Musa, Lee Titchmarsh, Gurmeet Jhita, Laura Koekkoek, Hiroyuki Ishiguro, Judith van Paassen, Beliz Ayhan, Fred Pretorius

With SAP recently focusing heavily on developing its S/4HANA Cloud solutions, now is an opportune time for corporate executives to investigate the deployment options and weigh up the investment versus the benefit of each.

Changing IT infrastructure and systems is costly, and executives need the right knowledge to make informed decisions to best meet their current and future demands at the optimal price point. What are the best options?

We will start by looking at the features of the various options before taking a deeper dive into what the differences are specifically for Treasury Management on SAP S/4HANA and how that might influence decisions.

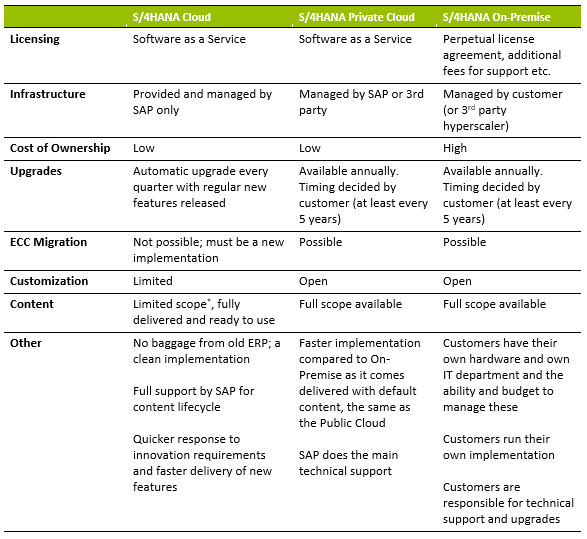

The main features are summarized in the table below:

*Scope covered should be sufficient for small to medium corporate treasuries, depending on complexity

Treasury Management on S/4HANA

In terms of selecting the right platform for treasury management on S/4HANA, there are many considerations, and the needs of each organization will differ. SAP has been working to ensure that the Public Cloud for Treasury Management has wider instrument coverage for corporate customers.

A development that could notably sway more corporates to consider the cloud-based options, is the inclusion of the new in-house banking component in the best practice offering from August 2022. In this module, which is embedded into Advanced Payment Management, SAP offers a completely rewritten solution, with advantages even over the traditional In-House Cash (IHC) module. IHC was previously not available to Public Cloud customers and this gap in the offering has no-doubt been a factor in customers deciding not to select the Public Cloud edition. These larger companies often need the payment functionalities available within IHC (such as payments on Behalf of, routing and internal transfers) and the lack of them is limiting. The addition of the in-house banking component makes for a more complete in-house bank functionality when paired with Advanced Payment Management (which is a prerequisite) and Treasury and Risk Management. This new in-house banking solution will also be made available to On-Premise customers during 2022 and with improved features and functionality, should be considered during upgrade decisions.

In Cash Management, S/4HANA Cloud comes standard with Basic Cash Management (Basic Bank Account Management and Basic Cash Operations). Advanced Cash Management, which delivers essentially the same as the On-Premise edition, barring one or two smaller features, is available, although an additional license is required. Liquidity Planning is only available if a customer has an SAP Analytics Cloud license.

SAP Treasury & Risk Management (TRM) is where the most differences currently exist between the Public Cloud and the Private Cloud or On-Premise editions. The Public Cloud has less instruments that are supported, although SAP is continually adding to the list.

Looking at the other most notable differences per area in TRM, the impact of the following in respect of the Public Cloud version should be discussed further with the customer:

- Hedge management – Reference-based hedging is currently not supported.

- Risk analyzers – Portfolio Analyzer is not offered, and SAP has no plans to include it. This is not generally required by corporate treasuries, so should not be an issue if the Public Cloud is selected.

- Securities – the offering is limited, although SAP is working to bridge the gaps. Asset-backed and mortgage-backed securities will be available in the August 2022 release.

- Derivatives – only interest rate swaps and cross currency swaps are possible, with no option to configure your own instruments.

- Position management – limited due to the reduced scope of instruments available in the cloud.

- Treasury analytics – FX reporting in SAP Analytics Cloud is limited but is being improved and customers can expect FX Hedging Area reports to be available by early 2023.

Making the Choice

Based on the above, the Public Cloud option makes sense for new businesses or smaller organizations that do not have the budget or resources to implement and support a customized solution. It would also suit organizations that need their systems to be responsive to market changes. Content is delivered as-is from SAP with minimal customization options, however, the cost of ownership is lower. It should also be noted that currently the Public Cloud edition of S/4HANA has been configured with local requirements for 43 countries. No more countries will be added; however, SAP is working on a tool which will enable customers to copy an existing country and create the settings for an additional country. This feature should be released in 2023.

In terms of treasury management, the Public Cloud would suit organizations with a vanilla treasury function and those that are looking to do a completely new implementation with no need to migrate from an existing system. This option does, however, require what SAP calls a “cloud mindset”, where customers cannot expect the system to fit into their existing processes but instead should look at how their organizational requirements can be met by SAP’s standard offerings.

The On-Premise solution would better suit larger organizations with well-established IT infrastructure and resources, as well as businesses using a broad spectrum of financial instruments that require customization. The On-Premise solution gives the customer full control and maximum freedom in terms of content, configuration, and timings of upgrades although there is a higher cost of ownership.

An attractive choice in the treasury space particularly is the hybrid one, i.e., the Private Cloud. Here customers would outsource their infrastructure management to SAP or another third party, whilst still ensuring they have the flexibility of options around treasury management scope.

With the Private Cloud and On-Premise, customers can still make use of Best Practice content as an accelerator. This content is available online for download and contains the likes of Process Flow diagrams and Test Scripts, helping customers to save time in an implementation. The Cloud’s Starter system is also provided as a way to see content before needing to configure it, thereby allowing the customer to test functionality upfront.

Zanders has in-depth knowledge and experience of Treasury Management on SAP S/4HANA and can help customers to analyze their requirements and ensure they make the best selection between Public Cloud, Private Cloud and On-Premise, or even a combination of the options.

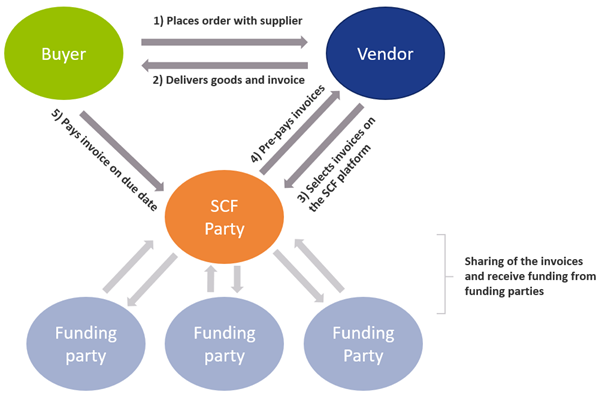

Vendor Supply Chain Finance (SCF) constitutes the transfer of a (trade) payable position towards the SCF underwriter (i.e. the bank). The beneficiary of the payment can then decide either to receive an invoice payment on due date or to receive the funds before, at the cost of a pre-determined fee.

The debtor’s bank account will only be debited on due date of the payable; hence the bank finances the differential between the due date and the actual payment date towards the beneficiary for this pre-determined fee. This article elaborates on why and how corporates set-up an SCF scheme with their suppliers.

The Vendor SCF construction can be depicted as:

There are multiple business rationales behind Supply Chain Finance. Why would a corporate want to setup an SCF scheme with its suppliers? The most prominent rationales are:

- Reduction of the need of more traditional trade finance

The need for individual line of credits and bank guarantees for each trade transaction is removed, making the trade process more efficient. - Sellers can flexibly and quickly fund short term financing needs

If working capital or financing is needed, the seller can quickly request for outstanding invoices to be paid out early (minus a fee). - Sharing the benefits of better credit rating from buyer towards seller

Because the financing is arranged by the buyer, the seller can enjoy the credit terms that were negotiated between buyer and financier/bank. - Streamlining the AP process

By onboarding various vendors into the SCF process, the buyer can enjoy a singular and streamlined payment process for these vendors. - Strengthening of trade relations

Because of the benefits of SCF, more competitive terms on the trade agreement itself can be negotiated.

SCF is typically considered a tool to improve the working capital position of a company, specifically to decrease the cash conversion cycle by increasing the payment terms with its suppliers without weakening the supply chain.

Set-up and onboarding

Typically, a set-up and onboarding process consists of the following steps. First a financing for SCF is obtained from, for example, a bank. In addition, an SCF provider must be selected and contracted. Most major banks have their own solutions but there are many third parties, for example fintechs, that provide solutions as well. Consequently, the SCF terms are negotiated, and the suppliers are onboarded to the SCF process. Lastly, your system should of course be able to process/register it. Therefore, the ERP accounts payable module needs to be adjusted, such that the AP positions eligible for SCF are interfaced into the SCF platform. Besides, your ERP system needs to be adjusted to be able to reconcile the SCF reports and bank statements.

Design considerations and Processing SCF in SAP

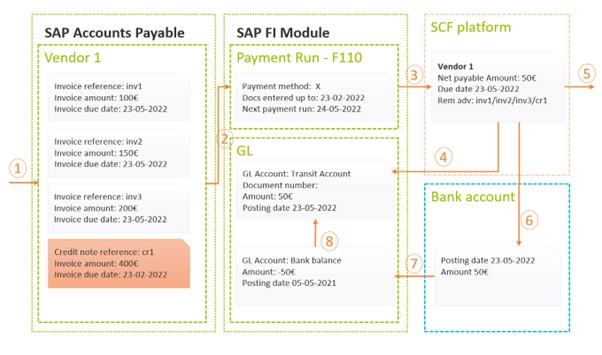

In the picture below we provide a high-level example of how a basic SCF process can work using basic modules in SAP. Note that, based on the design considerations and capabilities of the SCF provider, the picture may look a bit different. For each of the steps denoted by a number, we provide an explanation below the figure, going a little deeper into some of the possible considerations on which a decision must be made.

- Invoice and credit note data entry; In the first step, the invoices/credit notes will be entered, typically with payment terms sometime in the future, i.e. 90 days. Once entered and approved, these invoices are now available to the payment program.

- Payment run: The payment run needs to be engineered such that the invoices that are due in the future (i.e. 90 days from now) will be picked up already in today’s run. Some important considerations in this area are:

- Payment netting logic: the netting of invoices and credit notes is an important design consideration. Typically, credit notes are due immediate and the SCF invoices are due sometime in the future, i.e. 90 days from now. If one would decide to net a credit note due immediate with an invoice due in 90 days, this would have some adverse impact on working capital. An alternative is to exclude credit notes from being netted with SCF invoices and have them settled separately (i.e. request the vendor to pay it out separately or via a direct debit). Additionally, some SCF providers have certain netting logic embedded in their platform. In this case, the SAP netting logic should be fully disabled and all invoices should be paid out gross. Careful considerations should be taken when trying to reconcile the SCF settled items report as mentioned in step 4 though.

- Payment run posting: When executing the SAP payment run it is possible to either clear the underlying invoices on payment run date or to leave them open until invoice due date. If the invoices are kept open, they will be cleared once the SCF reporting is imported in SAP (see step 4). This is decision-driven by the accounting team and depends on where the open items should be rolling up in the balance sheet (i.e. payable against the vendor or payable against the SCF supplier).

- Payment file transfer: At this step, the payment file will be generated and sent to the SCF supplier. The design considerations are dependent on the SCF supplier’s capabilities and should be considered carefully while selecting an appropriate partner.

- File format: Most often we advise to implement a best practice payment file format like ISO pain.001. This format has a logical structure, is supported out of the box in SAP, while most SCF partners will support it too.

- Interface technology: The payment files need to be transferred into the SCF platform. This can be done via a multitude of ways; i.e. manual upload, automatically via SWIFT or Host2Host. This decision is often driven internally. Often the existing payment infrastructure can be leveraged for SCF payments as well.

- Remittance information: By following ISO pain.001 standard, the remittance information that remits which invoices are paid and cleared, can be provided in a structured format, irrespective of the volume of invoices that got cleared. This ensures that the beneficiary exactly knows which invoices were paid under this payment. Alternatively, an unstructured remittance can be provided but this often is limited to 140 characters maximum.

- Payment status reporting: Some SCF supplier will support some form of payment status reporting to provide immediate feedback on whether the payments were processed correctly. These reports can be imported in SAP; SAP can subsequently send notifications of payment errors to the key users who can then take corrective actions.

- SCF payment clearing reporting: At this step, the SCF platform will send back a report that contains information on all the cleared payments and underlying invoices for that specific due date. Most typically, these reports are imported in SAP to auto reconcile against the open items sitting in the administration.

- Auto import: If import of the statement into SAP is required, the report should be in one of SAP’s standard-supported formats like MT940 or CAMT.053.

- Auto reconciliation: If auto reconciliation of this report against line items in SAP is required, the reports line items should be matchable with the open line items in the SAP administration. Secondly, a pre-agreed identifier needs to be reported such that SAP can find the open item automatically (i.e. invoice reference, document number, end2endId, etc.). Very careful alignment is needed here, as slight differences in structure in the administration versus the reporting structure of SCF can lead to failed auto reconciliation and tedious manual post processing.

- Pay out to the beneficiary: Onboarded vendors can access the SCF platform and report on the pending payments and invoices. The vendor has the flexibility to have the invoices paid out early (before due date) by accepting the deduction of a pre-agreed fee. The SCF provider should ensure payment is made.

- Debiting bank account: At due date of the original invoice, the SCF provider will want to receive the funds.

- Payment initiation vs direct debit: The payment of funds can in principle be handled via two processes; either the SCF customer initiates the payment himself, or an agreement is made that the SCF provider direct debits the account automatically.

- Lump debit vs line items: Most typically, one would make a lump payment (or direct debit) of the total amount of all invoices due on that day. Some SCF providers may support line by line direct debiting although this might result in high transaction costs. Line by line debiting might be beneficial for the auto reconciliation process in SAP though (see step 7)

- Bank statement reporting: The bank statement of the cash account will be received and imported into SAP. Most often, the statements are received over the existing banking interface.

- Bank statement processing: Based on pre-configured posting rules and reconciliation algorithms in SAP, the open items in the administration are cleared and the bank balance is updated appropriately.

To conclude

If the appropriate SCF provider is selected and the process design and implementation in SAP is sound, the benefits of SCF can be achieved without introducing new processes and therefore creating a burden on the existing accounts payable team. It is fully possible to integrate the SCF processes with the regular accounts payable payments processes without adding additional manual process steps or cumbersome workarounds.

For more information, contact Ivo Postma at +31 88 991 02 00.

FRTB PLA’s catch-22: hedging, used to reduce a portfolio’s risk, may actually increase the likelihood of failing the PLA test.

Profit and loss attribution (PLA) is a critical component of FRTB’s internal models approach (IMA), ensuring alignment between Front Office (FO) and Risk models. The consequences of a PLA test failure can be severe, with desks forced to use the more punitive standardised approach (SA), resulting in a considerable increase in capital charges. The introduction of the PLA test has sparked controversy as it appears to disincentivise the use of hedging. Well-hedged portfolios, which reduce risk and variability in a portfolio's P&L, often find it more challenging to pass the PLA test compared to riskier, unhedged portfolios.

In this article, we dig deeper into the issues surrounding hedging with the PLA test and provide solutions to help improve the chances of passing the test.

The problem with performing PLA on hedged portfolios

The PLA test measures the compatibility of the risk theoretical P&L (RTPL), produced by Risk, with the hypothetical P&L (HPL) produced by the FO. This is achieved by measuring the Spearman correlation and Kolmogorov–Smirnov (KS) test statistic on 250 days of historical RTPLs and HPLs for each trading desk. Based on the results of these tests, desks are assigned a traffic light test (TLT) zone categorisation, defined below. The final PLA result is the worst TLT zone of the two tests.

| TLT Zone | Spearman Correlation | KS Test |

| Green | > 0.80 | < 0.09 |

| Amber | < 0.80 | > 0.09 |

| Red | < 0.70 | > 0.12 |

The impact of TLT zones

The impact of a desk’s PLA results depends on which TLT zone it has been assigned:

- Green zone: Desks are free to calculate their capital requirements using the IMA.

- Amber zone: Desks are required to pay a capital surcharge, which can lead to a considerable increase in their capital requirements.

- Red zone: Desks must calculate their capital requirements using the SA, which can lead to a significant increase in their capital.

Red and Amber desks must also satisfy 12-month backtesting exception requirements before they can return to the green zone.

Why are hedged portfolios more susceptible to failing the PLA test?

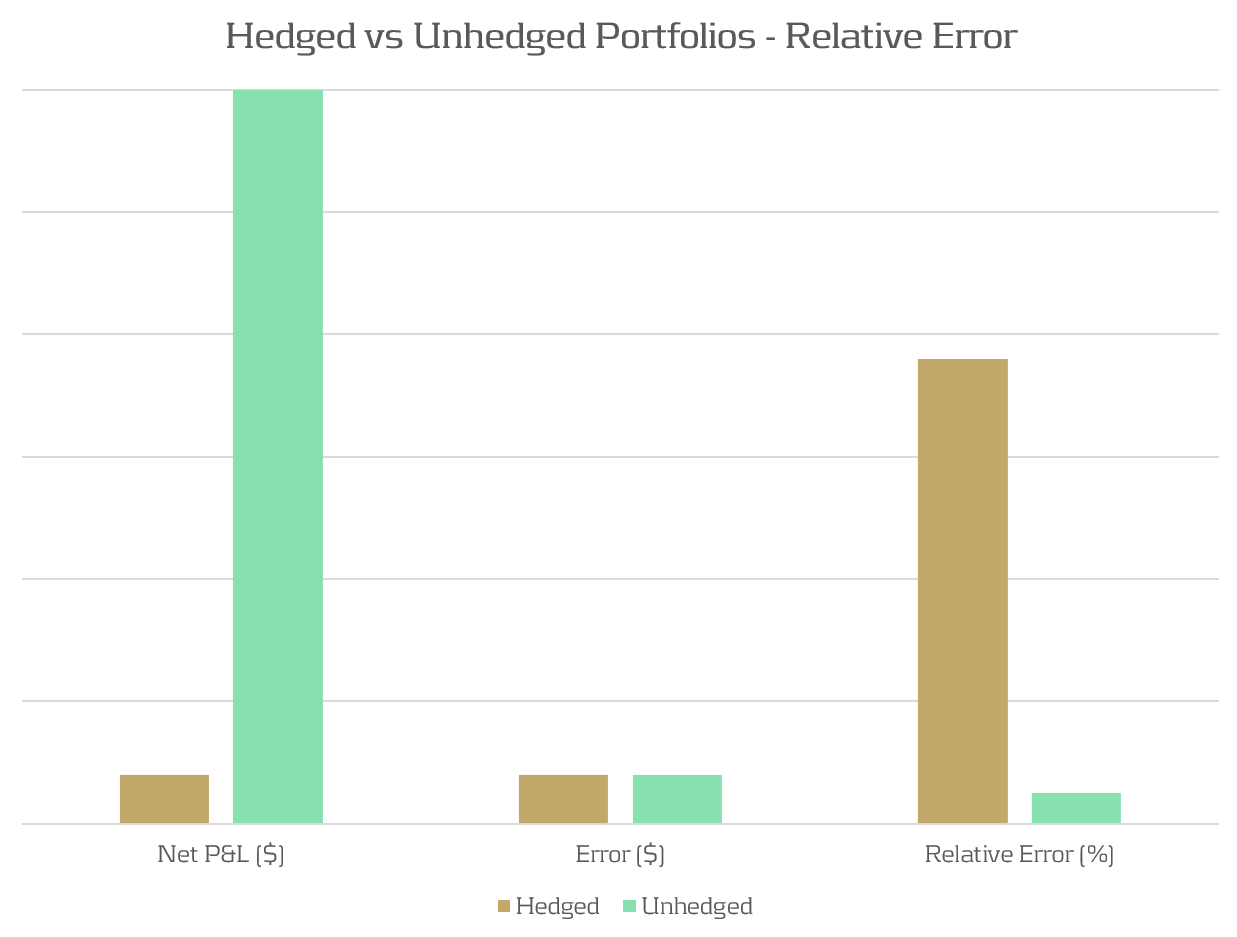

Due to modeling and data differences, we typically expect there to exist a small difference (error) between RTPLs and HPLs. For unhedged portfolios, the total P&L is typically much larger than this error, resulting in a small relative error. When portfolios are hedged, the total P&L of the portfolio is reduced, leading to a larger relative error than that of an unhedged portfolio. This is illustrated in Figure 1, which shows how for the same modeling error, a significantly different relative error can be observed, depending on the degree of hedging of the portfolios.

Figure 1: The relative P&L error can be significantly different between hedged and unhedged portfolios which have the same absolute error.

Demonstration: A delta-hedged option portfolio

Portfolio and simulation

To demonstrate the PLA hedging issue, we examine a simulated example of a desk with long put positions, hedged by a variable quantity of the underlying stock. In this example, the portfolio consists of 100 long puts and between 0 and 100 of the underlying stock as a hedge against the put positions.

To emulate the differences in pricing models between Risk and FO, a closed form solution is used to compute HPLs and a Monte Carlo pricing methodology is used for RTPLs. This produces a sufficiently small pricing error, such that the options and stock positions would comfortably pass the PLA test if they were held in separate portfolios. The P&Ls are obtained by repricing 250 scenarios of a Monte Carlo simulation of the underling risk factors.

The outcome

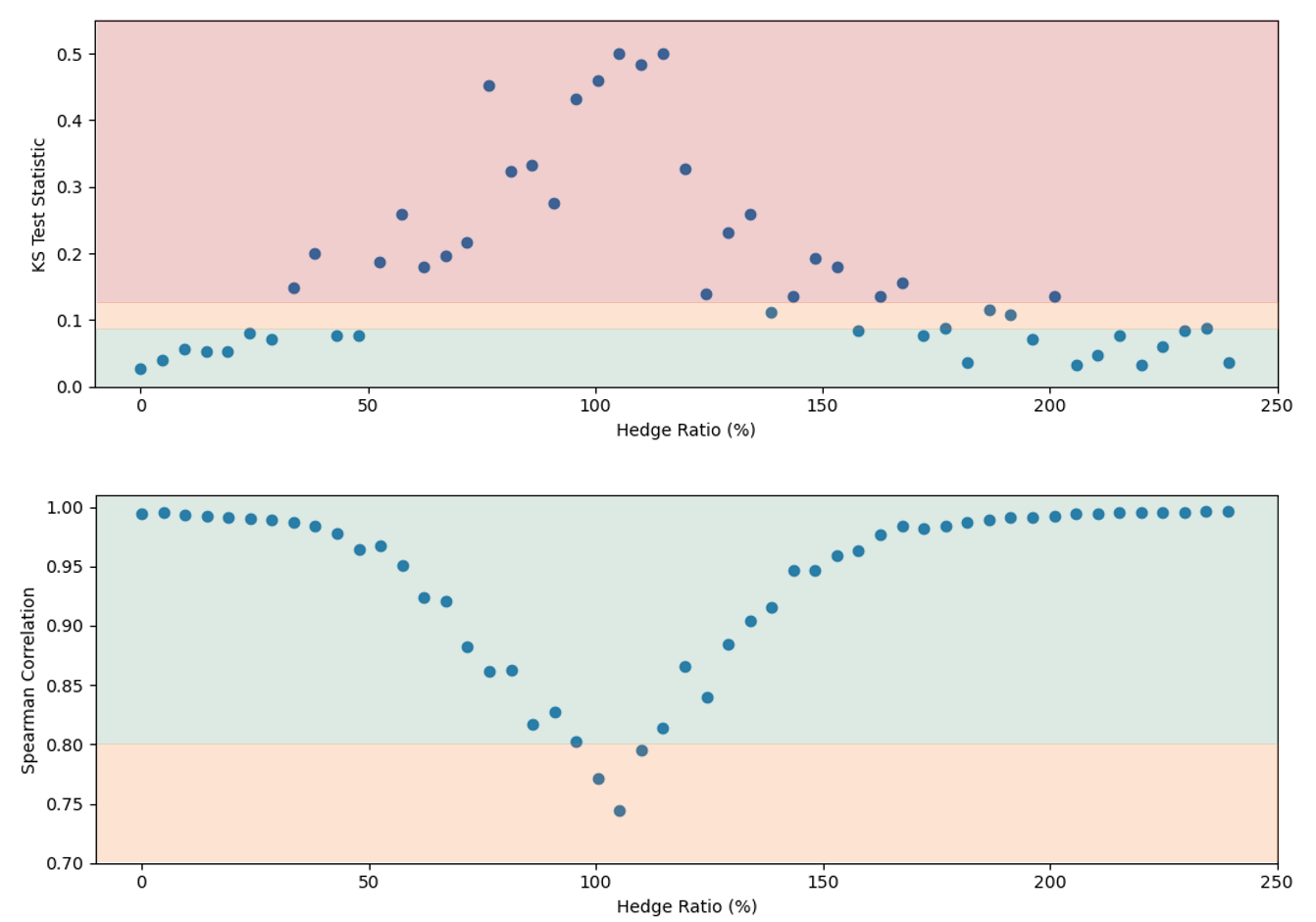

The results in Figure 2 show the PLA results for the two statistical tests against the total hedge ratio (the ratio between stock position delta and put position delta). The TLT zones are represented by the green, amber, and red shaded regions. This shows that the test statistics can vary quite considerably depending on the degree of hedging, with the KS test statistic entering the amber and red TLT zones for even a limited degree of hedging. The Spearman correlation is not as sensitive to the hedge ratio, but the statistic worsens as the hedging ratio approaches 100%.

Although the portfolio comfortably passes the PLA test when unhedged, it fails when hedged. Hence, quite surprisingly, hedging strategies used by banks to reduce risk may in fact be penalised by the regulator and increase capital requirements. Furthermore, failing desks would also need to satisfy 12-month PLA and backtesting requirements to return to the IMA.

Figure 2: The KS (top) and Spearman correlation (bottom) statistics for an example portfolio of 100 long puts and between 0 and 100 shares of the underlying stock. The hedge ratio is defined as the ratio between stock position delta and put position delta. The green, amber, and red shading represent the TLT zones.

Solutions for Hedged Portfolios

Reducing the impact of hedged portfolios

As demonstrated, some trading desks with well-hedged positions may find themselves losing IMA eligibility due to poor performance in the PLA test. However, the following strategies can be used to reduce the possibility of failures:

- Model Alignment: Ensure the modeling methodologies of risk factors and instrument pricing are consistent between FO and Risk.

- Data Alignment: Ensure that the data sourced for FO and Risk are aligned and are of similar quality and granularity.

- Risk Enhancements: Improve the sophistication of Risk pricing models to better incorporate the subtilities of the FO pricer. This may require pricing optimisations and high-performance computing.

- Proactive Monitoring: Develop ongoing monitoring frameworks to identify and remediate P&L issues early. We provide more insights on the development of PLA analytics here.

Will regulatory policy change be required?

It is clear that the current PLA regulation does not correctly account for the effects of hedging on the PLA test statistics, resulting in hedged portfolios being penalised. As banks move towards implementing FRTB IMA, regulators should reflect on the impact of the current PLA implementation and consider providing exemptions for hedged portfolios or, alternatively, a fundamental modification of the PLA test.

Zanders’ services

Zanders is ideally suited to helping clients develop models and implement FRTB workstreams. Below, we highlight a selection of the services we provide to implement, analyse, and improve PLA test results:

Conclusion

The PLA test under FRTB can disproportionately penalise well-hedged portfolios, forcing trading desks to adopt the more punitive SA. This effect is exacerbated by complex hedging strategies and non-linear instruments, which introduce additional model risks and potential discrepancies. To mitigate these issues, it is essential banks take steps to align their pricing models and data between FO and Risk. Implementing robust analytics frameworks to identify P&L misalignments is critical to quicky and proactively solve PLA problems. Zanders offers comprehensive services to help banks navigate the complexities of PLA and optimise their regulatory capital requirements.

For more information on this topic, contact Dilbagh Kalsi (Partner) or Hardial Kalsi (Manager).

The corporate landscape is being redefined by a plethora of factors, from new business models and changing regulations to increased competition from digital natives and the acceleration of the consumer digital-first mindset.

The new landscape is all about a digital real-time experience which is creating the need for change in order to stay relevant and ideally thrive. If we reflect on the various messages from the numerous industry surveys, it’s becoming crystal clear that a digital transformation is now an imperative.

We are seeing an increasing trend that recognizes technological progress will fundamentally change an organization and this pressure to move faster is now becoming unrelenting. However, to some corporates, there is still a lack of clarity on what a digital transformation actually means. In this article we aim to demystify both the terminology and relevance to corporate treasury as well as considering the latest trends including what’s on the horizon.

What is digital transformation?

There is no one-size-fits-all view of a digital transformation because each corporate is different and therefore each digital transformation will look slightly different. However, a simple definition is the adoption of the new and emerging technologies into the business which deliver operational and financial efficiencies, elevate the overall customer experience and increase shareholder value.

Whilst these benefits are attractive, to achieve them it’s important to recognize that a digital transformation is not a destination – it’s a journey that extends beyond the pure adoption of technology. Whilst technology is the enabler, in order to achieve the full benefits of this digital transformation journey, a more holistic view is required.

Figure 1 provides a more holistic view of a digital transformation, which embraces the importance of cultural change like the adoption of the ‘fail fast’ philosophy that is based on extensive testing and incremental development to determine whether an idea has value.

In terms of the drivers, we see four core pillars providing the motivation:

- Elevate the customer experience

- Operational agility and resilience

- Data driven real time vision

- Workforce enablement

Figure 1: Digital Transformation View

What is the relevance to corporate treasury?

Considering the digital transformation journey, it’s important to understand the relevance of the technologies available.

Whilst figure 2 highlights the foundational technologies, it’s important to note that these technologies are all at a different stage of evolution and maturity. However, they all offer the opportunity to re-define what is possible, helping to digitize and accelerate existing processes and elevate overall treasury performance.

Figure 2: Core Digital Transformation Technologies

To help polarize the potential application and value of these technologies, we need to look through two lenses.

Firstly, what are some of today’s mainstream challenges that currently impact the performance of the treasury function, and secondly, how these technologies provide the opportunity to both optimize and elevate the treasury function.

The challenges and opportunities to optimize

Considering some of the major challenges that still exist within corporate treasury, the new and emerging technologies will provide the foundation for the digital transformation within corporate treasury as they will deliver the core capabilities to elevate overall performance. Figure 3 below provides some insights into why these technologies are more than just ‘buzzwords’, providing a clear opportunity to elevate current performance.

Figure 3: Common challenges within corporate treasury

Cognitive cash flow forecasting systems can learn and adapt from the source data, enabling automatic and continuous improvements in the accuracy and timeliness of the forecasts. Additionally, scenario analysis accelerates the informed decision-making process. Focusing on currency risk, the cognitive technology is on a continuous learning loop and therefore continues to update its decision-making process which helps improve future predictions.

Moving onto working capital, these new cognitive technologies combined with advanced optical character recognition/intelligent character recognition can automate and accelerate key processes within both the accounts payables (A/P) and account receivables (A/R) functions to contribute to overall working capital management. On the A/R side, these technologies can read PDF and email remittance information as well as screen scrape data from customer portals. This data helps automate and accelerate the cash application process with levels exceeding 95% straight through reconciliation now being achieved. Applying cash one day earlier has a direct positive impact on days sales outstanding (DSO) and working capital. On the A/P side, the technology enables greater compliance, visibility and control providing the opportunity for ‘autonomous A/P’. With invoice approval times now down to just 10.4 business hours*, it provides a clear opportunity to maximize early payment discounts (EPDs).

Whilst artificial intelligence/machine learning technologies will play a significant role within the corporate treasury digital transformation, the increased focus on real-time treasury also points to the power of financial application program interfaces (APIs). API technology will play an integral part of an overall blended solution architecture. Whilst API technology is not new, the relevance to finance really started with Europe’s PSD2 (Payment Services Directive 2) Open Banking initiative, with API technology underpinning this. There are already several use cases for both Treasury and the SSC (shared service center) to help both digitize and importantly accelerate existing processes where friction currently exists. This includes real time balances, credit notifications and payments.

The latest trends

Whilst a number of these new and emerging technologies are expected to have a profound impact on corporate treasury, when we consider the broader enterprise-wide adoption of these technologies, we are generally seeing corporate treasury below these levels. However, in terms of general market trends we see the following:

- Artificial intelligence/machine learning is being recognized as a key enabler of strategic priorities, with the potential to deliver both predictive and prescriptive analytics. This technology will be a real game-changer for corporate treasury not only addressing a number of existing and longstanding pain-points but also redefining what is possible.

- Whilst robotic process automation (RPA) is becoming mainstream in other business areas, this technology is generally viewed as less relevant to corporate treasury due to more complex and skilled activities. That said, Treasury does have a number of typically manually intensive activities, like manual cash pooling, financial closings and data consolidations. So, broader adoption could be down to relative priorities.

- Adoption of API technology now appears to be building momentum, given the increased focus around real time treasury. This technology will provide the opportunity to automate and accelerate processes, but a lack of industry standardization across financial messaging, combined with the relatively slow adoption and limited API banking service proposition across the global banking community, will continue to provide a drag on adoption levels.

What is on the horizon?

Over the past decade, we have seen a tsunami of new technologies that will play an integral part in the digital transformation journey within corporate treasury. Given that, it has taken approximately ten years for cloud technology to become mainstream from the initial ‘what is cloud?’ to the current thinking ‘why not cloud?’ We are currently seeing the early adoption of some of these foundational transformational technologies, with more corporates embarking on a digital first strategy. This is effectively re-defining the partnership between man and machine, and treasury now has the opportunity to transform its technology, approach and people which will push the boundaries on what is possible to create a more integrated, informed and importantly real-time strategic function.

However, whilst these technologies will be supporting critical tasks, assisting with real-time decision-making process and reducing risk, to truly harness the power of technology a data strategy will also be foundational. Data is the fuel that powers AI, however most organizations remain heavily siloed, from a system, data, and process perspective. Probably the biggest challenge to delivering on the AI promise is access to the right data and format at the right time.

So, over the next 5-10 years, we expect the solutions underpinned by these new foundational technologies to evolve, leveraging better quality structured data to deliver real time data visualization which embraces both predictive and prescriptive analytics. What is very clear is that this ecosystem of modern technologies will effectively redefine what is possible within corporate treasury.

*) Coupa 2021 Business Spend Management Benchmark Report